Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Chapter 2

Gross Income

and Exclusions

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 2.1 Understand and apply the definition of gross income.

LO 2.2 Determine the tax treatment of significant elements of

gross income such as interest, dividends, alimony, and

prizes.

LO 2.3 Calculate the taxable and nontaxable portions of annuity

payments.

LO 2.4 Understand the tax rules for significant exclusions from

gross income including life insurance benefits, inheritances,

scholarships, health insurance benefits, meals and lodging,

municipal bond interest, and fringe benefits.

LO 2.5 Apply the rules governing inclusion of Social Security

payments as income.

Overview

This chapter starts with the definition of gross income. Tables 2.1 and 2.2 are lists of the

common inclusions in and exclusions from gross income. Detailed coverage is provided for

inclusions and exclusions that may present spe cific problems to taxpayers. The coverage

includes the special tax treatment for interest an d dividends, alimony, prizes and awards,

annuities, life insurance, and gifts and inheritances. Coverage of important exclusions

includes scholarships, accident and health insurance benefits, cert ain meals an d lodging,

municipal bond interest, and the special treatment of Social Security benefits. The ele-

ments of gross income discussed here represent much of what is included in the first

line of the individual tax formula.

2-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 2.1

THE NATURE OF GROSS INCOME

Gross income is the starting point for calculating a taxpayer’s tax liability. The tax law

states that gross income is:

...all income from whatever source derived, including (but not limited to) the follow-

ing items:

1. Compensation for services, including fees, commissions, fringe benefits, and similar items

2. Gross income derived from business

3. Gains derived from dealings in property

4. Interest

5. Rents

6. Royalties

7. Dividends

8. Alimony and separate maintenance payme nts

9. Annuities

10. Income from life insurance and endowment contracts

11. Pensions

12. Income from discharge of indebtedness

13. Distributive share of partnership gross income

14. Income in respect of a decedent

15. Income from an interest in an estate or trust

Income earned illegally from any source, including drug sales and organized

crime, is taxable. Al Capone, who headed an enormous, violent, and profitable

crime organization, eluded conviction for criminal activities until 1930 when he

was sent to prison for tax evasion.

The definition of gross income as ‘‘all income from whatever source derived’’ is per-

haps the most well-known definition in the tax law. Under this definition, unless there is an

exception in the law, the U.S. government considers all income taxable. Therefore, prizes

and awards, cash and noncash payments for goods and services, payments made in trade or

‘‘barter’’ (such as car repairs traded for tax preparation services), and illegal income not

generally reported to the IRS are all still taxable income.

Table 2.1 provides an expanded list of items that are included in gross income. When in

doubt, the general rule is that everything a taxpayer receives must be included in gross

income unless specifically excluded. Any noncash items must be included in gross income

at the fair market value of the items received.

The tax law provides that certain items of income are exempt from taxation; these items

are referred to as ‘‘exclusions.’’ The exclusions include such items as life insurance pro-

ceeds, gifts, and veterans’ benefits. A more complete list of exclusions from gross income

is provided in Table 2.2.

The IRS recently has been examining the transaction records of PayPal, the

online payment firm. The IRS suspects many taxpayers have not reported

income earned from sales on eBay. Beginning in 2011, certain larger online pay-

ment amounts must be reported to the IRS automatically.

2-2 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

TABLE 2.1 2010 INCLUSIONS IN GROSS INCOME

Alimony Gambling winnings

Amounts recovered after being deducted

in prior years

Group-term life insurance premium paid by

employer for coverage over $50,000

Annuities Hobby income

Awards Incentive awards

Back pay Interest income

Bargain purchase from employer Jury duty fees

Bonuses Living quarters, meals (unless furnished for

Breach of contract damages employer’s convenience, etc.)

Business income Military pay (unless combat pay)

Clergy fees and contributions Notary fees

Commissions Partnership income

Compensation for services Pensions

Contributions received by members

of the clergy

Prizes

Professional fees

Damages for nonphysical personal injury Punitive damages

Death benefits Reimbursement for moving expenses

Debts forgiven Rents

Directors’ fees Retirement pay

Dividends Rewards

Embezzled funds Royalties

Employee awards Salaries

Employee benefits (except certain fringe

benefits)

Scholarships (room and board)

Severance pay

Employee bonuses Strike and lockout benefits

Employee stock options Supplemental unemployment benefits

Estate and trust income Tips and gratuities

Farm income Travel allowances

Fees

Gains from illegal activities

Unemployment compensation

Wages

Gains from sale of property

TABLE 2.2 2010 EXCLUSIONS FROM GROSS INCOME

Accident insurance proceeds Inheritances

Annuities (to a limited extent) Life insurance proceeds

Bequests Meals and lodging (furnished for

Casualty insurance proceeds employer’s convenience, etc.)

Child support payments Military allowances

Damages for physical personal injury Minister’s dwelling rental value

or sickness allowance

Disability benefits (generally, but not always) Municipal bond interest

Federal Employees’ Compensation Act Relocation payments

payments Scholarships (tuition and books)

Gifts Social Security benefits (with limits)

Group-term life insurance premium paid by Veterans’ benefits

employer (coverage not over $50,000) Welfare payments

Health insurance proceeds Workers’ compensation

Section 2.1

The Nature of Gross Income 2-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 2.2 INTEREST AND DIVIDEND INCOME

Any interest or dividend income a taxpayer receives or that is credited to his or her account

is taxable income, unless it is specifically exempt from tax such as state or municipal bond

interest. If the interest or dividends total more than $1,500, the taxpayer is required to file

Schedule B of Form 1040 (or Form 1040A, Schedule 1), which lists the amounts and sour-

ces of the income.

The fair market value of gifts or services a taxpayer r eceives for making long-term

deposits or opening accounts in savings institutions is also taxable interest income. Interest

is reported in the year it is received by a cash basis taxpayer.

Taxpayers may defer reporting interest income on a bank certificate of deposit

(CD) if the CD has a maturity of 1 year or less, and there is a substantial penalty

for early withdrawal. For example, assume an investor purchases a 6-month CD

on September 1, 2010, which matures on March 1, 2011, and the bank charges

a penalty equal to 2 months of interest in the event of early withdrawal. In this

case, the 4 months of interest earned on the account during 2010 will not have

to be reported until the investor’s 2011 tax return is filed.

When a taxpayer withdraws funds early from a CD and must pay a penalty as

described above, the full amount of the interest is reported as income and the penalty

may be deducted on line 30 of Form 1040 as a deduction for adjusted gross income.

Self-Study Problem 2.1

Indicate whether each of the items listed below should be included in gross

income or excluded from gross income in 2010.

Included Excluded

1. Prizes and awards ____________ ____________

2. Embezzled funds ____________ ____________

3. Child support payments ____________ ____________

4. Alimony ____________ ____________

5. Pensions ____________ ____________

6. Inheritances ____________ ____________

7. Welfare payments ____________ ____________

8. Bequests ____________ ____________

9. Jury duty fees ____________ ____________

10. Royalties ____________ _____ _______

11. Life insurance proceeds paid at death ____________ ____________

12. Hobby income ____________ ____________

13. Rewards ____________ ____________

14. Partnershi p income ____________ ____________

15. Casualty insurance proceeds ____________ ____________

16. G.I. Bill benefits ____________ ____________

17. Scholarshi ps for room and board ____________ ____________

18. Mileage allowance ____________ ____________

19. Gifts ____________ ____________

2-4 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

U.S. Savings Bonds

The United States government issues three basic types of savings bonds to individuals,

Series EE Bonds, Series HH Bonds, and Series I Bonds. Series EE Bonds are issued at

a discount from their face value. These bonds increase in value over their life, and the

increase in redemption value is taxable. For example, a $100 savings bond might be issued

at $50 and be redeemable for $100 at maturity. The second type of savings bond, Series

HH Bond, is issued at face value and pays interest twice a year by check. Interest on

Series HH Bonds is reported in the year received by a cash basis taxpayer. (Note: As

of August 31, 2004, the Treasury stopped issuing Series HH bonds. HH bonds sold

before A ugust 31, 2004, may still be outstandi ng and paying interest.) Series I Bonds,

like Series EE Bonds, do not pay interest un til maturity, but earnings are adjusted for

inflation on a semiannual basis.

Cash basis taxpayers report the increase in redemption value (interest) on a Series EE

Bond or a Series I Bond using one of the following methods:

1. The interest may be reported in the year the bonds are cashed or in the year they

mature, whichever is earlier (no election is required to use this method), or

2. The taxpayer may elect to report the increase in redemption value each year.

If the taxpayer wants to change from method (1) to method (2), he or she may do so

without the permission of the IRS. In the year of change, all interest earned to date and

not previously reported must be reported on all Series EE Bonds and Series I B onds held

by the taxpayer. Once method (2) is selected, the taxpayer must continue to use it for all

Series EE Bonds currently held or acquired in the future. Taxpayers cannot change back

to meth od (1) with out permission of the IRS.

Dividends

Dividends are one type of distribution paid to a taxpayer by a corporation. Taxpayers may

receive the following types of distributions from a corporation:

1. Ordinary dividends

2. Nontaxable distributions

3. Capital gain distributions

Ordinary dividends are by far the most common type o f corporate distribution. They

are paid from the earnings and profits of the corporation.

Nontaxable distributions are a return of invested capital and are not paid from the earn-

ings and profits of the corporation. They are considered a return of the taxpayer’s invest-

ment in the corporation and are not included in the taxpayer’s income. Instead, the

taxpayer’s basis in the stock is reduced by nontaxable distributions until the basis reaches

zero.

1

After the stock has reached a zero basis, distributions that represent a return of cap-

ital are t axed as cap ital gains. Capital gain distributions are reported either on page 1 of

Form 1040 or on Schedule D.

Current Tax Rates for Dividends

The 2003 and 2006 tax acts enacte d special lower tax rates for qualifying dividends that will

‘‘sunset’’ at the end of 2010. For years, experts have argued that corporate dividends are

taxed twice, once when the corporat ion pays tax on profits, and once when the dividend

1

A taxpayer’s basis in an investment is usually the cost of the investment. The basis is used to determine the gain or loss

when the investment is sold.

Section 2.2

Interest and Dividend Income 2-5

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

is received by the shareholder. To provide some tax relief for individual taxpayers who

receive corporate dividends, the tax rates on dividends are as follows:

Qualifying Dividend Rate

Ordinary Tax Bracket 2003–2007 2008–2010

10% and 15% 5% 0%

Higher brackets 15% 15%

Dividends qualifying for thi s special treatment m ust be received by an individual who

has held the stock for more than 60 days during the 120-day period beginning 60 days

before the stock’s ‘‘ex-dividend’’ date, the date the stock no longer carries the right to

receive the dividend. Dividends received which do not meet the requirements are taxed

at ordinary rates. For additional rules defining ‘‘qualified’’ divi dends, please see t he IRS

Web site or a tax service. The definition is too lengthy and complex to cover fully in

this text. Corporat ions issuing dividends and broker age companies holding stock invest-

ments for taxpayers are required to classify and report the amount of qualifying dividends

to investors.

SECTION 2.3

ALIMONY

Alimony payments are deductible by the individual making the payments, and are taxable income

to the person receiving the payments. The term alimony, for income tax purposes, includes sep-

arate maintenance payments or similar periodic payments made to a spouse or former spouse.

Payments must meet certain requirements to be considered alimony. These requirements

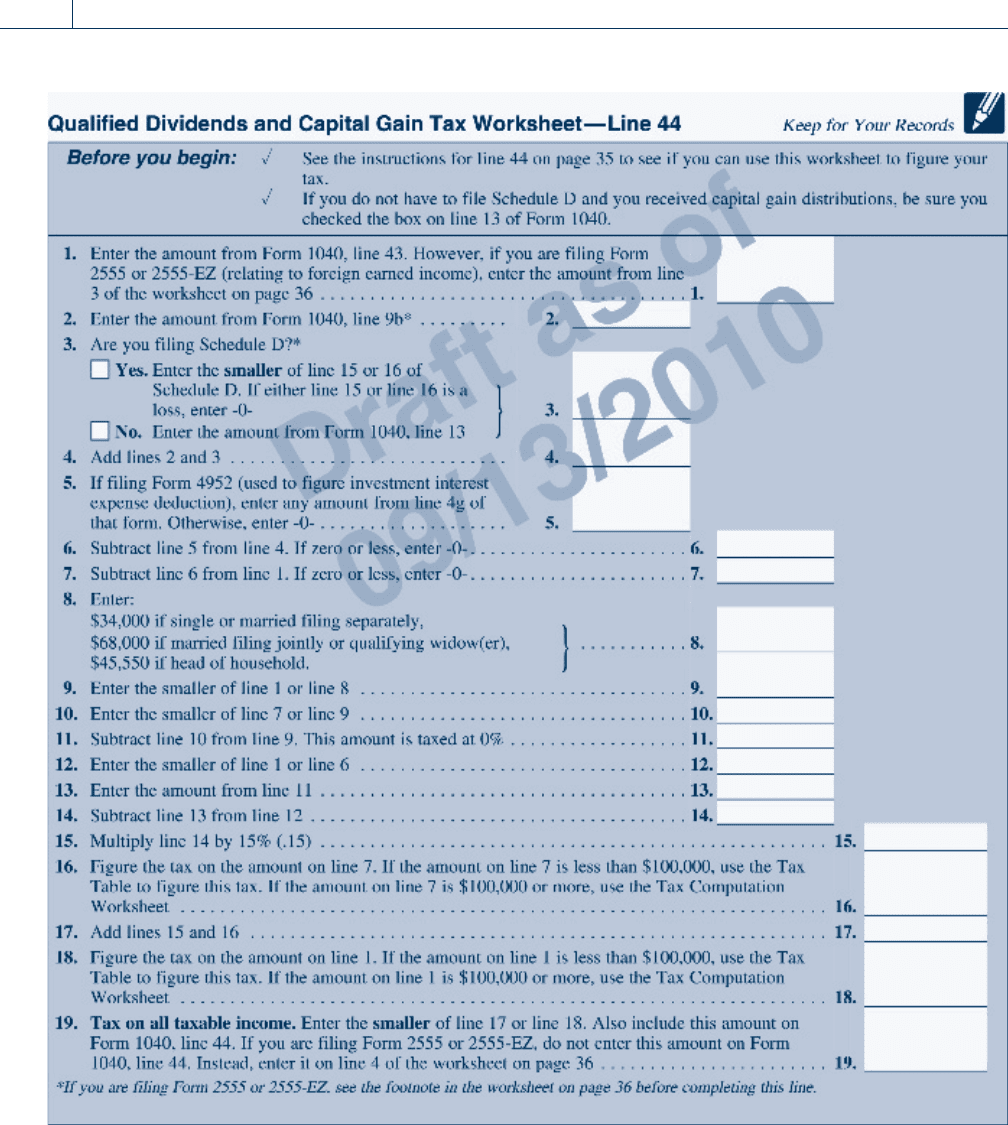

Self-Study Problem 2.2

Bill and Betty Brown received the following dividend and interest income

during 2010:

Bill

Received by

Betty Jointly

Dividends (all qualified for new rates):

IBM $275 $175

GM $ 450

AT&T 450 300

Interest:

Ford Bonds 425

Big Savings and Loan 2,150

U.S. Bonds 175

Nontaxable Distribution:

Western Gas & Electric 875

Totals

$725 $900 $3,650

The Browns have taxable income, including dividends and interest, of $40,000.

Complete Form 1040, Schedule B, an d the tax calculation worksheet on pages

2-7 and 2-8 for the Brown’s 2010 tax year.

2-6 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 2.3

Alimony 2-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

2-8 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

depend on whether the divorce or separation agreement was executed before 1985 or after 1984.

The post-1984 tax rules for divorce agreements are discussed below.

For divorce agreements executed after 1984, alimony payments must meet the following

requirements:

1. The payments must be in cash and must be received by the spouse (or former

spouse).

2. The payments must be made under a decree of divorce or separate maintenance or

under a written instrument incident to the divorce.

3. The payor must have no liability to make payments for any period following the

death of the spouse receiving the payments.

4. The payments must not be designated in the written agreement as anything other

than alimony.

5. If the parties are divorced or legally separated, they must not be members of the

same household at the time the payments are made.

Disguised child support payments may not be treated as alimony. Payments contingent

on the status of a child, such as the age or marital status of the child, are not considered

alimony.

EXAMPLE Under a 2007 divorce agreement, Sam has agreed to pay his former

spouse, Silvia, $1,000 per month. The payments meet all the tests for

classification as alimony, but they will be reduced to $600 per month

when their child, in Silvia’s custody, becomes 18 years of age. In this

situation, $400 of each payment must be treated as nondeductible

child support and cannot be considered alimony. N

During a divorce, the tax impact of structuring payments as alimony rather than

as property settlement payments should be carefully considered. If one spouse is

in a lower tax bracket than the other spouse, both spouses may be better off

structuring payments made to the lower-income spouse as alimony. The tax sav-

ings to the high-income spouse will be larger than the taxes paid by the low-

income spouse. The benefit of the tax savings can then be shared with the low-

income spouse in the form of higher alimony payments, resulting in a ‘‘win–win’’

situation.

Alimony Recapture

Congress has enacted provisions to prevent ‘‘front-end loading’’ of alimony payments. The

tax law may require taxpayers paying alimony to include previ ously deducted payments in

income if the payments significantly decrease in amount during the first few years. The

rules for alimony recapture are complex and vary depending on the year the divorce decree

was granted.

Property Transfers

A spouse who transfers property in settlement of a marital obligation is not required to rec-

ognize any gain as a result of the property’s appreciation. Thus, if in a divorce settlement a

wife transfers property with a fair market value of $10,000 and a tax basis of $3,000 to her

Section 2.3

Alimony 2-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

husband, she will not be required to rec ognize the gain of $7,000 ($10,000 $3,000).

Of course, the husband would be required to assume the wife’s tax basis ($3,000) in the

property.

Child Support

Payments made for chi ld support are not deductible by the taxpayer making them, nor are

they income to the recip ient. However, they may be an important factor in determ ining

which spouse is entitled to claim the dependency exemption for the child (see Chapter 1).

Child support payments must be up to date before any amount paid may be treated as ali-

mony. That is, if a taxpayer is obligated to pay both child support and alimony, he or she

must first meet the child support obligation before obtaining a deduction for alimony pay-

ments. Payments for child support include payments designated as such in the marital set-

tlement agreement, plus any alimony payments that are contingent upon the status of a

child.

EXAMPLE Jim is required under a 2007 divorce decree to pay $400 alimony and

$250 child support per month. Since the decree separately states that

$250 is child support, only $400 per month is deductible by Jim and

counts as income to his ex-wife. N

The IRS treats an annulled marriage as though it never existed. Therefore, the

IRS requires couples who have received an annulment to refile their tax returns

as unma rried persons for as many as 3 years back. In some cases, this can be a

very expensive procedure.

Self-Study Problem 2.3

Answer the following questions, assuming the divorce agreements were exe-

cuted after 1984.

1. A husband is required to pay his former wife $12,000 in alimony in the

current year. Since he is short of cash, he gives her an automobile worth

$12,000, which she accepts in place of the alimony. How much may the

husband de duct as alimony?

$ ____________

2. A husband is required to pay alimony of $2,000 per month to his ex-wife.

However, the alimony is reduced to $1,200 per month when their child,

who lives with his mother, becom es 18. How much of the monthly pay-

ment is alimony income to the wife?

$ ____________

3. A wife is required to transfer $100,000 worth of property to her ex-hus-

band as a property settlement. The property has a basis to the wife of

$20,000. How much taxable gain must the wife recognize on this transfer?

$ ____________

2-10 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.