ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 19: Specialised entities

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 493

ED 2009/8: Rate regulated activities

Background

Proposed guidance

3 ED 2009/8 Rate regulated activities

3.1 Background

Many governments have established regulatory mechanisms and bodies to govern

the provision of essential services such as electricity, gas etc. The regulatory

mechanisms often provide price protection to consumers whilst allowing companies

to earn a fair return.

Prices are often set in advance, based on estimated costs and volumes and a target

rate of return. The regulatory mechanism might also allow for the later

determination of actual costs and volumes. A company might then be allowed to

recover costs incurred through future rate increases. Alternatively, a company

might be required to return amounts to the consumer through future rate decreases.

This gives rise to gives rise to rights or obligations which may qualify as assets or

liabilities.

Illustration

X Plc is a regulated gas supplier. Flooding has caused significant damage to its

infrastructure. The regulatory mechanism allows X Plc to recover the costs of flood

damage costs from consumers over the five subsequent annual periods.

This right is clearly of benefit to X Plc. However it is unlikely that it would satisfy

the definition of an asset under existing IFRS.

In July 2009 the IASB issued an ED to address this issue. The ED contained

proposals to allow for assets and liabilities that arise from some rate-regulated

activities to be recognised under IFRS.

3.2 Proposed guidance

The ED clarifies in what circumstances regulated entities should recognise assets or

liabilities as a result of rate regulation, defines regulatory assets and regulatory

liabilities, sets out criteria for their recognition, specifies how they should be

measured and specifies disclosures.

The ED applies only to rate-regulated activities that meet the following two criteria:

an authorised body is empowered to establish rates that bind customers

the price established by regulation (the rate) is designed to recover the specific

costs the entity incurs in providing the regulated goods or services and to earn a

specified return (cost-of-service regulation).

Paper P2: Corporate Reporting (International)

494 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The ED requires an entity:

to recognise a regulatory asset or regulatory liability if the regulator permits the

entity to recover specific previously incurred costs or requires it to refund

previously collected amounts and to earn a specified return on its regulated

activities by adjusting the prices it charges its customers

to measure a regulatory asset or regulatory liability at the expected present value

of the cash flows to be recovered or refunded as a result of regulation, both on

initial recognition and at the end of each subsequent reporting period

to present current and non-current regulatory assets and regulatory liabilities,

without offsetting, separately from other assets and liabilities.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 495

Paper P2 (INT)

Corporate Reporting

CHAPTER

20

Performance measurement

Contents

1 Users of financial statements

2 Financial measures of performance

3 Financial ratios and examination technique

Paper P2: Corporate Reporting (International)

496 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Users of financial statements

Users and their information needs

Limitations of the financial statements

The information needs of management

Ratio analysis as a tool

1 Users of financial statements

1.1 Users and their information needs

The IASB Framework outlines seven different groups of users of financial

statements. Each user group has different information needs, but as a general rule

financial statements prepared in accordance with IFRSs should provide all user

groups with most of their needs.

The table below lists the user groups, indicates the information that they require

from published reports and accounts, and suggests which items in the financial

statements will be of most interest to each group.

User Information needs Items of interest

Investors/

potential

investors

Risks and returns relating to

their investment

Security of dividend

payments

Information to make

decisions about buying,

selling or holding shares

Future growth prospects.

Trend analysis: changes in

revenue, costs and profits

over the past few years

Dividend cover

Events and

announcements after the

reporting period

Share price

Corporate governance

reports. Narrative business

review.

Employees Stability of the company (job

security and job prospects)

Information about the

company’s ability to pay

bonuses or higher salaries.

Profitability and cash

position

Increases in salaries (%)

relative to increases in

profit and dividends

Directors’ remuneration

Lenders

(banks,

bondholders)

Whether the entity has

sufficient cash flow to repay

loans

The entity’s ability to pay

interest

The adequacy of collateral/

security for loans and bonds

Cash flow

Total borrowing by the

entity: financial gearing

Interest cover

New charges created over

the entity’s assets

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 497

Suppliers The entity’s ability to settle

its liabilities

The entity’s ability to

survive and continue as a

customer

Net current assets

Growth record

Customers

The entity’s ability to

survive and continue as a

supplier

Growth record

Cash flow

Government The entity’s contribution to

the economy

Regulation of activities

Taxation

Obtaining government

statistics

Revenue and profit

Market share

General public Environmental and social

awareness

Contributions to the local

economy

Environmental and social

reports

Directors’ report

Narrative business review

Note

Management are not included as a user group because they should have access to

much more detailed information about the company’s financial position and

performance, from internal reports and budgets.

1.2 Limitations of the financial statements

The financial statements provide a starting point for understanding the entity’s

performance. However they have a number of limitations, which are explained

below.

Historical information

Published accounts are historical in nature, and report the past performance of the

company. Past performance does not guarantee future performance. However, there

is very little information in the audited financial statements about the future

prospects of the company.

A Chairman’s statement, a directors’ report and a business review or Operating and

Financial Review are produced by companies in some countries. These narrative

reports often include information about changes to the business and the outlook for

the next few years. However, these often provide insufficient information and can

not always be relied on to provide an ‘unbiased’ view of the company’s future

prospects.

Users of financial statements, particularly shareholders and other investors, may use

trend analysis to analyse a company’s performance over the past few years, and

predict future performance from past trends. Stock market announcements by a

company and press releases by the company to the media, together with general

economic information, can also be used to try to predict future performance.

Paper P2: Corporate Reporting (International)

498 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The effect of inflation

Inflation affects the information in financial statements prepared under the

historical cost convention. When the rate of inflation is fairly high, information in

the financial statements may be unreliable.

For many companies, many of the assets in the statement of financial position

are undervalued because in a period of fairly high inflation the replacement cost

of the assets will be substantially higher than their carrying values (at net book

value, based on historical cost).

IAS 16 and IAS 39 allow certain assets to be re-valued in the statement of

financial position whilst others are carried at historical cost.

In a period of inflation, the reported profit is also misleading when the historical

cost convention is applied. The reported profit does not take account of the higher

cost of replacing inventory that has been sold or non-current assets that have

reached the end of their useful life.

Access to information

Most users will not have access to the forecasts and projections produced by

management as part of their monthly management accounts. This information

would be invaluable to investors who want to assess the future prospects of the

company.

Some users of financial information may be in a position to ask a company to

provide this information. For example:

a bank will want to see the cash flow forecasts and business plans of a company

before agreeing to lend it money

the government may have a statutory right to demand detailed financial

information from a company, for example about its sales, in order to compile

national statistics.

Insufficient detail

IFRSs specify the disclosures of information that entities should provide in their

financial statements.

Much of the detailed information is aggregated into a total figure, and companies

generally provide only the minimum level of disclosure required by IFRSs. Some

international accounting standards require the disclosure of details, such as IFRS 5

Non-current assets held for sale and discontinued operations. These help with the

interpretation of performance, but the disclosures are still not given in sufficient

detail to satisfy the needs of all users.

Some standards include voluntary disclosure requirements. For example, IAS 7

recommends analysis of operating cash flows under the direct method. However,

most companies choose not to provide any more information than is absolutely

necessary, and most use the indirect method.

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 499

Creative accounting

Over recent years, the rules in the IFRS accounting framework have been

strengthened, and the opportunities for ‘window dressing’ of the financial

statements have been reduced. Even so, there are still some opportunities for

companies to ‘manipulate’ the figures in their financial statements, to improve their

reported position and their financial ratios. This is known as creative accounting.

For example, some accounting standards still allow a choice of accounting

treatment. For example, IAS 16 allows the use of the cost model or revaluation

model for non-current assets. A company will be tempted to select the policy that

shows the ‘best’ results.

There are also a number of areas where accounting standards provide no rules or

where the rules on the accounting treatment of an item are unclear. This allows

companies to design their own accounting treatment, until such time as rules are

introduced or strengthened.

Even when standards do exist, the management of entities may be allowed to use

their judgement when applying an accounting policy or making an estimate. For

example, judgement is needed to decide whether the conditions have been met for

capitalisation of development costs (IAS 38).

Scope of the audit

In addition to the financial statements, the annual report and accounts published by

companies include other information that may be of relevance to users. This

information may include:

an operating and financial review, or a business review

a Chairman’s statement

a directors’ report

a corporate social responsibility report (or social and environmental report).

However, many companies publish an annual corporate social responsibility

report as a separate document.

The company itself is able to decide the content of these reports and the amount of

detail that they provide. As a general rule, a company will only want to publish

positive news and not the ‘bad news’. The information in these reports is not subject

to a full audit and so the audit opinion does not extend to them. (Auditors are

required to read the content of the reports, to ensure that it does not undermine the

credibility of the financial statements. If problems are found, the auditors will seek

adjustment from management but if this refused there is generally little that the

auditor can do.)

Note: In the EU, the recent EU accounts modernisation directive introduced a

requirement for listed companies to produce an annual business review. National

governments will give guidance or establish rules about what this review should

contain, but it will not be subject to audit.

Paper P2: Corporate Reporting (International)

500 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

1.3 The information needs of management

The management of a company needs much more information about the financial

performance and position of their company than other user groups. They need

reports more regularly, and often they need access to information immediately

through on-line IT systems. They also need information in sufficient detail and

suitably analysed.

Management have access to this amount of information and detail through the

reporting systems of the company, and in budgets, forecasts, business plans,

strategy documents and monthly management accounts. Detailed reports on

inventory levels, slow-moving items and the ageing of outstanding receivables

should also be available from the management information systems of the company.

However, the quality of the management information is only as good as the system

that provides it. Poor management information (information that is inaccurate and

unreliable, provided too late or irrelevant) can lead to wrong decisions being made

by management.

The management of an entity may also have access to information about

competitors, such as market share statistics (if these are collected by industry

regulators or the government). The financial statements of competitors are also a

valuable source of information about their profit margins, sales growth and possible

weaknesses.

1.4 Ratio analysis as a tool

It is difficult to assess a company’s financial performance by analysing the financial

results for one year. Better information is obtained by making comparisons with

financial performance in the previous year, or perhaps over several periods (trend

analysis).

For example, if a company’s revenue has increased by 15%, it might be expected

that gross profit should also increase by at least 15%, and that receivables should

increase by 15%. To sustain the growth in operations, some increase in non-current

assets and inventory levels – perhaps a 15% increase – should also be expected.

Ratio analysis is a key tool used for performance analysis, because ratios summarise

financial information, often by relating two or more items to each other, and they

present financial information in a more understandable form. Ratios also identify

significant relationships between different figures in the financial statements.

For example, knowing that the profit of a company is $50,000 is not particularly

useful information on its own, because the expected amount of profit should be

dependent on the size of the business and the amount of its sales turnover. If the

company generated a profit of $50,000 from $150,000 of sales, then it has performed

well. However, if a profit of $50,000 has been made from sales of $5 million, then the

profit level is much weaker. The profit margin (the ratio of profit to sales) is a basic

and widely-used ratio for analysing the strength of a company’s financial

performance.

Chapter 20: Performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 501

A ratio on its own does not provide useful information. Ratios are useful because

they provide a basis for making comparisons. Comparisons might indicate that

performance or the financial position is better or worse than it should be, or is

getting better or worse than in the past.

For example, suppose that a company measures its profit margin in the current year

as 20%. Is this good or bad? To evaluate performance, the current year profit margin

of 20% should be interpreted, by comparing it with:

last year’s profit margin, or the company’s profit margin for the past few years

the budgeted profit margin (available to investors, perhaps, through company

announcements)

the industry average (the average profit margin for companies in the industry)

the profit margin reported by individual competitors.

For example, if the budgeted profit margin was 25%, an actual profit margin of 20%

might suggest that management have under-performed in the period.

Note that a ratio does not explain why any under-performance or out-performance

has occurred. Ratios are used to indicate areas of good or weak performance, but

management then have to investigate to identify the cause.

Example

A company achieved a profit margin of 6% in the year just ended. This was less than

the budgeted profit margin of 10%, and less than the profit margin in the previous

year, which was 8%.

The actual profit margin of 6% indicates disappointing performance, but

management should investigate the cause or causes. For example, they might find

that any of the following reasons might explain the low profit margin:

Increased competition has forced down sales prices and so reduced profit

margins.

Advances in technology have lowered costs but prices have come down even

more.

Raw material costs have risen and the higher costs could not be passed on to the

customers.

There have been higher employment costs due to pay rises for manufacturing

employees, but these could not be passed on to the customers.

The company buys most of its supplies from foreign countries, and adverse

movements in exchange rates for its purchases have increased costs and reduced

profit margins.

There has been a change in the company’s sales mix, and the company has sold a

larger proportion of cheaper and lower-margin products than expected.

Paper P2: Corporate Reporting (International)

502 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Financial measures of performance

Categories of financial ratios

Profitability ratios

Efficiency ratios

Short-term liquidity ratios

Long-term solvency ratios

Investor ratios

Limitations of financial ratios

2 Financial measures of performance

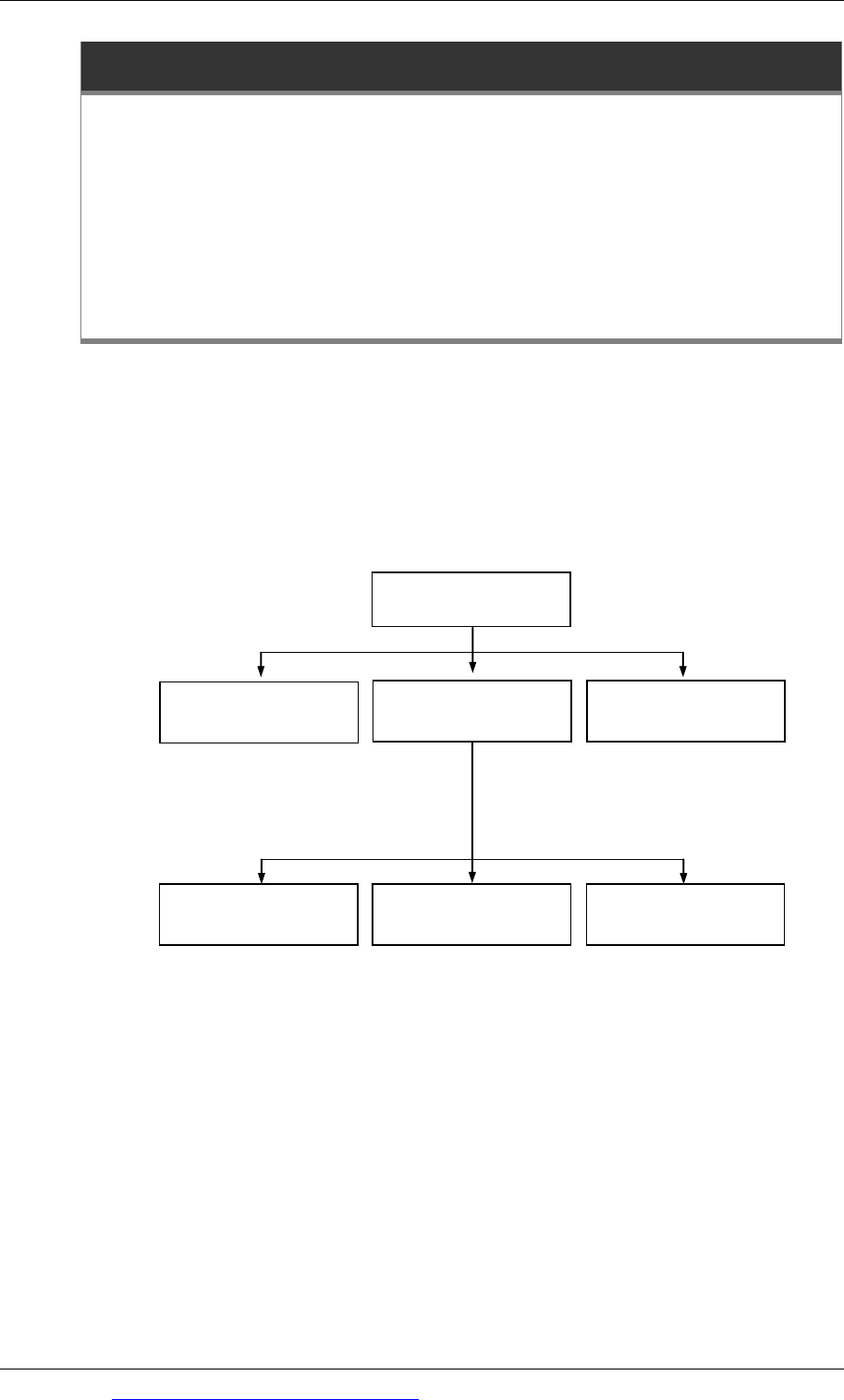

2.1 Categories of financial ratios

The basic financial ratios should already be familiar to you. Ratios can be divided

into five categories:

Financial position

ROCE

ROSF

Gross profit margin

Overheads %

Ratios

Profitability Efficiency

Inventory turnover

Receivables turnover

Payables period

Short-term liquidity

Long-term solvency

Investor ratios

Current ratio

Quick ratio

Gearing

Interest

EPS

PE

Dividend yield

Dividend cover

The main ratios will be considered in more detail. For the purpose of your

examination, you need to know how to calculate each ratio, but you must also

understand why each ratio, or each category of ratios, might be of particular interest

to a specific user group.

An examination question may ask you to provide an analysis of financial statements

for a particular user. It will not tell you which ratios to calculate. Instead, you will

have to decide for yourself which ratios may provide useful information for that

user. Therefore you should learn to identify and select the appropriate ratios for

each user group, and then analyse what the ratio appears to show, from the point of

view of that user.