ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 503

2.2 Profitability ratios

This category of ratios measures the performance of the company in terms of the

return (profit) earned on the capital employed in the business. These ratios are

relevant for measuring the success of management in using the resources under

their control. They also allow customers and suppliers to assess whether the

company has the ability to continue operating successfully in the future.

Return on (total) capital employed (ROCE)

The return on capital employed ratio measures profit before interest and tax with

the total capital employed in the business. It is therefore a measure of the success of

the company in making use of its invested capital.

%100

capitaldebt +reserves+capital Share

taxandinterest beforeProfit

×

Remember that when a ratio is calculated, it is important to compare ‘like with like’.

The figure above the line must be properly comparable with the figure below the

line. ‘Profit before interest and tax’ relates to the profit earned on all the capital of

the business, including its debt capital and any non-controlling interests in

subsidiaries.

The figure below the line should therefore include all equity capital (including non-

controlling interests) and all long-term debt capital.

Return on shareholders’ funds (ROSF)

The return on shareholders’ funds (ROSF) or return on shareholders’ capital (ROSC)

measures the return on the capital invested by shareholders. It measures how

efficiently the company is using the capital that only shareholders have provided, to

obtain profits.

In a company with no preference shares and no non-controlling interests, this ratio

is calculated as follows.

100%

reservescapitalShare

taxbeforeProfit

×

+

When a company has non-controlling interests or preference shares, you need to

decide on the most suitable method of calculating the ratio. Remember that the

figure above the line must be comparable with the figure below the line. For

example, if you are measuring the return on capital for equity shareholders in the

parent company, the most suitable ratio would be:

%100

companyparenttheofrsshareholdeequitytoleattributabreservescapitalShare

companyparenttheinrsshareholdeequitytoleattributabtaxProfit

×

+

after

Paper P2: Corporate Reporting (International)

504 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Using ROCE or ROSF

It is not necessary to calculate both these ratios. The ratio that you calculate

should be the ratio that is of the greatest interest to the particular user or user

group. For example, management may be most interested in ROCE, but an

equity investor would be interested in ROSF.

ROCE or ROSF could be compared to real interest rates that are currently

available to investors in the market. For example, if a company has a ROCE of

3% when interest rates of 5% are available in the bond markets, a shareholder

might be advised to consider selling his shares. However, it is important to

remember that bond yields are returns calculated from the market price of

bonds; whereas ROCE and ROSF are calculated from financial statements and

are not market rates of return.

Bank overdrafts might be included as part of capital employed in the ROCE

ratio, because many companies ‘roll over’ their overdraft facility and use it as

long-term funding. When a bank overdraft is large, the interest cost of the

overdraft might be high, and it would therefore be appropriate to include the

bank overdraft ‘below the line’ in capital employed, because the overdraft

interest is included ‘above the line’ in profit before interest and tax.

A company may be able to ‘manipulate’ its ROCE or ROSF ratios by using

accounting policies or financing strategies, such as:

− using operating leases or finance leases

− choosing to re-value non-current assets or choosing the historical cost model

− timing the acquisition of non-current assets or the timing of new financing so

as to have the minimal adverse impact on ROCE.

Gross profit percentage

The gross profit margin is the ratio of gross profit to sales income. Gross profit is

sales minus the cost of sales.

100%

Sales

profitGross

×

Analysing the gross profit margin can often provide useful information for users of

financial statements.

This ratio should normally remain fairly constant from one year to the next.

Even a fairly small change in the ratio might indicate that something of

significance has happened.

Variations between years may be attributable to

− a change in sales prices

− a change in sales mix

− a change in purchase/production costs

− an exceptional write-off of inventory

− exceptional expenses or lost revenues (such as the consequences of a strike

by employees).

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 505

Overhead percentage

Overhead percentage ratios measure the ratio of overhead costs to sales revenue.

The main overhead costs are administrative expenses and sales and distribution

costs.

100%

Sales

Overheads

×

Even when the gross profit margin is constant, the net profit margin may be affected

by changes in the overhead cost ratios.

An analysis of overhead costs is more meaningful if total overhead costs can be

analysed into variable overheads and fixed overheads

The ratio of variable overhead costs to sales revenue should remain constant

from one year to the next, unless something of significance happens (such as a

major increase in variable overhead costs)

The ratio of fixed overhead costs to sales revenue should decrease as the

company grows and increases its annual revenue. However, when a company

grows, fixed cost spending also increases, so the decline in the fixed costs/sales

ratio might not be ‘dramatic’ and substantial.

The overhead costs to sales ratios are affected by exceptional items, such as

company reorganisation and the cost of settlement of lawsuits/ legal disputes.

2.3 Efficiency ratios

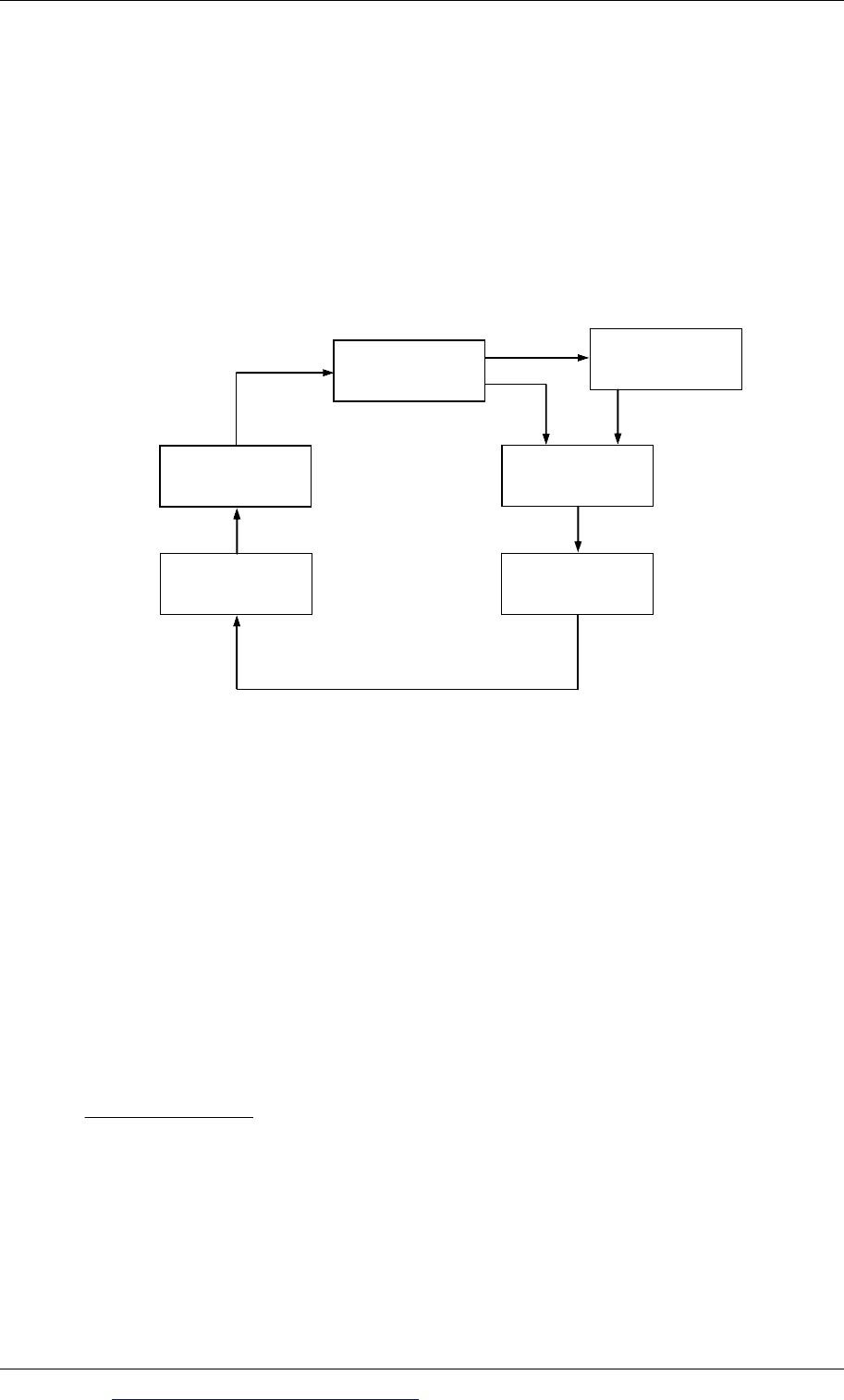

Cash flow is the lifeblood of an entity. Cash is needed to maintain operations by

paying suppliers and employees, and to allow the company to grow. Cash income

and spending can be controlled to some extent through management of the cash

operating cycle (management of ‘working capital’).

The operating cycle (also called the cash cycle) refers to the continuous cycle of

business activities, whereby an entity spends cash to acquire materials, labour and

other resources, and eventually recovers its cash (with a profit) by selling goods or

services to customers and collecting payment.

For a manufacturing entity, the operating cycle begins when the entity buys raw

materials on credit and turns the materials into finished goods. The finished goods

are then sold on credit, generating trade receivables. The entity then collects the

cash from the customers. The cash cycle is the average length of time between

paying cash to suppliers and receiving cash from customers.

Problems arise when cash income is not being generated by operations quickly

enough. When this happens, the entity may have difficulty with paying cash to its

suppliers. Alternatively, it needs to set aside much more capital than necessary for

working capital.

Poor working capital management and an inefficient cash cycle mean inadequate

cash flows. Examples of poor management include:

holding excessive levels of inventory

Paper P2: Corporate Reporting (International)

506 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

allowing customers extended periods of credit (not collecting receivables on

time).

When an entity ties up capital in excessive working capital (inventory and trade

receivables) its ROCE will be lower than it should be, and it may need to borrow

money to meet its obligations.

An entity with cash flow difficulties may be able to overcome its problems by

improving working capital management, without the need to go to a bank for a

loan, and without trying to take extra trade credit from suppliers.

Cash

Receivables

Finished goods

Raw materials

Work in

progress

Payables

Several working capital efficiency ratios are useful for assessing the efficiency of

working capital management and management of the operating cycle/cash cycle.

Lenders will also be interested in these ratios, because they may help to indicate any

problems with cash flow management that may affect the ability of an entity to

settle its current liabilities.

Inventory turnover

Inventory turnover is a measure of how quickly an entity uses its inventory. It is

also a measure of how slowly an entity uses its inventory, and how long items are

held in inventory before they are eventually used or sold.

Inventory turnover may be measured as ‘x times a year’.

Cos

t

o

f

sales

Average inventory

This shows the number of times the average level of inventory is sold in the year. A

low turnover indicates inefficient use of resources, because cash is tied up in

inventory. The slower inventory turnover, the greater the risk of obsolescence. A

high turnover indicates good inventory management. However, when inventory

turnover is too high, there could be ‘stock-out’ or ‘inventory-out’ problems.

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 507

It is also important to realise that the expected speed of inventory turnover varies

between different types of business. For example, a supermarket may expect a very

high inventory turnover (especially for fresh food items), whereas a car dealer’s

turnover will be much slower.

Inventory turnover may also be measured as an average number of days, rather

than as ‘x times a year’.

days365

salesofCost

inventoryAverage

×

This calculates the number of days a company takes to sell its average holding of

inventory. A short turnover period indicates good inventory management.

For a better understanding of inventory turnover, separate turnover ratios could be

calculated for:

raw materials

work in progress (the production cycle), and

finished goods

For an entity that has a seasonal business, with some months of high sales and some

months of low sales, it may be appropriate to calculate inventory turnover ratios at

different times of the year (for each season).

Receivables turnover

The receivables turnover ratio is usually measured in days. It is the average time

that it takes an entity to collect amounts due from customers. (It is sometimes called

‘debtor days’ or ‘days sales outstanding’.) An estimate for the receivables turnover

can be obtained from financial statements:

days365

salesCredit

sreceivabletradeAverage

×

The receivables turnover should be consistent with the industry average, and

should not be unreasonably long. Many entities give 30 days’ credit to their

customers, and sometimes more, perhaps as much as 90 days or even longer. The

ratio should therefore be interpreted with care. Even so, a high turnover ratio (a

long average receivables collection period) could indicate collection problems and

poor working capital management.

The ratio should ideally use credit sales ‘below the line’, but the financial

statements do not provide an analysis of sales into cash sales and credit sales.

Therefore total sales must normally be used, and this may produce an unrealistic

ratio.

The ratio can be compared to the normal credit period offered to customers by

the entity.

A change in the ratio from one year to the next may be due to:

Paper P2: Corporate Reporting (International)

508 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

− A change in settlement terms for credit customers, to encourage new

business

− the introduction of debt factoring, which will reduce the average receivables

collection period

− exceptional factors, such as one large new customer being offered extended

credit.

For an entity that has a seasonal business, with some months of high sales and some

months of low sales, it may be appropriate to calculate receivables turnover ratios at

different times of the year (for each season).

Payables payment period

The payables payment period is similar to receivables turnover, but it is the average

payment period to suppliers, rather than the average receivables collection period

from customers. It is normally measured in days.

days 365

purchasesCredit

payables tradeAverage

×

The figure above the line should be trade payables, and should exclude other

current liabilities, such as tax payable and interest payable. The figure below the line

should ideally be the figure for annual purchases on credit. However, this figure is

not available from the financial statements, and the figure for the annual cost of

sales should be used instead. However, this produces an estimate for the average

payment period that is ‘less accurate’.

A high ratio (long average payment period) might indicate efficient management,

because trade credit from suppliers is a form of free finance to fund the working

capital cycle. However, there may be situations when a long payables payment

period is a sign of poor working capital management or financial distress.

If an entity takes too long to pay its suppliers, and possibly fails to settle its

liabilities on time, relationships with suppliers could be damaged.

Taking a free credit period to settle liabilities may mean the company is losing a

prompt payment discount and so may indicate inefficient management.

A high ratio could also occur when the entity has insufficient cash to settle its

liabilities, and is therefore in some financial difficulty.

For an entity that has a seasonal business, with some months of high purchases and

some months of low purchases, it may be appropriate to calculate the average

payables payment ratios at different times of the year (for each season).

2.4 Short-term liquidity ratios

Liquidity means access to cash when it is needed. Short-term liquidity ratios are

used to assess the ability of an entity to have sufficient cash, normally from its

normal business cycle/cash cycle, to settle payments when they become due. The

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 509

ratios can be used together with information in the statement of cash flows to

analyse the liquidity (and cash flows) of the entity.

Current ratio

Liquidity comes from current assets, including cash. In the normal course of the

cash cycle, current assets such as trade receivables should produce cash in the near

future. The need for liquidity comes from the need to settle current liabilities.

The current ratio is simply a ratio that compares short-term sources of cash (current

assets) with short-term needs for cash (current liabilities).

sliabilitieCurrent

assetsCurrent

An ‘ideal’ current ratio varies between different industries. For example, companies

that operate supermarkets should have a very low current ratio, because they sell

many items quickly for cash, but take normal trade credit from suppliers. In other

industries, slow inventory turnover and long credit periods may be normal, so that

a typical current ratio for a well-managed company may be high.

As a very rough guide, an ‘ideal’ current ratio may be 1.5:1 or 2:1. A ratio of less

than 1:1 could indicate liquidity problems, because the entity might be unable to

obtain cash from normal business activities to settle its current liabilities.

It is important to monitor changes in the current ratio from one year to the next, to

assess whether liquidity is improving or getting worse.

Quick ratio (acid test ratio)

The current ratio includes inventory within current assets. For some entities,

inventory may take many months to sell and inventory turnover could be very

slow. In such cases, inventory is not a liquid asset and will not generate cash within

a fairly short period of time in order to pay off the current obligations due in the

next month or so.

The quick ratio or acid test ratio is similar to the current ratio, but it excludes

inventory from current assets.

sliabilitieCurrent

inventorylessassetsCurrent

By eliminating inventory, the quick ratio measures a worst-case-scenario. It can be

used to ask the question: Does the entity appear to have sufficient cash and near-

cash assets (including receivables) to provide the money to settle all current

liabilities on time?

‘Ideally’ the quick ratio should be about 0.8:1 to 1.0:1. (A high quick ratio might

indicate excessive holdings of cash!) However, the quick ratio in well-managed

entities can vary between companies in different industries.

Paper P2: Corporate Reporting (International)

510 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Notes on the current ratio and quick ratio

The following points might be helpful for interpreting an entity’s short-term

liquidity ratios:

A low ratio may indicate liquidity problems, particularly when the ratio is

significantly lower than in previous years.

However, a high ratio may indicate poor working capital management, due to:

− large amounts of capital tied up in inventory or receivables, or

− problems with debt collection (and so excessive receivables), or

− obsolete inventory that has not yet been written off, or

− excessive amounts of cash in the bank, earning low rates of interest (or

possibly no interest at all).

You should consider the main elements of the short-term liquidity ratios –

inventory, receivables, cash (or bank overdraft) and trade payables, possibly

using the working capital efficiency ratios. This may help you to assess whether

liquidity is either too low or too high.

Remember that as a general guide, a ‘normal’ current ratio should be 1.5:1 (quick

ratio 0.8:1), but this will depend on the industry of the entity. For example, a

house builder will have very high levels of finished goods and work in progress

and so a higher figure would be expected.

If the liquidity ratios seem very low, you may need to consider whether the

entity can obtain cash from other sources, if needed, to settle short-term

liabilities. For example, an entity may have an unused (‘committed’) overdraft

facility that it can use in case of need.

2.5 Long-term solvency ratios

‘Gearing’ examines the financing structure of a business and indicates to

shareholders the level of financial risk to which the company is exposed because of

its long-term capital structure.

A company finances its net assets with a combination of equity and reserves and

long-term debt. An entity is ‘high geared’ when a large proportion of its long-term

capital is in the form of debt. High financial gearing is seen as a high-risk strategy,

because earnings (and dividends) are more sensitive to changes in the company’s

performance (profit before interest and tax) when gearing is high.

An assessment of long-term solvency ratios is therefore relevant to investors and

lenders. These ratios, and changes in the ratios over time, can help them to assess

the credit risk in their investment.

Example

A company has the following long-term capital:

$400,000 $1 equity shares

$400,000 10% debt capital

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 511

The interest on the debt capital is fixed. A fall in annual profit before interest and tax

(PBIT) could affect its ability to pay the interest. Any fall in PBIT would also affect

the earnings available for distribution to the equity holders.

The following table shows how EPS – and solvency – may be affected by a decline in

PBIT, for a company with fairly high gearing. A tax rate of 30% is assumed.

Year1‐50%‐75%

$ $ $

PBIT 100,000 50,000 25,000

Interest (40,000) (40,000) (40,000)

––––––––––––––––––– ––––––––––––––––––– –––––––––––––––––––

Profit/(loss)beforetax 60,000 10,000 (15,000)

Taxat30% (18,000) (3,000) 4,500

––––––––––––––––––– ––––––––––––––––––– –––––––––––––––––––

Earnings 42,000 7,000 (10,500)

––––––––––––––––––– ––––––––––––––––––– –––––––––––––––––––

Shares 400,000 400,000 400,000

EPS $0.105 $0.0175 $(0.026)

In year 1 the company makes $100,000 resulting in earnings per share (EPS) to the

equity holders of 10.5 cents. If the PBIT of the company drops by 50% to $50,000 the

EPS drops by 83.3% from 10.5 cents to 1.75 cents.

If the performance drops by 75% the entity makes a loss and the EPS is negative.

A fall in EPS will affect the share price. In addition, a company with high gearing is

often seen by investors as a company with ‘volatile’ earnings, and the shares of

these companies often trade on a lower P/E multiple (a lower P/E ratio) than

companies with a lower gearing.

Gearing ratio

The gearing ratio (or leverage ratio) is usually calculated as follows:

100%

EquityDebt

Debt

or

Equity

Debt

×

+

Debt = Loans + Preference shares

Equity = Equity share capital + reserves + non-controlling interest

Notes on financial gearing

The following issues might be relevant if you are required to analyse the financial

gearing of a company:

Paper P2: Corporate Reporting (International)

512 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

A highly geared company, with a substantial proportion of its capital in the form

of debt, is seen by investors as ‘more risky’. Higher risk means that investors are

likely to expect a higher return from their investment, as compensation for the

higher risk.

High gearing is acceptable if it is accompanied by stable annual profits (PBIT) or

increasing profits.

A highly-geared company may find it more difficult to raise additional debt

capital, because lenders will demand either security for their loans/bonds, or

will demand a much higher yield/interest rate.

Gearing, measured from the figures in the financial statements, is affected by

accounting policy decisions such as the revaluation of non-current assets and the

choice between finance leases and operating leases.

In recent years, at least until the ‘credit crunch’ in 2008, some companies

deliberately increased their financial gearing by borrowing more. Some companies

borrowed and used the money to buy back and cancel equity shares. The reasons for

this have been:

a confidence that the annual profits (PBIT) of the company will be stable or will

increase, and

the comparatively low cost of debt compared with the cost of equity.

Interest rates were low, and there is tax relief on interest payments. Higher gearing

meant that if profits before interest continued to rise, EPS would rise at an even

faster rate. Increasing financial gearing was therefore a way of increasing EPS.

The ‘credit crunch’ from 2008 meant that banks became much more reluctant to

lend, and some companies found that their access to debt finance was severely

restricted. To raise finance, increasing equity and reducing gearing (by issuing new

shares or by retaining profits) became necessary – and the rate of business growth

declined.

Interest cover

The interest cover ratio measures the ability of a company to meet its obligations to

pay interest on debt. The assumption is that a company should be able to pay

interest charges out of its profits. The ratio therefore compares profit before interest

and tax with the annual interest charges.

Interest

interestbeforeProfit

It is a measure of the security of the interest payments. A high interest cover

suggests a sensible financing structure (although a very high ratio might suggest

that gearing could safely be increased, and that the company should borrow more

low-cost debt instead of higher-cost equity).

An interest cover of 2 times or less generally indicates that the company might have

difficulty paying its interest if there is a fall in its profits. (An interest cover ratio of

less than three times may also be considered ‘risky’, especially if the ratio is lower

than in previous years.)