Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Chapter 6

Credits and Special Taxes

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 6.1 Calculate the child tax credit.

LO 6.2 Determine the earned income credit (EIC).

LO 6.3 Compute the child and dependent care credit for an

individual taxpayer.

LO 6.4 Apply the special rules applicable to the American

Opportunity and lifetime learning credits.

LO 6.5 Understand the operation of the foreign tax credit, the

adoption credit, and the energy credits.

LO 6.6 Understand the basic alternative minimum tax calculation.

LO 6.7 Apply the rules for computing tax on the unearned income

of minor children and certain students.

LO 6.8 Distinguish between the different rules for married tax-

payers residing in community property states when filing

separate returns.

Overview

This chapter covers the most commonly seen tax credits and several special methods of cal-

culating tax. A credit is a direct reduction in tax liability instead of a deduction from

income. Credits are used because they target tax relief to certain groups of taxpayers.

Because of the progressive rate structure of the income tax, a deductio n provides greater

benefit to higher-income taxpayers, while a tax credit provides equal benefit, regardless

of the taxpayer’s income level. Many credits exist in the tax law that are not covered

here, such as the credit for research and development, the Welfare-to-Work credit, and

the credit for the elderly and disabled.

The second part of this chapter covers the alternative minimum tax (AMT), the tax on

unearned income of minor children (the ‘‘kiddie tax’’), and an overview of community

property law as it applies to the ind ividua l income t ax. Each of these provisions can add

substantial complexity to the individual income tax calculation. For example, if a taxpayer

is subject to the ‘‘kiddie tax,’’ he or she must calculate tax liability in an alternative manner,

using the marginal tax rates of his or her parents.

6-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

A credit of up to $8,000 applies to qualified first-time home buyers purchasing

a principal residence with a cost of $800,000 or less after November 6, 2009,

and before May 1, 2010. A similar credit is also available to taxpayers who

are ‘‘long term residents’’ who have owned and used a residence as a principal

residence for any 5-year period during the 8-year period ending on the date of

purchase of a subsequent principal residence. This credit is limited to $6,500.

The credits are phased out for taxpayers with AGI of $225,000 to $245,000 if

married and $125,000 to $145,000 if single, and may be cl aimed on the return

for the year prior to the purchase. These temporary credits are meant to target

assistance to the home construction industry and low to middle income home-

buyers. The credit is not required to be paid back by a taxpayer unless the res-

idence is sold or ceases to be a principal residence within a 3-year period.

EXAMPLE Eugene and Devona qualify for the maxim um $8,000 First Time

Homebuyer Credit and make their first-time home purchase on

January 17, 2010. They may claim the credit on either their 2009 or

their 2010 tax return. If they own and use the property as their pri-

mary residence until January 17, 2013, they will not have to repay

or recapture any of the credit. N

SECTION 6.1

CHILD TAX CREDIT

Individual taxpayers are permitted to take a tax credit based on the number of their

dependent children. The children must be under age 17, U.S. citizens, claimed as depend-

ents on the taxpayer’s return, and meet the definition of ‘‘qualifying child’’ discussed in

Chapter 1.

Maximum Credit and Phase-Outs

For 2010, the child tax cr edit is $1,000 per qualifying child. The available credit begins

phasing out when AGI reaches $110,000 for joint filers ($55,000 for married taxpayers fil-

ing separately) and $75,000 for single or head of household taxpayers. The credit is phased

out by $50 for each $1,000 (or part thereof ) of AGI above the threshold amounts. Since the

maximum credit available depends on the number of qualifying children, the inc ome level

at which the credit is fully phased out also depends on the number of children qualifying

for the credit.

EXAMPLE Hilary and Patrick are married and file a joint tax return claiming

their two children, ages 5 and 7, as dependents. Their AGI for

2010 is $118,700. Hilary and Patrick’s available child tax credit for

2010 is $1,550, computed as their maximum credit of $2,000

($1,000 2 children) reduced by a $450 phase-out. Since Hilary

and Patrick’s AGI is in excess of the $110,000 threshold, the maxi-

mum credit must be reduced by $50 for every $1,000 (or part

thereof) above the threshold amount {$50 [($118,700 $110,000)/

$1,000]}. Thus, the credit reduction equals $450 [$50 9 (rounded

from 8.7)]. N

6-2 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 6.2

EARNED INCOME CREDIT

The earned income credit (EIC) is available to qualifying individuals with earned income

and AGI below certain levels. The earned income credit is meant to assist the working

poor. Taxpayers with ‘‘disqualified income’’ (certain types of investment income) exceed-

ing $3,100 in 2010 are not allowed to claim the earned income credit. The earned income

credit is one of the few credits that is refundable. The taxpayer is eligible to claim the credit

and receive a refund equal to the amount of the credit, even if no tax is owed to the federal

government. The credit in effect can produce a ‘‘negative’’ income tax.

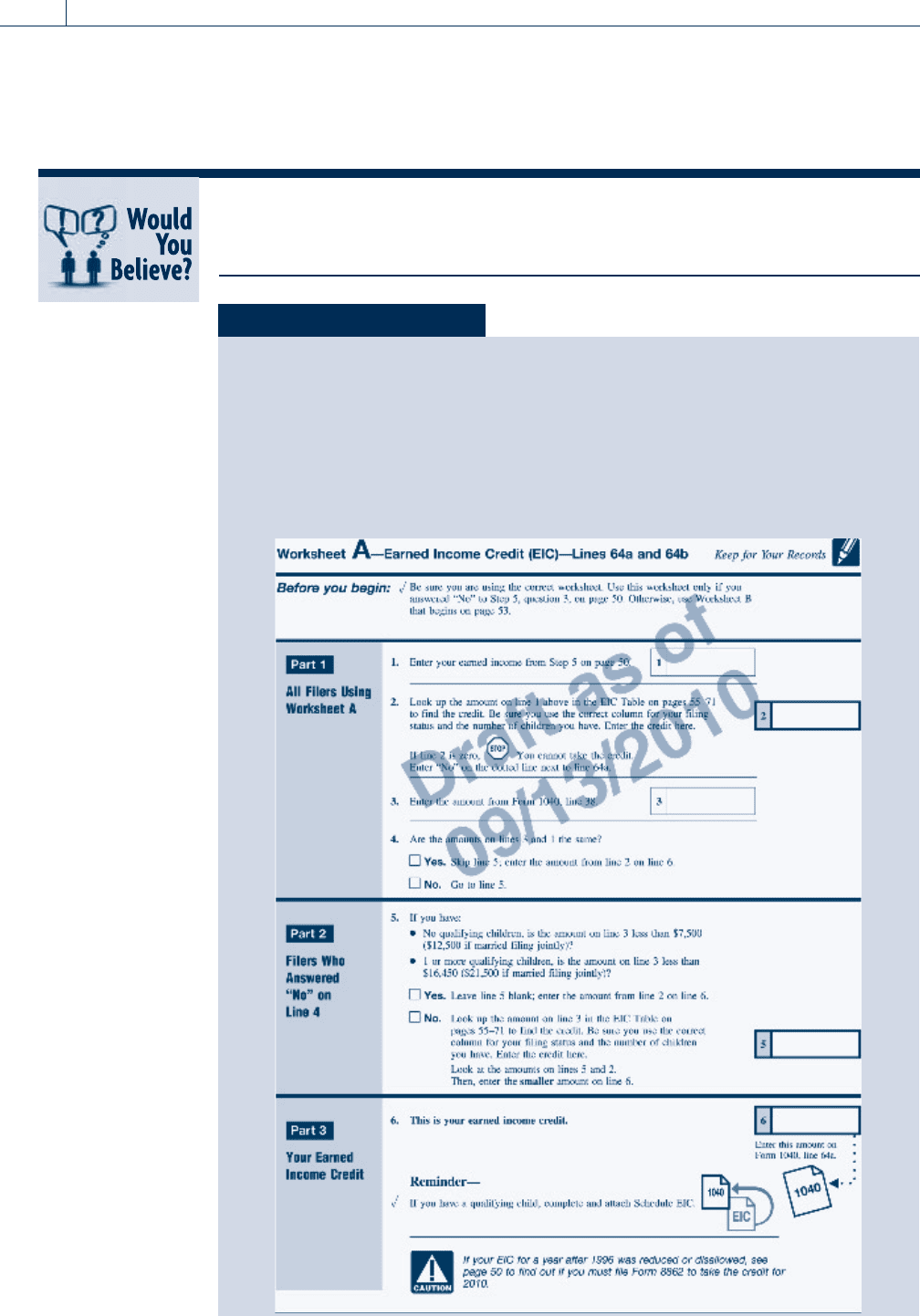

The formula for ca lculating the credit depends on the adjusted gross income of the tax-

payer and the number of qualifying children of the taxpayer. The IRS issues an earned

income credit table to assist taxpayers in computing the credit (see Appendix B). To com-

pute the credit, the taxpayer must fill out a form calcul ating the credit from the tables based

on earned income from wages, salaries, and self-employment income. If the taxpayer’s

adjusted gross income is different from earned income and exceeds certain threshhold

amounts shown below, the credit must also be calculated from the tables based on adjusted

gross income, and the smaller of the two credits calculated will be the credit allowed. This

calculation is illustrate d in Worksheet A on the following page.

Earned Income Credit Phaseout Ranges

Number of Qualifying Children

Item One Two Three or More None

Earned Income Amount $ 8,970 $12,590 $12,590 $ 5,980

Maximum Amount of Credit $ 3,050 $ 5,036 $ 5,666 $ 457

Threshold Phaseout Amount

(Single, Surviving Spouse,

or Head of Household)

$16,450 $16,450 $16,450 $ 7,480

Completed Phaseout Amount

(Single, Surviving Spouse,

or Head of Household)

$35,535 $40,363 $43,352 $13,460

Threshold Phaseout Amount

(Married Filing Jointly)

$21,460 $21,460 $21,460 $12,490

Completed Phaseout Amount

(Married Filing Jointly)

$40,545 $45,373 $48,362 $18,470

Appendix B provides tables showing the amount of the earned income credit for each

type of taxpayer.

To be eligible for the credit with no qualifying children, a worker must be over 25 and

under 65 years old and not be claimed as a dependent by another taxpayer. There is no age

requirement for taxpayers with qualifying children. Also, married taxpayers must file a joint

return in order to receive any earned income credit.

Self-Study Problem 6.1

a. Jose and Jane are married and file a joint tax return claiming their three

children, ages 4, 5, and 18, as dependents. Their AGI for 2010 is $105,600.

What is Jose and Jane’s child credit for 2010?

$ ____________

b.Herb and Carol are married and file a joint tax return claiming their three

children, ages 4, 5, and 18, as dependents. Their AGI for 2010 is $125,400.

What is Herb and Carol’s child credit for 2010?

$ ____________

Section 6.2

Earned Income Credit 6-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

As of 2010, a qualifying child must generally meet the tests to be a qualifying child as

discussed in Chapter 1, with some special variations primarily related to support and

divorced taxpayers. Please see the IRS Web site for additional information if necessary.

Studies have shown that as many as one out of three earned income credits are

calculated incorrectly or fraudulently. Treasury inspectors estimate that billions

of dollars worth of erroneous claims slip through the cracks every year.

Self-Study Problem 6.2

Dennis and Lynne have a 5-year-old child. Dennis has a salary of $16,200.

Lynne is self-employed with a loss of $400 from her business. Dennis and

Lynne receive $100 of taxable interest income during the year. Their earned

income for the year is $15,800 and their adjusted gross income is $15,900

($16,200 $400 þ $100).

Use Worksheet A and calculate their earned income credit from the EIC

table in Appendix B.

$ ____________

(Wages, Salaries)

(Adjusted Gross Income)

6-4 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 6.3

CHILD AND DEPENDENT CARE CREDIT

Congress enacted tax laws to provide benefits to taxpayers with dependents who must be

provided with care and supervision while the taxpayers work. Taxpayers are allowed a

credit for expenses for the care of their children and certain other dependents. To be eli-

gible for the child and dependent care credit, the dependent must either be under the age

of 13 or be a dependent or spouse of any age who is incapable of self-care. If a child’s

parents are divorced, the child need not be the dependent of the taxpayer claiming the

credit, but the child must live with that parent more than he or she lives with the other

parent. For example, a divorced mother with custody of a child may be entitled to the

credit even though the child is a dependent of the father.

Qualified Expenses

The expenses that qualify for the credit include amounts paid to enable both the taxpayer

and his or h er spouse to be employed. Qualified expenses include amounts paid for in-

home care, such as a housekeeper, as well as out-of-home care, such as a day care center.

Overnight camps do not qualify for the credit, nor do activities providing standard educa-

tion. Day camps such as soccer camps and dinosaur camps do qualify for the credit since

they are considered more ‘‘fun and games,’’ than education. Payments to relatives are eli-

gible for the credit, unless the payments are to a dependent of the taxpayer or to the tax-

payer’s child who is under the age of 19 at the end of the tax year. To claim the credit, the

taxpayer must include on his or her return the name, address, and taxpayer identification

number of the person or organization providing the care.

Allowable Credit

For taxpayers with adjusted gross income of less than $15,000, the child and dependent

care credit is equal to 35 percent of the qualified expenses. For taxpayers with income of

$15,000 or more, see Table 6.1 below for the applicable credit percentage. In determining

the credit, the maximum amount of qualified expenses to which the applicable percentage

is applied is $3,000 for one dependent and $6,000 for two or more dependents.

TABLE 6.1 CHILD AND DEPENDENT CARE CREDIT

PERCENTAGES

Adjusted Gross Income Applicable Percentage

Over But not over

$0 15,000 35%

15,000 17,000 34%

17,000 19,000 33%

19,000 21,000 32%

21,000 23,000 31%

23,000 25,000 30%

25,000 27,000 29%

27,000 29,000 28%

29,000 31,000 27%

31,000 33,000 26%

33,000 35,000 25%

35,000 37,000 24%

37,000 39,000 23%

39,000 41,000 22%

41,000 43,000 21%

43,000 No limit 20%

Section 6.3

Child and Dependent Care Credit 6-5

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Married taxpayers must file a joint return to claim the child and dependent care credit, and

the qualifying dependent care expenses are limited to the lesser of either spouse’s earned

income. For example, if a wife makes $22,000 and her husband earns $1,500, and they

spend $1,900 on child care, the maximum qualifying expenses are $1,500. A special rule applies

when a taxpayer is a full-time student. Full-time students with little or no income are deemed

to have earned income of $250 per month for one dependent and $500 per month for two or

more dependents for purposes of calculating this limitation. For example, if a taxpayer’s spouse

is a full-time student for 9 months of the year and has no income, the maximum amount of the

qualifying expenses for the care of one dependent is $2,250 ($250 per month 9months).

EXAMPLE Harry and Molly Grant are married and file a joint return. They have one

child and pay $4,000 for child care expenses during the year. Harry earns

$16,000 and Molly earns $8,500 during the year, resulting in adjusted gross

income of $24,500. The Grant’s child care credit is calculated as follows:

Qualified expenses

$4,000

Maximum for one dependent 3,000

Credit percentage from Table 6.1

30%

Credit allowed

$ 900

N

EXAMPLE Assume the same facts as in the example above, except the qualified

expenses are $2,100 (instead of $4,000). The credit is 30 percent of

$2,100, or $630. N

SECTION 6.4

EDUCATION TAX CREDITS

The HOPE credit, expanded and renamed the American Opportunity tax credit for 2009

and 2010, and the lifetime learning credit are the education credits available to help qual-

ifying low and middle income individuals defray the cost of higher education.

American Opportunity Credit

The American Opportunity credit is calculated as 100 percent of the first $2,000 of tuition,

fees, books, and course materials, and 25 percent of the next $2,000 for a maximum annual

credit of $2,500 per student. This credit is available for the first 4 years of post-secondary

education. The American Opportunity credit may be claimed for the expenses of students

pursuing bachelor’s or associate’s degrees, or vocational training. Room and board, trans-

portation costs, and personal living expenses are not qualifying expenses.

Tuition, fees, books, and course material expenses that qualify for the American Oppor-

tunity credit can be paid on behalf of the taxpayer, his or her spouse, or dependents.

Self-Study Problem 6.3

Julie Brown has been widowed for 5 years and has one dependent child. Her

adjusted gross income and her earned income are $90,000. Assume her taxable

income is $45,500, her regular tax is $6,228 (line 10 on Form 2441), and her

alternative minimum tax is $3,000 (line 11 on Form 2441). Julie has child care

expenses of $1,500 and expenses for the care of her disabled dependent

mother of $2,400. Calculate Julie’s child and dependent care credit for 2010

using page 1 of Form 2441 on page 6-7.

6-6 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 6.4

Education Tax Credits 6-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

6-8 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The student must carry at least one-half the normal course load for one term during the tax

year to qualify for the credit. In addition, the American Opportunity credit is not available

for any student convicted of a federal or state drug felony.

For 2010, the American Opportunity credit is phased out ratably for joint returns with

income between $160,000 and $180,000 and for singles (or head-of-household filers) with

income between $80,000 and $90,000. The American Opportunity credit is 40 percent

refundable, so up to $1,000 (40 percent of $2,500) may be refunded to the taxpayer if

the credit exceeds the taxpayer’s tax liability.

EXAMPLE Jenny graduates from high school in June 2010. In the fall, she enrolls

for twelve units at Big State University. Big State University considers

students who take twelve or more units full-time students. Jenny’s

father pays her tuition and fees of $2,300. In 2010, the American Oppor-

tunity credit for Jenny is $2,075 ((100% $2,000) þ (25% $300)). N

Qualifying expenses must be paid during the tax year for education during an academic

year beginning during that tax year. If tuition expenses are paid during the tax year for an

academic period beginning during the first 3 months of the following tax year, the expenses

may be claimed during the payment year.

Lifetime Learning Credit

Taxpayers can elect a nonrefundable tax credit of 20 percent of tuition and fees up to

$10,000 in 2010. Books are qualified expenses under the American Opportunity credit,

but not for the lifetime learning credit. The lifetime learning credit is available for expenses

paid for education of the taxpayer, his or her spouse, or dependents. The credit is available

for undergraduate, graduate, or professional courses at eligible educational institutions.

The student can be enrolled in just one cour se and still get the cr edit. The credit is not

subject to felony drug offense restrictions. The purpose of this credit is to encourage tax-

payers to take courses at eligible institutions to acquire or improve job skills.

EXAMPLE In September 2010, Scott pays $1,200 to take a course to improve his

job skills to qualify for a new position at work. His lifetime learning

credit for 2010 is $240 (20% $1,200). N

The lifetime learning credit is phased out at different levels than the American Oppor-

tunity credit. Married taxpayers with income between $100,000 and $120,000, and single

(or head -of-household) taxpayers with income between $50,000 and $60,000 must phase

the credit out evenly over the phase-out range for 2010.

EXAMPLE Jason, a single father, has AGI of $85,000 in 2010. In 2010, he pays $5,000

in qualified tuition for his son, who just started at Party-On University

(POU). Without any limitations, Jason would be entitled to a maximum

American Opportunity credit of $2,500. However, after applying the AGI

limitations, Jason’s American Opportunity credit is reduced by $1,250

($2,500 ($90,000 $85,000)/$10,000), resulting in a credit of $1,250.

Alternatively, assume Jason qualifies for a lifetime learning credit

of $500 (20% $2,500). During 2010, Jason pa id $2,500 of tuition for

a masters degree program in fine arts, which he has been attending

with the hope of eventually becoming a writer. The credit is fully

phased out under the lower phase-ou t ranges for the lifetime learn-

ing credit, so none of the credit may be claimed on his tax return. N

Section 6.4

Education Tax Credits 6-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Limitations

The use of the American Opportunity and lifetime learning credits is limited in the follow-

ing situations:

Married taxpayers who don’t file joint returns may not claim the credits.

Expenses paid for room and board do not qualify.

Expenses paid for nonacademic fees or for expenses that aren’t related to the stu-

dent’s course of instruction do not qualify. Also, expenses for courses that involve

sports, games, and hobbies don’t qualify for the credit unless the course is part of a

degree program.

Qualified educational expenses must be reduced by tax-free scholarships or employer

reimbursements received by students before calculating credits. However, expenses

paid from a gift or inheritance (which is tax free) do qualify for credits.

The credits cannot be used for expenses that are deducted from taxable income on a

tax return for education costs (e.g., unreimbursed job-related educational expenses) .

Students claimed as dependents of other taxpayers are not eligible for educational cred-

its. The persons who claim the students as dependents can claim the educational credit.

EXAMPLE Brenda, a college student, works part-time and pays part of her

college expenses; her parents pay the rest. Although Brenda files her

own tax return, her parents claim her as a dependent on their tax

return. Brenda cannot claim a credit for the qualified amounts she

paid, but her parents can claim a credit both for expenses they paid

and expenses paid by Brenda. N

EXAMPLE Gary, a college student, works part-time and pays part of his college

expenses. His parents pay for the rest. His parents have high income

and would not be able to claim an education credit for Gary. If Gary’s

parents decide not to claim Gary as a dependent, even though he

qualifies as a dependent, Gary can claim an education credit on his

own tax return for the expenses he paid and also for the expenses his

parents paid. Since Gary could have been claimed as a dependent by

his parents, he is not allowed to claim a dependency exemption on

his own tax return. N

Using Both Credits

Taxpayers cannot take both the American Opportunity credit and the lifetime learning credit

for the same student in the same tax year. An American Opportunity credit can be claimed

for one or more students, and the lifetime learning credit can be claimed for other students in

the same tax year. Also, the choice in one year doesn’t bind the taxpayer for future years. For

example, a taxpayer can claim the American Opportunity credit for a student in one tax year

and take the lifetime lear ning credit fo r the same student the followin g year. T axpayers

should claim the credit or combination of credits that gives the best tax benefit.

EXAMPLE In 2010, the Browns have a son, Boyd, who is a freshman in college,

and a daughter, Beth, who is a senior in college. They can take both

the American Opportunity credit for Boyd and the lifetime learning

credit for Beth for any qualifi ed educational expenses they pay in

2010. N

6-10 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.