Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

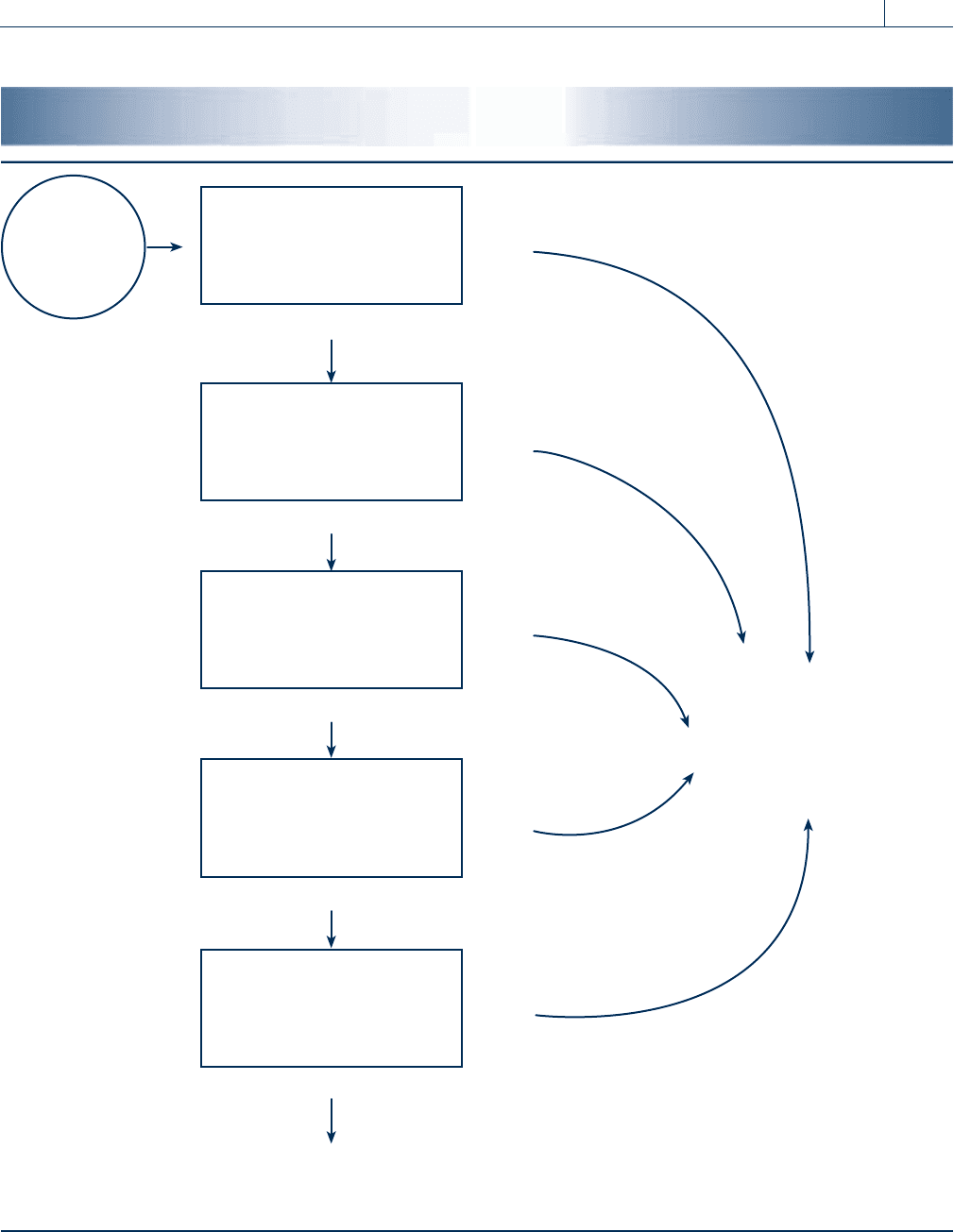

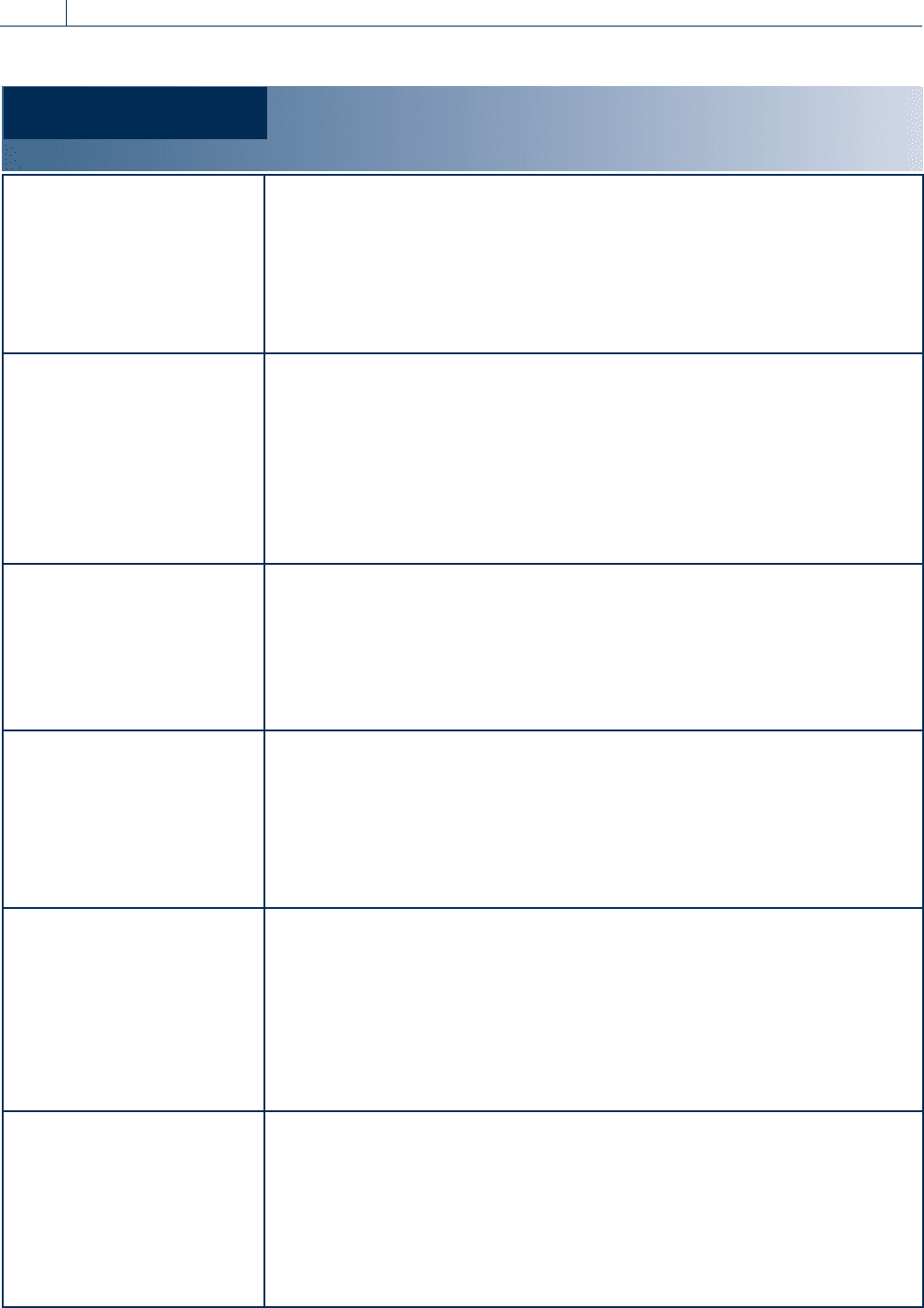

FIGURE 1.5 DEPENDENCY EXEMPTION TESTS

FLOW CHART FOR QUALIFYING RELATIVE

Yes

Yes

Yes

No

NO

DEPENDENC

Y

EXEMPTION

DEPENDENCY

EXEMPTION

Yes

No

No

No

No

Yes

Was the support

test met?

U.S. Citizen or

resident of U.S.,

Mexico, Canada?

Was the joint

return test

met?

Was the relationship

or member of house-

hold test met?

Is gross income

less than $3,650

(for 2010)?

START

Section 1.6

Personal and Dependency Exemptions 1-19

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Self-Study Problem 1.6

Indicate in each of the following independent situations the number of

exemptions the taxpayer should claim on their 2010 income tax returns. If a

test is not mentioned, you should consider that it is met.

______

1. Abel is 72 years old and married. His wife is 64 and meets the test for

blindness. How many exemptions should they claim on a joint return?

______

2. Betty and Bob are married and have a 4-year-old son. During the year

Betty gave birth to a baby girl. How many exemptions should Betty

and Bob claim on a joint return?

______

3. Charlie supports his 26-year-old brother, who is a full-time student.

His brother’s gross income is $4,500 from a part-time job. How many

exemptions should Charlie claim on his return?

______

4. Donna and her sister support their mother and provide 60 percent of

her support. If Donna provides 25 percent of her mother’s support

and her sister signs a multiple support agreement giving Donna the

exemption, how many exemptions should Donna claim on her return?

______

5. Frank is single and supports his son and his son’s wife, both of whom

lived with him for the entire year. The son (age 20) and his wife (age

19) file a joint return to get a refund, reporting $2,500 ($2,000 earned

by the son) in gross income. Both the son and daughter-in-law are full-

time students. How many exemptions should Frank claim on his return?

______

6. Gary is single and pays $5,000 towards his 20-year-old daughter’s col-

lege expenses. The remainder of her support is provided by a $9,500

tuition scholarship. The daughter is a full-time student. How many

exemptions should Gary claim on his return?

______

7. Helen is 50 years old and supports her 72-year-old mother, who is

blind and has no income. How many exemptions should Helen claim

on her return?

Your clients, Adam and Amy Accrual, have a 21-year-old daughter named

April. April is single and is a full-time student studying for her bachelor’s

degree in accounting at California Poly Academy (CPA) in Pismo Beach, Califor-

nia, where she lives with her roommates year-round. Last year April worked at

a local bar and restaurant 4 nights a week and made $18,000, which she used

for tuition, fees, books, and living expenses. Her parents help April by sending

her $300 each month to help with her expenses at college. This is all of the

support given to April by her parents. When preparing Adam and Amy’s tax

return you note that they claim April as a dependent for tax purposes. Adam is

insistent that they can claim April because of the $300 per month support and

the fact that they ‘‘have claimed her since she was born.’’ He will not let you

take April off his return as a dependent. Would you sign the Paid Preparer’s

declaration (see example above) on this return? Why or why not?

1-20 Chapter 1

The Individual Income Tax Return

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 1.7

THE STANDARD DEDUCTION

The standard deduction was placed in the tax law to provide relief for taxpayers with few

itemized deductions. The amount of the standard deduction is subtracted fro m adjusted

gross income by taxpayers who do not itemize their deductions. If a taxpayer’s gross

income is less than the standard deduction amount, the taxpayer has no taxable income.

The standard deduction amounts are presented below:

Filing Status 2010 Standard Deduction

Single $ 5,700

Married, filing jointly 11,400

Married, filing separately 5,700

Head of household 8,400

Qualifying widow(er) 11,400

Taxpayers may be able to reduce taxes by itemizing deductions on Schedule A

of Form 1040 rather than claiming the standard deduction. The U.S. General

Accounting Office has estimated that close to a billion dollars a year may be lost

by taxpayers who failed to itemize their deductions.

Additional Amounts for Old Age and Blindness

Taxpayers who are 65 years of age or older or blind are entitled to an additional standard

deduction amount. For 2010, the additional standard deduction amount is $1,400 for

unmarried taxpayers and $1,100 for married taxpayers and qualifying widows or widowers.

Taxpayers who are both at least 65 years old and blind are entitled to two additional stan-

dard deduction amounts. The additional standard deduction amounts are also available for

the taxp ayer’s spouse, but not for dependents. An individual is considered blind for pur-

poses of receiving an additional standard deduction amount if:

1. Central visual acuity does not exceed 20/200 in the better eye with correcting

lenses, or

2. Visual acuity is greater than 20/200 but is limited to a field of vision not greater than

20 degrees.

EXAMPLE John is single and 70 years old in 2010. His standard deduction is

$7,100 ($5,700 plus an additional $1,400 for being 65 years of age or

older). N

EXAMPLE Bob and Mary are married in 2010 and file a joint return. Bob is age

68, and Mary is 63 and meets the test for blindness. Their standard

deduction is $13,600 ($11,400 plus $1,100 for Bob being 65 years or

older and another $1,100 for Mary’s blindness). N

For 2008 and 2009, and likely 2010 if the law is extended as expected, taxpayers

are allowed an addition to the standard deduction amounts shown above if

they paid property taxes on a principal residence. The additional standard

deduction amount is limited to the lesser of $500 ($1,000 for joint filers) or

real estate taxes paid. This addition to the standard deduction is covered

more fully in Chapter 5. Plea se see the Whittenburg Web site for information

on laws pending as we go to press.

Section 1.7

The Standard Deduction 1-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Individuals Not Eligible for the Standard Deduction

The following taxpayers cannot use the standard deduction, but must itemize instead:

1. A married individual filing a separate return, whose spouse itemizes deductions.

2. A nonresident alien.

3. An individual filing a short-period tax return because of a change in the annual

accounting period.

EXAMPLE Ed and Ann are married individuals who file separate returns for

2010. Ed itemizes his deductions on his return. Ann’s adjusted gross

income is $12,000, and she has itemized deductions of $900. Ann’s

taxable income is calculated as follows:

Adjusted gross income $12,000

Itemized deductions (900)

Exemption amount

(3,650)

Taxable income

$ 7,450

Since Ed itemizes his deductions, Ann must also itemize deductions

and is not entitled to use the standard deduction amount. N

Special Limitations for Dependents

The standard deduction is limited for the tax return of a dependent. The total standard

deduction may not exceed the greater of $950 or the sum of $300 plus the dependent’s

earned income up to the basic standard deduction amount in total (for example, $5,700

for single taxpayers), plus any additional standard deduction amount for old age or blind-

ness. The standard deduction amount for old age and blindness is only allowed when a

dependent files a tax return. It is not allowed to increase the standard deduction of the tax-

payer claiming the dependent. Also, remember that a dependent may not claim a personal

exemption on his or her own return.

EXAMPLE Penzer, who is 4 years old, earned $6,500 as a child model during 2010. A

dependency exemption for Penzer is claimed by his parents on their tax

return. Penzer is required to file a tax return, and his taxable income will

be $800 ($6,500 less $5,700, the standard deduction amount). He is not

allowed to claim an exemption for himself. If Penzer had earned only $400,

his standard deduction would be $950 (the greater of $950 or $700 [$400 þ

$300]) and he would not owe any tax or be required to file a return. N

Self-Study Problem 1.7

Indicate in each of the following independent situations the amount of the stan-

dard deduction the taxpayers should claim on their 2010 income tax returns.

______

1. Adam is 45 years old, in good health, and single.

______

2. Bill and Betty are married and file a joint return. Bill is 66 years old,

and Betty is 60.

______

3. Charlie is 70, single, and blind.

______

4. Debbie qualifies for head of household filing status, is 35 years old,

and is in good health.

______

5. Elizabeth is 9 years old, and her only income is $3,600 of interest on a sav-

ings account. She is claimed as a dependent on her parents’ tax return.

______

6. Frank and Freida are married with two dependent children. They file a joint

return, are in good health, and both of them are under 65 years of age.

1-22 Chapter 1

The Individual Income Tax Return

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

In the spring of 2010, Congress passed health care legislation with the goal of

providing coverage over the next several years for many millions of Americans

who are currently not covered by health insurance. This may be one of the most

significant pieces of s ocial legislation passed in our lifetime, and much of it is

administered and enforced through our tax system. The following is a summary

of some tax elements of the health care legislation and the phase-in dates:

Tax Rates Beginning in 2013, high-income taxpayers (modified AGI over

$200,000 for single taxpayers and over $250,000 for married taxpayers) will

be subject to a new Medicare tax on most income. Please see Sections 4.10,

9.3, and 9.6 for coverage of the Medicare tax in 2010. The 2013 tax will be an

additional .9 percent on most earned income which is already subject to the

Medicare tax, and an additional 3.8 percent on most investment income, includ-

ing capital gains, interest, dividends and rental income. Distributions from IRAs

and retirement plans and municipal bond interest will be exempt from this tax.

Extended Coverage for Adult Children Beginning in 2010, any health plan

whichcoversdependentsmustbeextendedtoallowforcoverageofmost

unmarried adult children through age 26.

Small Employer Health Insurance Credit In 2010, small employers will be

allowed a credit for health insurance provided to workers who are not owners

and who meet certain criteria. This credit will continue with differing req uire-

ments through 2015.

Itemized Deduction Threshold Increases Beginning in 2013, the AGI thresh-

old for deducting medical expenses as an itemized deduction will increase from

7.5 percent to 10 percent of AGI, with a temporary reprieve for seniors age 65

or older.

Refundable Premium Assistance Credit Beginning in 2014, a tax return

credit will be allowed to help subsidize the purchase of health insurance

through new health benefit ‘‘exchanges’’ for certain low-income taxpayers.

Tax Return Penalty for Failure to Maintain Coverage Beginning in 2014, tax-

payers must have qualifying health coverage for themselves and their depend-

ents or be subject to a penalty which will be reported and paid on their

personal tax return.

‘‘Play or Pay’’ Penalty for Large Employers Not Offering Required Health

Insurance Beginning in 2014, large employers will be assessed penalties for

not offering health coverage. The calculation of the penalty is complex and

depends on many variables such as type of coverage provided by the employer

and income levels of the employees.

SECTION 1.8

A BRIEF OVERVIEW OF CAPITAL GAINS AND LOSSES

When a taxpayer sells an asset, there is normally a gain or loss on the transaction. Depend-

ing on the kind of asset sold, this ga in or loss will have different tax consequences. Chapter

8 of this text has detailed coverage of the effect of gains and losses on a taxpayer’s tax lia-

bility. Because of their importance to the understanding of the calculation of an individual’s

tax liability, however, a brief overview of gains and losses will be discussed here.

The amount of gain or loss realized by a taxpayer is determined by subtracting the

adjusted basis of the asset from the amou nt realized . Generally, the adjusted basis of an

asset is its cost less any depreciation (covered in Chapter 7) taken on the asset. The amount

realized is generally what the taxpayer receives from the sale (e.g., the sales price less any

cost of the sale). The formula for calculation of gain or loss can be stated as follows:

Gain (or loss) ¼ Amount realize d Adjusted basis

Section 1.8

A Brief Overview of Capital Gains and Losses 1-23

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Most gains and losses realized are also recognized for tax purposes. That is, most gains

or losses that occur are included in the taxpayer’s taxable income. The exceptions to this

general tax recognition rule are discussed in Chapter 8.

EXAMPLE Lisa purchased a rental house a few years ago for $100,000. Total

depreciation to date on the house is $25,000. In the current year she

sells the house for $155,000 and receives $147,000 after paying selling

expenses of $8,000. Her gain on the sale is $72,000 calculated as follows:

Amount realized ($155,000 $8,000) $147,000

Adjusted basis ($100,000 $25,000)

75,000

Gain realized

$ 72,000

This gain realized will be recognized as a taxable gain. N

Capital Gains and Losses

Gains and losses can be either ordinary or capital. Ordinary gains and losses are treated for tax

purposes just like other items such as salary and interest, and they are taxed at ordinary rates.

In general, a capital asset is any property (either personal or investment) held by a taxpayer, with

certain exceptions as listed in the tax law (see Chapter 8). Typical assets that are not capital assets

are inventory and accounts receivable. Examples of capital assets held by individual taxpayers

include stocks, bonds, land, cars, boats, and other items held as investments or for personal use.

The rates on long-term (held more than 12 months) capital gains are summarized as follows:

Ordinary Tax Bracket 2010 Capital Gains Tax Rate

10% and 15% 0%

All others 15%

Gain from property held 12 months or less is deemed to be short-term capital gain and

is taxed at ordinary income tax rates (i.e., up to a maximum rate of 35 percent in 2010).

EXAMPLE In 2010, Chris sells AT&T stock for $25,000. He purchased the stock

5 years ago for $15,000, giving him an adjusted basis of $15,000 and

a long-term gain of $10,000. Chris’ taxable income without the sale of

the stock is $190,000, which puts him in the 33 percent tax bracket.

The tax due on the long-term capital gain would be $1,500 (15%

$10,000) instead of $3,300 (33% $10,000) if the gain on the stock

were treated as ordinary income. N

When calculating gain or loss, the taxpayer must net all capital asset transactions to

determine the nature of the final gain or loss (see Section 8.4 for a discussion of this cal-

culation). If an individual taxpayer ends up with a net capital loss (short-term or long-

term), up to $3,000 per year can be deducted against ordinary income . The net loss not

used in the current year may be carried forward and used to reduce taxable income in

future years (see Section 8.5 for a discussion of capital losses). Losses from capital assets

held for persona l purposes, such as a non-bu siness auto or a per sonal residence, are not

deductible, even though gains on personal assets are taxable.

Taxpayers may wish to postpone the sale of capital assets until the hol ding

period is met to qualify for the preferential long-term capital gains rate. Of

course, there is always the risk that postponing the sale of a capital asset such as

stock may result in a loss if the price of the stock decreases below its cost during

volatile markets. The economic risks of a transaction should always be considered

along with the tax benefits.

1-24 Chapter 1

The Individual Income Tax Return

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Amy purchased gold coins as an investment. She paid $50,000 for the

coins. This year she sells the coins to a dealer for $35,000. As a result,

Amy has a $15,000 capital loss. She may deduct $3,000 of the loss

against her other income this year. The remaining unused loss of

$12,000 ($15,000 $3,000) is carried forward and may be deducted

against other income in future years. Of course, the carryover is

subject to the $3,000 annual limitation in future years. N

Volunteer Income Tax Assistance Program (VITA)

Many universities and colleges run VITA sites in conjunction with their accounting pro-

grams. This is a small but vital part of the VITA program r un by the IRS. The majority

of the VITA sites are not run by schools, but rather by community groups, such as

churches, senior groups (AARP), military bases, etc. If a student has a chance to participate

in a VITA program, he or she should do so if at all possible . The experience provides val-

uable insight into preparing tax returns for others.

The following is a brief description of the program from the IRS Web site

(www.irs.gov): The VITA Program offers free tax help to low-to-moderate-income (gen-

erally, $49,000 and below) people who cannot prepare their own tax returns. Certified vol-

unteers sponsored by various organizations receive training to help prepare basic tax

returns in communities across the country. VITA sites are generally located at community

and neighborhood centers, lib raries, school s, shopping malls, and other convenient loca-

tions. Most locations also offer free electronic filing. Please see the IRS Web site to locate

the nearest VITA site and for more information.

SECTION 1.9

TAX AND THE INTERNET

Taxpayers and tax practitioners can find a substantial amount of useful information on the

Internet. The Internet is a global communica tion system that connects millions of co m-

puters throughout the world. Government agencies, businesses, organizati ons, and groups

(e.g., the IRS, H&R Block, and Cengage Learning) maintain sites that contain information

of interest to the public.

The information available on various Web sites is subject to rapid change. Discussed

below are some current Internet sites that are of interest to taxpayers. Taxpayers should

be aware that the locations and information provided on the Internet are subject to change

by the site organizer without notice.

Self-Study Problem 1.8

Erin purchased stock in JKL Corporation several years ago for $8,750. In the

current year, she sold the same stock for $12,800. She paid a $200 sales

commission to her stockbroker.

1. What is Erin’s amount realized? $ ______________

2. What is Erin’s adjusted basis? $ ______________

3. What is Erin’s realized gain or loss? $ ______________

4. What is Erin’s recognized gain or loss? $ ______________

5. How is any gain or loss treated for tax purposes?

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Section 1.9

Tax and the Internet 1-25

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The IRS site, www.irs.gov

One of the most useful sites containing tax information is the one maintained by the IRS.

There are several places a taxpayer can enter the IRS site. Entering the main IRS site

shown above and clicking on Site Map provides one of the best entrances because it allows

the user to quickly scan information available from the IRS. Once a user has reached this Inter-

net page, he or she is provided quick links to other useful pages contained within the IRS site.

In addition, the IRS site has a search fu nction to assist users in locating information.

The Forms and Publications (www.irs.gov/formspubs/index.html) search function is

particularly useful and allows the user to locate and download almost any tax form or

publication available from the IRS. A help function is available to aid users of the IRS

site. E-mail access to the IRS is provided for users who have questions or want to commu-

nicate with the IRS. The IRS has also launched a YouTube video site and an iTunes pod-

cast site. The YouTube site has numerous educational videos including a series called

‘‘Your Guide to an I RS Audit’’ and others describing IRS careers, such as ‘‘Special

Agent’’ and ‘‘Revenue Agent.’’

H&R Block, www.hrblock.com

Another excellent Internet site for taxpayers is the one maintained by the computer tax

software company, H&R Block. The Tax Tips section of the site contains information

on law changes, tax planning, tax terms, and more.

Will Yancey’s home page, www.willyancey.com

This site is one of the best indexes available with links to other tax, accounting, and legal

Internet sites. The site has hundreds of links to commercial Web sites, federal government

Web sites, state and local Web sites, and international Web sites.

Many states are using Web sites to post names of delinquent taxpayers. Sup-

porters of ‘‘Internet Shaming’’ say it is an inexpensive way to encourage delin-

quent taxpayers to pay their taxes. Apparently, the threat of exposure is a good

motivator. Some critics, however, wonder how innocent taxpayers will be com-

pensated when inevitable mistakes are made. O. J. Simpson was listed among

California’s worst tax debtors on the state‘s public shaming Web site until he

was convicted of leading an armed holdup and sent to prison. Pamela Anderson

was included on the tax delinquents list in 2010 (www.ftb.ca.gov/indiv iduals/

txdlnqnt.shtml).

Self-Study Problem 1.9

Indicate whether the following statements are true or false by circling the

appropriate letter.

TF1. The Internet is controlled by the Federal Communications Com-

mission, which is part of the administrative branch of the United

States government.

TF2. Taxpayers can download tax forms and IRS publications from

the IRS Internet site.

TF3. A help function is available to aid users of the IRS site.

TF4. The H&R Block Internet site is maintained by Practitioner’s Pub-

lishing Co. for users of its textbooks.

1-26 Chapter 1

The Individual Income Tax Return

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 1.10ELECTRONIC FILING (e-Filing)

In Transition: The electronic filing rules discussed below are in constant transition

as the IRS works to convert as many taxpayers as possible to electronic filing. Addi-

tional information is available at the IRS Web site (www.irs.gov).

Electronic filing (e-filing) is the process of transmitting federal income tax return infor-

mation to the IRS Service Center using a computer with Internet access. For the taxpayer,

electronic filing offers a faster refund, either through a direct deposit to the taxpayer’s bank

account or by check. IRS statistics show an error rate of less than 1.0 percent on electron-

ically filed returns, compared with more than 20 percent on paper returns.

Electronic filing of individual income tax returns may be done with the IRS by using

one of two methods.

The first electronic filing method is e-filing using a personal computer and tax prepa-

ration software. Individual taxpayers may transmit their returns from home, workplaces,

libraries, or retail outlets. The IRS Web site contains detailed information on this process

as the IRS is constantly working to make e-filing more user friendly and widely available.

The IRS recently issued new warnings to taxpayers about identity th eft scams

where information is obtained from taxpayers through fake e-mail notices.

The e-mails look official and request detailed personal information. However,

the IRS never sends unsolicited e-ma ils asking for personal information.

The second e-filing opt ion is use of the services of a tax professional, including certified

public accountants, tax attorneys, IRS-enrolled agents, and tax preparation businesses qual-

ifying for the IRS tax professional e-filing program.

Electronic filing represents the major significant growth area in computerized tax services.

More than two-thirds of all individual taxpayers now e-file. In the future, electronic filing

will likely become mandatory for the entire professional tax return preparation industry.

General Electric Co. filed a 24 ,000-page return electronically in the summer of

2006, the first year certain large corporations were required to file electroni-

cally. The size of the e-filed return was 237 megabytes. If GE had sent paper

forms, the return would have been 8 feet tall.

Self-Study Problem 1.10

Indicate whether the following statements are true or false by circling the

appropriate letter.

TF1. Compared to paper returns, electronic filings significantly reduce

the error rate for tax returns filed.

TF2. Individuals may not use electronic filing for their own personal tax

returns, but must engage a tax professional if they wish to e-file.

TF3. Taxpayers who e-file generally receive faster refunds.

TF4. Taxpayers who e-file can only request their refund in the form of a

check.

Section 1.10

Electronic Filing (e-Filing) 1-27

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

KEY POINTS

Learning Objectives Key Points

LO 1.1:

Understand the history and

objectives of U.S. tax law.

The income tax was authorized by the Sixteenth Amendment to the Constitution on

March 1, 1913.

In addition to raising money to run the government’s programs, the income tax is used as

a tool of economic and social policies.

Examples of economic tax provisions are the limited allowance for expensing capital expen-

ditures and the accelerated cost recovery system (ACRS or MACRS) of depreciation. The

charitable contribution deduction is an example of a social tax provision.

LO 1.2:

Describe the different entities

subject to tax and reporting

requirements.

Individual taxpayers file Form 1040EZ, Form 1040A, or Form 1040.

Corporations must report income annually on Form 1120 and pay taxes.

An S corporation generally does not pay regular corporate income taxes; instead, the

corporation’s income passes through to its shareholders and is included on their individ-

ual tax returns.

A partnership files Form 1065 to report the amount of income or loss and show the

allocation of the income or loss to the partners.

Generally, all income or loss of a partnership is included on the tax returns of the partners.

LO 1.3:

Understand and apply the tax

formula for individuals.

AGI (adjusted gross income) is gross income less deductions for adjusted gross income.

AGI less the larger of itemized deductions or the standard deduction and less exemption

amounts equals taxable income.

Appropriate tax tables or rate schedules are applied to taxable income to calculate the

gross tax liability.

The gross tax liability less credits and prepayments equals the tax due or refund due.

LO 1.4:

Identify individuals who must file

tax returns and select their correct

filing status.

Conditions relating to the amount of the taxpayer’s income and filing status must exist

before a taxpayer is required to file a U.S. income tax return.

Taxpayers are also required to file a return if they have net earnings from self-employment

of $400 or more, receive advanced earned income credit payments (AEIC), or owe taxes

such as Social Security taxes on unreported tips.

There are five filing statuses: single; married, filing jointly; married, filing separately; head

of household; and qualifying widow(er).

LO 1.5:

Calculate the number of exemp-

tions and the exemption amounts

for taxpayers.

Taxpayers are allowed two types of exemptions: personal and dependency.

For 2010, each exemption reduces adjusted gross income by $3,650. Prior to 2010, high-

income taxpayers were subject to phase-outs of both exemptions and itemized deductions.

The phase-outs may be reinstated in 2011.

Personal exemptions are granted to taxpayers for themselves and their spouse.

Extra exemptions may be claimed for each person other than the taxpayer or spouse who

qualifies as a dependent. A dependent is an individual who is either a qualifying child or a

qualifying relative.

LO 1.6:

Calculate the correct standard or

itemized deduction amounts for

taxpayers.

The standard deduction was placed in the tax law to provide relief for taxpayers with few

itemized deductions.

For 2010, the standard deduction amounts are: Single $5,700; Married, filing jointly

$11,400; Married, filing separately $5,700; Head of household $8,400; Qualifying

widow(er) $11,400.

Taxpayers who are 65 years of age or older or blind are entitled to additional standard

deduction amounts of $1,400 for unmarried taxpayers and $1,100 for married taxpayers

and surviving spouses in 2010.

1-28 Chapter 1

The Individual Income Tax Return

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.