Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE, Chapter 3: Capital budgeting 15

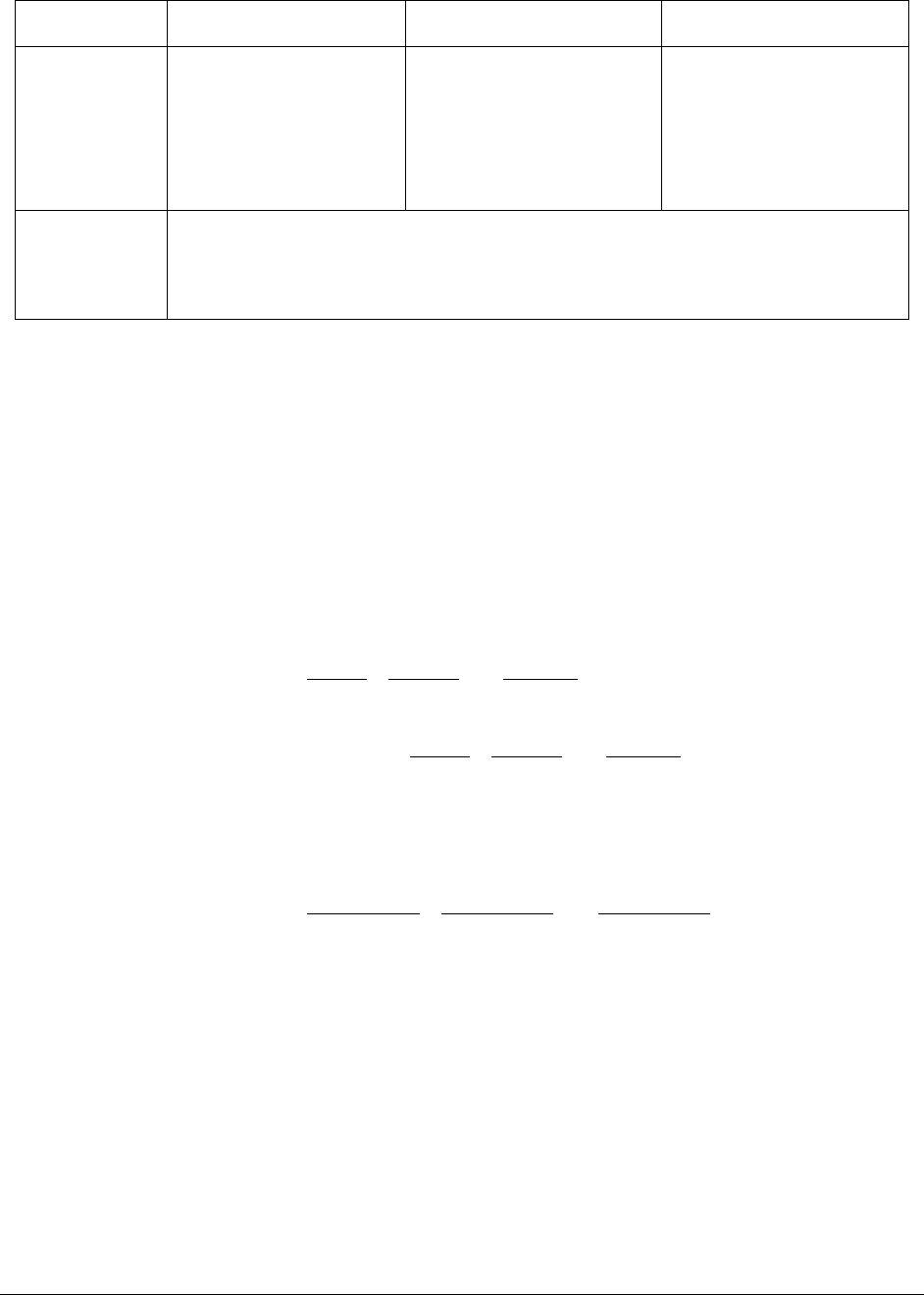

Discount rate < 8.51% Discount rate = 8.51% Discount rate > 8.51%

NPV criterion

A preferred:

NPV(A) > NPV(B)

Indifferent between A

and B:

NPV(A) = NPV(B)

B preferred:

NPV(B) > NPV(A)

IRR criterion

B always preferred to A, since

IRR(B) > IRR(A)

Calculating the crossover point

The crossover point—which we claimed above was 8.51% — is the discount rate at

which the NPV of the two projects is equal. A bit of formula manipulation will show you that

the crossover point is the IRR of the differential cash flows. To see this, suppose that for some

rate r, NPV(A) = NPV(B):

()

()

() ()

()

() ()

()

12

0

2

12

0

2

1

11

1

11

A

AA

A

N

N

B

BB

B

N

N

CF

CF CF

NPV A CF

r

rr

CF

CF CF

CF NPV B

r

rr

=+ + +

+

++

=+ + + =

+

++

…

…

Subtracting and rearranging shows that r must be the IRR of the differential cash flows:

()

() ()

11 22

00

2

0

1

11

AB

AB AB

AB

NN

N

CF CF

CF CF CF CF

CF CF

r

rr

−

−−

−+ + + =

+

++

…

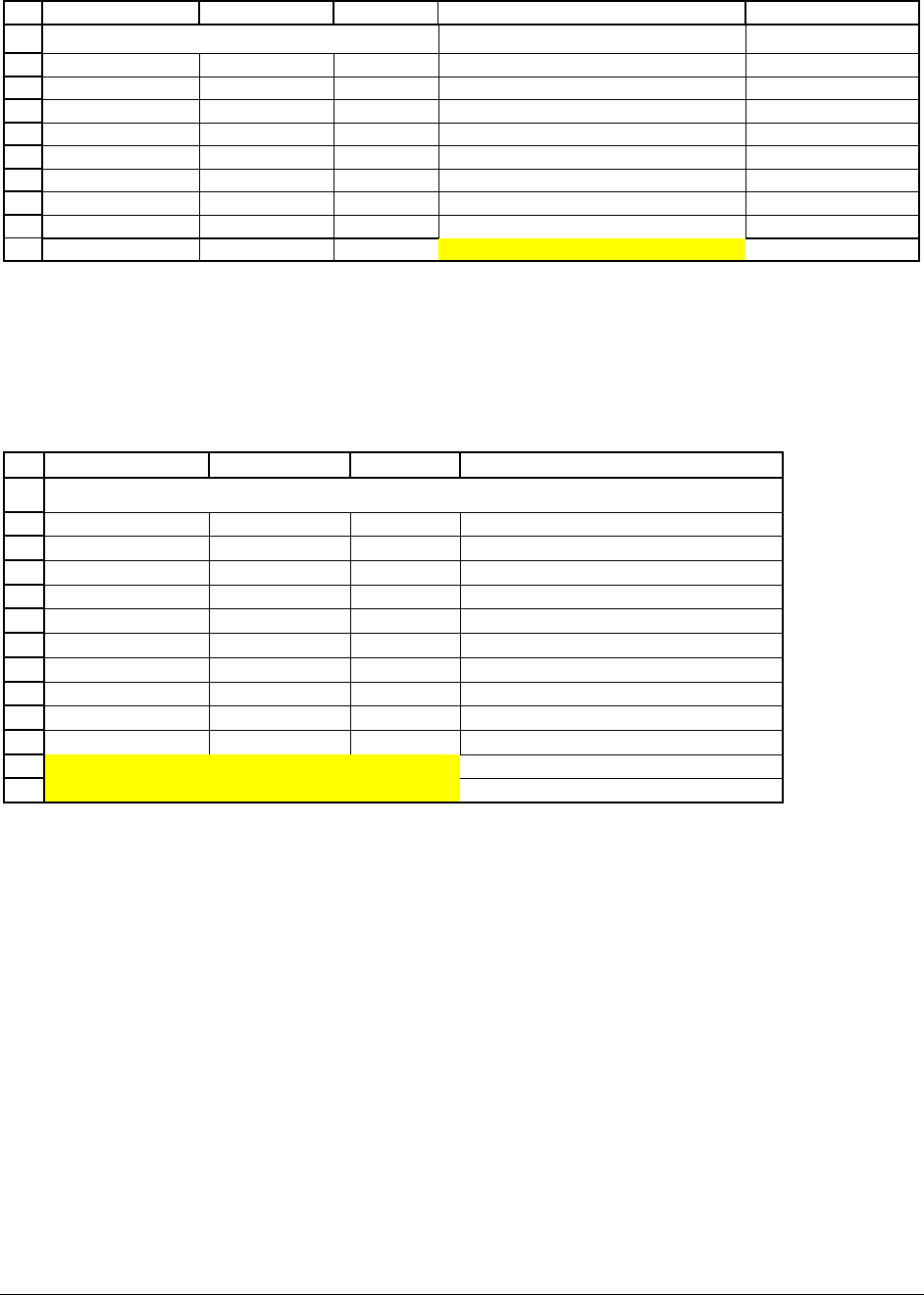

We can use Excel to calculate this crossover point. To do this, we first set up the

differential cash flows (you can see them in column D below):

PFE, Chapter 3: Capital budgeting 16

34

35

36

37

38

39

40

41

42

43

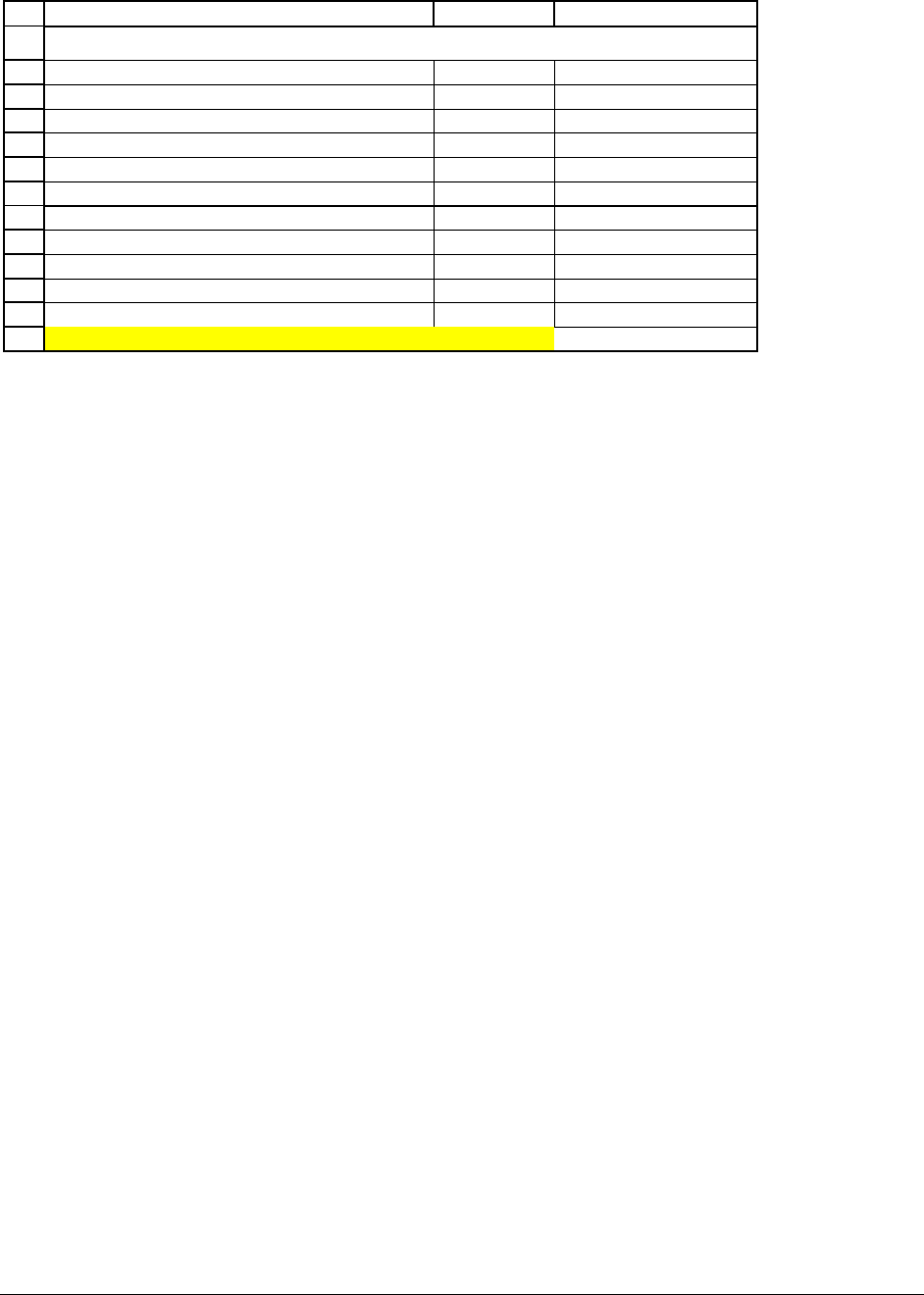

ABC D E

Calculating the crossover point

Year Project

A

Project B

Cashflow(A) - cashflow(B)

0 -500 -500 0 <-- =B36-C36

1 100 250 -150 <-- =B37-C37

2 100 250 -150

3 150 200 -50

4 200 100 100

5 400 50 350

IRR 8.51% <-- =IRR(D36:D41)

What to use? NPV or IRR?

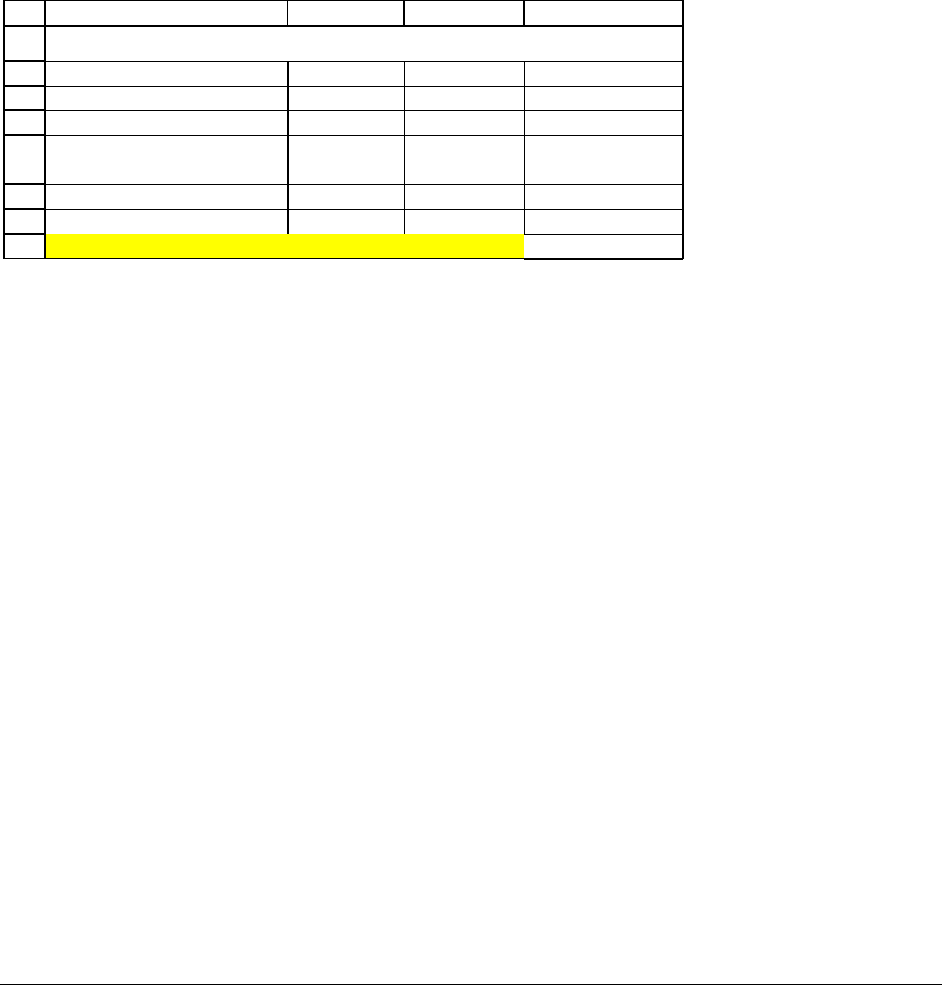

Let’s go back to the initial example and suppose that the discount rate is 8%:

1

2

3

4

5

6

7

8

9

10

11

12

13

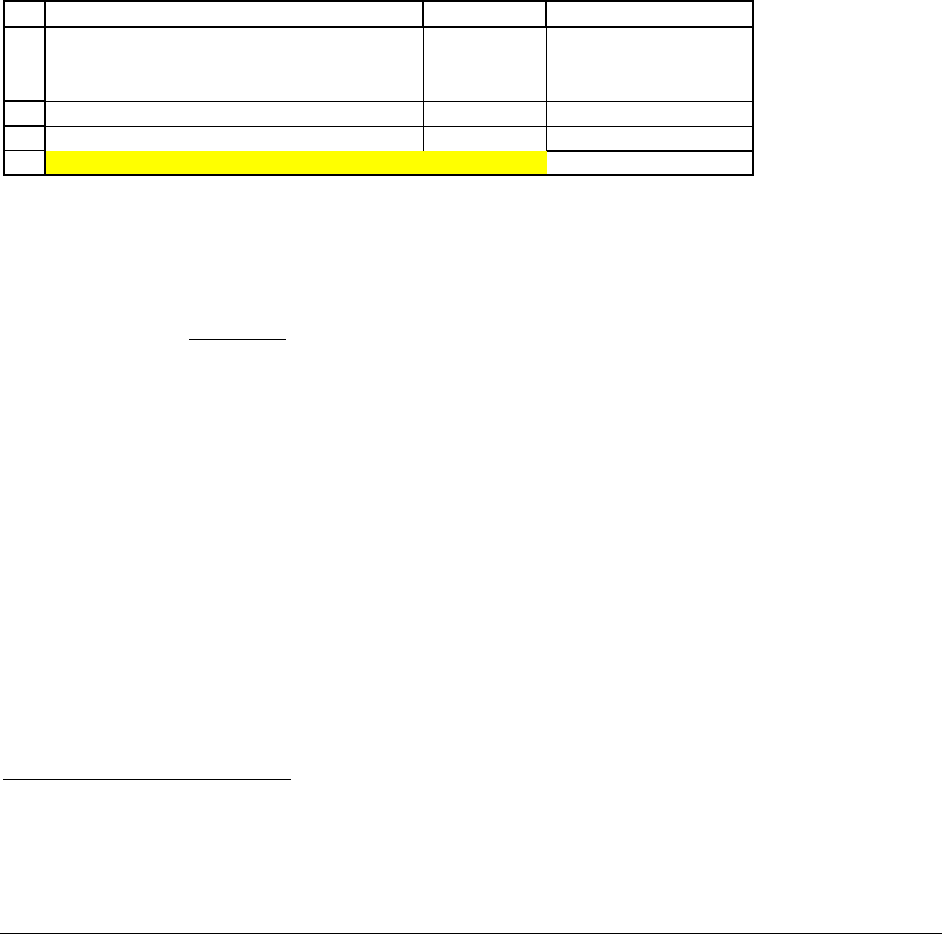

ABC D

Discount rate 8%

Year Project

A

Project B

0 -500 -500

1 100 250

2 100 250

3 150 200

4 200 100

5 400 50

NPV 216.64 212.11 <-- =C5+NPV(B2,C6:C10)

IRR 19.77% 27.38% <-- =IRR(C5:C10)

RANKING PROJECTS WITH NPV AND IRR

In this case we know there is disagreement between the NPV (which would lead us to

choose Project A) and the IRR (by which we choose Project B). Which is correct?

The answer to this question is that we should—for the case where the discount rate is

8%—choose using the NPV (that is, choose Project A). This is just one example of the general

principal discussed in Section 3 that using the NPV is always preferred, since the NPV is the

additional wealth that you get, whereas IRR is the compound rate of return. The economic

assumption is that consumers maximize their wealth, not their rate of return.

PFE, Chapter 3: Capital budgeting 17

Where is this chapter going?

Until this point in the chapter, we’ve discussed general principles of project choice using

the NPV and IRR criteria. The following sections discuss some specifics:

● Ignoring sunk costs and using marginal cash flows (Section 3.6)

● Incorporating taxes and tax shields into capital budgeting calculations (Section 3.7)

● Incorporating the cost of foregone opportunities (Section 3.9)

● Incorporating salvage values and terminal values (Section 3.11)

3.6. Capital budgeting principle: Ignore sunk costs and consider only

marginal cash flows

This is an important principle of capital budgeting and project evaluation: Ignore the

cash flows you can’t control and look only at the marginal cash flows—the outcomes of

financial decisions you can still make. In the jargon of finance: Ignore sunk costs, costs that

have already been incurred and are thus not affected by future capital budgeting decisions.

Here’s an example: You recently bought a plot of land and built a house on it. Your

intention was to sell the house immediately, but it turns out you did a horrible job. The house

and land cost you $100,000, but in its current state the house can’t be sold. A friendly local

contractor has offered to make the necessary repairs, but these will cost $20,000; your real estate

broker estimates that even with these repairs you’ll never sell the house for more than $90,000.

What should you do?

PFE, Chapter 3: Capital budgeting 18

• “My father always said ‘Don’t throw good money after bad.’” If this is your approach,

you won’t do anything. This attitude is typified in column B below, which shows that—

if you make the repairs you will lose 25% on your money.

• “My mother was a finance prof, and she said “Don’t cry over spilt milk. Look only at the

marginal cash flows” These turn out to be pretty good. In column C below you see that

making the repairs will give you a 350% return on your $20,000.

1

2

3

4

5

6

7

8

ABCD

House cost 100,000

Fix up cost 20,000

Year

Cash flow

wrong!

Cash flow

right!

0 -120,000 -20,000

1 90,000 90,000

IRR -25% 350% <-- =IRR(C6:C7)

IGNORE SUNK COSTS

Of course your father was wrong and your mother right (this often happens): Even

though you made some disastrous mistakes (you never should have built the house in the first

place), you should—at this point—ignore the sunk cost of $100,000 and make the necessary

repairs.

3.7. Capital budgeting principle: Don’t forget the effects of taxes—Sally and

Dave’s condo investment

In this section we discuss the capital budgeting problem faced by Sally and Dave, two

business-school grads who are considering buying a condominium apartment and renting it out

for the income.

PFE, Chapter 3: Capital budgeting 19

We use Sally and Dave and their condo to emphasize the place of taxes in the capital

budgeting process. No one needs to be told that taxes are very important.

2

In the capital

budgeting process, the cash flows that are to be discounted are after-tax cash flows. We

postpone a fuller discussion of this topic to Chapters 6 and 7, where we define the concept of

free cash flow. For the moment we concentrate on a few obvious principles, which we illustrate

with the example of Sally and Dave’s condo investment.

Sally and Dave—fresh out of business school with a little cash to spare—are considering

buying a nifty condo as a rental property. The condo will cost $100,000, and (in this example at

least) they’re planning to buy it with all cash. Here are some additional facts:

• Sally and Dave figure they can rent out the condo for $24,000 per year. They’ll have to

pay property taxes of $1,500 annually and they’re figuring on additional miscellaneous

expenses of $1,000 per year.

• All the income from the condo has to be reported on their annual tax return. Currently

Sally & Dave have a tax rate of 30%, and they think this rate will continue for the

foreseeable future.

• Their accountant has explained to them that they can depreciate the full cost of the condo

over 10 years—each year they can charge $10,000 depreciation

(

10-

condo cost

year depreciable life

= ) against the income from the condo.

3

This means that they

can expect to pay $3,450 in income taxes per year if they buy the condo and rent it out

and have net income from the condo of $8,050:

2

Will Rogers: “The difference between death and taxes is death doesn’t get worse every time Congress meets.”

3

You may want to read the sidebar on depreciation before going on.

PFE, Chapter 3: Capital budgeting 20

1

2

3

4

5

6

7

8

9

10

11

12

13

ABC

Cost of condo

100,000

Sally & Dave's tax rate

30%

Annual reportable income calculation

Rent 24,000

Expenses

Property taxes -1,500

Miscellaneous expenses -1,000

Depreciation -10,000

Reportable income 11,500 <-- =SUM(B6:B10)

Taxes (rate = 30%) -3,450 <-- =-B3*B11

Net income 8,050 <-- =B11+B12

SALLY & DAVE'S CONDO

PFE, Chapter 3: Capital budgeting 21

SIDEBAR: What is depreciation?

In computing the taxes they owe, Sally and Dave get to subtract expenses from their income. Taxes

are computed on the basis of the income before taxes (=income – expenses – depreciation – interest).

When Sally and Dave get the rent from their condo, this is income—money earned from their asset.

When Sally and Dave pay to fix the faucet in their condo, this is an expense—a cost of doing

business.

The cost of the condo is neither income nor an expense. It’s a capital investment—money paid for an

asset that will be used over many years. Tax rules specify that each year part of the capital

investments can be taken off the income (“expensed,” in the accounting jargon). This reduces the

taxes paid by the owners of the asset and takes account of the fact that the asset has a limited life.

There are many depreciation methods in use. The simplest method is straight-line depreciation. In

this method the asset’s annual depreciation is a percentage of its initial cost. In the case of Sally and

Dave, for example, we’ve specified that the asset is depreciated over 10 years. this results in annual

depreciation charges of

$100,000

- $10,000

10

initial asset cost

straight line depreciation= annually

depreciable life span

==

In some cases depreciation is taken on the asset cost minus its salvage value: If you think that the

asset will be worth $20,000 at the end of its life (this is the salvage value), then the annual straight-

line depreciation might be $8,000:

-

$100,000 $20, 000

$8, 000

10

straight line depreciation

initial asset cost salvage value

=

with salvage value

depreciable life span

annually

−

−

==

Accelerated depreciation

Although historically depreciation charges are related to the life span of the asset, in many cases this

connection has been lost. Under United States tax rules, for example, an asset classified as having a

5-year depreciable life (trucks, cars, and some computer equipment is in this category) will be

depreciated over 6 years (yes six) at 20%, 32%, 19.2%, 11.52%, 11.52%, 5.76% in each of the years

1, 2, … , 6. Notice that this method accelerates the depreciation charges—more than one-sixth of the

depreciation is taken annually in years 1-3 and less in later years. Since—as we show in the text—

depreciation ultimately saves taxes, this is in the interest of the asset’s owner, who now gets to take

more of the depreciation in the early years of the asset’s life.

PFE, Chapter 3: Capital budgeting 22

Two ways to calculate the cash flow

In the previous spreadsheet you saw that Sally and Dave’s net income was $8,050. In

this section you’ll see that the cash flow produced by the condo is much more that this amount.

It all has to do with depreciation: Because the depreciation is an expense for tax purposes but

not a cash expense, the cash flow from the condo rental is different. So even though the net

income from the condo is $8,050, the annual cash flow is $18,050—you have to add back the

depreciation to the net income to get the cash flow generated by the property.

16

17

18

19

ABC

Cash flow, method 1

Add back depreciation

Net income 8,050 <-- =B14

Add back depreciation 10,000 <-- =-B11

Cash flow 18,050 <-- =B18+B17

In the above calculation, we’ve added the depreciation back to the net income to get the

cash flow.

An asset’s cash flow

(the amount of cash produced by an asset during a particular

period) is computed by taking the asset’s net income (also called profit after taxes or

sometimes just “income”) and adding back non-cash expenses like depreciation.

4

Tax shields

There’s another way of calculating the cash flow which involves a discussion of tax

shields. A tax shield is a tax saving that results from being able to report an expense for tax

purposes. In general a tax shield just reduces the cash cost of an expense—in the above

4

In Chapter 6 we introduce the concept of free cash flow, which is an extension of the cash flow concept discussed

here.

PFE, Chapter 3: Capital budgeting 23

example, since Sally & Dave’s property taxes of $1,500 are an expense for tax purposes, the

after-tax cost of the property taxes is:

()

This $450 is the

tax shield

1 30% *$1,500 $1,500 30% *1,500 $1, 050

↑

−=−=

.

The tax shield of $450 (

30%*$1,500= ) has reduced the cost of the property taxes.

Depreciation is a special case of a non-cash expense which generates a tax shield. A little

thought will show you that the $10,000 depreciation on the condo generates $3,000 of cash.

Because depreciation reduces Sally & Dave’s reported income, each dollar of depreciation saves

them $0.30 (30 cents) of taxes, without actually costing them anything in out-of-pocket expenses

(the $0.30 comes from the fact that Sally & Dave’s tax rate is 30%). Thus $10,000 of

depreciation is worth $3,000 of cash. This $3,000 depreciation tax shield is a cash flow for Sally

and Dave.

In the spreadsheet below we calculate the cash flow in two stages:

•

We first calculate Sally and Dave’s net income ignoring depreciation (cell B29). If

depreciation were not an expense for tax purposes, Sally and Dave’s net income would

be $15,050.

•

We then add to the this figure the depreciation tax shield of $3,000. The result (cell B32)

gives the cash flow for the condo.

PFE, Chapter 3: Capital budgeting 24

21

22

23

24

25

26

27

28

29

30

31

32

33

ABCDE

Cashflow, method 2

Compute after-tax income without

depreciation, then add depreciation

tax shield

Rent 24,000

Expenses

Property taxes -1,500

Miscellaneous expenses -1,000

Depreciation 0

Reportable income 21,500 <-- =SUM(B22:B26)

Taxes (rate = 30%) -6,450 <-- =-B3*B27

Net income without depreciaiton 15,050 <-- =B27+B28

Depreciation tax shield 3,000 <-- =B3*10000

Cash flow 18,050 <-- =B31+B29

This is what the net income

would have been if

depreciation were not an

ex

p

ense for tax

p

ur

p

oses.

The effect of depreciation is to

add a $3,000 tax shield.

Is Sally and Dave’s condo investment profitable?—a preliminary calculation

At this point Sally and Dave can make a preliminary calculation of the net present value

and internal rate of return on their condo investment. Assuming a discount rate of 12% and

assuming that they only hold the condo for 10 years, the NPV of the condo investment is $1,987

and its IRR is 12.48%:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

ABC

Discount rate 12%

Year Cash flow

0 -100,000

1 18,050

2 18,050

3 18,050

4 18,050

5 18,050

6 18,050

7 18,050

8 18,050

9 18,050

10 18,050

Net present value, NPV 1,987 <-- =B5+NPV(B2,B6:B15)

Internal rate of return, IRR 12.48% <-- =IRR(B5:B15)

SALLY & DAVE'S CONDO--preliminary valuation