Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE, Chapter 3: Capital budgeting 35

Using this example, you can see the role taxes play even if we sell the machine at a loss.

Suppose, for example, that the machine is sold in year 7 for $50, which is less than the book

value:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

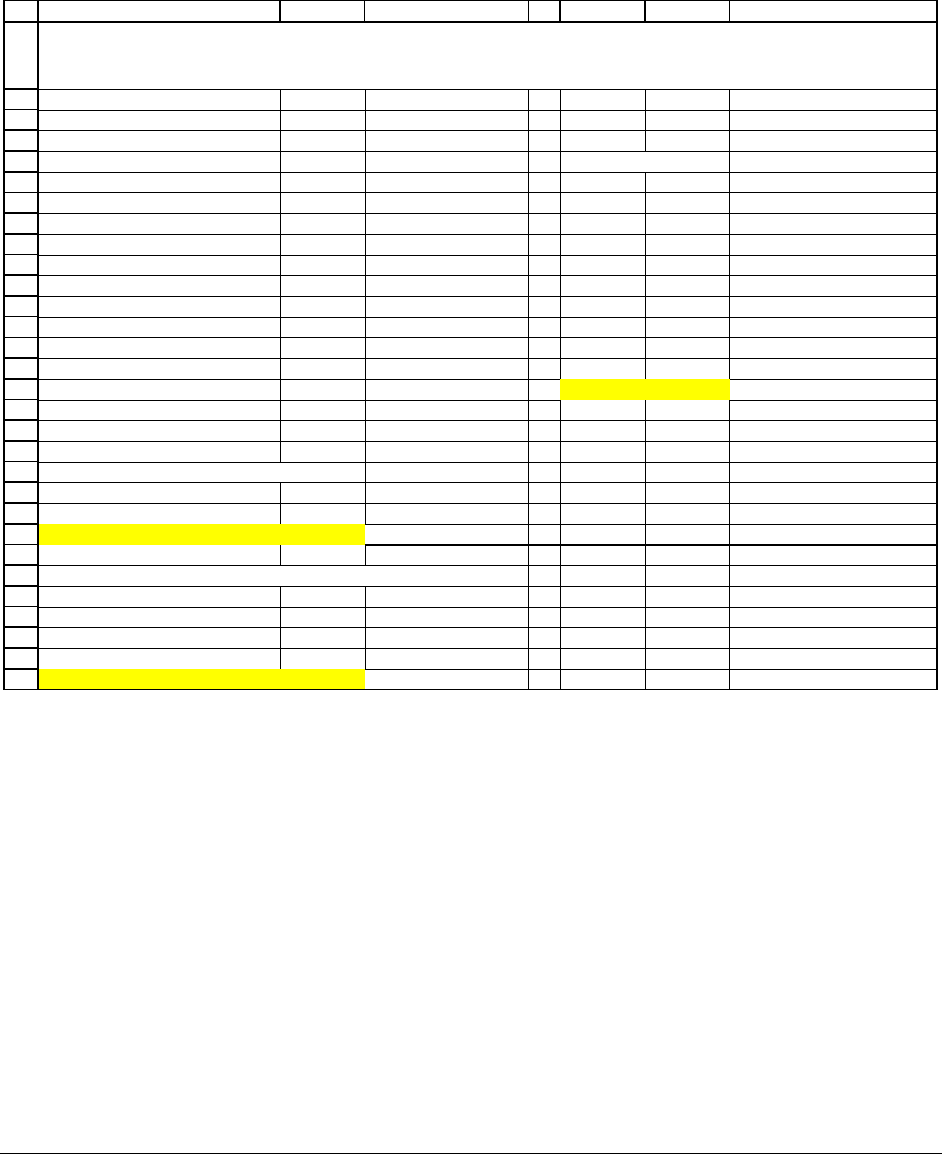

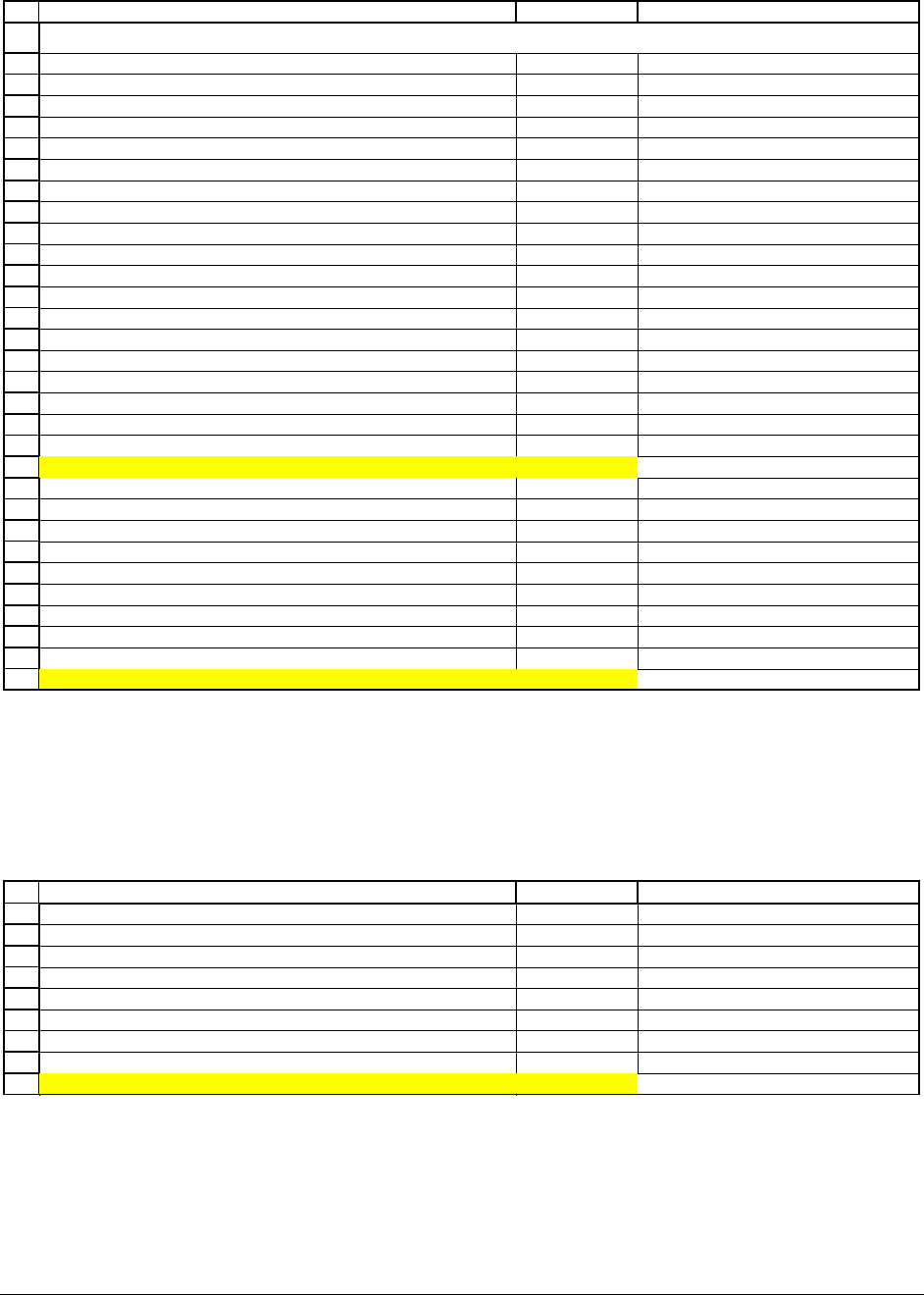

ABCDEFG

Cost of the machine 800

Annual anticipated sales 1,000

Annual COGS 400

Annual SG&A 300

NPV Analysis

Annual depreciation 100 Year Cash flow

0 -800 <-- =-B2

Tax rate 40% 1 220 <-- =$B$23

Discount rate 15% 2 220

3 220

Annual profit and loss (P&L)

4 220

Sales 1,000 5 220

Minus COGS -400 6 220

Minus SG&A -300 7 290 <-- =$B$23+B30

Minus depreciation -100

Profit before taxes 200 <-- =SUM(B12:B15) NPV 142 <-- =F7+NPV(B9,F8:F15)

Subtract taxes -80 <-- =-B8*B16

Profit after taxes 120 <-- =B16+B17

Calculating the annual cash flow

Profit after taxes 120

Add back depreciation 100

Cash flow 220

Calculating the cash flow from salvage value

Machine market value, year 7 50

Book value, year 7 100

Taxable gain -50 <-- =B26-B27

Taxes paid on gain -20 <-- =B8*B28

Cash flow from salvage value 70 <-- =B26-B29

BUYING A MACHINE--NPV ANALYSIS

with salvage value. Machine sold in year 7

In this case, the negative taxable gain (cell B28, the jargon often heard is “loss over

book”) produces a tax shield—the negative taxes of -$20 in cell B29. This tax shield is added to

the market value to produce a salvage value cash flow of $70 (cell B30). Thus even selling an

asset at a loss can produce a positive cash flow.

PFE, Chapter 3: Capital budgeting 36

3.9. Capital budgeting principle: Don’t forget the cost of foregone

opportunities

This is another important principle of capital budgeting. An example: You’ve been

offered the project below, which involves buying a widget-making machine for $300 to make a

new product. The cash flows in years 1-5 have been calculated by your financial analysts:

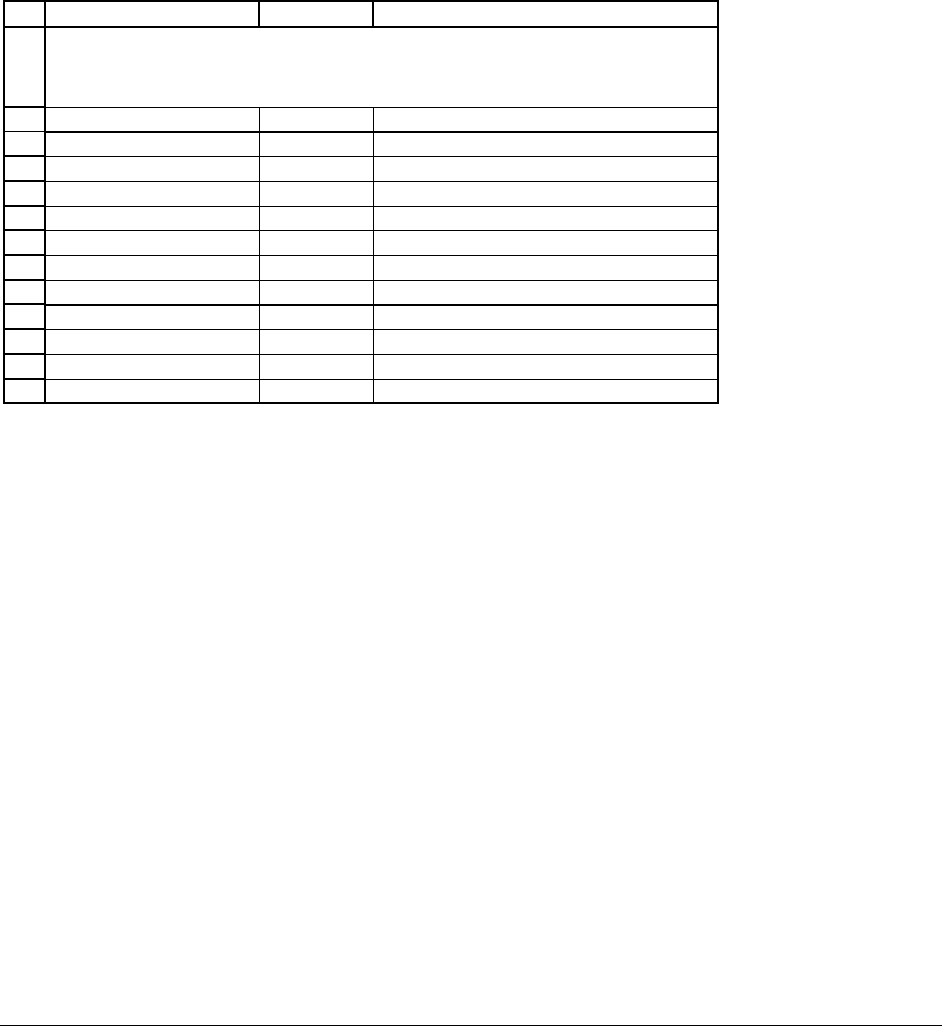

1

2

3

4

5

6

7

8

9

10

11

12

13

AB C

Discount rate 12%

Year Cashflow

0 -300

1 185

2 249

3 155

4 135

5 420

NPV 498.12 <-- =NPV(B2,B6:B10)+B5

IRR 62.67% <-- =IRR(B5:B10)

DON'T FORGET THE COST OF

FOREGONE OPPORTUNITIES

Looks like a fine project! But now someone remembers that the widget process makes

use of some already existing but underused equipment. Should the value of this equipment be

somehow taken into account?

The answer to this question has to do with whether the equipment has an alternative use.

For example, suppose that, if you don’t buy the widget machine, you can sell the equipment for

$200. Then the true year 0 cost for the project is $500, and the project has a lower NPV:

PFE, Chapter 3: Capital budgeting 37

16

17

18

19

20

21

22

23

24

25

26

27

AB C

Discount rate 12%

Year Cashflow

0 -500

The $300 direct cost + $200

<-- value of the existing machines

1 185

2 249

3 155

4 135

5 420

NPV 298.12

IRR 31.97%

While the logic here is clear, the implementation can be murky: What if the machine is

to occupy space in a building that is currently unused? Should the cost of this space be taken

into account? It all depends on whether there are alternative uses, now or in the future.

7

3.10. In-house copying or outsourcing? A mini-case illustrating foregone

opportunity costs

Your company is trying to decide whether to outsource its photocopying or continue to

do it in-house. The current photocopier won’t do anymore—it either has to be sold or

thoroughly fixed up. Here are some details about the two alternatives:

•

The company’s tax rate is 40%.

•

Doing the copying in-house requires an investment of $17,000 to fix up the existing

photocopy machine. Your accountant estimates that this $17,000 can be immediately

booked as an expense, so that its after-tax cost is

(

)

1 40% *17,000 10, 200−=. Given this

7

There’s a fine Harvard case on this topic: “The Super Project,” Harvard Business School case 9-112-034.

PFE, Chapter 3: Capital budgeting 38

investment the copier will be good for another five years. Annual copying costs are

estimated to be $25,000 on a before-tax basis; after-tax this is

()

1 40% *25,000 15,000−=.

•

The photocopy machine is on your books for $15,000, but its market value is in fact

much less—it could only be sold today for $5,000. This means that the sale of the copier

will generate a loss for tax purposes of $10,000; at your tax rate of 40%, this loss gives a

tax shield of $4,000. Thus the sale of the copier will generate a cash flow of $9,000.

•

If you decide to keep doing the photocopying in-house, the remaining book value of the

copier will be depreciated over 5 years at $3,000 per year. Since your tax rate is 40%,

this will produce a tax shield of 40%*$3,000 = $1,200 per year.

•

Outsourcing the copying will be $33,000 per year—$8,000 more expensive than doing it

in-house on the rehabilitated copier. Of course this $33,000 is an expense for tax

purposes, so that the net savings from doing the copying in-house is

()

(

)

1 * cos 1 40% *$33,000 $19,800taxrate outsourcing ts−=−=.

•

The relevant discount rate is 12%.

We will show you two ways to analyze this decision. The first method values each of the

alternatives separately. The second method looks only at the differential cash flows. We

recommend the first method—it’s simpler and leads to fewer mistakes. The second method

produces a somewhat “cleaner” set of cash flows that take explicit account of foregone

opportunity costs.

PFE, Chapter 3: Capital budgeting 39

Method 1: Write down the cash flows of each alternative

This is often the simplest way to do things; if you do it correctly, this method takes care

of all the foregone opportunity costs without your thinking about them. Below we write down

the cash flows for each alternative:

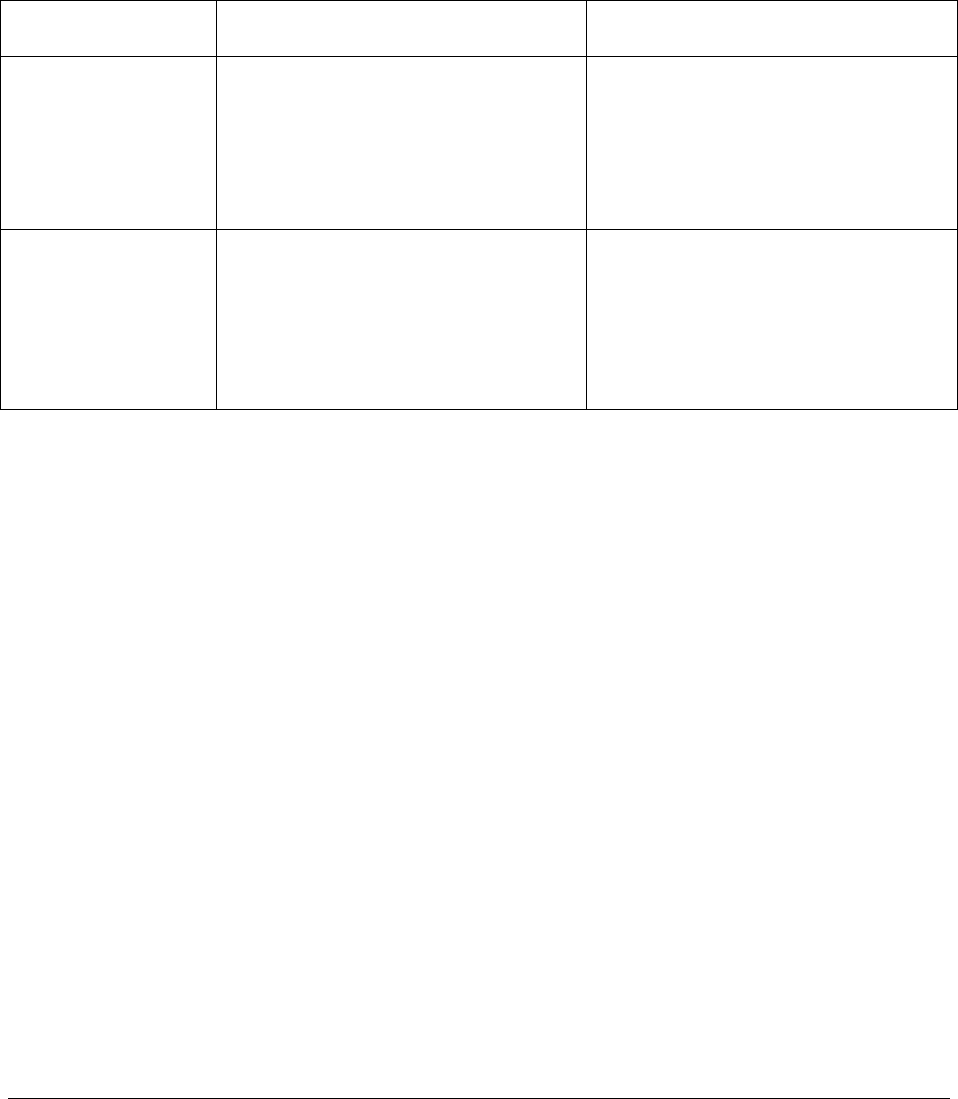

In house Outsourcing

Year 0

()

()

1*

1 40% *17,000 $10,200

taxrate machine rehab cost−−

=− − =−

()

*

$5, 000 40% * $15,000 5, 000

$9,000

Sale price of machine

tax rate loss over book value+

=+ −

=

Years 1-5

annual cash flow

()

()

-

1 40% *$25,000

40%*$3,000 $13,800

1-taxrate *in house costs

+tax rate* depreciation

−

=− −

+=−

(

)

()

1

1 40% *$33, 000

$19,800

tax rate * outsourcing costs−−

=− − =

=−

Putting these data in a spreadsheet and discounting at the discount rate of 12% shows that

it is cheaper to do the in-house copying. The NPV of the in-house cash flows is -$59,946,

whereas the NPV of the outsourcing cash flows is -$62,375. Note that both NPVs are negative;

but the in-house alternative is less negative (meaning: more positive) than the outsourcing

alternative; therefore the in-house is preferred:

PFE, Chapter 3: Capital budgeting 40

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

ABC

Annual cost savings (before tax) after fixing up the machine 8,000

Book value of machine 15,000

Market value of machine 5,000

Rehab cost of machine 17,000

Tax rate 40%

Annual depreciation if machine is retained 3,000

Annual copying costs

In-house 25,000

Outsourcing 33,000

Discount rate 12%

Alternative 1: Fix up machine and do copying in-house

Year Cash flow

0 -10,200 <-- =-B5*(1-B6)

1 -13,800 <-- =-$B$9*(1-$B$6)+$B$6*$B$7

2 -13,800

3 -13,800

4 -13,800

5 -13,800

NPV of fixing up machine and in-house copying -59,946 <-- =B15+NPV(B11,B16:B20)

Alternative 2: Sell machine and outsource copying

Year Cash flow

0 9,000 <-- =B4+B6*(B3-B4)

1 -19,800 <-- =-(1-$B$6)*$B$10

2 -19,800

3 -19,800

4 -19,800

5 -19,800

NPV of selling machine and outsourcing -62,375 <-- =B25+NPV(B11,B26:B30)

SELL THE PHOTOCOPIER OR FIX IT UP?

Method 2: Discounting the differential cash flows

In this method we subtract the cash flows of Alternative 2 from those of Alternative 1:

34

35

36

37

38

39

40

41

42

ABC

Subtract Alternative 2 CFs from Alternative 1 CFs

Year Cash flow

0 -19,200 <-- =B15-B25

1 6,000 <-- =B16-B26

26,000

36,000

46,000

56,000

NPV(Alternative 1 - Alternative 2) 2,429 <-- =B36+NPV(B11,B37:B41)

The NPV of the differential cash flows is positive. This means that Alternative 1 (in-

house) is better than Alternative 2 (outsourcing):

PFE, Chapter 3: Capital budgeting 41

()

(

)

()

--()0

This means that

-()

NPV In house Outsourcing NPV In house NPV Outsourcing

NPV In house NPV Outsourcing

−= − >

>

If you look carefully at the differential cash flows, you’ll see that they take into account

the cost of the foregone opportunities:

Differential

cash flow

Explanation

Year 0 -$19,200 This is the after-tax cost of rehabilitating the old copier plus the

foregone opportunity cost of selling the copier. In other words:

This is the cost in year 0 of deciding to do the copying in-house.

Years 1-5 $6,000 This is the after-tax saving of doing the copying in-house: If you

do it in house, you save $8,000 pre-tax (= $4,800 after tax) and

you get to take depreciation on the existing copier (= tax shield of

$1,200). Relative to in-house copying, the outsourcing alternative

has a foregone opportunity cost of the loss of the depreciation tax

shield.

If you examine the convoluted prose in the table above (“the outsourcing alternative has a

foregone opportunity cost of the loss of the depreciation tax shield”) you’ll agree that it may just

be simpler to list each alternative’s cash flows separately.

PFE, Chapter 3: Capital budgeting 42

3.11. Accelerated depreciation

As you know by now, the salvage value for an asset is its value at the end of its life;

another term sometimes used is terminal value. Here’s a capital budgeting example that

illustrates the importance of accelerated depreciation in computing the cash:

•

Your company is considering buying a machine for $10,000.

•

If bought, the machine will produce annual cost savings of $3,000 for the next 5 years;

these cash flows will be taxed at the company’s tax rate of 40%.

•

The machine will be depreciated over the 5 year period using the accelerated depreciation

percentages allowable in the United States.

8

At the end of the 6

th

year, the machine will

sold; your estimate of its salvage value at this point is $4,000, even though for accounting

purposes its book value is $500.

You have to decide what the NPV of the project is, using a discount rate of 12%. Here

are the relevant calculations:

8

These accelerated depreciation percentages—termed ACRS (for “accelerated cost recovery system”) are discussed

briefly in Section 3.7.

PFE, Chapter 3: Capital budgeting 43

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

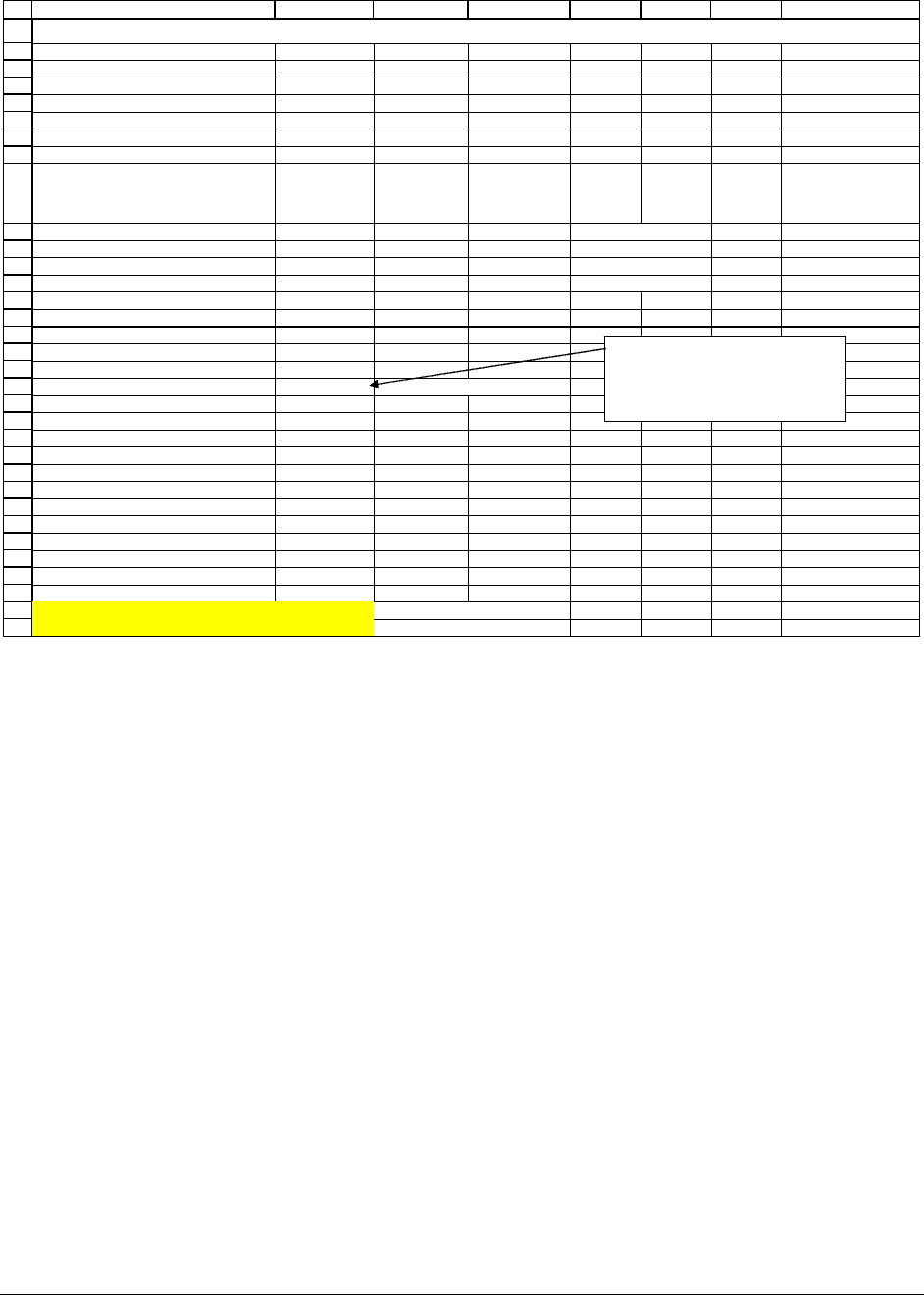

ABCDEFGH

Machine cost 10,000

Annual materials savings, before tax 3,000

Salvage value, end of year 5 12,000

Tax rate 40%

Discount rate 12%

Depreciation schedule (ACRS)

Year

ACRS

depreciation

percentage

Actual

depreciation

Depreciation

tax shield

1 20.00% 2,000 800 <-- =$B$5*C10

2 32.00% 3,200 1,280 <-- =$B$5*C11

3 19.20% 1,920 768 <-- =$B$5*C12

4 11.52% 1,152 461 <-- =$B$5*C13

5 11.52% 1,152 461

6 5.76% 576 230

Terminal value

Year 5 sale price, estimated 12,000 <-- =B4

Year 5 book value 576 <-- =B2-SUM(C10:C14)

Taxable gain 11,424 <-- =B18-B19

Taxes 4,570 <-- =B5*B20

Net 7,430 <-- =B18-B21

Y

ear 0 1 2 345

Purchase price -10,000

After-tax cost savings 1,800 1,800 1,800 1,800 1,800 <-- =$B$3*(1-$B$5)

Depreciation tax shield 800 1,280 768 461 461 <-- =D14

Terminal value 7,430 <-- =B22

Total cashflow -10,000 2,600 3,080 2,568 2,261 9,691 <-- =SUM(G26:G29)

Net present value 3,540.46 <-- =NPV(B6,C30:G30)+B30

IRR 22.84% <-- =IRR(B30:G30)

CAPITAL BUDGETING WITH ACCELERATED DEPRECIATION

The book value at the end of year 5 is

the initial cost of the machine

($10,000)

minus

the sum of all

the depreciation taken on the

machine through year 5 ($9,424).

3.12. Conclusion

In this chapter we’ve discussed the basics of capital budgeting using NPV and IRR.

Capital budgeting decisions can be crudely separated into “yes-no” decisions (“should we

undertake a given project?”) and into “ranking” decisions (“which of the following list of

projects do we prefer?”). We’ve concentrated on two important areas of capital budgeting:

•

The difference between NPV and IRR in making the capital budgeting decision. In many

cases these two criteria give the same answer to the capital budgeting question.

However, there are cases—especially when we rank projects—where NPV and IRR give

PFE, Chapter 3: Capital budgeting 44

different answers. Where they differ, NPV is the preferable criterion to use because the

NPV is the additional wealth derived from a project.

•

Every capital budgeting decision ultimately involves a set of anticipated cash flows, so

when you do capital budgeting, it’s important to get these cash flows right. We’ve

illustrated the importance of sunk costs, taxes, foregone opportunities, and salvage values

in determining the cash flows.