ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 523

Paper P2 (INT)

Corporate Reporting

CHAPTER

21

Other issues

Contents

1 Convergence with IFRS and improvements to

IFRSs

2 First-time adoption of IFRS

Paper P2: Corporate Reporting (International)

524 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Convergence with IFRS and improvements to IFRSs

Convergence with IFRS: background

Advantages and disadvantages of harmonisation

Improvements in IFRSs: 2008 exposure draft

1 Convergence with IFRS and improvements to IFRSs

1.1 Convergence with IFRS: background

IAS 1 Presentation of Financial Statements states that ‘An entity whose financial

statements comply with IFRSs shall make an explicit and unreserved statement of

such compliance in the notes (to the financial statements). Financial statements shall

not be described as complying with IFRSs unless they comply with all the

requirements of IFRSs.’

The IASC is not able to force countries to adopt IFRS and so it has been left to

individual countries to decide to what extent business entities should be required to

use IFRS. Within the European Union (EU), all companies listed on an EU stock

market were required to use IFRSs when preparing their group accounts for

financial periods beginning on or after 1 January 2005. Therefore, the first set of IFRS

accounts produced by these companies was for the financial year to 31 December

2005 (or their first year-end date after 31 December 2005).

The EU did not want to transfer all authority for the implementation of accounting

standards to the IASB. It therefore introduced an endorsement mechanism. All

IFRSs must be reviewed by the EU before they are approved for use by listed

companies within the EU. To date, all IFRSs have been adopted with the exception

of certain parts of IAS 39.

Only listed EU groups are required to use IFRS. The decision for all other entities

has been left to the individual member states of the EU. In the UK, for example, all

companies are permitted to use international accounting standards for financial

periods beginning on or after 1 January 2005, in both individual company accounts

as well as in consolidated accounts. Therefore non-listed companies and the

individual companies within listed groups have the choice to move to IFRS or to

continue using UK accounting standards.

The US has also embrace IFRSs. There is currently a project between the IASB and

the US standards setter, the FASB, for convergence of IFRSs with US GAAP. The

two accounting boards have a short-term convergence project which has covered

topics including impairment, research and development, borrowing costs, segment

reporting, government grants and investment properties. Already, the IASB issued

IFRS 8 Segment reporting, which is based on the equivalent US standard.

Other areas that are under discussion are business combinations, consolidations, fair

value measurement, liabilities and equity, performance reporting, revenue

recognition and retirement benefits. For many of these topics that IASB has issued

discussion papers to amend the current treatment and harmonise with US GAAP.

Chapter 21: Other issues

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 525

This is a long term project which will continue over the next few years.

1.2 Advantages and disadvantages of harmonisation

There are some strong arguments in favour of the harmonisation of accounting

standards in all countries of the world, and in particular for the convergence of US

GAAP and IFRSs. However, there are also some arguments against harmonisation -

even though these are probably not as strong as the arguments in favour.

Advantages of harmonisation

1 Investors and analysts of financial statements can make better comparisons

between the financial position, financial performance and financial prospects of

entities in different countries. This is very important, in view of the rapid growth

in international investment by institutional investors.

2 For international groups, harmonisation will simplify the preparation of group

accounts. If all entities in the group share the same accounting framework, there

should be no need to make adjustments for consolidation purposes.

3 If all entities are using the same framework for financial reporting, management

should find it easier to monitor performance within their group.

4 Global harmonisation of accounting framework may encourage growth in cross-

border trading, because entities will find it easier to assess the financial position

of customers and suppliers in other countries.

5 Access to international finance should be easier, because banks and investors in

the international financial markets will find it easier to understand the financial

information presented to them by entities wishing to raise finance.

Disadvantages of harmonisation

1. National legal requirements may conflict with the requirements of IFRSs. Some

countries may have strict legal rules about preparing financial statements, as the

statements are prepared mainly for tax purposes. Consequently, laws may need

re-writing to permit the accounting policies required by IFRSs.

2. Some countries may believe that their framework is satisfactory or even superior

to IFRSs. This has been a problem with the US, although currently is not as much

of an issue as in the past.

3. Cultural differences across the world may mean that one set of accounting

standards will not be flexible enough to meet the needs of all users.

Additionally, there are issues on the implementation of IFRS to consider. For some

entities, they will need to amend computer and accounting systems to deal with

differing formats of accounting statements and different recognition methods of

assets and liabilities.

There may an impact on accounting ratios as assets and liabilities are restated in

accordance with IFRSs. For example, a company with significant development costs

will have to capitalise these in accordance with IAS 38. In the previous jurisdiction

they may have been able to write them off as an expense. This increase in assets will

Paper P2: Corporate Reporting (International)

526 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

affect the return on capital employed ratio. Any other performance ratios that

change may affect the analysts’ view of performance and could affect internal

performance measures such as profit related pay. Analysts will need to be informed

about the changes so they can continue to assess the performance of the business.

Additionally, employee performance plans may need to be amended so there is no

change in the underlying nature of the bonus scheme. An entity may also need to

look at the need for additional staff training.

1.3 Improvements in IFRSs: 2008 exposure draft

The IASB issued an exposure draft in 2008 entitled ‘Improvements to IFRSs’ and

with a sub-title ‘Proposed Amendments to International Financial Reporting

Standards’.

The exposure draft (ED) was issued as part of the annual improvements project of

the IASB, and similar EDs may well be issued in the future with a similar purpose.

The purpose of the ED was to provide a ‘streamlined process’ for dealing with a

number of non-urgent but necessary amendments to a number of different IFRSs. In

other words, the purpose of the ED was to set out a number of proposed minor

changes to several IFRSs and to introduce the changes if the response to the ED was

favourable.

This avoided the need for issuing a separate ED for each IFRS, with each ED

containing minor proposed changes.

The IFRSs for which minor changes were proposed were:

IFRS 2

IFRS 5

IFRS 8

IAS 7

IAS 18

IAS 38

IAS 38

IAS 39.

For example the proposed change to IAS 7 Statement of cash flows was to specify that

if expenditure is incurred with the object of generating future cash flows, but the

expenditure does not create an asset, the cash flow should be included in cash flows

from operating activities and should not be included in investment cash flows.

The proposed amendment to IFRS 5 was to include a minor clarification about the

required disclosures in the financial statements relating to non-current assets held

for sale.

For the purpose of the P2 examination, you should be prepared to discuss the

nature of this type of exposure draft, and the benefit of a streamlined process’ for

combining minor amendments to different IFRSs into a single exposure draft.

Chapter 21: Other issues

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 527

First-time adoption

IFRS 1: First-time adoption

Opening statement of financial position of a first-time adopter

Opening IFRS statement of financial position: exemptions from IFRSs

Presentation and disclosure by a first-time adopter

2 First-time adoption

2.1 IFRS 1: First-time adoption of International Reporting Standards

A first-time adopter of IFRSs is an entity that presents IFRS financial statements for

the first time, and fully complies with the requirements of IFRSs.

The special requirements for a first-time adopter are set out in IFRS 1.

A first-time adopter must adjust its statement of financial position produced

under ‘local GAAP’ to a statement of financial position produced using IFRSs.

This adjustment should be made by ‘retrospective application’ of the IFRSs.

In order to make adjustments to move from a statement of financial position

prepared under local GAAP to a statement of financial position prepared with

IFRSs, a number of prior year adjustments must be made for all the accounting

policy changes. These adjustments are made in the financial statements by

adjusting the opening reserves in the first-time adopter’s opening IFRS

statement of financial position. These adjustments are usually made to the

accumulated profits reserve (retained profits reserve).

2.2 Opening statement of financial position of a first-time adopter

The retrospective application of IFRSs means that adjustments are made to the first-

time adopter’s opening statement of financial position. This is the entity’s statement

of financial position at the date of transition to IFRSs.

IFRS 1 defines the date of transition to IFRSs as ‘the beginning of the earliest period

for which an entity presents full comparative information under IFRS in its first

IFRS financial statements.’

IFRS 1 also states that an entity must use the same accounting policies in its opening

IFRS statement of financial position and throughout all the financial periods

presented in its first IFRS financial statements. These should be the IFRSs that apply

as at the reporting date for the first IFRS financial statements (and any previous

versions of IFRSs that may have applied at earlier dates should not be used).

Paper P2: Corporate Reporting (International)

528 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company was a first-time adopter of IFRS and prepared its first IFRS financial

statements for the year to 31 December 2005. In its financial statements, it prepared

comparative financial information for the previous financial year.

The previous financial year is the year to 31 December 2004.

The date of transition to IFRS is the beginning of this period, which is 1 January

2004.

The opening IFRS statement of financial position of this first-time adopter is

therefore 1s January 2004. The adjustments made by retrospective application of

IFRSs must therefore be made to a statement of financial position as at this date.

However, the entity is not required to present this opening IFRS statement of

financial position in its financial statements for the year to 31 December 2005. It is

only required to present its normal comparative information for the previous

financial year, although the comparative information is prepared using IFRSs for the

year to 31 December 2004.

The IFRSs used to prepare all the information for the first IFRS financial statements

should be the IFRSs that apply at 31 December 2005.

2.3 Opening IFRS statement of financial position: exemptions from IFRSs

The general rule in IFRS 1 is that in the opening IFRS statement of financial position,

a first-time adopter must:

recognise all assets and liabilities whose recognition is required by IFRSs

not recognise assets or liabilities if IFRSs do not permit such recognition

re-classify items recognised under the previous GAAP as one type of asset,

liability or component of equity if IFRSs require that they should be classified

differently

apply IFRSs in measuring all assets and liabilities.

However, IFRS 1 lists a number of exemptions where these general rules should not

be applied (or need not be applied).

A first-time adopter may elect to use one or more available exemptions from the

application of IFRSs. (One of these is an exemption that allows an entity to

choose to use a ‘deemed cost’ for items of property, plant and equipment.

‘Deemed cost’ is either the fair value of the asset as at the date of transition to

IFRS, or a previous GAAP revaluation at or before that date.)

IFRS 1 prohibits the retrospective application of some IFRSs for the opening IFRS

statement of financial position. For example, IFRS 1 states that estimates made

under IFRSs for the date of transition to IFRS must be ‘consistent with’ estimates

made by the entity under the previous GAAP, unless there is objective evidence

that these estimates were in error.

Chapter 21: Other issues

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 529

Example

Suppose that the date of transition to IFRS for ABC Company is 1 January 2004.

Information came to light in June 2004 showing that an estimate for accrued

expenses at 31 December 2003 should have been different. According to IAS 10

Events after the reporting period the information reveals an adjusting event, and the

statement of financial position as at 31 December 2003 should be altered.

IFRS 1 states that this is not permitted. Unless the estimate of accrued expenses for

the statement of financial position as at 31 December 2003 was clearly an error, no

adjustment should be made. Instead, the entity should account for the new

information in its financial statements for the year to 31 December 2004.

2.4 Presentation and disclosure by a first-time adopter

IFRS 1 requires that a first-time adopter must include at least one year of

comparative information in its first IFRS financial statements. (This is why the date

of transition to IFRS cannot be later than the beginning of the previous financial

year).

IFRS 1 also requires a first-time adopter to disclose the following reconciliations:

A reconciliation of equity that was reported under the previous GAAP with the

equity reported under IFRSs, for both of the following dates: (1) the date of

transition to IFRS and (2) the end of the last financial period in which the entity

presented its financial statements under the previous GAAP.

For example, suppose that a first-time adopter presents just one year of

comparative information, and prepared its first IFRS financial statements for the

year to 31 December 2005. The reconciliation of equity between ‘old GAAP’ and

IFRSs should be made for both 1 January 2004 and 31 December 2004.

A reconciliation of the profit or loss reported under the previous GAAP and

the profit or loss using IFRSs, for the entity’s most recent financial period before

adopting IFRSs.

If the entity recognises impairment losses for the first time in its opening IFRS

statement of financial position, it should provide the information that would

have been required by IAS 36 Impairment of assets if the impairment losses had

been recognised in the financial period beginning with the date of transition to

IFRS.

Paper P2: Corporate Reporting (International)

530 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

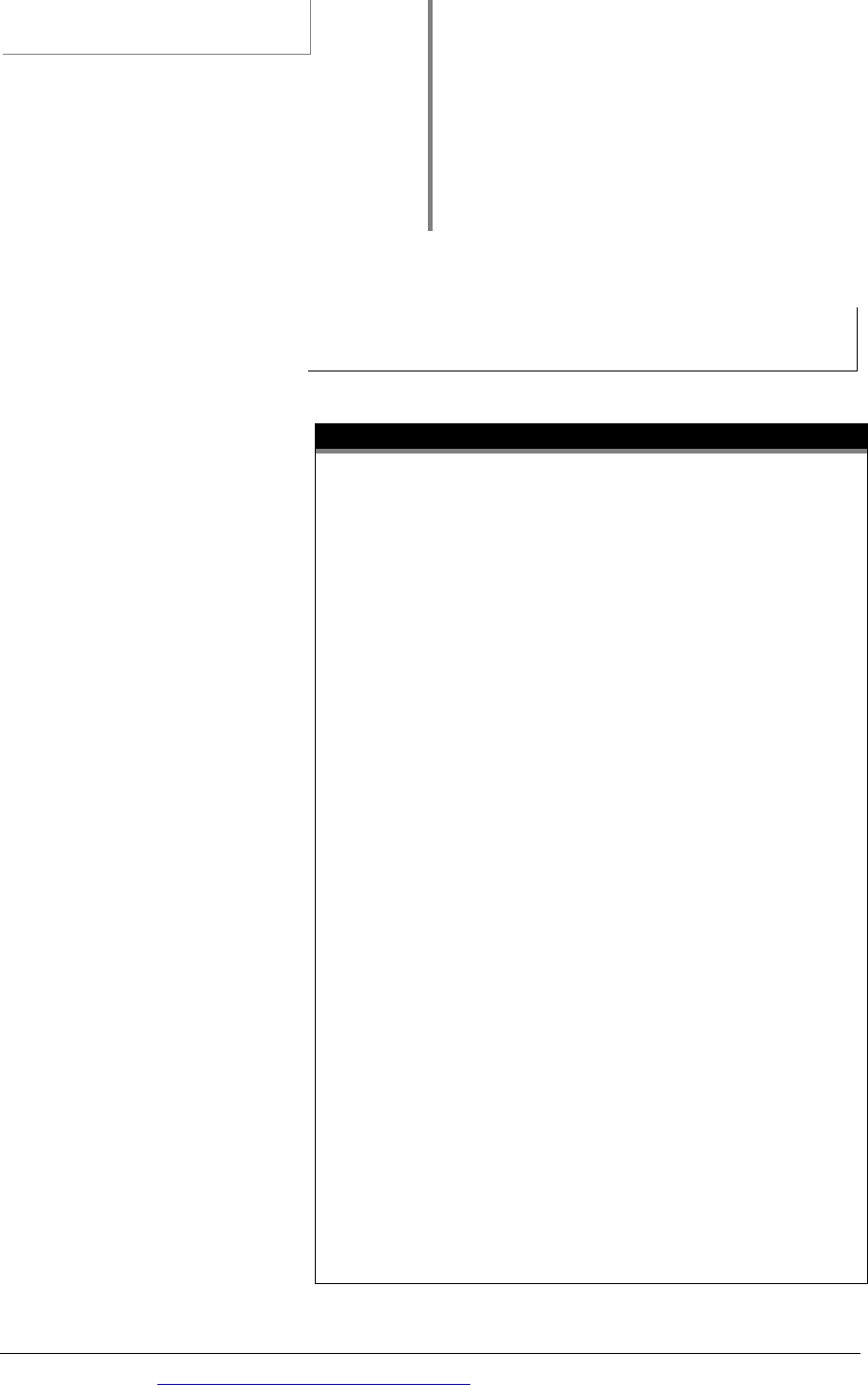

Example

Reconciliation of equity

A simplified example of a reconciliation of equity is shown below.

Previous

GAAP

Effect of

transition

to IFRSs IFRSs

Property, plant and equipment 2,000 300 2,300

Intangible assets 400 (50) 350

––––––––––––––––

––––––––––––––––

––––––––––––––––

Total non-current assets 2,400 250 2,650

––––––––––––––––

––––––––––––––––

––––––––––––––––

Trade and other receivables 1,200 0 1,200

Inventory 800 (70) 730

Cash 50 0 50

––––––––––––––––

––––––––––––––––

––––––––––––––––

Total current assets 2,050 (70) 1,980

Total assets 4,450 180 4,630

––––––––––––––––

––––––––––––––––

––––––––––––––––

Loans 800 0 800

Trade payables 415 0 415

Current tax liability 30 0 30

Deferred tax liability 25 220 245

––––––––––––––––

––––––––––––––––

––––––––––––––––

Total liabilities 1,270 220 1,490

––––––––––––––––

––––––––––––––––

––––––––––––––––

Total assets less total liabilities 3,180 (40) 3,140

––––––––––––––––

––––––––––––––––

––––––––––––––––

Issued capital 1,000 0 1,000

Revaluation reserve 0 190 190

Retained earnings (balance) 2,180 (230) 1,950

––––––––––––––––

––––––––––––––––

––––––––––––––––

Total equity 3,180 (40) 3,140

––––––––––––––––

––––––––––––––––

––––––––––––––––

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 531

Paper P2 (INT)

CorporateReporting

Q&A

Practice questions

Contents

Page

Corporate governance and corporate social

responsibility

1 Environmentalreporting 534

Group financial statements: introductory questions

2 PandQ 534

3 P,SandA 535

4 GroupandNCI 536

5 H,SandT 536

6 Disposal 537

7 Stepacquisitionandpartialdisposal 537

Group financial statements: advanced questions

8 TheEdgeleyGroup 538

9 TheAGroup 539

10 Herbert 541

11 Abbeville 543

Foreign currency

12 Orlando 545

13 MancasterandStockpot 545

Paper P2: Corporate reporting (International)

532 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Group statements of cash flows

14 Statementofcashflows 548

15 Bella 549

16 BishopGroup 551

17 GrapeGroup 554

Non-current assets

18 IMPS 556

19 Prima 557

Financial instruments

20 Financialinstruments 558

Substance over form

21 HAM 559

22 Flow 561

Financial reporting for listed companies

23 AZ 562

24 EPS 562

Accounting for retirement benefit costs

25 UniversalSolutions 563

26 IFRS2 564

Revenue, construction contracts and agriculture

27 TheLuckyDairy 565

Taxation

28 Cohort 566