Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

minimum tax such as state income and property taxes, miscellaneous itemized deductions,

including employee business expenses, and personal and dependency exemptions may cause

a taxpayer to owe alternative minimum tax.

When legislation was introduced (and failed) to repeal the federal individual

alternative minimum tax, Senator Baucus commented: ‘‘Now, the Darth Vader

of the tax code is bearing down on millions of unsuspecting families. Repealing

the AMT will protect millions of American families from this unfair and unex-

pected tax. It’s time to put the AMT in a galaxy far, far away and erase it from

the tax code.’’ (Press release, Office of U. S. Senator Chuck Grassley)

An opposing opinion about the alternative minimum tax is that it represents

a gradual implementation of a ‘‘flat tax’’ by accident rather than by design. As

the regular tax rate schedule is indexed up every year and the AMT rate sched-

ule stays the same, more and more people will be taxed using the AMT’s nearly

flat 26–28 percent rates and significantly limited deductions.

EXAMPLE Gram and Sally are married taxpayers who file a joint tax return.

Their taxable income and regular tax for 2010 are calculated as

follows:

Adjusted gross income $100,000

Itemized deductions:

Home mortgage interest $20,000

Contributions 2,000

Other miscellaneous deductions

(in excess of 2% of AGI)

11,000

Total itemized deductions (33,000)

Exemptions

(7,300)

Taxable income

$ 59,700

Tax from 2010 tax table

$ 8,121

If Gram and Sally have private activity bond interest of $30,000 not

included in arriving at the amount of adjusted gross income shown

above, the amount of their alternative minimum tax is computed as

follows:

Adjusted gross income $100,000

Add: tax preferences and adjustments

30,000

Total 130,000

Less: allowable itemized deductions:

Home mortgage interest $20,000

Contributions

2,000

Total deductions

(22,000)

Alternative minimum taxable income 108,000

The AMT exemption

(71,050)

Alternative minimum tax base

36,950

Tentative minimum tax (26% of $36,950)

$ 9,607

Section 6.8

The Individual Alternative Minimum Tax (AMT) 6-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Since the gross alternative minimum tax is greater than the regular

tax, the taxpayers must pay a net alternative minimum tax of $1,486

($9,607 $8,121).

Their alternative minimum taxable income may also be computed by

starting with taxable income of $59,700, adding the $7,300 of personal

and dependency exemptions, adding back any itemized deductions

which are not allowed for AMT purposes (other miscellaneous deduc-

tions of $11,000), and adding the $30,000 of tax preferences: $59,700 þ

$7,300 þ $11,000 þ $30,000 ¼ $108,000. This method of calculation is

similar to the one followed on Form 6251, Alternative Minimum Tax. N

Many taxpayers in states with high state income tax are finding themselves pay-

ing the alternative minimum tax for the sole reason that their state income taxes

and property taxes are not allowed as a deduction in the AMT calcul ation. Care-

ful timing of state income tax and property tax payments may result in signifi-

cant tax savings for taxpayers in this situation.

Self-Study Problem 6.8

Harold Brown, a single taxpayer, has adjusted gross income of $100,000. He

has a deduction for home mortgage interest of $23,000, cash contributions of

$11,000, property taxes of $10,000, state income taxes of $10,000, and miscel-

laneous itemized deductions (after the 2 percent limitation) of $10,000. Assum-

ing Harold’s regular tax liability is $4,438, use Form 6251 on pages 6-23 and

6-24 to calculate the amount of Harold’s net alternative minimum tax. (Hint:

First calculate taxable income before personal exemptions are taken, the start-

ing point of Form 6251.)

Your client, William Warrant, was hired for a management position at an

Internet company planning to start a Web portal called ‘‘indulgedanimals.

com’’ for dogs, cats, and other pets. When he was hired, William was given

an incentive stock option (ISO) worth $500,000, which he exercised during

the yea r. Exercise of the ISO creates a tax preference item for the alterna-

tive minimum tax (AMT) and causes him to have to pay substantial addi-

tional tax when combined with his other tax items for the year. He is livid

about the extra tax and refuses to file the AMT Form 6251 with his tax

return because the AMT tax is ‘‘unfair’’ and ‘‘un-American’’ according to

him. Would you sign this tax return?

6-22 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 6.8

The Individual Alternative Minimum Tax (AMT) 6-23

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

6-24 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 6.9

UNEARNED INCOME OF MINOR CHILDREN

Many parents have found it beneficial from a tax-planning standpoint to give income-

earning assets, such as stocks, bonds, bank certificates of deposit, and mutual funds, to

their minor children. Since the children are generally in a lower income tax bracket,

the income from assets such as interest, dividends, and capital gains on stock sale has tra-

ditionally been taxed at a lower rate than the parents’ rate. However, tax law contains

provisions that limit the benefit o f shifting income to certain dependent children. The

net unearned income of dependent children may be taxed at their parents’ rates. This

parental tax rate applies to children who are 18 or younger at the end of the year or stu-

dents ages 19 through 23, who have at least one living parent, and who have ‘‘net

unearned income’’ for the year. Although there is no statutory definition for a parent,

the term is generally considered to mean a parent or step-parent of the child.

For purposes of determining the child’s (or young adult’s ) income subject to the paren-

tal tax rate, net unearned income is never considered to include wages or salary of a minor

child and is computed as follows:

Unearned income $xxxx.xx

Less the greater of:

1. $950 (child’s standard deduction), or

2. The allowable itemized deductions

directly connected with the

production of the unearned income (

xxx.xx)

xxxx.xx

Less statutory deduction (

950.00)

Net unearned income

$xxxx.xx

If the net unearned income is zero or less, the child’s tax is calculated using the child’s

tax rate. However, if the amount is positive, the child’s tax is calculated by applying the

parents’ tax rate, if higher, to that amount.

EXAMPLE Dyana and Mark have two children, Alex (age 1) and Nathan (age 7).

Alex received $4,000 in interest income and Nathan received $3,000 in

interest income during 2010. Alex and Nathan did not pay any invest-

ment expenses for the year. Dyana and Mark have taxable income for

the year of $45,050. Alex and Nathan’s 2010 income tax is calculated

as follows:

Step 1: Calculate Net Unearned Income Alex Nathan

Unearned income $4,000 $3,000

Less the greater of:

$950 (standa rd deduction), or

investment expenses

(950) (950)

3,050 2,050

Less statutory deduction

(950) (950)

Net unearned income

$2,100 $1,100

Section 6.9

Unearned Income of Minor Children 6-25

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Step 2: Calculate the Total Parental Tax

Parents’ taxable income $45,050

Plus: the children’s net unearned

income ($2,100 þ $1,100)

3,200

Revised taxable income

$48,250

Tax on revised income (from tax table) $ 6,404

Tax on parents’ regular income ($45,050)

(5,924)

Total parental tax

$ 480

Step 3: Allocate Total Parental Tax

Alex’s parental tax

$2,100

($2,100 þ $1,100)

$480 ¼

$315

Nathan’s parental tax

$1,100

($2,100 þ $1,100)

$480 ¼

$165

Step 4: Calculate Total Tax Alex Nathan

Regular 10% tax on $950 $ 95 $ 95

Plus allocable parental tax

315 165

Total tax

$410 $260

Both Alex and Nathan must include a Form 8615, Tax for Children

Under Age 18 Who Have Investment Income of More Than $1,900,

with their individual income tax returns. N

If a child’s parents are divorced, the taxable income of the parent with custody is used to

calculate the parental tax. Also, if married parents file separate returns, the parent’s return

with the larger amount of taxable income is used in the calculation.

Election to Include a Child’s Unearned Income on Parents’ Return

If certain conditions are met, parents may elect to include a child’s gross income on the

parents’ tax return. The election eliminates the child’s return filing requirements and

saves the parents the trouble of filing the special c alculation Form 8615 for the ‘‘kiddie

tax.’’ To qualify for this election, the following conditions must be met:

1. The child’s gross income is from interest and dividends only.

2. The gross income is more than $950 and less than $9,500.

3. No estimated tax has been paid in the name of the child and the child is not subject

to backup withholding.

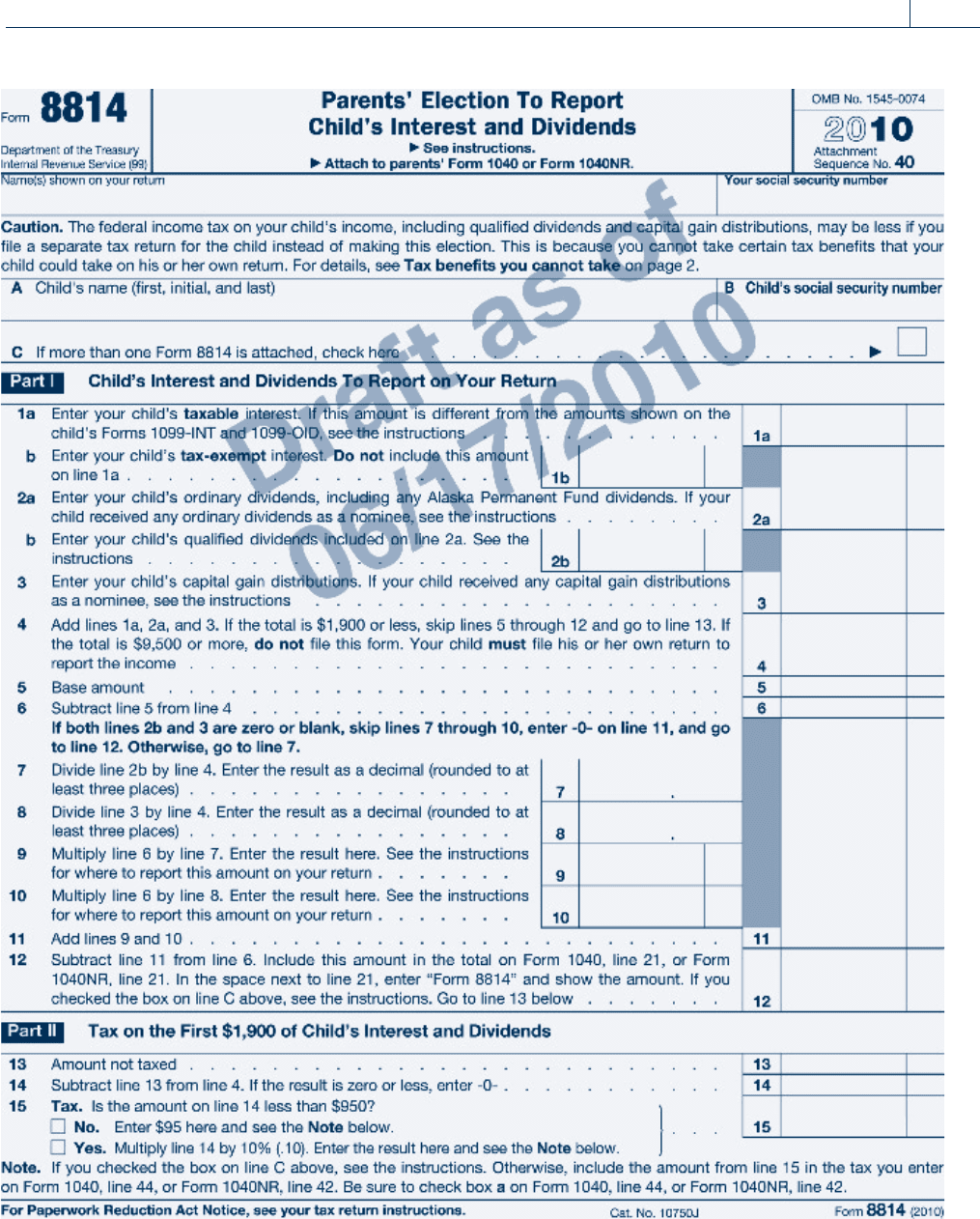

EXAMPLE Sam is 12 years old and has $2,300 of interest from a savings

accountsetupforhimbyhisgrandparents.ThisisSam’sonly

income for the year. Instead of completing the Kiddie Tax Form

(Form 8615) and paying the tax on his $2,300 in income, Sam’s

parents may elect to include the $2,300 on their tax return thereby

eliminating Sam’s filing requirement. The election to include the

income of a minor child on the parents’ return is made on Form

8814, as illustrated on page 6-27. N

6-26 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

2,300

Sam’s Parents

Sam

2,300

1,900

400

400

0

950

1,350

x

95

Section 6.9

Unearned Income of Minor Children 6-27

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

6-28 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 6.10

COMMUNITY PROPERTY

When married couples file separate income tax returns, a special problem arises. Income

derived from property held by a married couple, either jointly or separately, as well as

wages and other income earned by a husband and wife, must be allocated between the

spouses. State law becomes important in making this allocation.

The law in nine states is based on a community property system of marital law. In these

states, the property rights of married couples differ from the property r ight s of married

couples residing in the remaining common law states. The nine states that are community

property states are:

Arizona Louisiana Texas

California Nevada Washington

Idaho New Mexico Wisconsin

Under the community property system, all property is deemed to be either separate

property or community property. Separate property includes property acquired by a spouse

before marriage or received after marriage as a gift or inheritance. All other property

owned by a married couple is presumed to be community property. For federal income

tax purposes, each spouse is automatically taxed on half of the income from community

property.

The tax treatment of income from separate property depends on the taxpayer’s state

of residence. In Texas, Louisiana, Wisconsin, and Idaho, income from separate prop-

erty produces community income. Thus, just as each spouse is taxed on half of the

income from community property, each spouse is also taxed on half of the income

from separate property. In the other five community property states, income on sepa-

rate property is ‘‘separate income’’ and is reported in full on the tax return of the spouse

who owns the property. Income such as nontaxable dividends or royalties from mineral

interests assumes the classification of the asset from which the income is derived. Cap-

ital gains also retain their classification ba sed on the classification of the property from

which the gain arises.

EXAMPLE John and Marsha are married and live in Texas. John owns, as his sep-

arate property, stock in AT&T Corpora tion. During the year, John

receives dividends of $4,000. Assuming John and Marsha file separate

returns, each of them must report $2,000 of the dividends. On the

other hand, if John and Marsha lived in California, John would report

the entire $4,000 of the dividends on his tax return and Marsha

Self-Study Problem 6.9

Bill and Janet have one child, Robert, who is 9 years old. Robert has inter-

est income of $3,000 for the year. Bill and Janet’s taxable income for the

year is $46,050. Calculate Robert’s tax liability for 2010, assuming Bill and

Janet do not make an election to include Robert’s income on their tax

return.

$ ____________

Section 6.10

Community Property 6-29

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

would not be required to include any of the dividend income on her

tax return. N

In all of the community property states, income from salary and wages is generally

treated as having been earned one-half by each spouse.

EXAMPLE Robert and Linda are married but file separate tax returns. Robert

receives a salary of $30,000 and has interest income of $500 from a

savings account which is in his name. The savings account was estab-

lished with salary earned by Robert since his marriage. Linda collects

$20,000 in dividends on stock she inherited from her father. The

amount of income which Linda must report on her separate income

tax return depends on the state in which Robert and Linda reside.

Three different assumptio ns are presented below:

State of Residence

Texas California Common Law

Salary $15,000 $15,000 0

Dividends 10,000 20,000 $20,000

Interest

250 250 0

Total

$25,250 $35,250 $20,000

N

Spouses Living Apart

To simplify problems that could arise when married spouses residing in a community

property state do not live together, the tax law contains an exception to the above commu-

nity property rules. Under this special provision, a spouse will be taxed only on his or her

actual earnings from personal services. For this provision to apply, the following conditions

must be satisfied:

1. The individuals must live apart for the entire year,

2. They must no t file a joint return, and

3. No portion of the earned income may be transferred between the spouses.

EXAMPLE Bill and Betty, both residents of Nevada, are married but live apart

for the entire year. Bill has a salary of $30,000 and Betty has a salary

of $35,000. Normally, Bill and Betty would each report $32,500. How-

ever, if the required conditions are met, Bill and Betty would each

report their own salary. If Bill and Betty had any unearned income,

such as dividends or interest, the income would be reported under

the general community property rules. The special provision applies

only to earned income of the spouses. N

Another provision addresses the problem of spouses who fail to qualify for the above

special exception because they do not live apart for the entire year. In certain cases, a

spouse who fails to include in income his or her share of community income, as required

6-30 Chapter 6

Credits and Special Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.