Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE, Chapter 6, Weighted average cost of capital page 17

Why do firms repurchase stock?

In recent years share buybacks have exceeded dividends as a form of distribution to

shareholders. Firms repurchase stock instead of paying extra dividends for several reasons:

•

Repurchases are used to “soak up” extra cash and keep dividend growth predictable.

Most dividend-paying firms think their shareholders want to see a steady pattern of

dividend growth. So if they have extra cash, they’ll use it to buy back shares instead of

increasing the dividend paid to shareholders.

•

Repurchases help reduce shareholder taxes on cash paid out to shareholders. When a

dividend is paid, all the shareholders receiving the dividend pay taxes on it at their

ordinary income tax rate. Stock repurchases are voluntary (you don’t have to sell your

stock back to the company ... ). If you let your stock be repurchased, the gain in most

cases is taxed at your capital gains tax rate (lower than the ordinary income tax rate).

•

Stock repurchases benefit both the shareholder who is bought out and the shareholder

who does not let his shares be repurchased. Why? When some of the shares of the firm

are repurchased, those shareholders who “stay in” the firm will get a larger share of its

income and dividend payments in the future. So all parties gain.

6.4. Calculating the WACC for Courier

So far we’ve calculated Courier’s cost of equity as r

E

= 19.36%. This is the return

demanded by the company’s shareholders. Now we want to calculate Courier’s weighted

PFE, Chapter 6, Weighted average cost of capital page 18

average cost of capital

()

1

EDC

ED

WACC r r T

ED ED

=+−

+

+

. Before we can do this, however,

we need to compute the values of the following variables:

•

E: the market value of Courier’s equity. As you can see from the previous spreadsheet,

on September 30, 2000, Courier had 2,938,000 shares worth $21.66 per share. This gives

E = 2,938,000*21.66=$63,637,080.

•

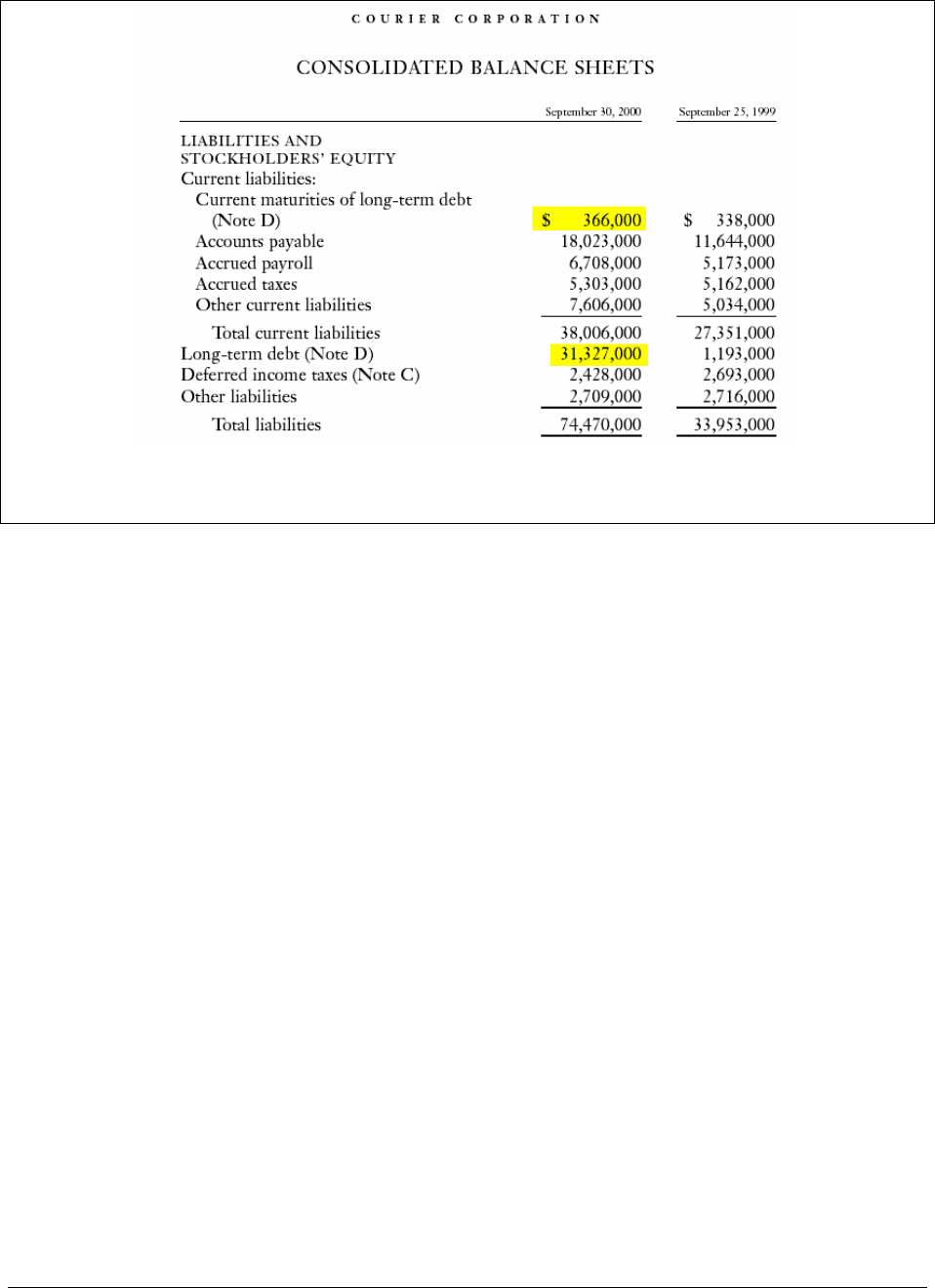

D: The value of Courier’s debt. On 30 September 2000, Courier had debt of

$31,693,000 . This information comes from the company’s annual report (see Figure

6.1). Courier’s

debt includes both the current portion of long-term debt and the long-

term debt itself.

10

10

The calculation of the WACC actually calls for the market value of the firm’s debt. However, this is a number

which is very difficult to calculate; instead it is standard practice to use the book value of the debt as illustrated.

PFE, Chapter 6, Weighted average cost of capital page 19

Figure 6.1: Courier’s liabilities from its balance sheet. The debt items are marked.

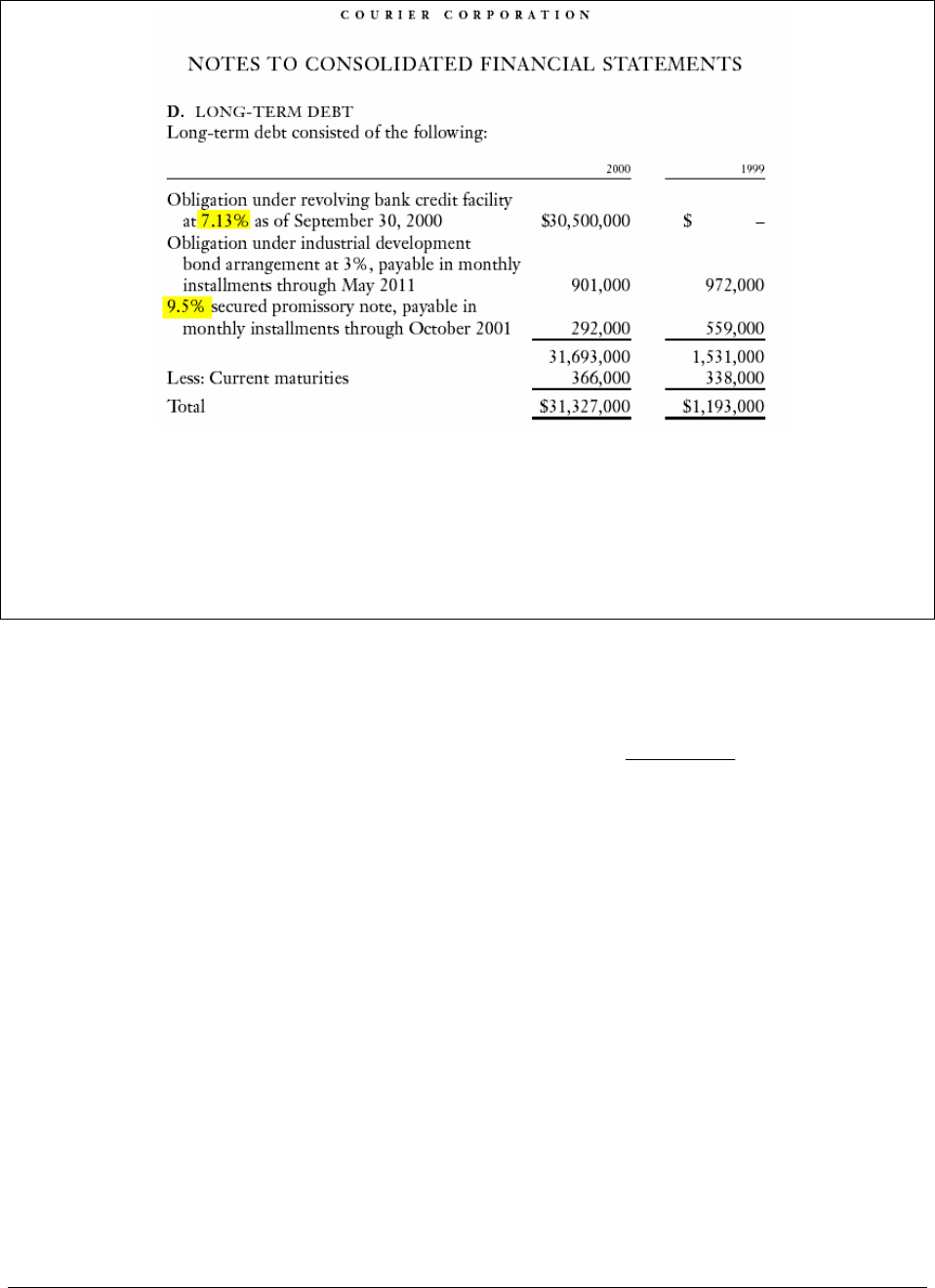

•

r

D

, the cost of Courier’s borrowing. In theory r

D

ought to be the marginal cost of debt—

the borrowing rate of the company for additional debt. However, this rate is usually

difficult to derive. A plausible alternative is use information about the current borrowing

rate of the company. In Figure 6.2 you can see what the company reports about its long

term debt. You can see that the debt has been borrowed at various interest rates. We use

the borrowing rate of 7.13% (the rate applicable to most of the debt) as the company’s

cost of debt r

D

.

PFE, Chapter 6, Weighted average cost of capital page 20

Figure 6.2: Courier’s borrowing terms, as set out in the notes to its financial statements. As

you can see, most of the company’s borrowing is at the rate of 7.13%. We use this rate as the

firm’s cost of debt r

D

.

•

T

C

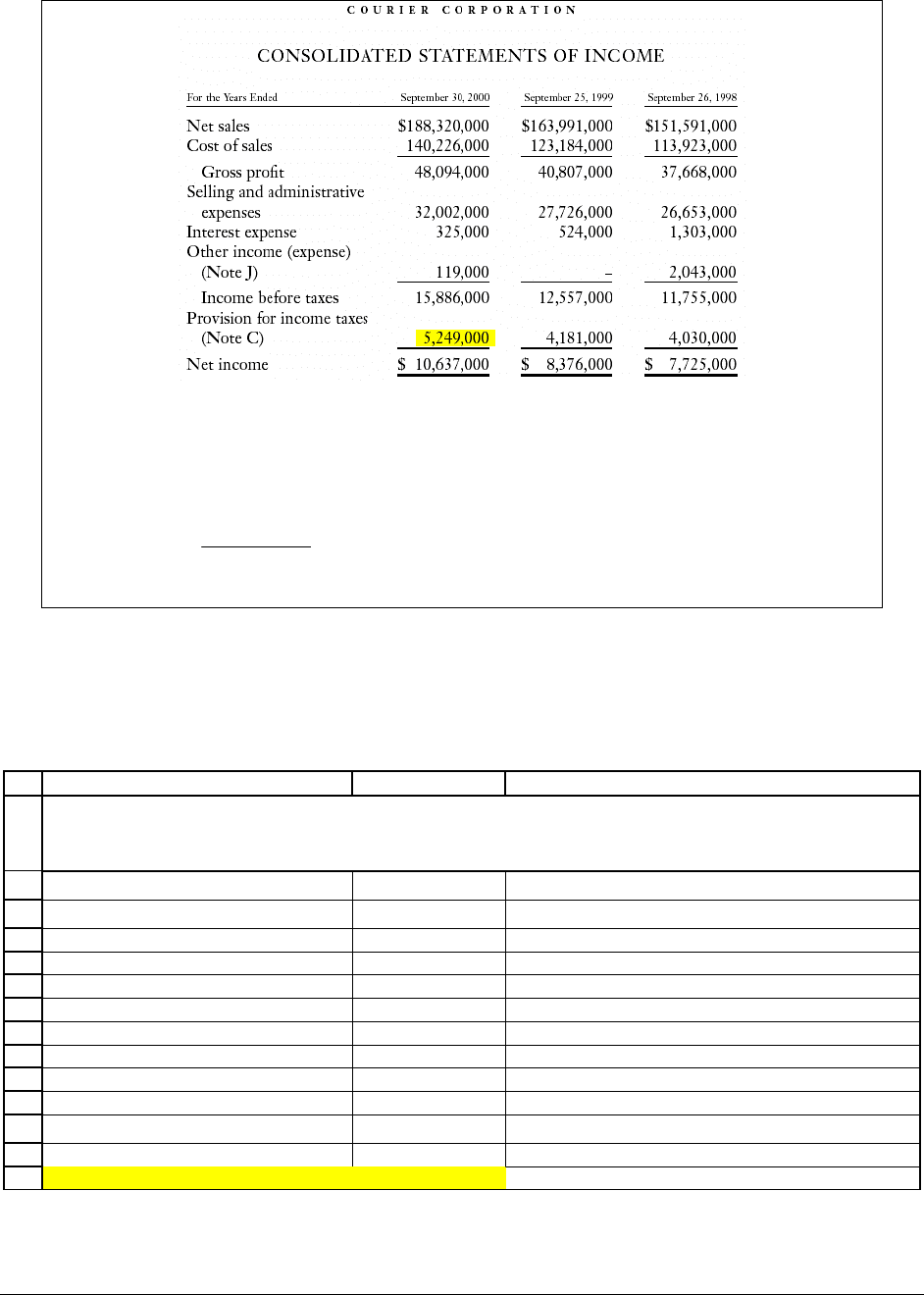

, Courier’s tax rate. We can calculate Courier’s tax rate from its provision for income

taxes. Courier’s provision for income taxes in 2000 was

5,249,000

33.04%

15,886,000

= . We use

this as an estimate for the firm’s tax rate T

C

.

PFE, Chapter 6, Weighted average cost of capital page 21

Figure 6.3: Courier’s income statements show the taxes paid. By dividing the

company’s year 2000 taxes by its income before taxes, we arrive at a tax rate of

5,249,000

33.04%

15,886,000

C

T == .

So what’s Courier’s WACC?

Here’s our calculation for Courier’s WACC:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

AB C

Cost of equity, r

E

19.36% <-- Computed from total equity payouts

Cost of debt, r

D

7.13% <-- From Courier Corp. financial statements

Sept. 2000 equity value, E 63,637,080 <-- Number of shares times current share price

Sept. 2000 debt value, D 31,693,000 <-- From Courier Corp. financial statements

Total: Equity + Debt, E+D 95,330,080 <-- =SUM(B5:B6)

Percentage of equity, E/(E+D) 67% <-- =B5/B7

Percentage of debt, D/(E+D) 33% <-- =B6/B7

Tax rate, T

C

33.04% <-- From Courier Corp. financial statements

WACC 14.51% <-- =B2*B9+B3*(1-B12)*B10

COURIER CORPORATION (CRRC)

Calculating the WACC, Sept. 2000

PFE, Chapter 6, Weighted average cost of capital page 22

In the next section we’ll use the WACC of 14.51% for Courier to calculate the value of

its equity.

6.5. Two uses of the WACC

The weighted average cost of capital (WACC) is the weighted average rate of return

required by a company’s shareholders and debtholder. We presume that this rate of return

reflects the average risk of shareholder and debtholder future cash flows. This is plausible, since

we have derived the cost of equity r

E

from anticipated future payouts to shareholders, and we

have derived the cost of debt r

D

from the rate demanded on the firm’s debts by its lenders. Thus

the WACC represents a weighted average of the riskiness of shareholder and debtholder cash

flows.

When the riskiness of a stream of cash flows is similar to the riskiness of the cash flows

received by shareholders and debtholders, the WACC is the appropriate risk-adjusted discount

rate. There are two important cases where this is often true:

•

In capital budgeting situations. When a company is considering investing in a project

whose risk is comparable to the riskiness of the company as a whole, the WACC is an

appropriate discount rate for the project’s cash flows.

•

To value the company as a whole. Below we define the concept of free cash flow (FCF).

The value of the Courier is the discounted value of its future anticipated FCFs, where the

WACC is the discount rate.

In this section we illustrate both these uses of the WACC for Courier.

PFE, Chapter 6, Weighted average cost of capital page 23

Using the WACC as a discount rate for projects

The WACC of Courier Corporation is 14.51%—this is the weighted average return

demanded by the firm’s shareholders and bondholders. Recall that Courier is in the book

printing business. Suppose the company is thinking of investing in a project whose riskiness is

like the riskiness of its current business. This could be something as simple as another printing

press to print more books or a warehouse to house them, but it could also be something much

more complicated—like the acquisition of another printing company.

In all of these cases, the WACC is the natural starting point as a discount rate. What we

mean by “starting point” is that—in discounting the cash flows of the project—Courier should

assume that initial discount rate is 14.51% and then “tweak” the discount rate a bit to adjust for

perceived risks.

Let’s say that the company is considering buying a machine that will allow them to print

more books. The cash flows, NPV, and IRR of the machine are given below. If the riskiness of

the machine’s cash flows is similar to the riskiness of Courier’s overall cash flows, then the

WACC is a reasonable discount rate. The analysis below shows that company should not

undertake the investment—the investment’s NPV is negative (-$16,460) and its IRR (7.80%) is

less than the WACC of 14.51%:

PFE, Chapter 6, Weighted average cost of capital page 24

1

2

3

4

5

6

7

8

9

10

11

12

13

AB C

WACC 14.51%

Year Cash flow

0 -100,000

1 15,000

2 22,000

3 33,000

4 44,000

5 12,000

NPV -16,460 <-- =NPV(B2,B6:B10)+B5

IRR 7.80% <-- =IRR(B5:B10)

COURIER CORPORATION (CRRC)

Using the WACC as a discount rate

Of course there’s always room for “tweaking,” since some of the assumptions we made

may not be as accurate as we thought. Suppose, for example, that the machine’s cash flows are

perceived to be much less risky than the overall cash flows of Courier. As an extreme case we

might consider the case where the machine cash flows are only as risky as Courier’s debt. Since

the company’s after-tax cost of debt is 7.13%*(1-33.04%) = 4.77%, this would then be an

appropriate discount rate for the project and the company should accept it (since the IRR of

7.80% is higher than 4.77%).

Valuing Courier Corporation using its WACC and predicted free cash flows (FCFs)

In the previous subsection we used the weighted average cost of capital (WACC) to value

a typical project of the firm. The second major use of the WACC is to value companies. A

complete explanation of this use of the WACC will have to wait until Chapter 9, where we

explain the concept of free cash flow (FCF) in detail. For our purposes in this chapter, the

free

cash flow (FCF) is the amount of cash generated by the company’s business activities, by its

operations as opposed to its financing activities. The FCF is “free” in the sense that it can be

PFE, Chapter 6, Weighted average cost of capital page 25

used to provide cash to the firm’s shareholders and debtholders in the form of dividends and

share repurchases (payments to shareholders) and interest payments (to debtholders).

To accurately define the FCF, you need some knowledge of accounting. If the following

table gives you problems, you should read the accounting refresher in Chapter 7.

Here’s the definition of the FCF:

PFE, Chapter 6, Weighted average cost of capital page 26

Defining the Free Cash Flow (FCF)

Profit after taxes This is the basic measure of the profitability of the

business, but it is an accounting measure that includes

financing flows (such as interest), as well as non-cash

expenses such as depreciation. Profit after taxes does not

account for either changes in the firm’s working capital or

purchases of new fixed assets, both of which can be

important cash drains on the firm. The FCF definition

takes changes in working capital and purchases of new

fixed assets into account separately.

+ Depreciation This non-cash expense is added back to the profit after tax.

The sum of the next two items is the change in net working capital, often denoted by

∆NWC

- Increase in current assets related

to the firm’s operations.

When the firm’s sales increase, more investment is needed

in inventories, accounts receivable, etc. This increase in

current assets is not an expense for tax purposes (and is

therefore ignored in the profit after taxes), but it is a cash

drain on the company. For purposes of calculating the

FCF, the increase in current assets does not include

changes in cash and marketable securities.

+ Increase in current liabilities

related to the firm’s operations

An increase in the sales often causes an increase in

financing related to sales (such as accounts payable or taxes

payable). This increase in current liabilities—when related

to sales—provides cash to the firm. The FCF includes all

current liability items related to operations; it does not

include financial items such as short-term borrowing, the

current portion of long-term debt, and dividends payable.

- Capital expenditures (CAPEX) An increase in fixed assets (the long-term productive assets

of the company) is a use of cash, which reduces the firm’s

free cash flow.

+ after-tax interest payments (net) FCF measures the cash produced by the business activity of

the firm. The FCF should not include any items related to

the firm’s financing. In particular we need to neutralize the

effect of interest payments which appear in the firm’s profit

after taxes. We do this by:

•

Adding back the after-tax cost of interest on debt

(after-tax since interest payments are tax-

deductible),

•

Subtracting out the after-tax interest payments on

cash and marketable securities.

FCF = sum of the above

In 2000 Courier Corporation had a free cash flow (FCF) of $6,381,240: