Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 15, Using SML and WACC page 2

Overview

This is the second of two chapters that show the use of the security market line (SML).

In the Chapter 14 we discussed the use of the SML for performance measurement, and this

chapter we discuss how to use the SML to calculate the cost of capital for a firm.

1

We discussed

calculating the firm’s cost of capital in Chapter 6, where we used the Gordon model to calculate

the cost of equity. In this chapter we use the SML to calculate the firm’s cost of capital. These

two models—the Gordon model and the SML—are the major approaches to computing the

firm’s cost of capital.

Finance concepts discussed in this chapter

• The use of security market line (SML) to calculate the cost of equity r

E

for a firm.

• Calculating the firm’s weighted average cost of capital (WACC). Note that the

computation of the WACC was also discussed in Chapter 6, where we used the Gordon

model to calculate the firm’s cost of equity r

E

.

• Calculating the market value of the firm’s debt and equity, the firm’s tax rate T

C

, and the

firm’s cost of debt r

D

. Our discussion of these issues in this chapter is in many ways a

repeat of a similar discussion in Chapter 6.

• The concept of asset beta,

β

Assets

and its use as an alternative method to calculate the

firm’s WACC.

Throughout this chapter we assume that you know how to calculate the

β

of a stock (this

issue was discussed in the previous chapter). In actual fact you often don’t have to compute the

1

If you need a lightning review of the SML, look at the first section of Chapter 13.

PFE Chapter 15, Using SML and WACC page 3

β

of a firm’s shares—the information is publicly available (in this chapter, for example, we use

data on

β

provided by Yahoo).

Excel functions used

• NPV

• Countif

15.1. The CAPM and the firm’s cost of equity—an initial example

Abracadabra Inc. is considering a new project, which has the following free cash flows.

2

3

4

5

6

7

8

9

10

11

12

13

14

AB

Year FCF

0 -1,000

1 1,323

2 1,569

3 3,288

4 1,029

5 1,425

6 622

7 3,800

8 3,800

9 3,800

10 2,700

In order to decide whether to accept or reject the project, the company needs to calculate

the risk-adjusted discount rate for these cash flows. It decides that the riskiness of the new

project is very much like the riskiness of Abracadabra’s current activities; the financing for the

project is also similar to that of the firm. In this case the appropriate discount rate is the

2

An extended discussion of the free cash flow (FCF) is given in Chapter 6 (section 6.???). Figure 15.1 reviews the

concept in tabular form.

PFE Chapter 15, Using SML and WACC page 4

weighted average cost of capital (WACC); this is the average cost of financing the firm’s

activities. Assuming that Abracadabra has both equity and debt, the formula for the WACC is

given by:

()

*1*

proportion proportion

=

of firm of firm

* * 1 corporate *

cost of cost of

financed by financed by

tax rate

equity debt

equity debt

EDC

C

ED

ED

WACC r r T

ED ED

T=

r= r

=+−

++

⎛⎞ ⎛⎞

⎛⎞⎛⎞ ⎛⎞

⎜⎟ ⎜⎟

⎜⎟

⎜⎟ ⎜⎟

⎜⎟ ⎜

=+−

⎜⎟⎜⎟ ⎜⎟

⎜⎟ ⎜

⎜⎟ ⎜⎟

⎜⎟

⎜⎟ ⎜

⎝⎠ ⎝⎠

⎝⎠

⎜⎟ ⎜

⎝⎠ ⎝⎠

⎟

⎟

⎟

⎟

PFE Chapter 15, Using SML and WACC page 5

[separate page]

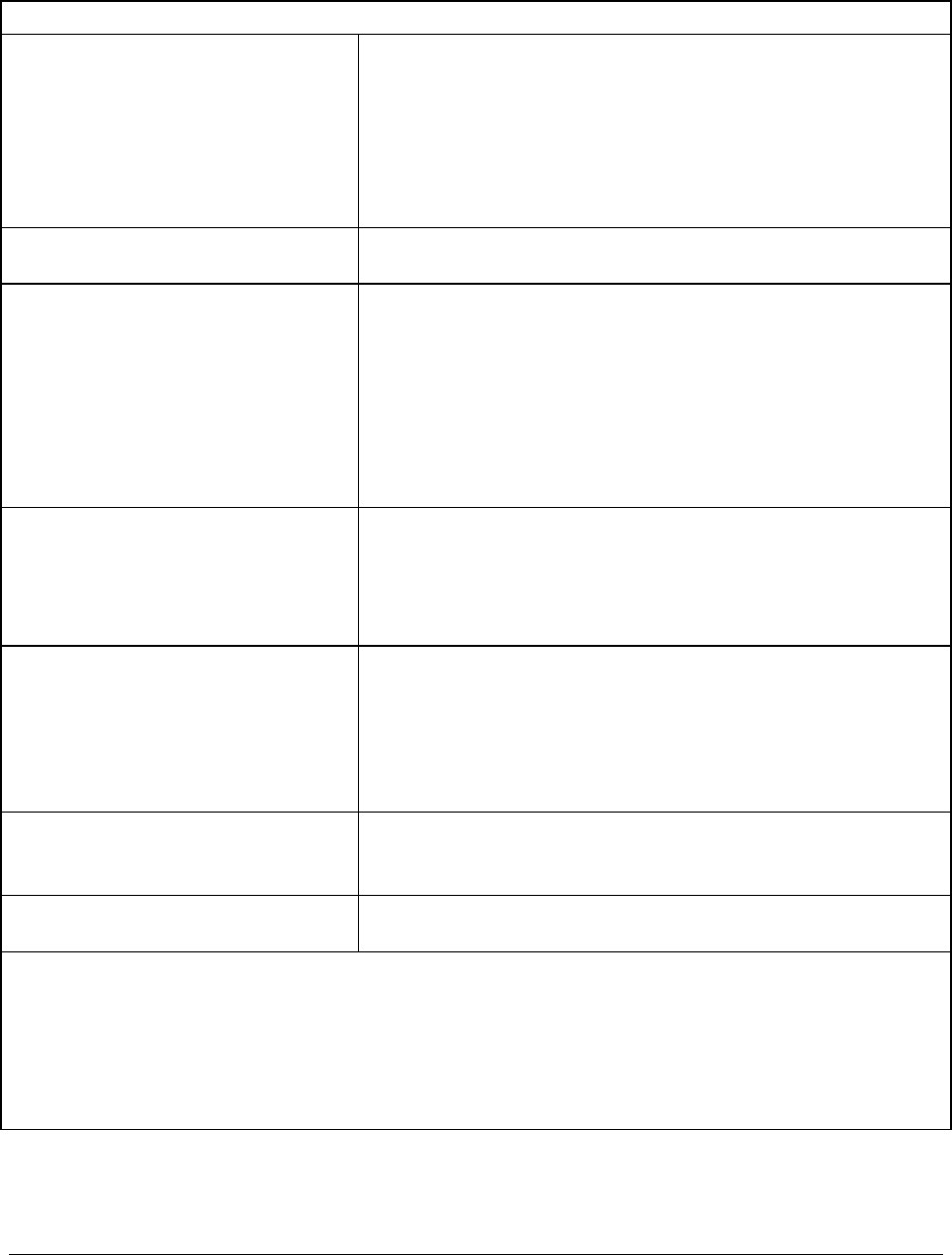

Defining the Free Cash Flow

Profit after taxes This is the basic measure of the profitability of the

business, but it is an accounting measure that includes

financing flows (such as interest), as well as non-cash

expenses such as depreciation. Profit after taxes does not

account for either changes in the firm’s working capital or

purchases of new fixed assets, both of which can be

important cash drains on the firm.

+ Depreciation This noncash expense is added back to the profit after tax.

+ after-tax interest payments (net) FCF is an attempt to measure the cash produced by the

business activity of the firm. To neutralize the effect of

interest payments on the firm’s profits, we:

•

Add back the after-tax cost of interest on debt

(after-tax since interest payments are tax-

deductible),

•

Subtract out the after-tax interest payments on cash

and marketable securities.

- Increase in current assets When the firm’s sales increase, more investment is needed

in inventories, accounts receivable, etc. This increase in

current assets is not an expense for tax purposes (and is

therefore ignored in the profit after taxes), but it is a cash

drain on the company.

+ Increase in current liabilities An increase in the sales often causes an increase in

financing related to sales (such as accounts payable or taxes

payable). This increase in current liabilities—when related

to sales—provides cash to the firm. Since it is directly

related to sales, we include this cash in the free cash flow

calculations.

- Increase in fixed assets at cost An increase in fixed assets (the long-term productive assets

of the company) is a use of cash, which reduces the firm’s

free cash flow.

FCF = sum of the above

Figure 15.1. The free cash flow (FCF) is the amount of cash generated by a firm’s business

activities. Discounting the FCFs at a firm’s weighted average cost of capital (WACC) gives the

value of the firm. The important concept of FCF was introduced in Chapter 6. It appears in

several other places in this book: In the context of accounting and financial planning models, we

discuss the FCF in Chapters 7, 8, 9. In Chapter 18 we return to the concept of FCF in the context

of stock valuation.

PFE Chapter 15, Using SML and WACC page 6

We can use the SML to calculate the cost of equity for Abracadabra. Here are our

assumptions for this problem:

•

The firm’s stock has a beta

β

= 1.4.

•

The expected market return is E(r

M

) = 10%

•

The risk-free rate r

f

= 4%.

•

Abracadabra’s equity has a market value E = $10,000

•

Abracadabra’s debt has a market value D = $15,000

•

Abracadabra can borrow new funds at a cost of r

D

= 6%.

•

Abracadabra’s corporate tax rate is T

C

= 40%.

The first three assumptions mean that Abracadabra’s cost of equity r

E

as given by the

SML is 12.4%:

(

)

[]

*

4% 1.4* 10% 4% 12.4%

Ef M f

rr Er r

β

⎡⎤

=+ −

⎣⎦

=+ − =

Then Abracadabra’s weighted average cost of capital (WACC) is:

()

()

1

10,000 15,000

12.4%* 6%* 1 40% *

10,000 15,000 10,000 15,000

7.12%

EDC

ED

WACC r r T

ED ED

=+−

++

=+−

++

=

The WACC of 7.12% is the discount rate we will use to determine whether or not Abracadabra

should undertake the project.

The following spreadsheet shows our calculations for the WACC (rows 20-36) and the

NPV calculation for the project (rows 2-16).

PFE Chapter 15, Using SML and WACC page 7

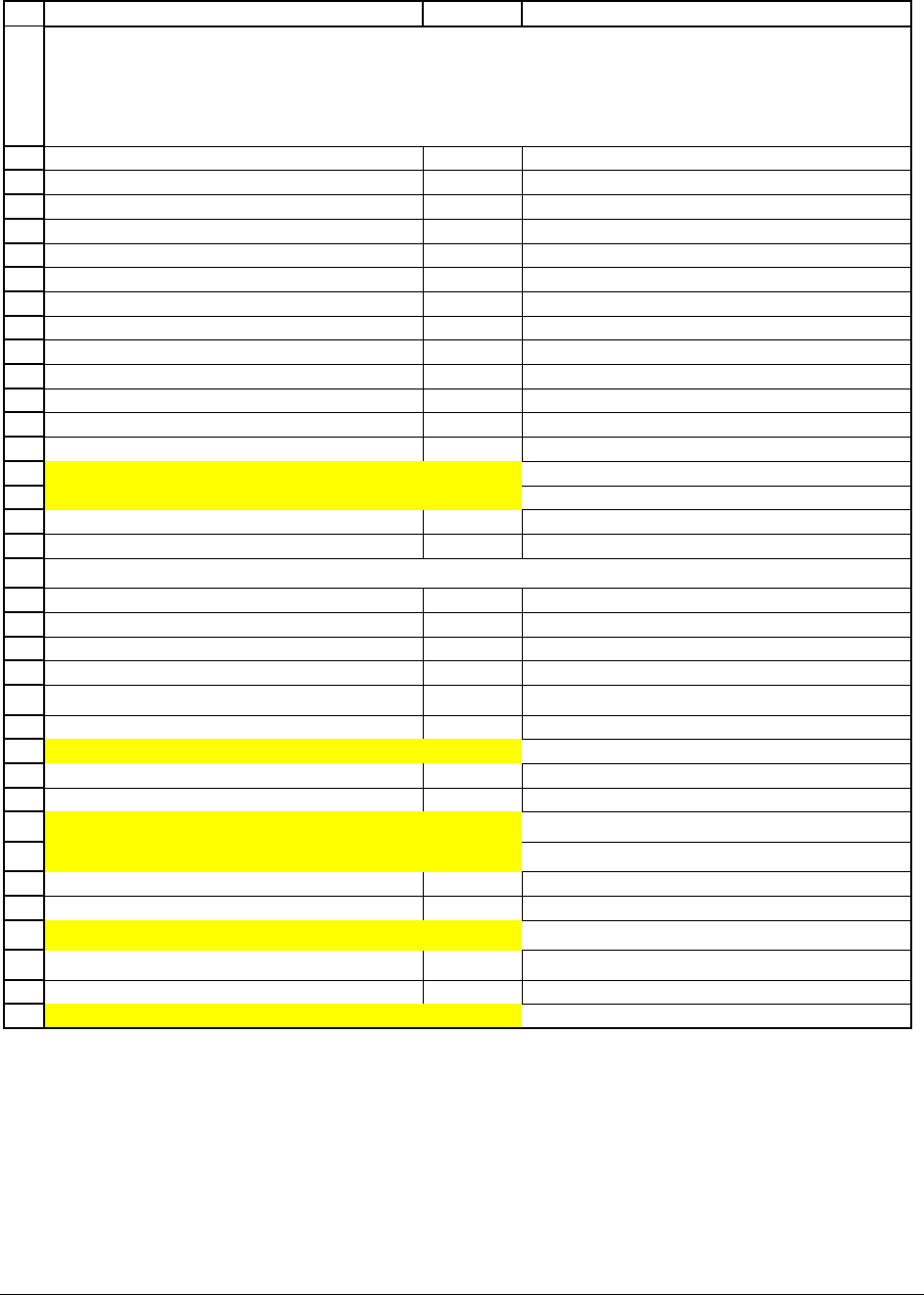

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

AB C

Year FCF

0 -1,000

1 1,323

2 1,569

3 3,288

4 1,029

5 1,425

6 622

7 3,800

8 3,800

9 3,800

10 2,700

Weighted average cost of capital, WACC 7.12% <-- =B36

Project NPV 14,424 <-- =NPV(B15,B4:B13)+B3

Computing Abracadabra's Weighted Average Cost of Capital (WACC)

Market value of equity, E 10,000

Market value of debt, D 15,000

Market value of equity + debt, E+D 25,000

Corporate tax rate, T

C

40%

Abracadabra's stock beta, ≅

1.4

Facts about market

E(r

M

)

10%

r

f

4%

Abracadabra's cost of capital

Cost of equity using SML, r

E

12.40% <-- =B30+B26*(B29-B30)

Cost of debt, r

D

6.00%

Weighted average cost of capital (WACC) 7.12% <-- =B20/B22*B33+B21/B22*B34*(1-B24)

VALUING ABRACADABRA'S INVESTMENT

we calculate the WACC using the SML to

compute the cost of equity r

E

When the project free cash flows are discounted at the WACC, the net present value

(NPV) is $14,424. Since the NPV is positive, Abracadabra should undertake the project.

PFE Chapter 15, Using SML and WACC page 8

Comparing the SML and the Gordon model for calculating the WACC

The weighted average cost of capital is the most widely used discount rate for computing

the value of corporate projects and for computing the value of the firm. The WACC depends

critically on the cost of equity r

E

. In this chapter we compute the cost of equity using the

security market line, whereas in Chapter 6 we computed the cost of equity using the Gordon

dividend model.

The Gordon dividend model and the SML are only two practical ways of calculating the

cost of equity.

3

Both models have their advantages and disadvantages—the Gordon model is

simple to calculate but is very sensitive to assumptions about the firm’s equity payout—the total

dividends plus stock repurchases of the firm. The SML requires relatively more calculations, but

is more widely used. The SML also requires us to make assumptions about the expected return

on the market E(r

M

). This problem is discussed in the next section.

So which model should you use in practice? The best answer is to use both models and to

compare the results. This way each model can serve as a “reality check” on the other. We apply

this logic in Chapter 18, which discusses stock valuation. There we apply both models and

compare the results to see if we have arrived at an appropriate WACC.

3

The academic finance literature has come up with other models for calculating the cost of equity, but in practice

these models are very difficult to apply and rarely used.

PFE Chapter 15, Using SML and WACC page 9

15.2. Using the SML to calculate the cost of capital—calculating the

parameter values

The Abracadabra example of the previous section gives the broad outlines of calculating

the cost of capital using the SML, but it leaves a number of questions unanswered:

•

How do we calculate the market value of a firm’s equity, E?

•

How do we calculate the expected return on the market E(r

M

) ?

•

How do we calculate the risk-free rate, r

f

?

•

How do we calculate the market value of a firm’s debt, D?

•

How do we calculate the firm’s cost of borrowing, r

D

?

•

How do we calculate the firm’s corporate tax rate T

C

?

We discuss each of these questions in turn. Although we occasionally provide an

illustration, we save a full-blown example for the following section.

The market value of a firm’s equity, E

This is easy: For a firm whose shares are sold on the stock market, the market value of

the equity (E in our WACC equation) is the number of shares times the market value per share.

The expected return on the market E(r

M

)

There are two ways to calculate the expected return on the market: 1) We can use the

historical market return, or 2) We can use a version of the Gordon dividend model to derive E(r

M

) from current market data. Neither method is perfect, though we prefer the latter.

E(r

M

) using the historic returns: A standard technique is to use a broad-based index—

usually the S&P 500 index—to proxy for the market portfolio. To do this, you need some data.

PFE Chapter 15, Using SML and WACC page 10

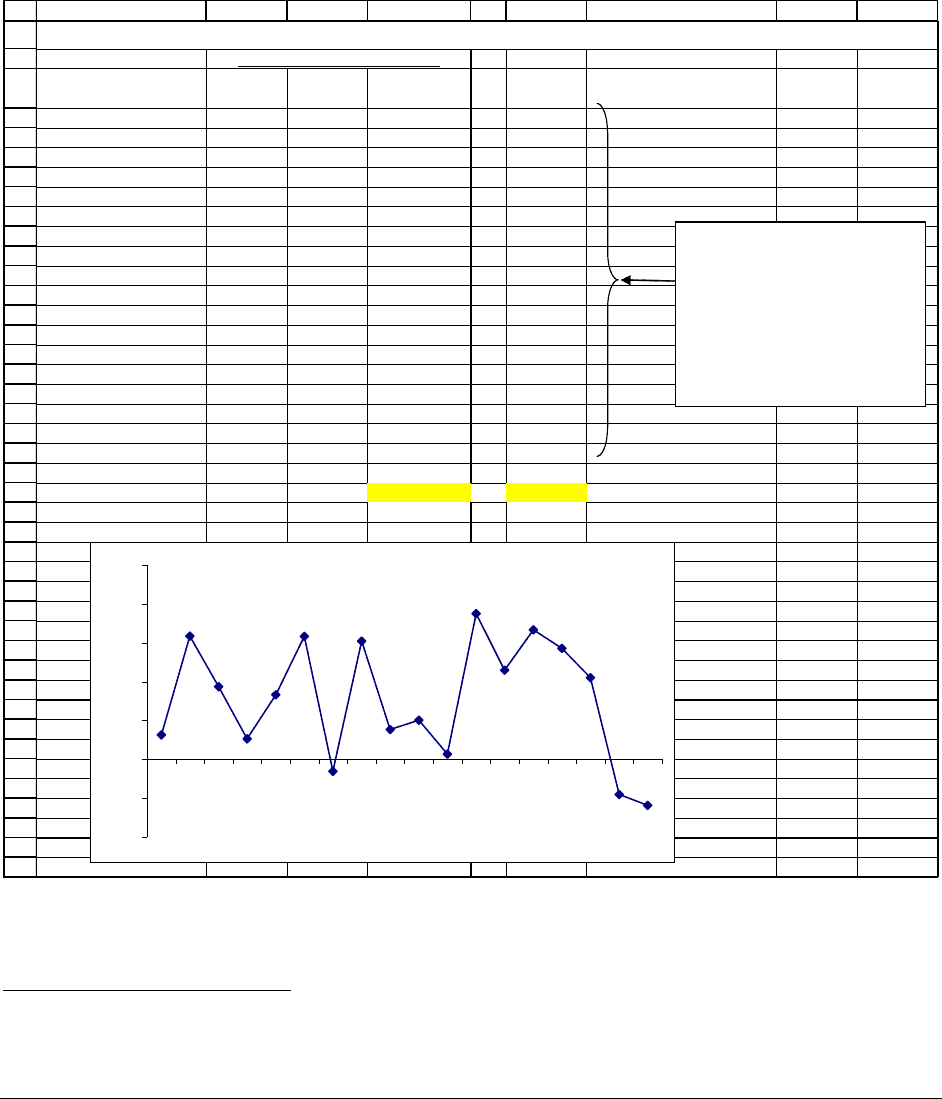

Below we show you the returns on Vanguard’s 500 Index Fund. This is an index mutual fund

which is invested in the S&P 500 index.

4

The average return on the S&P is around 15.51% for

the period 1984-2001 (cell F23). This historical average return is often used as a proxy for the

expected market return in the SML.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

ABCDEF G HI

Year

Capital

return

Income

return

Index 500

Total return

S&P 500

return

1984 1.54% 4.68% 6.22% 6.27%

1985 26.09% 5.14% 31.23% 31.75%

1986 14.04% 4.02% 18.06% 18.68%

1987 2.27% 2.43% 4.70% 5.26%

1988 11.55% 4.67% 16.22% 16.61%

1989 26.67% 4.70% 31.37% 31.69%

1990 -6.84% 3.52% -3.32% -3.10%

1991 26.28% 3.94% 30.22% 30.47%

1992 4.45% 2.97% 7.42% 7.62%

1993 7.06% 2.84% 9.90% 10.08%

1994 -1.51% 2.69% 1.18% 1.32%

1995 34.35% 3.09% 37.44% 37.58%

1996 20.53% 2.35% 22.88% 22.96%

1997 31.11% 2.08% 33.19% 33.36%

1998 27.00% 1.61% 28.61% 28.58%

1999 19.70% 1.37% 21.07% 21.04%

2000 -9.95% 0.90% -9.05% -9.10%

2001 -13.11% 1.08% -12.03% -11.89%

Average

12.29% 3.00% 15.30% 15.51% <-- =AVERAGE(F4:F21)

Standard deviation 14.49% 1.28% 14.89% 14.92% <-- =STDEVP(F4:F21)

Vanguard's 500 Index fund

RETURNS ON THE S&P 500 INDEX, 1984-2001

S&P 500 Return, 1984-2001

-20%

-10%

0%

10%

20%

30%

40%

50%

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

These are the S&P returns

including dividends as given

by Vanguard on its website.

The difference between the total

return on Vanguard's Index 500

portfolio and the total return on

the S&P is largely due to the

management fees of the

Vanguard Index 500 fund.

4

We discussed index funds in the Chapter 14, section 14.4.

PFE Chapter 15, Using SML and WACC page 11

Why use Vanguard instead of Yahoo for S&P Returns?

The usual data sources (for example Yahoo) give only the price data for the S&P 500

index. (This is somewhat strange, since Yahoo’s data for individual stocks is adjusted for

dividends.) Vanguard’s website gives the total return data both for its Index 500 Fund and for

the actual S&P 500 index. The Index 500 Fund’s returns are slightly lower than those of the

S&P 500. This is primarily due to the management fees paid by Index 500 to Vanguard.

E(r

M

) using current market data

This technique is less widely used, though we prefer it.

5

It is based on the Gordon

dividend model that gives the expected return on a stock as a function of the stock’s current

equity payout Div

0

, the current market value of the firm’s equity P

0

, and the expected growth

rate of g of the equity payout. The equity payout is defined as the sum of the firm’s dividends

and its stock repurchases (see Chapter 6, page000 for a full explanation):

()

0

0

0

0

1

where

current equity payout of firm (total dividends + stock repurchases)

current market value of equity

anticipated equity payout growth rate

E

Gordon Dividend Model

Div g

rg

P

Div

P

g

+

=+

=

=

=

To use the Gordon model to calculate the expected return on the market, we restate the

model in terms of the price-earnings ratio: Assume that every year the firm pays out a

5

It was first published in Corporate Finance: A Valuation Approach by Simon Benninga and Oded Sarig,

McGraw-Hill 1997.