Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

SECTION 2.4

PRIZES AND AWARDS

Prizes and awards are taxable income to the recipient. Winnings from television or

radio shows, door prizes, lotteries, and o ther contest winnings are income to taxpayers.

In addition, all other awards are generally taxable, even if they are awards given for

accomplishments and with no action on the part of the taxpayer. If the prize or

award is received in property instead of ca sh, the fair market value of the property is

included in the taxpayer’s income. Taxpayers may refuse a prize and exclude its value

from income.

An exception is provided for certain employee achievement awards in the form of tan-

gible personal property, such as a gold watch for 25 years of service. If the award is made

in recognition of length of service o r safety achi evement, the value of the property may

be excluded from income. Generally, the maximum amount excludable is $400. How-

ever, if the award is a ‘‘qualified plan award,’’ the maximum exclusion is increase d to

$1,600.

The Oscar show’s gift bags, including more than $100,000 in resort vacations,

chocolates, and other goodies, were the subject of an IRS press release remind-

ing presenters and performers that the bags qualified as taxable income.

One of the saddest recent taxable prizes was the free ride to space received

by Brian Emmett, a software consultant. He won a free space flight in a sweep-

stakes, but he had to give up his seat when he discovered that he would owe

more than $25,000 in taxes on the $138,000 value of the trip.

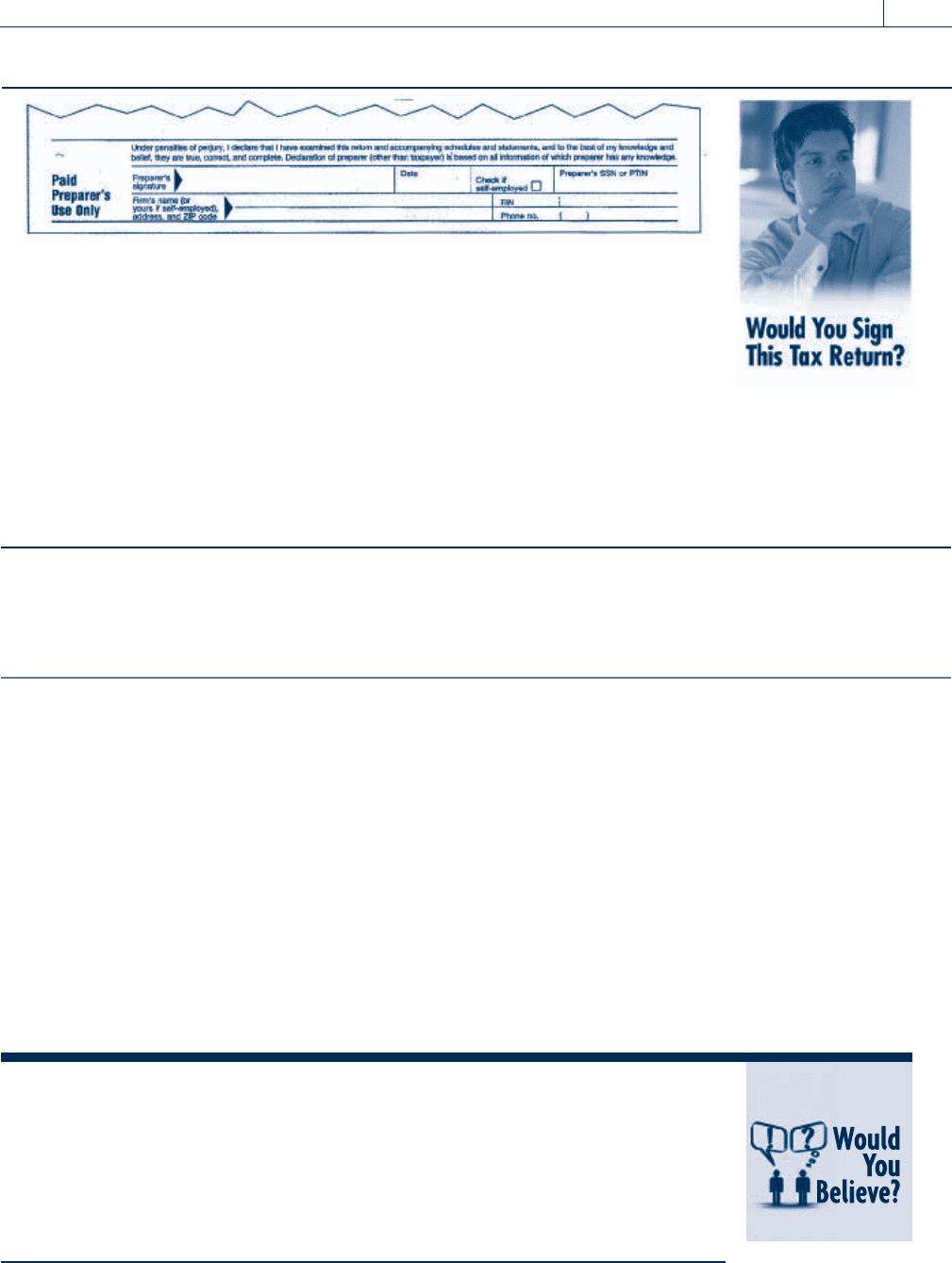

For the last 10 years, you prepared the joint tax returns for Dominic (hus-

band; age 40) and Dulce (wife; age 35) Divorcio. Last year they got a divorce

and remained as your separate tax clients. Under the dissoluti on decree,

Dominic has to pay Dulce $2,500 per month alimony, which he does for the

current year. You have completed Dominic’s tax return for the current year

and you deducted the required alimony payments to Dulce on Dominic’s

Form 1040. Dulce came in to have you prepare her tax return and refused

to report her alimony received as income. She stated, ‘‘I am not going to

pay tax on the $30,000 from Dominic.’’ She views the payments as ‘‘a gift

for putting up with him for all those years of marriage.’’ Dulce will not

budge on excluding this alimony from income. Would you sign the Paid Pre-

parer’s declaration (see example above) on this return? Why or why not?

Section 2.4

Prizes and Awards 2-11

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Van enters a drawing and wins a new automobile. The automobile

has a window sticker price of $20,200. The fair market value of the

prize should be included in Van’s gross income, but the fair market

value is probably not the window sticker price; instead, it is the price

at which a similar car normally would be sold. N

SECTION 2.5

ANNUITIES

When taxpayers consider retirement, they often purchase annuities. An annuity is a type of

investment in which the taxpayer purchases the right to receive periodic payments for the

remainder of his or her life. The amount of each periodic payment is based on the annuity

purchase price and the life expectancy of the annuitant. Standard mortality tables, based on

the current age of the annuitant, are used to calculate the annuity amount.

The General Rule

Each annuity payment received by a taxpayer has both an element of taxable income and an

element of tax-free return of the original purchase price. To calculate the taxable and non-

taxable portions of the payment, the tax law includes an exclusion ratio. The portion of

thepaymentthatmaybeexcludedfromincomeisbasedontheratiooftheinvestment

in the contract to the total expected return. The investment in the contract is the total

of the amounts paid by the taxpayer. The total expected return is equal to the annual pay-

ment multiplied by the life expectancy of the annuitant, based on mortality tables provided

by the IRS. This calcu lation of the amount excluded from the taxpayer’s incom e may be

summarized as follows:

Amount Excluded ¼

Investment in the Contract

Annual Payment Life Expectancy

Amount Received

Once the exclusion ratio is calculated for an annuity, it remains constant, even if the

annuitant’s situation changes. For example, the ratio would not change if the annuitant dis-

covers tha t he or she has cancer and is expected to live only 2 more year s. For annuities

Self-Study Problem 2.4

For each of the follow ing independent cases, indicate the amount of gross

income that should be included on the taxpayer’s return.

Gross Income

1. Helen enters a radio contest and wins $2,000. $ ____________

2. In 2010, Professor Deborah wins an award of $10,000

for a book on literature she published 4 years ago. The

award was presented in recognition of her past literary

achievements.

$ ____________

3. Bill is a professional baseball player. Because he has hit

50 home runs this season, he was given a new wrist watch

worth $2,500. $ ____________

4. John is an employee of Big Corporation. He is awarded

$5,000 for a suggestion to improve the plant layout. $ ____________

2-12 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

starting after 1986, including those under the simplified method discussed on the following

page, the maximum amount excludable is limited to the taxpayer’s investment in the annuity.

After the taxpayer’s investment is recovered, all additional amounts received are fully taxable.

If the taxpayer dies before the entire investment in the contract is recovered, then any unrec-

overed amount is recognized as a loss on the annuitant’s tax return for the year of death.

If the annuity began before 1987, the exclusion ratio is used for the life of the annuitant,

even after the taxpayer has recovered all of the investment in the annuity. Alternatively, if

the annuitant dies before recovering his or her entire investment in the contract, the unrec-

overed portion is lost.

EXAMPLE Allen purchases an annuity for $100,000 which pays him $12,000 per

year for life. At the date of purchase, his life expectancy is 10 years.

If he receives $12,000 in the current year, the amount excluded under

the general rule is calculated as follows:

$100,000

$12,000 10 years

$12,000 ¼ $10,000 exclusion

The taxable portion is $2,000, which is the total payment of

$12,000 less the $10,000 exclusion. N

The Simplified Method

Individual taxpayers generally must use the ‘‘simplified’’ method, instead of the general

rule just discussed, to calculate the taxable amount from an annuity for annuities starting

after November 18, 1996. Nonqualified plan annuities and certain annuitants age 75 and

over must still use the general rule.

To calculate the excluded amount, the IRS provides the following worksheet.

Simplified Method Worksheet

1. Enter total amount received this year. 1. ____________

2. Enter cost in the plan at the annuity starting date. 2. ____________

3. Age at annuity starting date

Enter

55 and under 360

56–60 310

61–65 260 3. ____________

66–70 210

71 and older 160

4. Divide line 2 by line 3. 4. ____________

5. Multiply line 4 by the number of month ly payments

this yea r. If the annuity starting date was before 1987,

also enter this amount on line 8, and skip lines 6 and 7.

Otherwise, go to line 6.

5. ____________

6. Enter the amount, if any, recovered tax free in prior years. 6. ____________

7. Subtract line 6 from line 2. 7. ____________

8. Enter the smaller of line 5 or 7. 8. ____________

9. Taxable amount this year: Subtra ct line 8 from line 1. Do

not enter less than zero.

9. ____________

Section 2.5

Annuities 2-13

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Note 1: The denominators provided in step 3 above are effective for annuity

starting dates after November 18, 1996. For annuity starting dates prior to

November 18, 1996, see any standard tax service.

Note 2: When annuity benefits with starting dates after 1997 are paid over two

lives (joint and survivor annuities), a different set of denominators must be used

in step 3.

Combined Age

of Annuitants

Number of

Payments

110 or less 410

111–120 360

121–130 310

131–140 260

141 and over 210

EXAMPLE Joey, age 67, began receiving benefits under a joint and survivor

annuity to be paid over the joint lives of himself and his wife Jody,

who is 64. He received his first annuity payment in March of the

current year. Joey contributed $38,000 to the annuity and he had no

distributions from the plan before the current year. The monthly

payment to Joey is $1,700.

Joey must use the simplified method to calculate his taxable

amount. Using the worksheet, Joey’s taxable amount for the current

year would be:

Simplified Method Worksheet

1. Enter total amount received this year. 1. $17,000.00

2. Enter cost in the plan at the annuity

starting date.

2.

$38,000.00

3. Combined age at annuity starting date

Enter

110 or less 410

111–120 360

121–130 310 3.

260

131–140 260

141 and over 210

4. Divide line 2 by line 3. 4.

$146.15

5. Multiply line 4 by the number of monthly pay-

ments this year.

5.

$1,461.50

6. Enter the amount, if any, recovered tax free in

prior years.

6.

0.00

7. Subtract line 6 from line 2. 7.

$38,000.00

8. Enter the smaller of line 5 or 7. 8.

$1,461.50

9. Taxable amount this year: Subtrac t line 8 from

line 1. Do not enter less than zero. N

9.

$15,538.50

2-14 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Employee Annuities

Many employees participate in retirement plans organized by their employers. Employers

generally make periodic payments to the plans on behalf of their employees. If the pay-

ments are made to qualified retirement plans, contributions by the employer are not tax-

able to the employees in the current year. Since the contributions are not taxable when

made, they are not considered part of the employee’s investment in the contract when cal-

culating the exclusion ratio.

SECTION 2.6

LIFE INSURANCE

Life insurance proceeds are excluded from gross income based on the premise that it would

be inappropriate in a time of need to tax the proceeds from a life insurance policy. There-

fore, a major exclusion from gross income is provided for life insurance proceeds. To be

excluded, the proceeds must be paid to the beneficiary by reason of the death of the

Self-Study Problem 2.5

Part a

Phil retired in January 2010 at age 63. His pension is $1,500 per month from a

qualified retirement plan to which Phil contributed $42,500. Phil’s life expec-

tancy is 21 years, and this year he received eleven payments for a total pension

income of $16,500. Calculate Phil’s taxable income from the annuity in the cur-

rent year, using the general rule.

$ ____________

Part b

Calculate Phil’s taxable income using the following Simplified Method Worksheet.

Simplified Method Worksheet

1. Enter total amount received this year. 1. ____________

2. Enter cost in t he plan at the annuity starting date. 2. ____________

3. Age at annuity s tarting date

Enter

55 and under 360

56–60 310

61–65 260 3. ____________

66–70 210

71 and older 160

4. Divide line 2 by line 3. 4. ____________

5. Multiply line 4 by the number of monthly payments this

year. If the annuity starting date was before 1987, also

enter this amount on line 8, and skip lines 6 and 7.

Otherwise, go to line 6. 5. ____________

6. Enter the amount, if any, recovered tax free in prior years. 6. ____________

7. Subtract line 6 from line 2. 7. ____________

8. Enter the smaller of line 5 or 7. 8. ____________

9. Taxable amount this year: Subtract line 8 from line 1.

Do not enter less than zero.

9. ____________

Section 2.6

Life Insurance 2-15

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

insured. If the proceeds are taken over several years instead of in a lump sum, the insurance

company pays interest on the unpaid proceeds. The interest is generally taxable income.

Early payouts of life insurance, also called accelerated death benefits or viatical settle-

ments, are excluded from gross income for certain terminally or chronically ill taxpayers.

The taxpayer may either collect an early payout from the insurance company or sell or assign

the policy to a viatical settlement provider. A terminally ill individual must be certified by a

medical doctor to have an illness which is reasonably expected to cause death within

24 months. A chronically ill individual must be certified by a medical doctor as unable to

perform daily living activities without assistance. Chronically ill taxpayers may only exclude

gain on accelerated death benefits to the extent proceeds are used for long-term care.

If an insurance policy is transferred to another person for valuable consideration, all or a

portion of the proceeds from the life insurance policy may be taxable to the recipient. For

example, taxable proceeds result when a policy is transferred to a creditor in payment of a

debt. When a transfer for value occurs, the proceeds at the death of the insured are taxable

to the extent they exceed the cash surrender value of the policy at the time it was transferred,

plus the amount of the insurance premiums paid by the purchaser. There is an exception to the

rule that policies transferred for valuable consideration result in taxable proceeds. Transfers to

a partner of the insured, a partnership in which the insured is a partner, or a corporation in

which the insured is an officer or a shareholder do not cause the policy proceeds to be taxable.

EXAMPLE Howard dies on January 15, 2008, and leaves Wanda, his wife, a

$50,000 insurance policy, the proceeds of which she elects to receive

as $10,000 per year plus interest for 5 years . In the current year,

Wanda receives $12,200 ($10,000 þ $2,200 interest). She must include

the $2,200 of interest in income. N

EXAMPLE David owns a life insurance policy at the time he is diagnosed with a

terminal illness. After his diagnosis, he sells the policy to Viatical

Settlements, Inc., for $100,000. David is not required to include the

gain on the sale of the insurance in his gross income. N

EXAMPLE Amy transfers to Bill an insurance policy with a face value of $40,000

and a cash surrender value of $10,000 for the cancellation of a debt

owed to Bill. Bill continues to make payments, and after 2 years Bill

has paid $2,000 in premiums. Amy dies and Bill collects the $40,000.

Since the transfer was for valuable consideration, Bill must include

$28,000 in taxable income, which is equal to the $40,000 total pro-

ceeds less $10,000 value at the time of transfer and $2,000 of premi-

ums paid. If Amy and Bill were partners in the same partnership, the

entire proceeds ($40,000) would be tax free. N

Self-Study Problem 2.6

On March 19, 2008, Karen dies and leaves Larry an insurance policy with a face

value of $100,000. Karen is Larry’s sister, and Larry elects to take the proceeds over

10 years ($10,000 plus interest each year). This year Larry receives $13,250 from

the insurance company. How much income must Larry report for the current year?

$ ____________

2-16 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 2.7

GIFTS AND INHERITANCES

Taxpayers are allowed to exclude from income the fair market value of gifts and inheritan-

ces received, but income received from the property after such a transfer is taxable. Nor-

mally, the gift tax or estate tax is paid by the donor or the decedent’s estate; such property is

therefore usually tax free to the person receiving the gift or inheritance.

One tax problem that may arise concerning a gift is the definition of what constitutes

a gift. The courts define a gift as a voluntary transfer of property without adequate con-

sideration. Gifts made in a business setting are suspect since they may be disguised pay-

ments for goods or services. The courts are likely to rule that gifts in a business setting

are taxable income, even if there was no obligation to make the payment. Also, if the

recipient renders services for the gift, it will be presumed to be income for the services

performed.

EXAMPLE In January of the current year, Richard inherits shares of Birch Corpo-

ration stock worth $22,000. After receiving the stock, he is paid

$1,300 in dividends during the current year. His gross income from

the inheritance in the current year would be $1,300. The $22,000 fair

market value of the stock is excluded from gross income. N

SECTION 2.8

SCHOLARSHIPS

A scholarship is an amount paid or awarded to, or for the benefit of, a student to aid the

student in the pursuit of his or her studies. Scholarships granted to degree candidates are

taxable income, with the exception of amounts spen t for tuition, fees, books, and course-

required supplies and equipment. Therefore, scholarship amounts received for such

items as room and board are taxable to the recipient.

EXAMPLE In 2010, Diane receives a $5,000 scholarship to study accounting at

Big State University. Diane’s expenses for tuition and books amount

to $1,200 during the fall semester; therefore, she would have taxable

income of $3,800 ($5,000 $1,200) from the scholarship. N

Payments received by stude nts for part-time employment are not excludable; they are

taxable as compensation. For example, students in work–study programs must include

their compensation in gross income.

Self-Study Problem 2.7

Don is an attorney who supplied a list of potential clients to a new attorney,

Lori. This list aided in the success of Lori’s practice. Lori was very pleased and

decided to do something for Don. In the current year, Lori gives Don a new

car worth $40,000. Lori was not obligated to give this gift to Don, and she did

not expect Don to perform future services for the gift. How much income, if

any, should Don report from this transaction? Explain your answer.

Income $ ____________________

Explain____________________________________________________________________

___________________________________________________________________________

Section 2.8

Scholarships 2-17

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 2.9

ACCIDENT AND HEALTH INSURANCE

Many taxpayers are covered by accident and health insurance plans. These plans pay for the

cost of medical care of the taxpayer and any dependents who are insured under the plan.

The taxpayer may pay the total premiums of the plan, or his or her employer may pay

part or all of the premiums. Taxpayers are allowed liberal exclusions for payments received

from these accident and health plans. The taxpayer may exclude the total amount received

for payment of me dica l care . This exclusion applies to any amount p aid for the medical

care of the taxpayer, his or her spouse, or dependents. The payment may be made to

the doctor, the hospital, or the taxpayer as reimbursement for the payment of the expenses.

In addition, any premiums paid by a taxpayer’s employer are excluded from the taxpayer’s

income, and the premium payments may be deducted by the employer.

Most accident and health-care policies also pay fixed amounts to the insured for loss of

the use of a member or function of the body. These amounts may also be excluded from

income. For example, a taxpayer who receives $25,000 because he or she is blinded in

one eye may exclude the $25,000 from income.

EXAMPLE Bob is a married taxpayer. His employer pays a $250 per month pre-

mium on a policy covering Bob and his family. Jean, Bob’s wife, is sick

during the year and her medical bills amount to $6,500; the insurance

company paid $6,000 for the bills. Bob and Jean may exclude from

income the $250 per month premium paid by Bob’s employer and the

$6,000 paid by the insurance company. The $500 not paid by the

insurance company is deductible on Bob and Jean’s return, subject to

the medical expense deduction limitations (see Chapter 5). N

Self-Study Problem 2.8

Indicate whether each item below would be included in or excluded from the

income of the recipient in 2010.

Included Excluded

1. A $2,000 National Merit scholarship for tuition ___________ ___________

2. A basketball scholarship for room and board ___________ ___________

3. Payments under a work–study program ___________ ___________

4. Salary for working at Beech Research Laboratory ___________ ___________

5. A stipend for a graduate teaching assistant ___________ ___________

6. Payment received from an employer while on

leave working on a research project

___________ ___________

Self-Study Problem 2.9

Marjorie, a single taxpayer, is an employee of Big State Corporation. Big State

Corporation pays premiums of $1,000 on her health insurance for the current

year. Also, during the current year, Marjorie has an operat ion for which the

insurance company pays $5,000 to her hospital and doctor. Of the above

amounts, how much must Marjorie include in her gross income?

$ ____________

2-18 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 2.10

MEALS AND LODGING

If certain tests are met, employers may exclude the value of meals and lodging from an

employee’s taxable income. The exclusion is granted for any meals and lodging furnished

by the employer for the convenience of the employer, but only if:

1. The meals are furnished on the business premises of the employer during working

hours because the taxpayer must be available for emergency calls or the employer

limits the employee to short meal periods, and

2. The lodging is on the business premises and must be accepted as a requirement for

employment.

To exclude the value of lodging provided by the employer, the employee must be

required to accept the lodging to perform the duties of the job properly. Fo r example, a

taxpayer who receives lodging on an offshore oil rig may exclude the value of the lodging

from income, since the employee cannot go home at night. The exclusion for lodging also

includes the value of utilities such as electricity, water, heat, gas, and similar items that

make the lodging habitable.

The value of meals or lodging provided by the employer in other situations, and cash

allowances for meals or lodging, must be included in the employee’s gross income.

SECTION 2.11

MUNICIPAL BOND INTEREST

In 1913 when the Sixteenth Amendment was enacted, Congress questioned the constitu-

tionality of taxing the interest earned on state and local government obligations. Congress

provided an exclusion from taxpayers’ income for the in terest on such bonds. To qualify for

Self-Study Problem 2.10

In each of the following independent cases, indicate whether the value of the

meals or lodging should be included in or excluded from the taxpayer’s income.

Included Excluded

1. A waiter is required to eat lunch, furnished by

his employer, on the premises during a busy

lunch hour.

___________ ___________

2. A police officer receives a cash allowance to

pay for meals while on duty.

___________ ___________

3. A worker receives lodging at a remote

construction site in Alaska.

___________ ___________

4. A taxpayer manages a motel and, although

the owner does not require it, she lives at the

motel rent free.

___________ ___________

5. A bank teller is furnished meals on the premises

to limit the time she is away during busy hours.

___________ ___________

6. A hospital provides a free lunchroom for its staff;

the staff is not required to eat there, but the

hospital’s administration wants to encourage the

employees to be on the premises for emergencies.

___________ ___________

Section 2.11

Municipal Bond Interest 2-19

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

the exclusion, the interest must be from an obligation of a state, territory, or possession of

the United States, or a political subdivision of the foregoing or of the District of Columbia.

The interest exclusion allows high-income taxpayers to lend money to state and local

governments at lower interest rates (discounts). For example, a taxpayer in the 33 percent

tax bracket can receive the same after-tax return on a 6 percent municipal bond as he or she

can receive on an 8.96 percent corporate bond. This equivalent after-tax return rate for a

tax-free bond can be calculated as follows:

After-tax return ¼

Tax-free interest rate

1 the taxpayer’s tax rate

Taxpayers in low tax brackets are likely to find that they earn a higher overall

return investing in taxable bonds rather than comparable tax-free municipal bonds.

This is because the smaller tax benefit from the municipal bonds doesn’t make up

for the reduced interest rate paid on municipal bonds. Municipal bonds are also

generally not appropriate investments for IRAs or other retirement accounts since

income on these accounts is excluded from tax until withdrawn, anyway.

SECTION 2.12

SOCIAL SECURITY BENEFITS

Many taxpayers may exclude all of their Social Security benefits from gross income. Middle

and upper income Social Security recipients, however, may have to include up to 85 per-

cent of their benefits in gross income. The formula to determine taxable Social Security

income is based on modified adjusted gross income (MAGI). Generally, MAGI is the tax-

payer’s adjusted gross income (without Social Security benefits) plus any tax-free interest

income. On rare occasions, taxpayers will also have to add back unusual items such as

the foreign earned income exclusion, employer-provided adoption benefits, or interest

on education loans. If MAGI plus 50 percent of Social Security benefits is less than the

base amount shown below, benefits are excluded from income.

Base Amounts Applies to

$32,000 Married filing jointly

$0 Married taxpayers who did not live apart for the entire

year and still filed separate returns

$25,000 All other taxpayers

Self-Study Problem 2.11

Calculate the taxable interest rate that will provide the equivalent after-tax

return in the cases that follow.

1. A taxpayer is in the 28 percent tax bracket and invests in a San Diego City

Bond paying 7 percent. What taxable interest rate will provide the same

after-tax return?

____________ %

2. A taxpayer is in the 33 percent tax bracket and invests in a New York State

Bond paying 6.5 percent. What taxable interest rate will provide the same

after-tax return?

____________ %

2-20 Chapter 2

Gross Income and Exclusions

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.