ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 325

based on relevant costs only. Local taxes and the costs of the security services

($28,000 in total for the next year) could be avoided and so these are relevant costs.

The rental cost of the warehouse cannot be avoided, and so should be ignored in the

economic assessment of the decision whether to close the warehouse or keep it open

for another year.

Sunk costs

Sunk costs are costs that have already been incurred (historical costs) or costs that

have already been committed by an earlier decision. Sunk costs must be ignored for

the purpose of evaluating a decision, and cannot be relevant costs.

For example, suppose that a company must decide whether to launch a new

product on to the market. It has already spent $500,000 on developing the new

product, and a further $40,000 on market research.

A financial evaluation for a decision whether or not to launch the new product

should ignore the development costs and the market research costs, because the

$540,000 has already been spent. The costs are sunk costs.

1.5 Opportunity costs

Relevant costs can also be measured as an opportunity cost. An opportunity cost is a

benefit that will be lost by taking one course of action instead of the next-most

profitable course of action.

Example

A company is offered the opportunity to do a job for a customer that will earn net

cash inflow of $4,000. However in order to do this job, it would be necessary to use

equipment that is operating at full capacity on other work. If the equipment is used

for this job, the company will have to give up other work that would earn net cash

inflow of $1,800.

An opportunity cost of doing the work for the customer is $1,800, because this is the

benefit that would be lost by doing the job instead of using the equipment for the

other work.

$

Net cash flow from job for the customer 4,000

Opportunity cost of using the equipment (1,800)

Net benefit from the job for the customer 2,200

Paper F2: Management Accounting

326 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Identifying relevant costs

Relevant costs of materials

Relevant costs of labour

Relevant costs and overheads

Relevant costs of non-current assets

Using relevant costs

2 Identifying relevant costs

For your examination, you need to understand the concept of relevant costs, and be

able to identify a relevant cost in a given situation.

In many cases, the relevant cost of materials or labour is the additional variable

costs that will be incurred as a consequence of a decision. CVP analysis therefore

provides the relevant costs in many situations. However, there are some situations

where the variable costs are not the relevant costs of a decision, or are not the only

relevant costs.

There are certain rules or guidelines that might help you to identify the relevant

costs for the purpose of decision-making.

2.1 Relevant costs of materials

The relevant costs of a decision to do some work or make a product will usually

include costs of materials. Relevant costs of materials are the additional cash flows

that will be incurred (or benefits that will be lost) by using materials for the purpose

that is under consideration.

The relevant cost of materials for a decision is the effect on cash flows that will occur

as a consequence of using the materials. The relevant cost of materials depends first

of all on whether the materials:

have not yet been purchased and will have to be purchased if a particular

decision is taken, or

have already been purchased and are currently held as inventory.

If none of the required materials are currently held as inventory, the relevant cost

of the materials is simply their purchase cost. If the decision is to go ahead with the

proposal, materials will have to be purchased and the relevant cost is the cash that

will have to be paid to acquire and use the materials.

If the required materials are currently held as inventory, identifying the relevant

costs is a bit more complex.

The materials have been purchased already; therefore their historical purchase

cost is irrelevant. Costs that have already been incurred are sunk costs and

cannot be relevant.

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 327

The relevant costs of materials held as inventory depend on what the

consequences of using these materials will be for future cash flows.

Relevant costs of materials are identified by applying the following rules:

Materials already purchased (held in inventory)

It is essential to remember that the historical cost of materials held in inventory

cannot be the relevant cost of the materials, because their historical cost is a sunk

cost. The rule for identifying relevant costs for materials, as set out in the above

chart, can be explained as follows.

If materials are held in inventory and will be required if a particular decision is

taken:

If the materials are in regular use, more materials will have to be purchased to

replace them.

If the materials are not in regular use, the consequences for future cash flows

will depend on what the materials would otherwise be used for.

Example

A company is considering whether to do a special job for a customer. The job will

need 200 units of direct materials. These are already held in inventory, but they are

used regularly for other work that the company does. These 200 units were

purchased for $3 per unit, but their purchase cost has recently been increased to

$3.20 by the supplier.

Paper F2: Management Accounting

328 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

If the decision is taken to do the job for the supplier, the 200 units already held will

be used. However, because the materials are used regularly for other work,

additional replacement materials will have to be purchased. These will cost $3.20

per unit, which is the relevant cost. The relevant cost of using the 200 units of

materials is therefore $640 (200 units × $3.20).

A different situation applies when materials are already held in inventory, but they

are not in regular use. Their historical purchase cost is not relevant, because this is a

sunk cost. The relevant cost of the materials depends on how the materials would be

used or disposed of if they are not used for the purpose under consideration. There

are only two possible uses of such materials.

They can be disposed of, and they might have a sales value from disposal.

They might have an alternative use, from which there would be some net cash

benefit.

The relevant cost of the materials is the higher of the net sales proceeds from

disposal and the net cash inflow from putting them to an alternative use. The higher

of these two amounts is the opportunity cost of the materials.

Example

A company has been asked to quote a price for a one-off contract.

The contract would require 5,000 kilograms of material X. Material X is used

regularly by the company. The company has 4,000 kilograms of material X currently

in inventory, which cost $2 per kilogram. The price for material X has since risen to

$2.10 per kilogram.

What are the relevant costs of the material X for the contract?

Answer

Material X

This is in regular use. Any units of the material that are held in inventory will have

to be replaced for other work if they are used for the contract. The relevant cost is

their replacement cost.

Relevant cost = replacement cost = 5,000 kilograms × $2.10 = $10,500.

Example

A company has been asked to quote a price for a one-off contract.

The contract would require 2,000 kilograms of material Y. There are 1,500 kilograms

of material Y in inventory, but because of a decision taken several weeks

ago, material Y is no longer in regular use by the company. The 1,500 kilograms

originally cost $7,200, and have a scrap value of $1,800. New purchases of material Y

would cost $5 per kilogram.

What are the relevant costs of the materials for the contract?

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 329

Answer

Material Y

This is not in regular use. There are 1,500 kilograms in inventory, and unless they

are used for the contract they will be sold as scrap. The contract would need 2,000

kilos, so an additional 500 kilograms would have to be purchased. The relevant cost

of material Y for the contract would be as follows:

$

Material held in inventory (scrap value) 1,800

New purchases (500 × $5)

2,500

Total relevant cost of Material Y 4,300

The scrap value of the 1,500 kilos already purchased is their scrap value. This is the

benefit that would be lost if the materials are used for the contract instead of using

them for the next-most beneficial use (which is to sell them as scrap).

Example

In order to carry out some work, a company would need to use 500 kilos of Material

M. It already has sufficient quantities of the material in inventory, but due to the

recent closure of a business operation, the materials are no longer in regular use.

The material M has a scrap value of $3 per kilo after selling costs. However, they

could also be used as an alternative material in another operation, where it could be

used instead of the same quantity of material P. Material P is in regular use and

costs $4 per kilo to buy.

What are the relevant costs of the material M?

Answer

Material M

This is not in regular use. There are 500 kilograms in inventory, and if they are not

used for the work, they will either by sold as scrap (for $3 per kilo) or used in a

different operation, which would save purchases of 500 kilos of material P at $4 per

kilo.

The relevant cost is the higher of these two values – 500 kilos × $4 = $2,000 – because

this is how the materials should be used if they are not used for the work under

consideration.

2.2 Relevant costs of labour

The relevant costs of a decision to do some work or make a product will usually

include costs of labour.

Paper F2: Management Accounting

330 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The relevant cost of labour for any decision is the additional cash expenditure (or

saving) that will arise as a direct consequence of the decision.

If the cost of labour is a variable cost, and labour is not in restricted supply, the

relevant cost of the labour is its variable cost. For example, suppose that part-

time employees are paid $10 per hour, they are paid only for the hours that they

work and part-time labour is not in short supply. If management is considering a

decision that would require an additional 100 hours of part-time labour, the

relevant cost of the labour would be $10 per hour or $1,000 in total. This

represent additional cash spending that would be incurred.

If labour is a fixed cost and there is spare labour time available, the relevant

cost of using labour is $0. The spare time would otherwise be paid for as idle

time, and there is no additional cash cost of using the labour to do extra work.

For example, suppose that a new contract would require 30 direct labour hours,

direct labour is paid $15 per hour, and the direct work force is paid a fixed

weekly wage for a 40-hour week. If there is currently spare capacity, so that the

labour cost would be idle time if it is not used for the new contract, the relevant

cost of using 30 hours on the new contract would be $0. The 30 labour hours

must be paid for whether or not the contract work is undertaken.

If labour is in limited supply, the relevant cost of labour should include the

opportunity cost of using the labour time for the purpose under consideration

instead of using it in its next-most profitable way.

Labour in limited supply

When labour is in restricted supply, there are alternative ways of using the labour

time in order to earn cash for the entity. If labour is used for a particular purpose, it

cannot be used for something else.

The relevant cost of labour is therefore:

the cost of the labour, plus

the contribution that would otherwise be earned from putting the labour to its

alternative use.

The contribution forgone is a relevant cost, not the profit forgone. Fixed costs will

not be affected by a switch of labour from one job to another. The relevant cash

flows are the net cash revenue that would be lost. This is the contribution forgone.

Labour costs can be treated as a variable cost whenever it is in short supply, for

the purpose of calculating the relevant cost of labour

Example

A company has been asked by a customer to carry out a special job. The work

would require 20 hours of skilled labour time. There is a limited availability of

skilled labour, and if the special job is carried out for the customer, skilled

employees would have to be moved from doing other work that earns a

contribution of $40 per labour hour. Skilled labour is paid $30 per hour.

What is the relevant cost of the labour?

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 331

Answer

Skilled labour is in restricted supply and using labour for the job will mean that

other work that earns $30 per hour will be lost.

$

Cost of labour hours (20 hours × $30)

600

Contribution forgone – an opportunity cost: (20 hours × $40)

800

Total relevant cost of skilled labour 1,400

Example

A company has been asked to do a special job for a customer. This would require 8

hours of Grade A labour and 6 hours of Grade B labour. Grade A labour is paid $20

per hour and Grade B labour is paid $15 per hour.

The Grade A labour would have to be taken off other work that earns a contribution

of $40 per hour. There is sufficient Grade B labour available: if the Grade B

employees do not work on this job, they will be paid but will have no other

revenue-earning work to do.

Required

What are the relevant costs of the labour for the job?

Answer

Grade A labour is in restricted supply. Grade B labour time is available and would

otherwise be paid for as idle time. The relevant labour costs are therefore as

follows.

$

Grade A labour: basic pay (8 hours × $20) 160

Grade A labour: opportunity cost (8 hours × $40) 320

Grade B labour: no incremental cost 0

Relevant cost of labour 480

Example

A company is considering a contract that will require labour time in three

departments.

Department 1. The contract would require 200 hours of work in department 1,

where the work force is paid $10 per hour. There is currently spare labour capacity

in department 1 and there are no plans to reduce the size of the workforce in this

department.

Department 2. The contract would require 100 hours of work in department 2

where the workforce is paid $12 per hour. This department is currently working at

Paper F2: Management Accounting

332 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

full capacity. The company could ask the work force to do overtime work, paid for

at the normal rate per hour plus 50% overtime premium. Alternatively, the work

force could be diverted from other work that earns a contribution of $4 per hour.

Department 3. The contract would require 300 hours of work in department 3

where the workforce is paid $20 per hour. Labour in this department is in short

supply and all the available time is currently spent making product Z, which earns a

contribution of $10 per hour.

Required

What is the relevant cost for the contract of labour in the three departments?

Answer

Department 1. There is spare capacity in department 1 and no additional cash

expenditure would be incurred on labour if the contract is undertaken.

Relevant cost = $0.

Department 2. There is restricted labour capacity. If the contract is undertaken,

there would be a choice between:

overtime work at a cost of $18 per hour ($12 plus overtime premium of 50%) –

this would be an additional cash expense, or

diverting the labour from other work, and losing contribution of $4 per hour –

cost per hour = $12 basic pay + contribution forgone $4 = $16 per hour.

It would be better to divert the work force from other work, and the relevant cost of

labour is therefore 100 hours × $16 per hour = $1,600.

Department 3. There is restricted labour capacity. If the contract is undertaken,

labour would have to be diverted from making product Z which earns a

contribution of $10 per labour hour. This is an opportunity cost of labour if the

contract work is undertaken. The relevant cost of the labour in department 3 is:

$

Labour cost (300 hours × $20)

6,000

Contribution forgone (300 hours × $10)

3,000

Total relevant cost , Department 3 9,000

Summary of relevant costs of labour:

$

Department 1 0

Department 2 1,600

Department 3 9,000

10,600

Chapter 14: Relevant costs

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 333

2.3 Relevant costs and overheads

Relevant costs of expenditures that might be classed as overhead costs should be

identified by applying the normal rules of relevant costing. Relevant costs are future

cash flows that will arise as a direct consequence of making a particular decision.

Fixed overhead absorption rates are therefore irrelevant, because fixed overhead

absorption is not overhead expenditure and does not represent cash spending

However, it might be assumed that the overhead absorption rate for variable

overheads is a measure of actual cash spending on variable overheads. It is therefore

often appropriate to treat a variable overhead hourly rate as a relevant cost, because

it is an estimate of cash spending per hour for each additional hour worked.

The only overhead fixed costs that are relevant costs for a decision are extra cash

spending that will be incurred, or cash spending that will be saved, as a direct

consequence of making the decision.

Example

A company has three car showrooms, A, B and C. The budgeted sales and profit or

loss for each showroom next year are as follows.

A B C Total

$000 $000 $000 $000

Sales 2,000

1,600

2,400

6,000

Contribution 300

150

150

600

Less: Fixed costs (180)

(120)

(200)

(500)

Profit/(Loss) 120

30

(50)

100

60% of the total fixed costs are general company overheads. These are apportioned

to the three stores on the basis of sales revenue. The other fixed costs are specific to

each store and are avoidable if the store is closed down.

Required

What would be the annual profit if showroom C is closed down?

Answer

The general overhead costs apportioned to Showroom C would not be saved if the

showroom is closed down.

Total general overhead costs = 60% × $500,000 = $300,000.

Paper F2: Management Accounting

334 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

These are apportioned on the basis of sales revenue; therefore the apportionment to

showroom C is:

$300,000 × (2,400/6,000) = $120,000.

The fixed costs saved or avoided if showroom C is closed = $(200,000 – 120,000) =

$80,000.

If showroom C is closed:

$

Loss of contribution 150,000

Saving in fixed costs 80,000

Reduction in profit 70,000

The profit would therefore fall from $100,000 to $30,000.

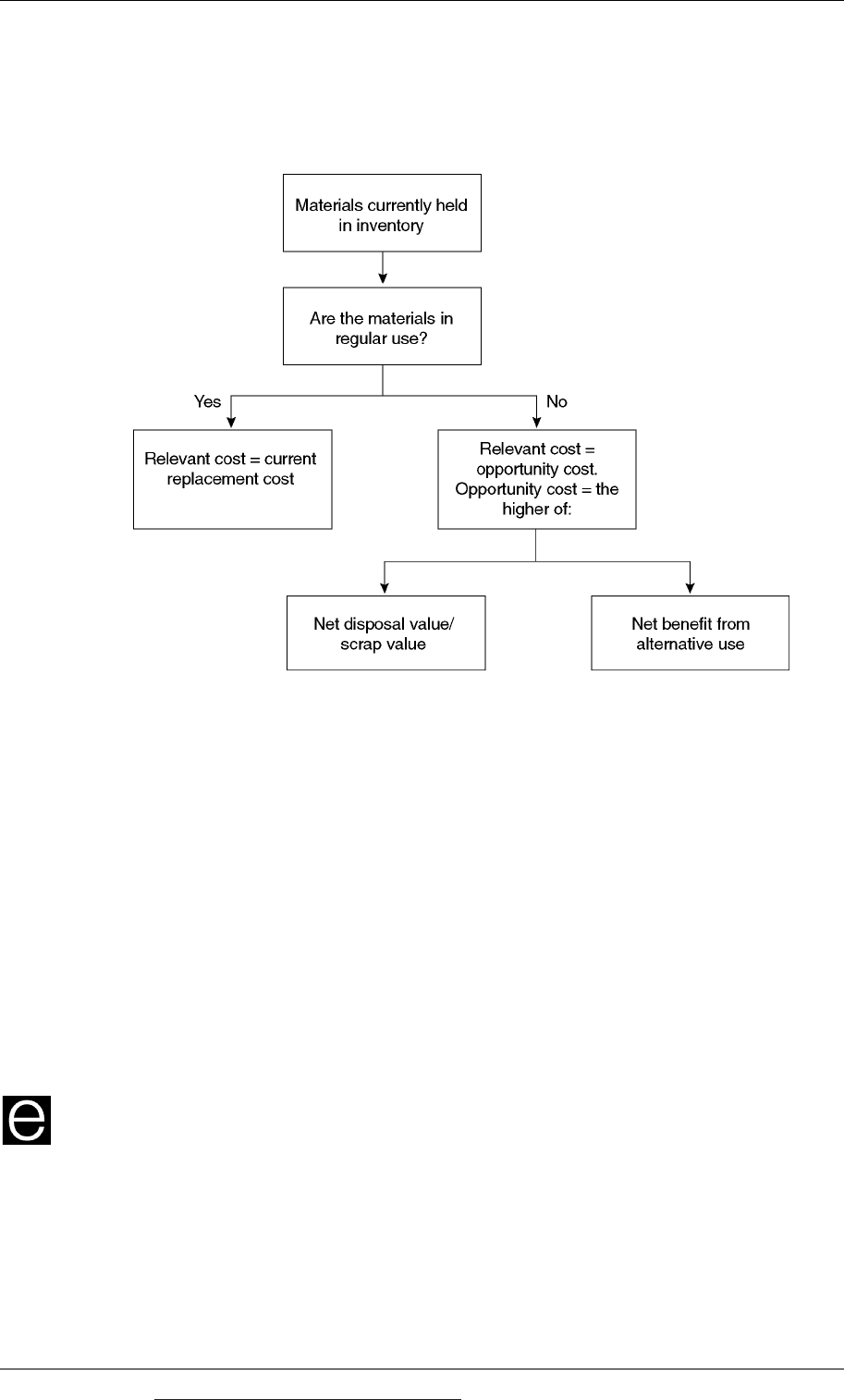

2.4 Relevant costs of non-current assets (NCAs)

Non-current assets are ‘capital assets’ such as buildings, plant and equipment etc

that an entity acquires for long-term use.

The costs of non-current assets or the revenue from non-current assets are

sometimes a factor in a management decision.

A decision might be concerned with whether or not to buy a new non-current

asset. When a new non-current asset is purchased, its relevant cost is its

purchase cost, and there might also be a residual value at the end of its life when

the asset is eventually sold. Decisions about buying non-current assets (capital

expenditure decisions) are outside the syllabus for the examination.

A decision might be concerned with whether to dispose of a non-current asset

now. Alternatively, a decision might involve using a non-current asset in a

different way and for a different purpose.

You might be required to identify the relevant costs or benefits of a non-current

asset that is already owned by a business entity. The relevant costs of these non-

current assets are identified in a similar way to the relevant costs of materials.

If, as a consequence of taking a decision, the non-current asset would have to be

replaced, a relevant cost is its replacement cost.

If, as a consequence of taking a decision to use the asset for a different purpose,

the non-current asset would not be replaced, the relevant cost (opportunity

cost) of the non-current asset is the higher of its:

- net disposal value (or scrap value), and

- the net benefit that would be obtained from using the asset in the next-best

way.

The relevant cost of non-current assets can also be described as their ‘deprival

value’. It is calculated in a similar way to the relevant cost of materials that have

already been purchased.

The following diagram shows the rules that should be applied in order to identify

the relevant costs of non-current assets such as machinery. (Compare this diagram