Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

by the community property laws, may be relieved of any liability related to this income. To

be granted relie f, the taxpayer mu st not know of or have r eason to know of the omitted

community property income.

Self-Study Problem 6.10

Tom and Rachel are married and living together in California. Their income is

as follows:

Tom’s salary $40,000

Rachel’s salary 30,000

Dividends (Tom’s property) 5,000

Dividends (Rachel’s property) 3,000

Interest (community property)

4,000

Total

$82,000

a. If Rachel files a separate tax return, she should report income of:

$ ____________

b.If Tom and Rachel lived in Texas, what should Rachel report as income?

$ ____________

KEY POINTS

Learning Objectives Key Points

LO 6.1:

Calculate the child tax credit.

Credits are a direct reduction in tax liability instead of a deduction from income.

For 2010, the child tax credit is $1,000 per qualifying child.

Child tax credit begins phasing out when AGI reaches $110,000 for joint filers ($55,000 for

married taxpayers filing separately) and $75,000 for single or head of household taxpayers.

LO 6.2:

Determine the earned income

credit (EIC).

The earned income credit (EIC) is available to qualifying individuals with earned income and

AGI below certain levels and is meant to assist the working poor.

The EIC formula for calculating the credit is based on the adjusted gross income of the tax-

payer and the number of qualifying children of the taxpayer.

To compute the credit, the taxpayer must fill in a form calculating the credit from the tables

based on earned income from wages, salaries, and self-employment income.

To be eligible for the credit with no qualifying children, a worker must be over 25 and

under 65 years old and not be claimed as a dependent by another taxpayer.

LO 6.3:

Compute the child and dependent

care credit for an individual

taxpayer.

To be eligible for the child and dependent care credit, the dependent must either be under

the age of 13 or be a dependent or spouse of any age who is incapable of self-care.

If a child’s parents are divorced, the child need not be the dependent of the taxpayer claim-

ing the credit, but the child must live with that parent more than he or she lives with the

other parent.

Section 6.10

Community Property 6-31

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The expenses that qualify for the credit include amounts paid to enable both the taxpayer

and the spouse to be employed.

For taxpayers with adjusted gross income of less than $15,000, the child and dependent care

credit is equal to 35 percent of the qualified expenses. For taxpayers with AGI of $15,000 or

more, the credit gradually decreases from 35 percent to 20 percent for AGI over $43,000.

In determining the credit, the maximum amount of qualified expenses to which the applicable

percentage is applied is $3,000 for one dependent and $6,000 for two or more dependents.

Full-time students with little or no income are deemed to have earned income of $250 per

month for one dependent and $500 per month for two or more dependents for purposes of

calculating this limitation.

LO 6.4:

Apply the special rules applicable

to the American Opportunity and

lifetime learning credits.

For 2010, the partially refundable American Opportunity credit is 100 percent of the first

$2,000 of tuition, fees, books, and materials paid and 25 percent of the next $2,000, for a

total annual credit of $2,500 per student.

The American Opportunity credit is available for the first 4 years of post-secondary education.

Taxpayers can elect a nonrefundable lifetime learning tax credit of 20 percent of tuition and

fees up to $10,000 in 2010.

The American Opportunity credit is phased out for joint filers with income between

$160,000 and $180,000 and for single and head of household filers with income between

$80,000 and $90,000. The lifetime learning credit is phased out between $100,000 and

$120,000 for married taxpayers and between $50,000 and $60,000 for those single or head

of household taxpayers.

Taxpayers cannot take both the American Opportunity credit and the lifetime learning credit

for the same student in the same tax year.

The credits cannot be used for expenses that are deducted from taxable income on a tax

return.

LO 6.5:

Understand the operation of the

foreign tax credit, the adoption

credit, and the energy credits.

U.S. taxpayers are allowed to claim a foreign tax credit on income earned in a foreign

country and subject to income taxes in that country.

Taxpayers may make an annual election to claim a deduction instead of a credit for the for-

eign taxes, but most taxpayers receive a greater tax benefit by claiming the foreign tax credit.

Generally, the foreign tax credit is equal to the amount of the taxes paid to foreign govern-

ments; however, there is an ‘‘overall’’ limitation on the amount of the credit, which is calcu-

lated as the ratio of net foreign income to U.S. taxable income times the U.S. tax liability.

Unused foreign tax credits may be carried back 1 year and forward 10 years to reduce tax

liability in those years.

Individuals are allowed an income tax credit for qualified adoption expenses. The total

expense that can be taken as a credit for all tax years with respect to an adoption of a

child is $13,170 (for 2010).

A tax credit for the purchase of new personal- or business-use hybrid gas-electric vehicles is

available from 2006 through 2010.

For 2009 and 2010, taxpayers may claim credits of up to $1,500 for energy-efficient home

improvements and a 30 percent credit for solar, wind, or geothermal property.

LO 6.6:

Understand the basic alternative

minimum tax calculation.

The AMT was designed in the 1960s to ensure that wealthy taxpayers could not take advan-

tage of special tax write-offs (tax preferences and other adjustments) to avoid paying tax.

Adjustments are timing differences that arise because of differences in the regular and AMT

tax calculations (e.g., depreciation timing differences), while preferences are special provi-

sions for the regular tax that are not allowed for the AMT (e.g., state income taxes).

For 2010, the alternative minimum tax rates for calculating the tentative AMT are 26 per-

cent of the first $175,000 ($87,500 for married taxpayers filing separately), plus 28 percent

on amounts above $175,000 applied to the taxpayer’s alternative minimum tax base.

6-32 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Reinforce the tax information covered in this chapter by completing the online

interactive tutorials located at the Income Tax Fundamentals Web site:

www.cengagebrain.com.

LO 6.7:

Apply the rules for computing tax

on the unearned income of minor

children and certain students.

The tax law contains provisions that limit the benefit of shifting income to certain minor

children.

The net unearned income of minor children is taxed at their parents’ rates.

This parental tax rate applies to dependent children who are 18 or younger or are students

ages 19 through 23 at the end of the year, have at least one living parent, and have ‘‘net

unearned income’’ for the year.

If certain conditions are met, parents may elect to include a child’s gross income on the

parents’ tax return. The election eliminates the child’s return filing requirements and saves

the parents the trouble of filing the special calculation Form 8615 for the ‘‘kiddie tax.’’

LO 6.8:

Distinguish between the different

rules for married taxpayers residing

in community property states when

filing separate returns.

Income derived from community property held by a married couple, either jointly or sepa-

rately, as well as wages and other income earned by a husband and wife, must be allo-

cated between the spouses if filing separately.

Nine states use a community property system of marital law. These states are Arizona,

Louisiana, Texas, California, Nevada, Washington, Idaho, New Mexico, and Wisconsin.

In general, in a community property state, income is split one-half (50 percent) to each spouse.

There are exceptions for certain separate property (e.g., property owned prior to marriage, etc.).

QUESTIONS and PROBLEMS

GROUP 1:

MULTIPLE CHOICE QUESTIONS

.............................................. .............................................. .

LO 6.1

1. Russ and Linda are married and file a joint tax return claiming their three children,

ages 4, 7, and 18, as dependents. Their adjusted gross income for 2010 is $105,300.

What is Russ and Linda’s total child credit for 2010?

a. $600

b. $1,200

c. $1,000

d. $2,000

e. Some other amount

LO 6.1

2. Jennifer is divorced and files a head of household tax return claiming her children, ages

4, 7, and 17, as dependents. Her adjusted gross income for 2010 is $81,300. What is

Jennifer’s total child credit for 2010?

a. $850

b. $1,200

c. $1,650

Questions and Problems 6-33

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

d. $2,000

e. Some other amount

LO 6.2

3. Assuming they all meet the income requirements, which of the following taxpayers

qualify for the earned income credit in 2010?

a. A married taxpayer who files a separate tax return and has a dependent child

b. A single taxpayer who waited on tables for 3 months of the tax year and is claimed as

a dependent by her mother

c. A single taxpayer who is self-employed and has a dependent child

d. a and c above

e. None of the above qualify for the earned income credit

LO 6.3

4. Which of the following payments does not qualify as a child care expense for purposes

of the child and dependent care credit?

a. Payments to a day care center

b. Payments to the taxpayer’s sister (21 years old) for daytime babysitting

c. Payments to a housekeeper who also babysits the child

d. Payments to the taxpayer’s dependent brother (16 years old) for daytime babysitting

e. All of the above qualify for the child and dependent care credit

LO 6.4

5. The American Opportunity credit is 100 percent of the first ______ of tuition and fees

paid and 25 percent of the next ______.

a. $600; $1,200

b. $1,100; $550

c. $2,000; $2,000

d. $1,100; $5,500

e. None of the above

LO 6.4

6. Jane graduates from high school in June 2010. In the fall, she enrolls for six units at Big

State University. Big State University considers students who take twelve or more

units full-time. Jane’s father pays her tuition and fees of $2,500 for the fall semest er

and in December prepays $2,500 for the spring semester. In 2010, the American

Opportunity credit for Jane’s tuition and fees before any AGI limitation is:

a. $5,000

b. $2,500

c. $2,200

d. $1,800

e. Some other amount

LO 6.4

7. In September 2010, Sam pays $2,200 to take a course to improve his job skills to qual-

ify for a new position at work. His lifetime learning credit for 2010 is:

a. $220

b. $240

c. $360

d. $1,100

e. Some other amount

LO 6.4

8. In November 2010, Simon pays $6,200 to take a course to improve his job skills to

qualify for a new position at work. Simon’s employer reimbursed him for the cost of

the course. For 2010, Simon’s lifetime learning credit is:

a. $0

b. $1,000

6-34 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

c. $2,500

d. $1,500

e. Some other amount

LO 6.4

9. John, a single father, has AGI of $51,000 in 2010. In 2010, he pays $4,000 in qualified

tuition for his dependent son, who just started attending Small University (SU). What

is John’s American Opportunity credit for 2010?

a. $1,650

b. $1,485

c. $2,500

d. $660

e. Some other amount

LO 6.4

10. Joan, a single mother, has AGI of $85,000 in 2010. In September 2010, she pays $5,000

in qualified tuition for her dependent son who just started at Big University (BU).

What is Joan’s American Opportunity credit for 2010?

a. $1,650

b. $1,485

c. $990

d. $1,250

e. Some other amount

LO 6.4

11. Becky, a college freshman, works part-time and pays $1,600 of her college tuition

expenses. Although Becky files her own tax return, her parents claim her as a dependent

on their tax return. Becky’s parents have AGI of $50,000. What is the amount of American

Opportunity credit her parents can claim on their tax return for the tuition Becky paid?

a. $0

b. $495

c. $1,600

d. $1,650

e. Some other amount

LO 6.5

12. Taxpayer L has income of $55,000 from Norway, which imposes a 30 percent income

tax, and income of $45,000 from France, which imposes a 40 percent income tax. L has

taxable income from U.S. sources of $200,000 and U.S. tax liability before credits of

$90,000. What is the amount of the foreign tax credit?

a. $16,500

b. $34,500

c. $30,000

d. $100,000

e. $45,000

LO 6.5

13. John and Joan pay $16,500 of qualified adoption expenses in 2010 to finalize the adop-

tion of a qualified child who is not a sp ecial ne eds child. Their AGI is $190,000 for

2010. What is their adoption credit for 2010?

a. $16,500

b. $13,170

c. $10,707

d. $2,463

LO 6.5

14. In connection with the adoption of an eligible child who is a U.S. citizen and who is

not a child with special needs, Sean pays $4,000 of qualified adoption expenses in 2009

and $3,000 of qualified adoption expenses in 2010. The adoption is finalized in 2010.

Questions and Problems 6-35

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

There is no phase-out of the adoption credit. What are the adoption credits for both

2009 and 2010, respectively?

a. $0; $7,000

b. $4,000; $1,000

c. $4,000; $3,000

d. $7,000; $0

LO 6.5

15. In 2010, Irene, an unmarried individual, pays $6,500 in qualified adoption expenses to

an adoption agency for the final adoptio n of an eligible child who is not a child with

special needs. In the same year, the individual’s employer, under a qualified adoption

assistance program, pays an additional $4,000 for other qualified adoption expenses to

an attorney on behalf of Irene for the adoption of the child. Assuming Irene is not sub-

ject to the phase-out, she may exclude, from her personal income, how m uch of the

$4,000 payment made by her employer?

a. $6,500

b. $5,000

c. $4,000

d. $2,000

LO 6.5

16. If a taxpayer does not have enough tax liability to use all the available adoption credit,

the unused portion may be carried forward for how many years?

a. Two

b. Three

c. Five

d. Seven

LO 6.6

17. Which of the following is not a tax preference or adjustment item for the individual

alternative minimum tax computation?

a. Miscellaneous itemized deductions

b. State income taxes

c. State income tax refunds

d. Private activity bond interest

e. All of the above are adjustments or tax preference items

LO 6.8

18. Dana and Larry are married and live in Texas. Dana earns a salary of $45,000 and

Larry has $25,000 of rental income from his separate property. If Dana and Larry

file separate tax returns, what amount of income must Larry report?

a. $0

b. $22,500

c. $25,000

d. $47,500

e. None of the above

LO 6.8

19. Which of the following conditions need not be satisfied in order for a married tax-

payer, residing in a community property state, to be taxed only on his or her separate

salary?

a. The husband and wife must live apart for the entire year.

b. A minor child must be living with the spouse.

c. The husband and wife must not file a joint income tax return.

d. The hu sband and wife must not transfer earned income between themselves.

e. All of the above must be satisfied.

6-36 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

GROUP 2:

PROBLEMS

.............................................. .............................................. .

LO 6.1 1. Calculate the child credit for the following taxpayers. Please show your work.

a. Jeremy is a single (head-of-household) father with a dependent 8-year-old son and

$79,600 of AGI:

_______________________________________________________________________

b. Jerry and Ann have two dependent preschool children and $100,000 of AGI:

_______________________________________________________________________

c. James and Apple have two dependent children and $120,400 of AGI:

_______________________________________________________________________

LO 6.2 2. How does the earned income credit produce a ‘‘negative’’ income tax?

_________________________________________________ ________________________

_________________________________________________ ________________________

_________________________________________________ ________________________

LO 6.2 3. Diane is a single taxpayer who qualifies for the earned income credit. Diane has two

qualifying children who are 3 and 5 years old. During 2010, Diane’s wages are

$16,100 and she receives dividend income of $500. Calculate Diane’s earned income

credit using the EIC table in Appendix B.

$ ____________

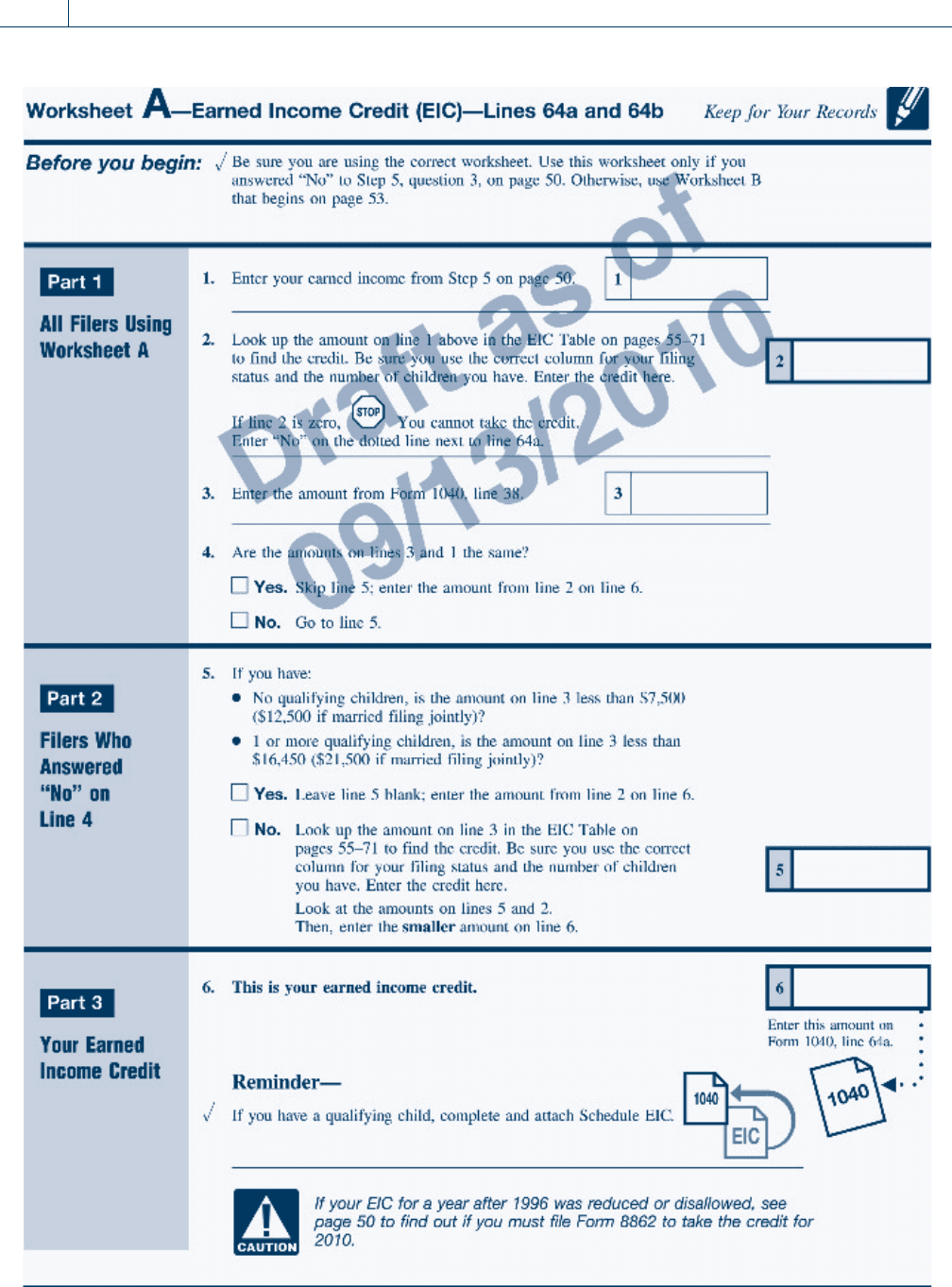

LO 6.2 4. Margaret and David Simmons are married and file a joint income tax return. They

have two dependent children, Margo, 4 years old (Social Security number 316-31-

4890), and Daniel, who was born during the year (Social Security number 316-31-

7894). Margaret’s wages are $4,000, and David has wages of $14,000. In addition,

they receive interest income of $200 during the year. Margaret and David do not

have any other items of income and do not have any deductions for adjusted gross

income. Assuming the Simmons file Form 1040A for 2010, complete Schedule EIC,

the Earned Income Credit Worksheet, from the 1040A Instructions on pages 6-39

and 6-40. (The Earned Income Credit table is in Appendix B.)

LO 6.2 5. What is the maximum investment income a taxpayer is allowed to have and still be

allowed to claim the earned income credit? Please speculate as to why there is an

investment income limit in the tax law.

_________________________________________________ ________________________

_________________________________________________ ________________________

_________________________________________________ ________________________

LO 6.3 6. Calculate the amount of the child and dependent care credit allowed for 2010 in each

of the following cases, assuming the taxpayers had no income other than the stated

amounts.

a. William and Carla file a joint tax retu rn. Carla earned $26,000 during the year,

while William attended law school full- time for 9 months and earned no income.

They paid $3,500 for the care of their 3-year-old child, Carl.

$ ____________

b. Raymond and Michele file a joint tax return. Raymond earned $32,500 during the

year, while Michele earned $9,000 for the year from a part-time job. They paid

$7,000 for the care of their two children under age 13.

$ ____________

Questions and Problems 6-37

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

c. Beth is a single taxpayer who has two dependent children under age 5. Beth earned

$23,500 in wages during the year and paid $6,700 for the care of her children.

$ ____________

LO 6.3 7. Clarita is a single taxpayer with two dependent children, ages 10 and 12. Clarita pays

$3,000 in qua lified child care expense s during the year. If her adjusted gross income

(all from wages) for the year is $18,500, calculate Clarita’s ch ild and dependent care

credit for 2010.

$ ____________

LO 6.3 8. Go to the IRS Web site (www.irs.gov) and redo Problem 7 (Chapter 6, Group 2) using

the most recent interactive ‘‘Fill-in Forms’’ Form 2441, Child and Dependent Care

Expenses. Print out the completed Form 2441. Also note the ‘‘document rights’’ feature

available for saving filled-in forms to the computer.

LO 6.3 9. Mary and John are married and have AGI of $100,000 and two young children. John

doesn’t work, and they pay $6,000 a year to day care providers so he can shop, clean,

and read a little bit in peace. How much child and dependent care credit can Mary and

John claim? Why?

LO 6.3 10. Martha has a 3-year-o ld child and pays $10,000 a year in day care costs. Her salary is

$45,000. How much is her child and dependent care credit?

LO 6.3 11. Marty and Jean ar e married and have 4-year-old twins. Jean is going to school full-time

for 9 months of the year, and Marty earns $45,000. The twins are in day care so Jean

can go to school while Marty is at work. The cost of day care is $10,000. What is their

child and dependent care credit? Please explain your calculation.

_________________________________________________ ________________________

_________________________________________________ ________________________

_________________________________________________ ________________________

LO 6.4 12. What is the reason there are education tax credits in the tax law:

_________________________________________________ ________________________

_________________________________________________ ________________________

_________________________________________________ ________________________

LO 6.4 13. Please explain the difference between the types of education covered by the American

Opportunity credit and the lifetime learning credit.

_________________________________________________ ________________________

_________________________________________________ ________________________

_________________________________________________ ________________________

LO 6.4 14. Janie graduates from high school in 2010 and enrolls in college in the fall. Her parents

pay $4,000 for her tuition and fees.

a. Assuming Janie’s parents have AGI of $170,000, what is the American Opportunity

credit they can claim for Janie?

_________________________________________________ ______________________

_________________________________________________ ______________________

_________________________________________________ ______________________

b. Assuming Janie’s parents have AGI of $75,000, what is the American Opportunity

credit they can claim for Janie?____________________________________________

6-38 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Questions and Problems 6-39

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

(Wages, Salaries)

(Adjusted Gross Income)

6-40 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.