Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

19

The Black-Scholes Model

19.1 Overview

In a pathbreaking paper published in 1973, Fisher Black and Myron

Scholes proved a formula for pricing European call and put options on

non-dividend-paying stocks. Their model is probably the most famous

model of modern fi nance. The Black-Scholes formula is relatively easy

to use, and it is often an adequate approximation to the price of more

complicated options.

In this chapter we make no pretense at a full-blown development of

the model; this requires a knowledge of stochastic processes and a not-

inconsiderable mathematical investment. Instead, we shall describe the

mechanics of the model and show how to implement it in Excel. We also

illustrate several uses of the Black-Scholes formula in the valuation of

structured assets.

19.2 The Black-Scholes Model

Consider a stock whose price is lognormally distributed.

1

The Black-

Scholes model uses the following formula to price European calls on a

stock:

C SNd Xe Nd

rT

=−

−

() ()

12

where

d

SX r T

T

dd T

1

2

21

=

++

=−

ln / /2)()(

σ

σ

σ

Here C denotes the price of a call, S is the price of the underlying

stock, X is the exercise price of the call, T is the call’s time to exercise, r

is the interest rate, and σ is the standard deviation of the logarithm of

the stock’s return. N( ) denotes a value of the standard normal distribu-

tion. It is assumed that the stock will pay no dividends before date T.

By the put-call parity theorem (see Chapter 16), a put with the same

exercise date T and exercise price X written on the same stock will have

1. The lognormal distribution is discussed in Chapter 18.

510 Chapter 19

price P = C − S + Xe

−rT

. Substituting for C in this equation and doing

some algebra gives the Black-Scholes European-put-pricing formula:

PXeNd SNd

rT

=−−−

−

() ()

21

We note that in Chapter 17 we hinted at one form of the proof of the

Black-Scholes formula. There it was shown numerically that the Black-

Scholes formula coincides with the binomial option-pricing model

formula when (1) the length of a typical period approaches 0, (2) the

“up” and “down” moves in the binomial model converge to a lognormal

price process, and (3) the term structure of interest rates is fl at.

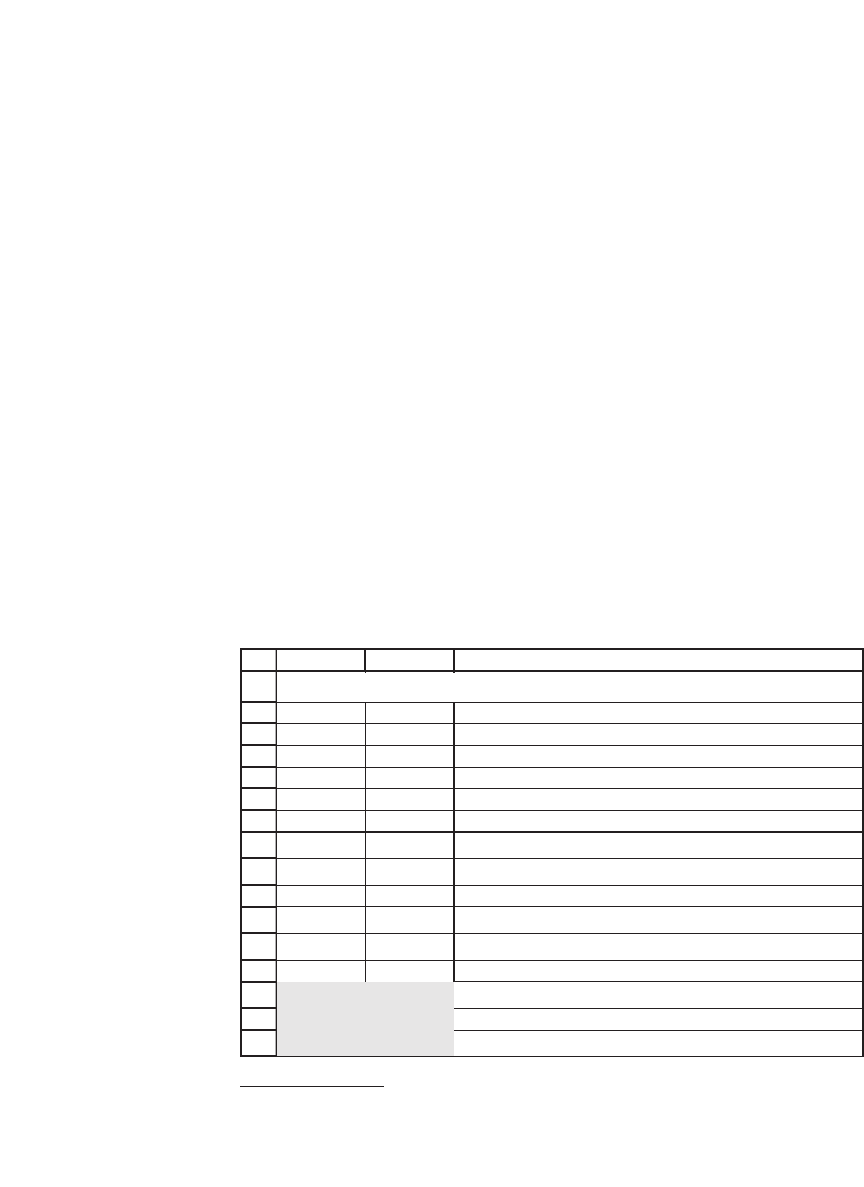

19.2.1 Implementing the Black-Scholes Formulas in a Spreadsheet

The Black-Scholes formulas for call and put pricing are easily imple-

mented in a spreadsheet. The following example shows how to calculate

the price of a call option written on a stock whose current price S = 50,

when the exercise price X = 45, the annualized interest rate r = 4 percent,

and σ = 30 percent. The option has T = 0.75 years to exercise. All three

of the parameters T, r, and σ are assumed to be in annual terms.

2

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

AB C

S 50 Current stock price

X 45 Exercise price

r 4.00% Risk-free rate of interest

T 0.75 Time to maturity of option (in years)

Sigma 30%

Stock volatility,

σ

d

1

0.6509 <-- (LN(S/X)+(r+0.5*sigma^2)*T)/(sigma*SQRT(T))

d

2

0.3911

<-- d

1

-sigma*SQRT(T)

N(d

1

)

0.7424

<-- Uses formula NormSDist(d

1

)

N(d

2

)

0.6521

<-- Uses formula NormSDist(d

2

)

Call price 8.64

<-- S*N(d

1

)-X*exp(-r*T)*N(d

2

)

Put price 2.31 <-- call price - S + X*Exp(-r*T): by Put-Call parity

2.31

<-- X*exp(-r*T)*N(-d

2

) - S*N(-d

1

): direct formula

Black-Scholes Option-Pricing Formula

2. Section 18.7 discusses how to calculate the annualized σ of the lognormal process given

nonannual data.

511 The Black-Scholes Model

The spreadsheet calculates the put price twice: In cell B15 the put price

is computed by using put-call parity, and in cell B16 it is calculated by

using the direct Black-Scholes formula.

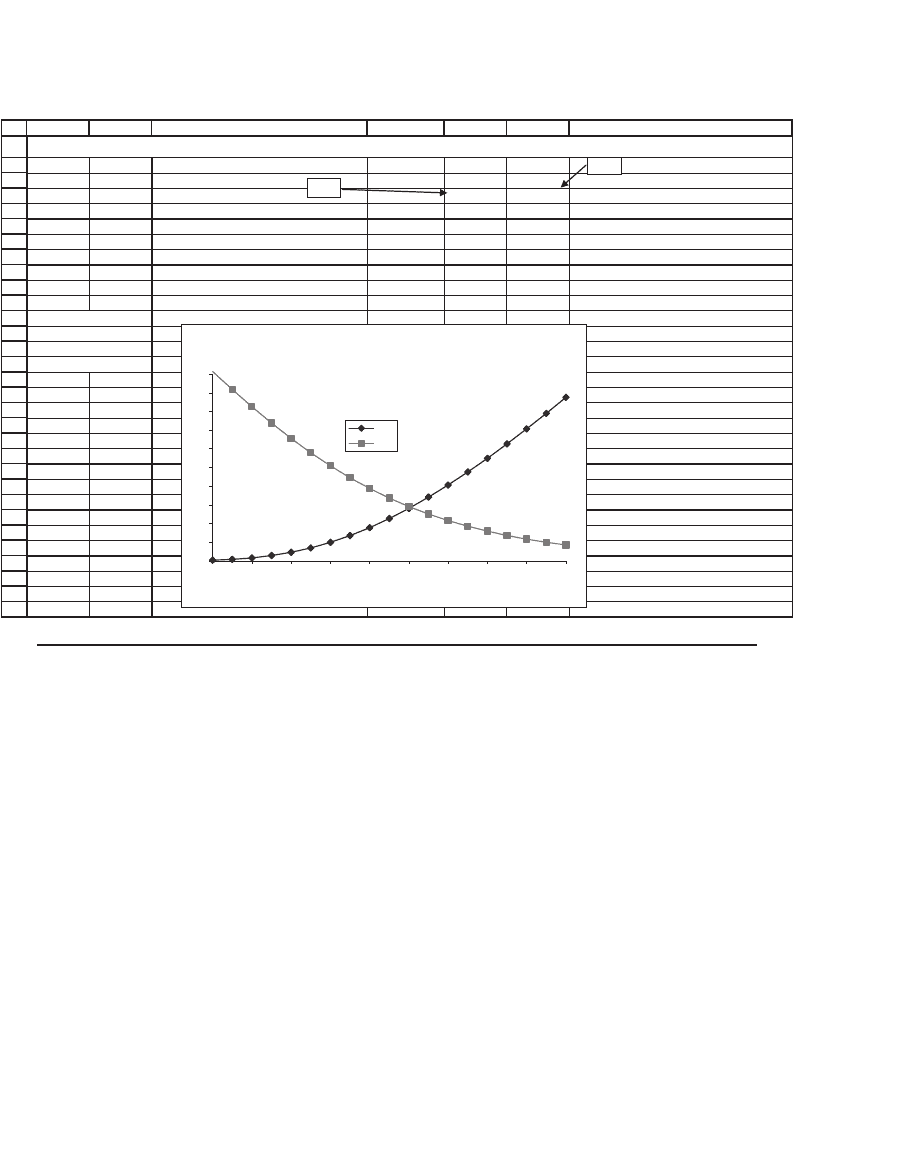

We can use this spreadsheet to do the usual sensitivity analysis. For

example, the following Data|Table (see Chapter 31) gives—as the stock

price S varies—the Black-Scholes value of the call compared to its intrin-

sic value [i.e., max(S − X, 0)].

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

DCEFGHIJKL

Stock

price

Call

price

Intrinsic

value

8.6434 5

5 0.0000 0

10 0.0000 0

15 0.0000 0

20 0.0029 0

25 0.0484 0

30 0.3101 0

35 1.1077 0

40 2.7319 0

45 5.2777 0

50 8.6434 5

55 12.6307 10

60 17.0378 15

65 21.7056 20

70 26.5256 25

75 31.4304 30

80 36.3811 35

Data table: Comparing

the Black-Scholes

to the intrinsic value

M

Black-Scholes Price versus Instrinsic Value

0

5

10

15

20

25

30

35

0 1020304050607080

Stock price, S

Call

price

Intrinsic

value

Data table header:

= B14

Data table header:

=Max(B2-B3,0).

This is the option's

intrinsic value

.

19.3 Using VBA to Defi ne a Black-Scholes Pricing Function

Although the spreadsheet implementation of the Black-Scholes formu-

las illustrated in the previous section is suffi cient for some purposes, we

are sometimes interested in having a closed-form function that we can

use directly in Excel. We can do so with Visual Basic for Applications. In

the following program we defi ne functions dOne, dTwo, and BSCall:

Function dOne(Stock, Exercise, Time, Interest, sigma)

dOne = (Log(Stock / Exercise) + Interest * _

Time) / (sigma * Sqr(Time)) _

+ 0.5 * sigma * Sqr(Time)

End Function

512 Chapter 19

Note the use of the Excel function NormSDist, which gives the standard

normal distribution; in order to use this function in VBA, we must write

Application.NormSDist.

19.3.1 Pricing Puts

By the put-call parity theorem we know that a put is priced by the

formula P = C − S + Xe

−rT

. We can implement this in another VBA

function, BSPut:

Function dTwo(Stock, Exercise, Time, Interest, sigma)

dTwo = dOne(Stock, Exercise, Time, Interest, _

sigma) - sigma * Sqr(Time)

End Function

Function BSCall(Stock, Exercise, Time, Interest, sigma)

BSCall = Stock * Application.NormSDist(dOne(Stock, _

Exercise, Time, Interest, sigma)) - _

Exercise * Exp(-Time * Interest) * _

Application.NormSDist(dTwo(Stock, Exercise, _

Time, Interest, sigma))

End Function

Function BSPut(Stock, Exercise, Time, Interest, sigma)

BSPut = BSCall(Stock, Exercise, Time, Interest, _

sigma) + Exercise * Exp(-Interest * Time) - Stock

End Function

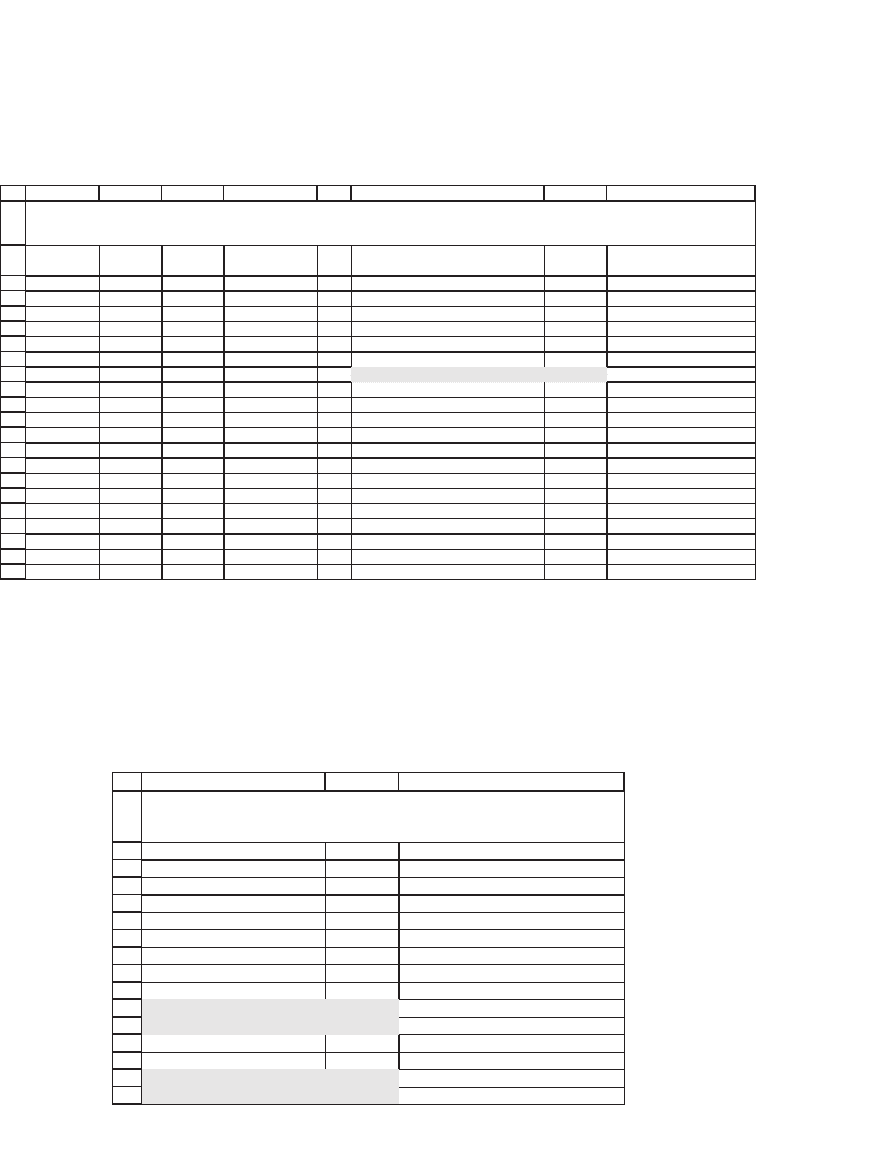

19.3.2 Using These Functions in an Excel Spreadsheet

Here’s an example of these functions used in Excel. The graph was

created by a data table. (In presentations we usually hide the fi rst row

of such a table; here we have shown it.)

513 The Black-Scholes Model

19.4 Calculating the Implied Volatility

The Black-Scholes formula depends on fi ve parameters: The stock price

S, the option exercise price X, the option’s time to maturity T, the interest

rate r, and the standard deviation of the returns of the stock underlying

the option σ (sigma). Four of these fi ve parameters are straightforward,

but the fi fth parameter, σ, is problematic. There are two common ways

of computing σ:

•

σ can be computed based on the historical returns of the stock.

•

σ can be computed based on the implied volatility of the stock.

In the two subsections that follow, we illustrate both methods of comput-

ing σ.

19.4.1 The Sigma of Historical Returns

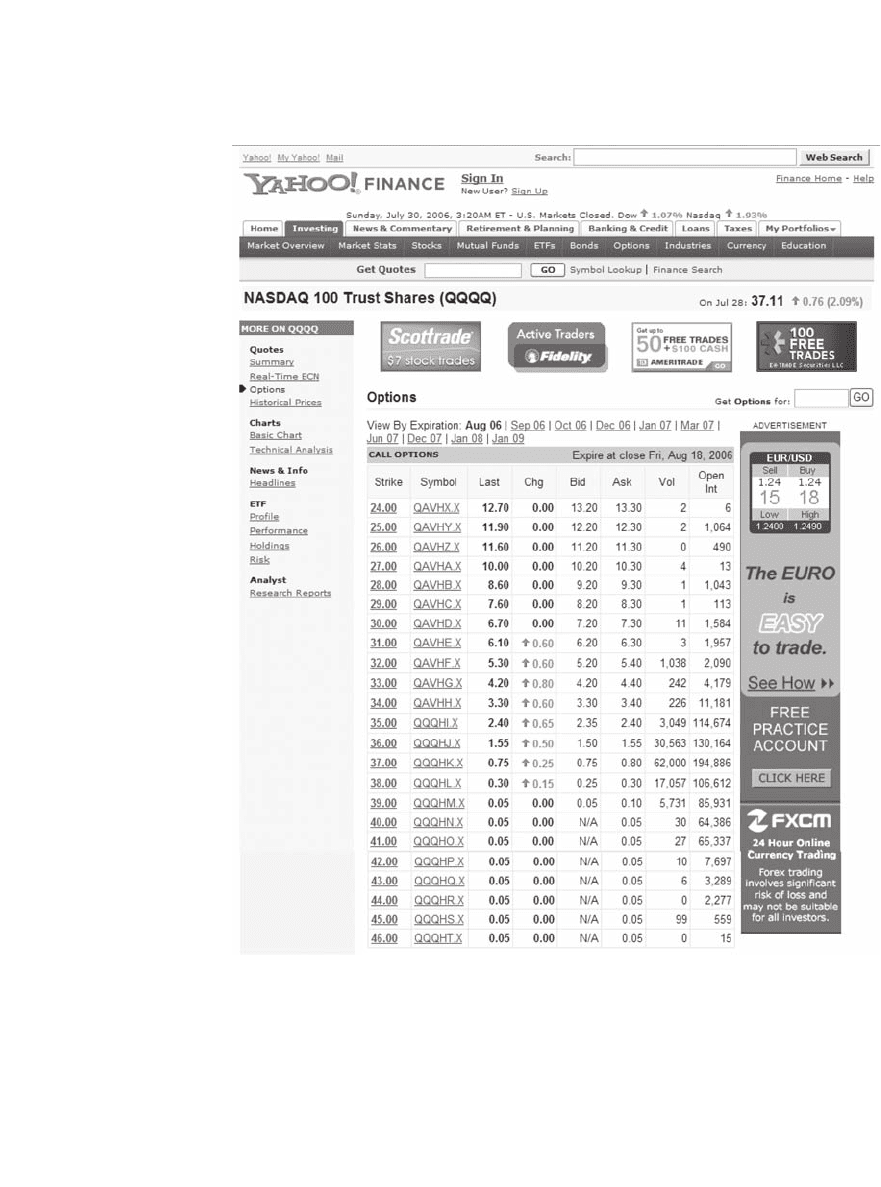

We examine the option prices on the Nasdaq index QQQQ on 28 July 2006.

A complete listing of these prices (from Yahoo) is given in Figure 19.1.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

AB C D EF G

S100

X100

Stock price Call Put

T 1.00 20.3185 10.8022 <--This is the header of the Data Table

Interest 10.00% 40 0.1802 50.6639

Sigma 40.00% 45 0.4104 45.8941

50 0.8081 41.2918

Call price 20.3185 <-- =BSCall(B2,B3,B4,B5,B6) 55 1.4241 36.9079

Put price 10.8022 <-- =BSPut(B2,B3,B4,B5,B6) 60 2.3019 32.7857

65 3.4739 28.9576

70 4.9600 25.4437

To the right is a data 75 6.7683 22.2520

table that gives the 80 8.8965 19.3803

call and put values for 85 11.3341 16.8179

various stock 90 14.0645 14.5482

6055.219660.7159 .secirp

100 20.3185 10.8022

105 23.7954 9.2791

110 27.4740 7.9578

115 31.3316 6.8154

120 35.3469 5.8306

125 39.5002 4.9839

130 43.7736 4.2574

BLACK-SCHOLES MODEL IN VBA

=B8

=B9

Call and Put Prices Using Black-Scholes

0

5

10

15

20

25

30

35

40

45

50

40 50 60 70 80 90 100 110 120 130

Stock price, S

Call

Put

514 Chapter 19

Figure 19.1

QQQQ index call prices, 28 July 2006. The highlighted prices are for in-the-money

options.

515 The Black-Scholes Model

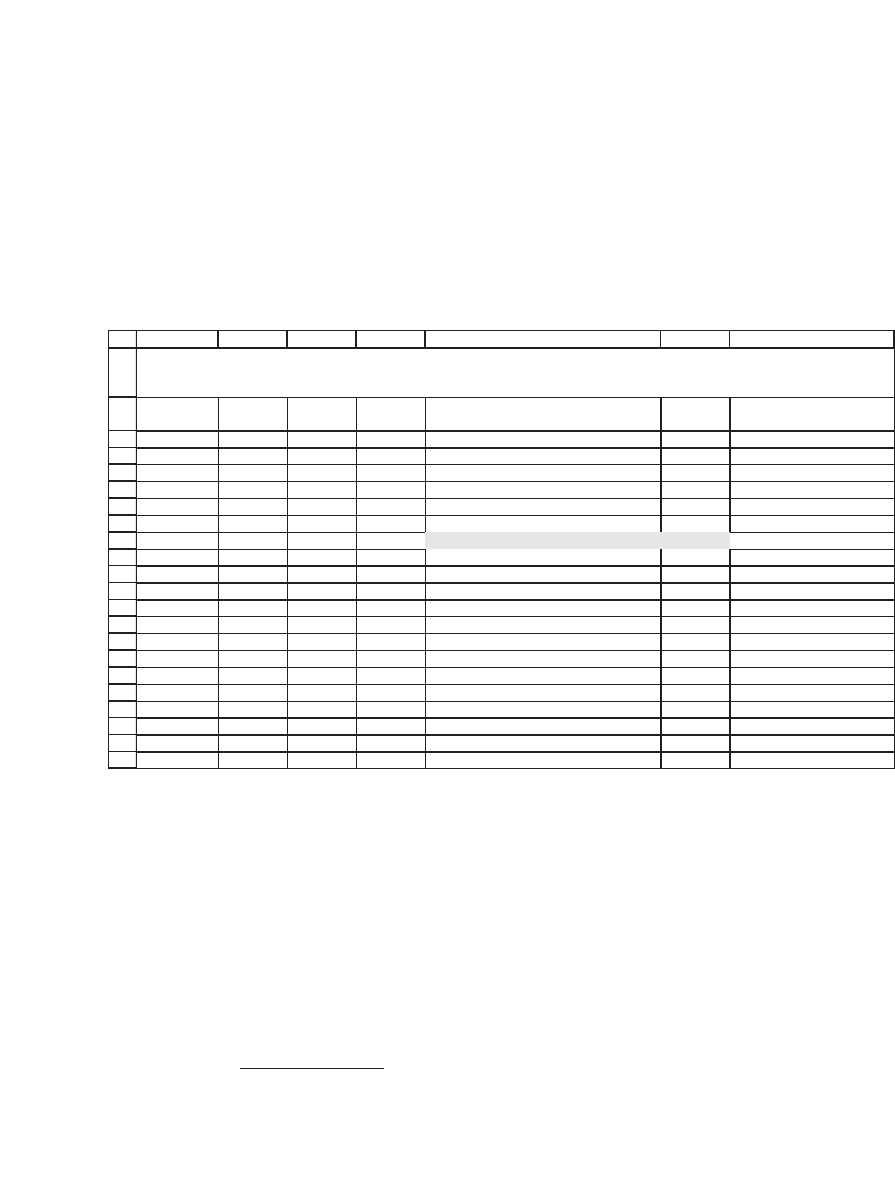

The historical prices of the QQQQ and the resulting historical volatil-

ity are computed in the next spreadsheet:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

38

39

40

41

42

43

44

45

ABC DE F G H

Date

Closing

price

Return

30-May-06 38.61

31-May-06 38.79 0.47% <-- =LN(B4/B3)

Return statistics

1-Jun-06 39.71 2.34% <-- =LN(B5/B4) Average daily return -0.09% <-- =AVERAGE(C4:C45)

2-Jun-06 39.61 -0.25% <-- =LN(B6/B5) Standard deviation of daily return 1.31% <-- =STDEVP(C4:C45)

5-Jun-06 38.75 -2.20% <-- =LN(B7/B6)

6-Jun-06 38.72 -0.08% Annualized mean return -23.59% <-- =250*G5

7-Jun-06 38.43 -0.75% Annualized sigma 20.66% <-- =G6*SQRT(250)

8-Jun-06 38.37 -0.16%

9-Jun-06 38.12 -0.65%

12-Jun-06 37.37 -1.99%

13-Jun-06 37.22 -0.40%

14-Jun-06 37.6 1.02%

19-Jul-06 36.62 1.29%

20-Jul-06 36.08 -1.49%

21-Jul-06 35.7 -1.06%

24-Jul-06 36.41 1.97%

25-Jul-06 36.62 0.58%

26-Jul-06 36.59 -0.08%

27-Jul-06 36.35 -0.66%

28-Jul-06 37.11 2.07%

QQQQ HISTORICAL PRICES, DAILY DATA

and resulting statistics

Based on two months of daily data, the annualized QQQQ sigma is

20.66 percent. Note that this result is based on the assumption of 250

trading days per year; many traders use 365 days, which would of course

give a higher σ. Based on this volatility, the at-the-money QQQQ August

2006 call would be priced at 0.85 and the QQQQ August 2006 put would

be priced at 0.63 (cell B12):

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

AB C

Current date 28-Jul-06

Option expiration date 18-Aug-06

3S 7.11

3X7

T 0.06 <-- =(B3-B2)/365

Interest 5.00%

Sigma 20.66%

Call price 0.8447 <-- =BSCall(B5,B6,B7,B8,B9)

Put price 0.6284 <-- =BSPut(B5,B6,B7,B8,B9)

Actual prices

Call 0.75

Put 0.55

PRICING THE AUGUST 2006 QQQQ OPTIONS

σ

Using the Historical Volatility

σ

516 Chapter 19

Compared to the actual prices, this picture seems to indicate that the

historical volatility somewhat overstates the volatility at which the

options are actually priced. Note, however, that it is not clear which data

are the correct historical data. If, for example, we were to use two years

of monthly data to determine the historical volatility for the QQQQ, we

would arrive at a much lower number:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

38

39

40

41

42

43

44

45

ABCD E F G

Date

Closing

p

rice

Return

30-Jul-04 34.40

2-Aug-04 33.54 -2.53%

Return statistics

1-Sep-04 34.64 3.23% Average monthly return 0.18% <-- =AVERAGE(C4:C45)

1-Oct-04 36.38 4.90% Standard deviation of monthly return 3.31% <-- =STDEVP(C4:C45)

1-Nov-04 38.57 5.85%

1-Dec-04 39.73 2.96% Annualized mean return 2.17% <-- =12*F5

3-Jan-05 37.22 -6.53% Annualized sigma 11.48% <-- =F6*SQRT(12)

1-Feb-05 37.05 -0.46%

1-Mar-05 36.40 -1.77%

1-Apr-05 34.82 -4.44%

2-May-05 37.90 8.48%

1-Jun-05 36.64 -3.38%

19-Jul-06 36.62 1.29%

20-Jul-06 36.08 -1.49%

21-Jul-06 35.70 -1.06%

24-Jul-06 36.41 1.97%

25-Jul-06 36.62 0.58%

26-Jul-06 36.59 -0.08%

27-Jul-06 36.35 -0.66%

28-Jul-06 37.11 2.07%

QQQQ HISTORICAL PRICES, MONTHLY DATA

and resulting statistics

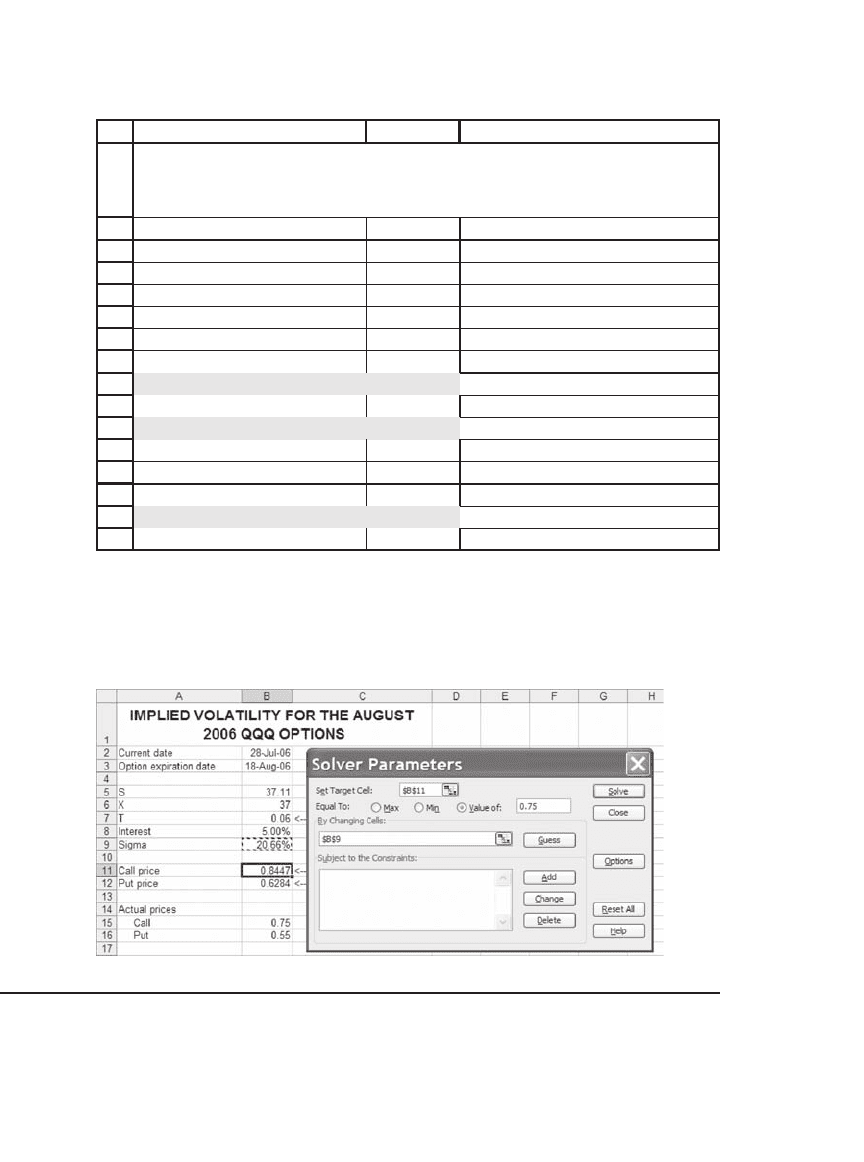

19.4.2 The Implied Volatility

The implied volatility ignores history; instead it determines the option

σ based on actual option prices. Whereas the historical volatility is a

backward-looking volatility, the implied volatility is a forward-looking

estimate.

3

To estimate the implied volatility for the August 2006 QQQQ calls, we

solve the Black-Scholes formula for the sigma that gives the current

market price:

3. The nomenclature “forward-looking” versus “backward-looking” makes it sound as if

the implied volatility is always better than the historical. This is, of course, not the

intention.

517 The Black-Scholes Model

The implied volatility is 17.96 percent. This exactly gives the market

call price of $0.75 (cell B15) and almost gives the market put price of

$0.55 (cell B16). We solved the problem by using Solver:

1

2

3

4

5

6

7

8

9

10

11

13

12

14

15

16

AB C

Current date 28-Jul-06

Option expiration date 18-Aug-06

S 37.11

3X7

T 0.06 <-- =(B3-B2)/365

Int

Im

Put price 0.5337 <-- =BSPut(B5,B6,B7,B8,B9)

Actual prices

Put

IMPLIED VOLATILITY FOR THE

AUGUST 2006 QQQQ OPTIONS

erest 5.00%

plied volatility,

σ

17.96%

Call price 0.7500 <-- =BSCall(B5,B6,B7,B8,B9)

Call 0.75

0.55

19.5 A VBA Function to Find the Implied Variance

We want to design a Visual Basic for Applications function that com-

putes the implied volatility. To do so, we fi rst note that the option price