ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 335

with the previous diagram showing the relevant cost of materials. They are the

same!)

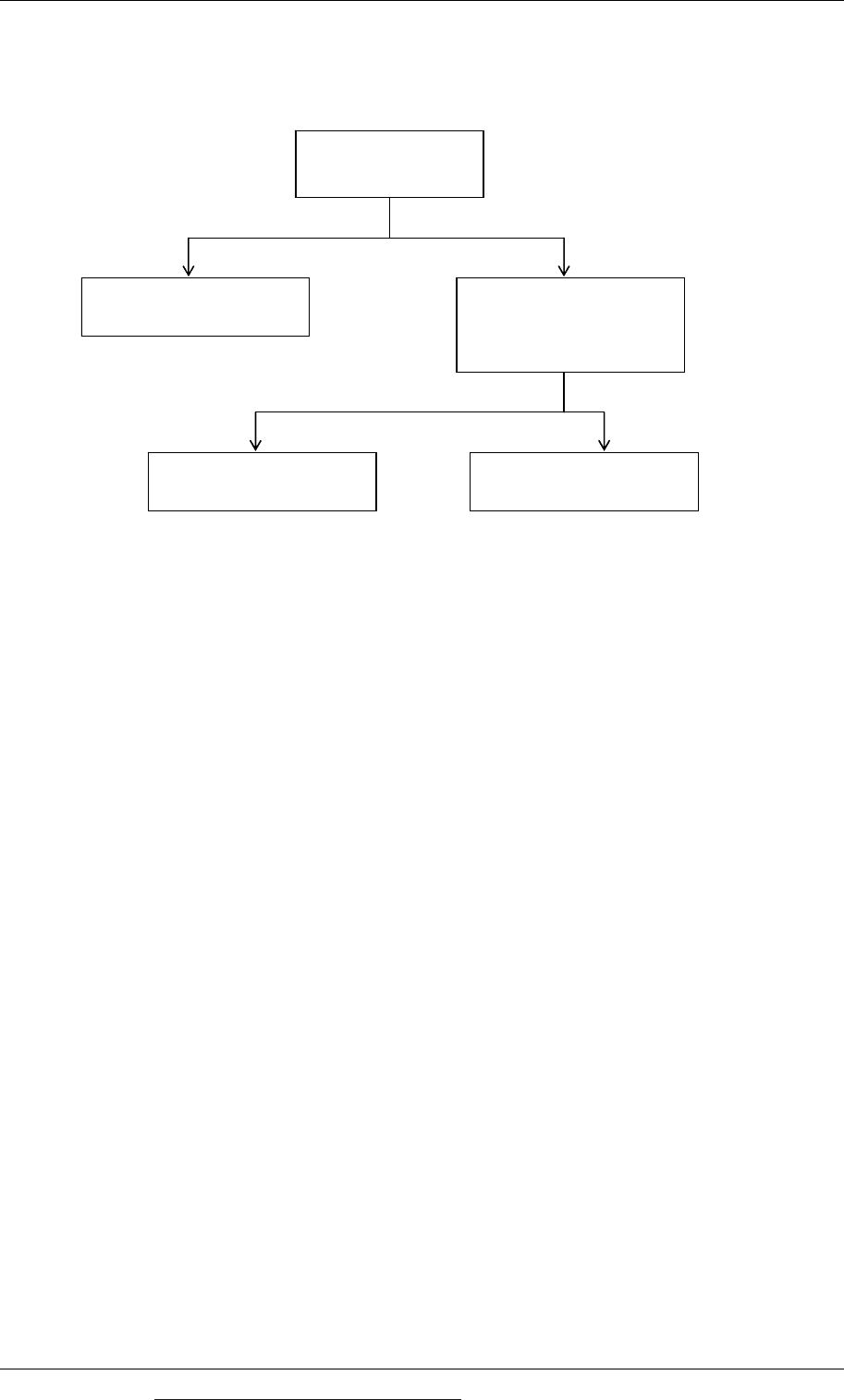

Is the machine

in regular use?

Relevant cost = current

replacement cost

Relevant cost =

Opportunity cost.

Opportunity cost = the

hi

g

her of:

Net disposal value

/

scrap value

Net benefit from

alternative use

Yes No

Note on terminology for non-current assets

If you have already studied financial accounting (financial reporting) you will be

familiar with non-current assets, depreciation of non-current assets and net book

value. If you are not familiar with financial accounting yet, the following brief

explanation might be useful.

A non-current asset is held for a number of years. The cost of a non-current asset

is ‘written off’ as an expense in the income statement over its expected useful

life.

There is a annual notional charge in the income statement for the use of an asset.

This is a depreciation charge. For example, if a non-current asset has a life of

four years and costs $40,000, there might be an annual depreciation charge for

the asset of $10,000 each year for four years.

The net book value of a non-current asset is its original cost (assuming that it is

not-re-valued at any time) less the accumulated depreciation to date. The asset

above that cost $40,000 would therefore have a net book value of $30,000 after

one year, $20,000 after two years, $10,000 after three years and $0 at the end of

the fourth year.

The points to note about depreciation and net book value, for the purpose of

relevant costing, are that:

Depreciation charges are a notional annual charge: they do not represent cash

flows

Net book value is a notional value of an asset: it has no economic or ‘cash flow’

significance.

Depreciation and net book value should always be ignored when identifying the

relevant costs of non-current assets.

Paper F2: Management Accounting

336 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A machine was purchased eight years ago for $20,000 and is depreciated at the rate

of $2,000 per year. The net book value of the machine is $4,000 and its net disposal

value is $3,000. A similar machine would cost $45,000 today.

The machine is not due to be replace for another two years, but as it has developed a

fault which cannot be repaired, the company must replace the machine

immediately.

Required

What is the relevant cost of the machine?

Answer

The machine is obviously in regular use. The relevant cost of the machine is

therefore its replacement cost, $45,000.

Note the following points.

The purchase price of $20,000 is not a relevant cost. It is a sunk cost that was

incurred in the past.

Net book values are not relevant costs. They do not represent cash flows or

disposal values. In this example the NBV of $4,000 is not a relevant cost.

The net disposal value of $3,000 is only relevant if the machine will not be

replaced and has no alternative use.

Example

A company has an item of equipment that originally cost $50,000. It would now cost

$60,000 to replace. Its current carrying amount (net book value) is $20,000 and it is

being depreciated by $10,000 each year.

The company does not use the equipment any more, and does not foresee any

further use for it. Another company, not a competitor, has offered to buy the

equipment for $12,000.

What is the relevant cost of the equipment?

Answer

The asset has no other use and would not be replaced if it is disposed of. The

options are to sell the equipment and earn $12,000 or not to sell it and earn nothing.

The relevant cost is $12,000.

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 337

Example

A company has an item of equipment that originally cost $30,000. Its net book value

is now $12,000. It could be used now on a three-month contract. If it is not used for

the contract it would be sold off, and the net disposal proceeds would be $4,000.

After use on the contract, the equipment would no longer have any sale value, and

it would have to be dismantled and disposed of at a cost of $2,000.

What is the relevant cost of the equipment?

Answer

The asset has no other use and will not be replaced. If the contract is undertaken, the

company will lose the opportunity to sell the equipment for $4,000. In addition, it

would have to pay disposal costs of $2,000 at the end of the three months. The total

relevant cost is therefore $4,000 + $2,000 = $6,000.

(The net book value is totally irrelevant.)

2.5 Using relevant costs

Relevant costs are used in accounting for decision-making. The costs and revenues

that are taken into consideration when evaluating the effect of a decision must be

the costs and revenues that are relevant to that decision. Non-relevant costs and

revenues must be ignored when evaluating a decision.

The examination syllabus does not cover the use of relevant costs for specific

decision-making problems, but you will come across these in your future studies of

accounting.

Practice multiple choice questions

1 A company is considering whether to undertake a job for a customer. The job would

require 1,800 kilos of a material that is used regularly in production. The company

already holds 1,200 kilos of the material in inventory, which cost $7,200 last month.

The supplier has recently announced a price increase of 5% for the material.

What is the total relevant cost of the material for the contract?

A $3,780

B $7,560

C $10,980

D $11,340 (2 marks)

2 A company is considering a contract that would require 120 hours of skilled labour.

The skilled labour is paid $24 per hour and all skilled employees are fully employed

manufacturing a product to which the following data relates:

Paper F2: Management Accounting

338 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

$ $

Selling price

75

Less: Variable costs

Skilled labour 36

Other variable costs 15

51

Contribution per unit

24

No other supply of skilled labour is available.

What is the total relevant cost of the labour for the contract?

A $1,920

B $2,880

C $4,800

D $6,000

(2 marks)

3 A company would need 800kg of material D for a contract it is considering. It

already has 600 kg of the material held in inventory. These materials were

purchased last month, but since then the supplier has increased the purchase price

by 6% to $53. The company uses material D regularly in normal production.

What is the total relevant cost for the contract of raw material D?

A $40,492

B $40,600

C $42,400

D $44,944

(2 marks)

4 A company owns a machine that has a current net book value of $2,700. It has not

been used for several months, but it could now be used on a job for a customer

which would last for up to six months. If the machine is not used for this job, it will

be sold immediately to earn net income of $2,900. After using the machine for the

contract, it would have no further use or value, and it would have to be disposed of

at a cost of $500.

What is the total relevant cost of the machine for the contract?

A $2,400

B $2,700

C $2,900

D $3,400

(2 marks)

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 339

Paper F2

Management Accounting

CHAPTER

15

Limiting factors and

linear programming

Contents

1 Limitingfactordecisions:singlelimitingfactor

2 Limitingfactordecisions:linearprogramming

3 Linearprogramming:graphicalsolution

Paper F2: Management Accounting

340 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Limiting factor decisions: single limiting factor

Definition of a limiting factor

Deciding whether there is a limiting factor

Maximising profit when there is a single limiting factor

Budgeting with one limiting factor

1 Limiting factor decisions: single limiting factor

1.1 Definition of a limiting factor

It is normally assumed in budgeting that a company can produce as many units of

its products (or services) that are necessary to meet the available sales demand.

Sales demand is therefore normally the factor that sets a limit on the volume of sales

in each period.

Sometimes, however, there could be a shortage of a key production resource, such

as an item of direct materials, or skilled labour, or machine capacity. In these

circumstances, the limiting factor setting a limit to the volume of sales and profit in

a particular period is the availability of the scarce resource.

It is assumed in this chapter that an entity makes and sells more than one different

product. When there is a limiting factor, the problem is therefore to decide how

many of each different product to make and sell in order to maximise profits.

1.2 Deciding whether there is a limiting factor

A limiting factor needs to be identified when the budget is prepared. The existence

of a limiting factor can be established by comparing:

the amount of each resource required to produce the quantities of products in

the budget, and

the total amount of the resource that will be available.

Example

A company makes three products, A, B and C, using the same direct labour work

force and the same machines to make all the products. Budgeted data for the

company is as follows.

Product X Product Y Product Z

Budgeted production (units) 30,000 24,000 18,000

Time required per unit minutes minutes minutes

Direct labour time (minutes) 15 20 40

Machine time (minutes 10 15 30

Chapter 15: Limiting factors and linear programming

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 341

The company expects to have 26,000 direct labour hours and 21,000 machine hours

available in the period.

Required

Is either direct labour time or machine time a limiting factor?

Answer

We need to compare the time required for production and the time available

Labour time Machine

time

Time required hours

hours

Product X 7,500

5,000

Product Y 8,000

6,000

Product Z 12,000

9,000

Total time required 27,500

20,000

Time available 26,000

21,000

Surplus/(shortfall) (1,500)

1,000

Direct labour time is a limiting factor but machine time is not a limiting factor.

1.3 Maximising profit when there is a single limiting factor

Limiting factor analysis uses the same principles as CVP analysis and relevant

costing, although it is normally sufficient to use the concepts of simple CVP

analysis.

When there is just one limiting factor (other than sales demand), total profit will be

maximised in a period by maximising the total contribution earned with the

available scarce resources.

The objective should be to maximise total contribution.

This will be achieved by maximising the contribution in total from the scarce

resource.

Products should therefore be ranked in order or priority for manufacture and

sale.

The priority ranking should be according to the contribution earned by each

product (or service) for each unit of the scarce resource that the product uses.

The products or services should be produced and sold in this order of priority,

up to the expected sales demand for each product.

The planned output and sales should be decided by working down through the

priority list until all the units of the limiting factor have been used.

In other words, in order to maximise profit, the aim should be to maximise the

contribution for each unit of limiting factor used.

Paper F2: Management Accounting

342 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company makes four products, A, B, C and D, using the same direct labour work

force on all the products. Budgeted data for the company is as follows.

Product A

B

C D

Annual sales demand (units) 4,000

5,000

8,000 4,000

$

$

$ $

Direct materials cost 3.0

6.0

5.0 6.0

Direct labour cost 6.0

12.0

3.0 9.0

Variable overhead 2.0

4.0

1.0 3.0

Fixed overhead 3.0

6.0

2.0 4.0

Full cost 14.0

28.0

11.0 22.0

Sales price 15.5

29.0

11.5 27.0

Profit per unit 1.5

1.0

0.5 5.0

Direct labour is paid $12 per hour. However, only 6,000 direct labour hours are

available during the year.

Required

Identify the quantities of production and sales of each product that would maximise

annual profit.

Answer

The products should be ranked in order of priority according to the contribution

that they make per direct labour hour.

A

B

C D

$

$

$ $

Sales price per unit 15.5

29.0

11.5 27.0

Variable cost per unit 11.0

22.0

9.0 18.0

Contribution per unit 4.5

7.0

2.5 9.0

Direct labour hours perunit 0.5

1.0

0.25 0.75

Contribution per direct labour hour 9.0

7.0

10.0 12.0

Priority for making and selling 3

rd

4

th

2

nd

1

st

The products should be made and sold in the order D, C, A and then B, up to the

volume of sales demand for each product and until all the available direct labour

hours (limiting factor resources) are used up.

Chapter 15: Limiting factors and linear programming

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 343

Profit-maximising budget

Product

Sales units

Direct labour

hours

Contribution

per unit

Total

contribution

$ $

D (1

st

) 4,000 3,000

9.0 36,000

C (2

nd

) 8,000 2,000

2.5 20,000

A (3

rd

) 2,000 (balance) 1,000

4.5 9,000

6,000

65,000

1.4 Budgeting with one limiting factor

You might not be told by an examination question that a limiting factor exists,

although you might be told that there is a restricted supply of certain resources. You

might be expected to identify the limiting factor by calculating the budgeted

availability of each resource and the amount of the resource that is needed to meet

the available sales demand.

Example

A company manufactures and sells two products, Product X and Product Y. The two

products are manufactured on the same machines. There are two types of machine,

and the time required to make each unit of product is as follows:

Product X Product Y

Machine type 1 10 minutes per unit 6 minutes per unit

Machine type 2 5 minutes per unit 12 minutes per unit

Sales demand each year is for 12,000 units of Product X and 15,000 units of Product Y.

The contribution per unit is $7 for Product X and $5 for Product Y.

There is a limit to machine capacity, however, and in each year there are only 3,000

hours of Machine 1 time available and 4,200 hours of Machine 2 time available.

Required

Recommend the quantities of Product X and Y that the company should make and

sell in order to maximise its annual profit.

Answer

The first step is to identify whether or not there is any limiting factor other than sales

demand. To do this we calculate the required machine time to manufacture units of

Product X and Y to meet the maximum sales demand. We then compare this

requirement for machine time with the actual time available.

Paper F2: Management Accounting

344 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Machine type 1

Machine type 2

hours

hours

Time required

To make 12,000 units of Product X 2,000

1,000

To make 15,000 units of Product Y 1,500

3,000

Hours needed to meet sales demand 3,500

4,000

Hours available 3,000

4,200

Shortfall (500)

-

Machine type 1 is a limiting factor, but Machine type 2 is not. To maximise

contribution and profit, we should therefore give priority to the product that gives

the higher contribution per Machine type 1 hour.

Product X Product Y

Contribution per unit $7 $5

Machine type 1 time per unit 10 minutes 6 minutes

Contribution per hour (Machine type 1)

$42 $50

Priority for making and selling 2

nd

1

st

Profit-maximising budget

Product

Sales

units

Machine

type 1 hours

Contribution

per unit

Total

contribution

$ $

Y (1

st

) 15,000

1,500

5.0 75,000

X (2

nd

) - balance 9,000

1,500

7.0 63,000

3,000

138,000

Exercise 1

A company makes four products, W, X, Y and Z, using the same single item of direct

material in the manufacture of all the products. Budgeted data for the company is as

follows.

Product W

X

Y Z

Annual sales demand (units) 4,000

4,000

6,000 3,000

$

$

$ $

Direct materials cost 5.0

4.0

8.00 6.00

Direct labour cost 4.0

6.0

3.00 5.00

Variable overhead 1.0

1.5

0.75 1.25

Fixed overhead 8.0

12.0

6.00 10.00

Full cost 18.0

23.5

17.75 22.25

Sales price 50.0

31.5

59.75 54.25

Profit per unit 32.0

8.0

42.00 32.00

Due to restricted supply, only $78,000 of direct materials will be available during the

year.