Menke W. Geophysical Data Analysis: Discrete Inverse Theory

Подождите немного. Документ загружается.

248

13

Numerical

Algorithms

Program

PLS,

continued.

11

12

13

14

do

17

j

=

ntr, mcur

/*

triangularize new columns

alfa

=

0.0

/*

build transformation

k

=

igp(j)

/*

location of j-th column of triangle

do

11

i=j, n

alfa

=

alfa

t

gp(i,k)**2

continue

alfa

=

sqrt(

alfa

)

if( gp(j,k) .It.

0.0

)

then

/*

choose sign

alfa

=

-alfa

end if

u(k)

=

-alfa

t

=

gp(j,k)

+

alfa

if( abs(t) .It. test

)

then

/*

div by

O?

ierr=l

return

end if

gp(j,k)

=

t

beta

=

-u(k)

*

gp(j,k)

do

14

jj

=

j+l, mcur

/*

apply transformation to columns

kk

=

igpcjj)

gama

=

0.0

do 12 i=j, n

gama

=

gama

+

gp(i,kk)*gp(i,k)

continue

gama

=

gama

/

beta

do

13

i=j, n

gp(i,kk)

=

gp(i,kk)

-

gama*gp(i,k)

continue

continue

gama

=

0.0

/*

apply transformation to data vector

do 15 i

=

j, n

gama

=

gama

+

dp(i)*gp(i,k)

15 continue

gama

=

gama

/

beta

do

16

i

=

j, n

dp(i)

=

dp(i)

-

gama*gp(i,k)

16

continue

17

continue

18

19

xm(iv)

=

0.0

do

19

i=mcur,l,-1

/*

back-solve for unknowns

t

=

dp(i)

do

18

j=itl,rncur

k

=

igp(j)

/*

location of j-th column of triangle

t

=

t

-

gp(i,k)

*

m(k)

continue

xm(igp(i))

=

t

/

u(igp(i))

continue

return

end

13.4

L,

Problems with Inequality Constraints

249

FORTRAN

Code (MLIC)

for

the Minimum-Length Solution with Inequality

Constraints

subroutine

mlic

(f,xm,h,n,m,nst,mst, fp,test,ierr)

real

f(nst,mst),

xm(mst),

h(nst), test, fp((m+l)*n)

integer n,

m,

nst,

mst,

npst, mpst,

ierr

/*

subroutine

MLIC

finds the minimum

L2

solution length

/*

subject to linear inequality constraints f*xm .ge. h

/*

protocol:

/*

/*

h: (sent, altered) the n by

m

constraint matrix. This matrix

/*

must be dimensioned at least (m+l)*n in

size

/*

/*

xm:

(returned)

a

vector

of

length

m

of

unknowns. Must be

/*

dimensioned

at

least

n in length

/*

/*

h: (sent, altered)

a

vector of length n of constraints. must be

/*

at

least

m+l

in length

/*

/*

n: (sent) the number of

data

(rows of g, currently limited to be

/*

less

than

or

equal to

99)

/*

/*

m:

(sent) the number

of

unknowns (columns of g)

/*

/*

fp: (scratch)

a

scratch vector

at

least

n*(m+l) in length

/*

/*

test: (sent) division by numbers

smaller

than

test

generates

/*

an error condition, solutions within

test

of zero are considered

/*

feasible

/*

/*

ierr: (returned) an error flag, zero on no error,

-1

on

/*

no feasible solution, positive on other errors.

/*

subroutines needed:

ADD,

SUB,

PLS

real

hp(100), e(100)

/*

must be redimensioned

if

n

gt

99

do

2

i=l,

n

/*

build

(m+l)

by n matrix with f-transpose at top

/*

and h-transpose at bottom

j

=

(m+l)*(i-l)

do

1

k=l,

m

fp(j+k)

=

f(i,k)

1

continue

2

continue

fp(j+m+l)

=

h(i)

do

3

i=l,

m

/*

build

m+l

vector hp

hp(i)

=

0.0

3

continue

hp(m+l)

=

1.0

/*

solve positive

least

squares problem fp*xm=hp

call

pls (fp,xm, hp,m+l, n,m+l, n, f, h, e,m+l,n,

test,

ierr)

if

(

ierr .ne.

0

)

then

return

end if

xnorm

=

0.0

250

13

Numerical

Algorithms

Program

MLIC,

continued.

do

5

i=l, m+l

/*

compute residuals and their

L-2

norm

e(i)

=

-hp(i)

do

4

j=1,

n

e(i)

=

e(i)

+

fp((j-l)*(m+l)+i)*xm(j)

4

continue

5

continue

xnorm

=

xnom

+

e

(i)

**2

xnorm

=

sqrt( xnorm

/

float(m+l)

)

6

if( xnorm .It. test

)

then

else

ierr=-1

/*

constraints incompatible

do

6

i=l, m

xm(i)

=

-e(i)/e(m+l)

continue

ierr=O

end if

return

end

13.5

Finding Eigenvalues

and

Eigenvectors

25

1

13.5

Finding the Eigenvalues and

Eigenvectors

of

a Real

Symmetric Matrix

If

the real symmetric matrix

A

is diagonal, then the process of

finding its eigenvalues and eigenvectors is trivial: the eigenvalues are

just the diagonal elements, and the eigenvectors are just unit vectors in

the coordinate directions. If it were possible to find a transformation

that diagonalized a matrix while preserving lengths, then the eigen-

value problem would essentially be solved. The eigenvalues in both

coordinate systems would be the same, and the eigenvectors could

easily be rotated back into the original coordinate system. (In fact,

since they are unit vectors in the transformed coordinate system, they

simply

are

the elements of the inverse transform.)

Unfortunately, there is no known method of finding a finite number

of unitary transformations that accomplish this goal. It is possible,

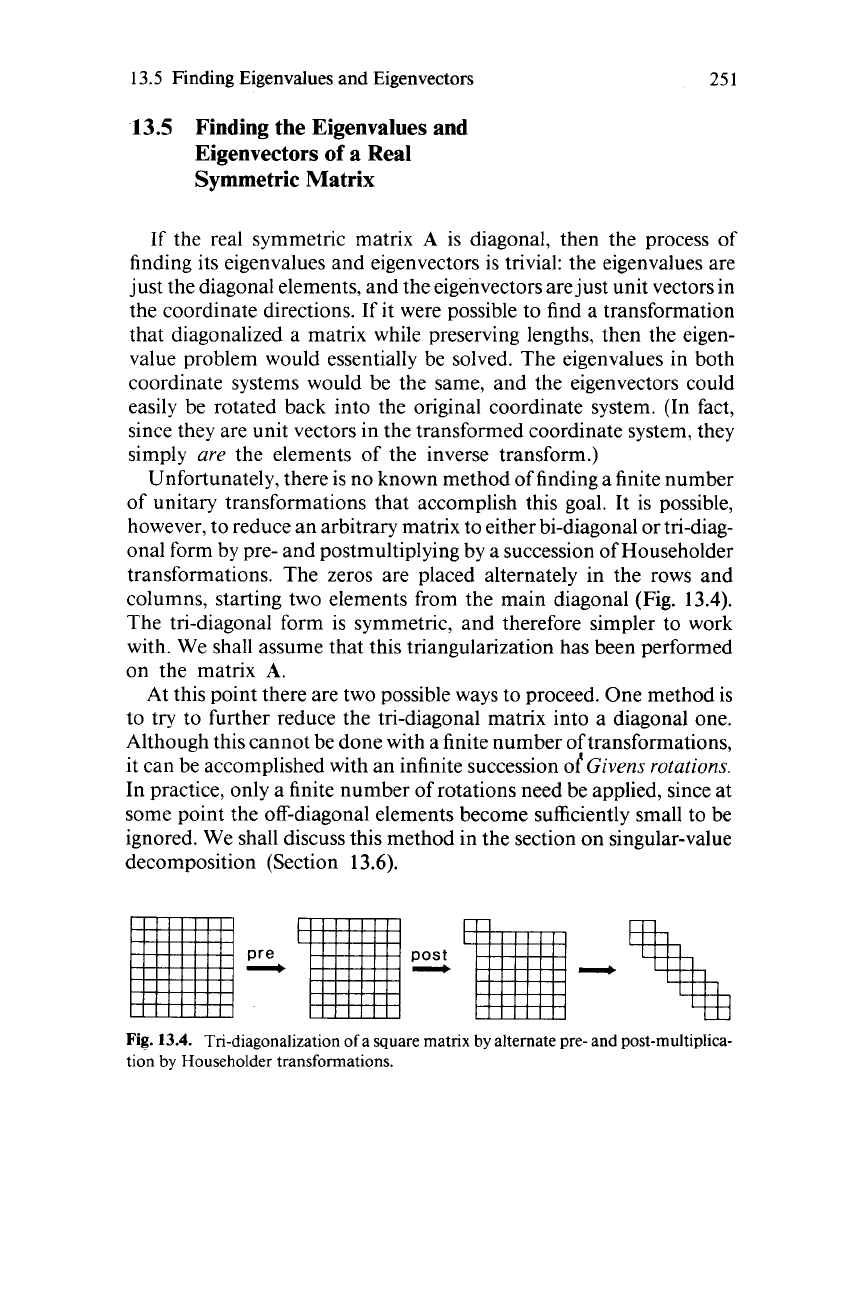

however, to reduce an arbitrary matrix to either bi-diagonal or tri-diag-

onal form by pre- and postmultiplying by a succession of Householder

transformations. The zeros are placed alternately in the rows and

columns, starting two elements from the main diagonal

(Fig.

13.4).

The tri-diagonal form is symmetric, and therefore simpler to work

with. We shall assume that this triangularization has been performed

on the matrix

A.

At this point there are two possible ways to proceed. One method is

to try to further reduce the tri-diagonal matrix into a diagonal one.

Although this cannot be done with a finite number of transformations,

it can be accomplished with an infinite succession

of

Givens rotations.

In practice, only a finite number of rotations need be applied, since at

some point the off-diagonal elements become sufficiently small to be

ignored. We shall discuss this method in the section on singular-value

decomposition (Section

13.6).

post

L

Fig.

13.4. Tri-diagonalization of a square matrix

by

alternate pre- and post-multiplica-

tion

by

Householder transformations.

252

13

Numerical Algorithms

The second method

is

to find the eigenvalues of the tri-diagonal

matrix, which are the roots of its characteristic polynomial

det(A

-

AI)

=

0.

When

A

is

tri-diagonal, these roots can be found by a recursive

algorithm.

To

derive this algorithm, we consider the

4

X

4 tri-diagonal matrix

’

1

(13.6)

where

u,,

b,,

and

c,

are the three nonzero diagonals. When the determi-

nant

is

computed by expanding in minors about the fourth row, there

are only two nonzero terms:

det(A

-

A,)=

(u4-

A)det[

;

u2;A

h”,

]

-

c4

det

[

(‘2

U2

-

A

0

a,

-A

b2

0

c2

a2

-A

b,

0

c3

a3

-

A

b4

0

0

c,

a,

-

A

uI

-A

h2

0I-A

h2

0

uj

-

i

0

(‘3

h4

(I

3.7)

Because all but one element in the last column of the second matrix are

zero, this expression can be reduced to

det(A

-

U)

=

(a,

-

A)

det

[

u2,

A

h”,

1

-

b4h

det

[

[

A-AAI=

U,

-2

b2

UI

-A

h2

(‘2

u2

-

I

U)

-

I

(1

3.8)

The determinant

of

the

4

X

4

matrix

A

is related to the determinants

of

the

3

X

3

and

2

X

2

submatrices in the upper left-hand comer

of

A.

This relationship can easily be generalized to a matrix

of

any size as

PN

=

(‘N

-

A)PN-

I

-

bNcNpN-2

(1

3.9)

where

pN

is the determinant

of

the

N

X

N

submatrix. By defining

p-l

=

0

and

p,,

=

1,

this equation provides a recursive method for

computing the value of the characteristic polynomial for any specific

value

of

A.

This sequence

of

polynomials is a

Sturm

sequence,

which

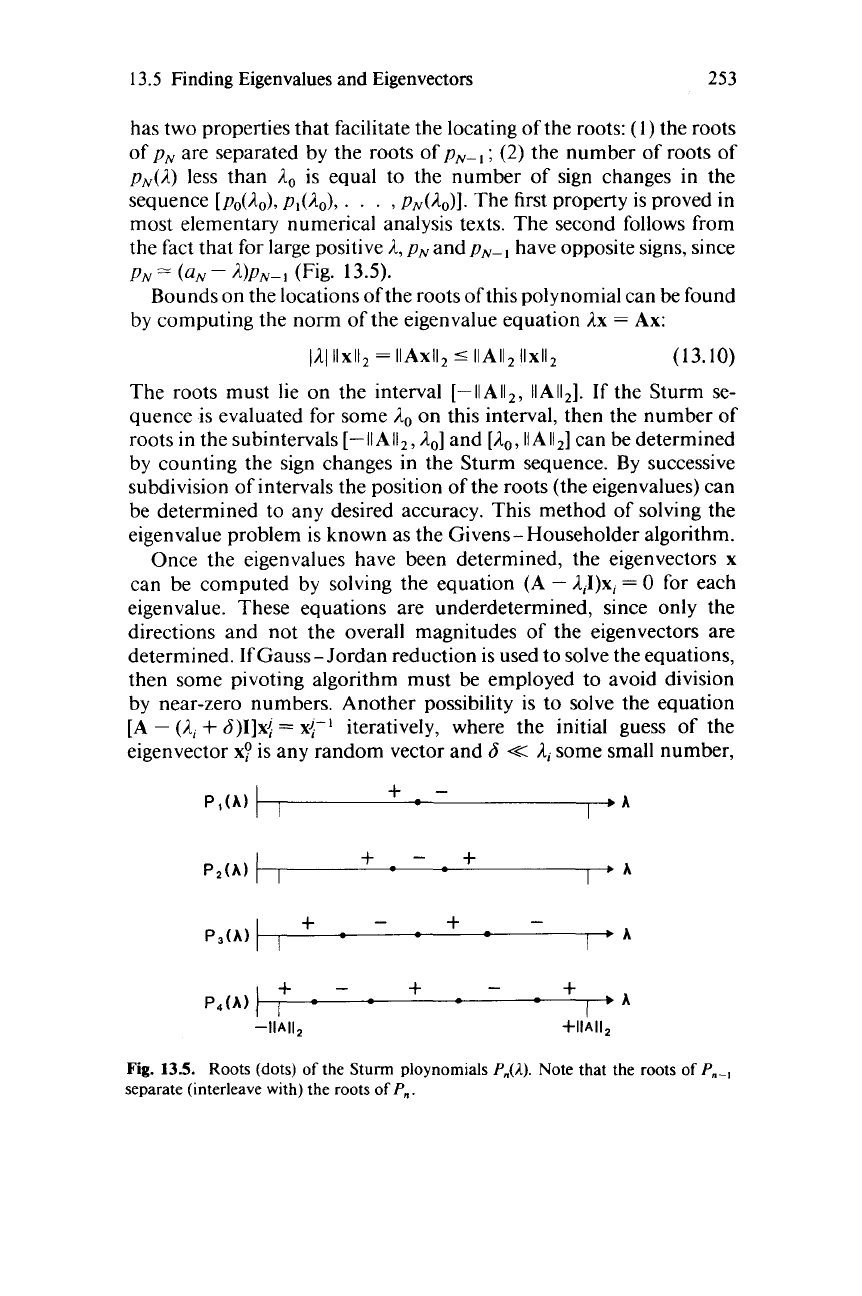

13.5 Finding Eigenvalues and Eigenvectors 253

has two properties that facilitate the locating of the roots:

(I)

the roots

of

PNare separated by the roots

of

PN-I ; (2) the

number

of roots of

PN(A) less than A

o

is equal to the

number

of

sign changes in the

sequence

[Po(A

o),

PI(A

o),

. . . , PN(A

o)].

The first property is proved in

most elementary numerical analysis texts.

The

second follows from

the fact that for large positive

A,PNandPN-I have opposite signs, since

PN= (aN- A)PN-l (Fig. 13.5).

Bounds on the locations

of

the roots

of

this polynomial can be found

by computing the norm

of

the eigenvalue equation

AX

=

Ax:

IAlllxll

2

= IIAxll

2

~

IIAII

211xll

2

(13.10)

The

roots must lie on the interval

[-IIAI1

2

,

IIAII

2

] . If the Sturm se-

quence is evaluated for some

Ao

on this interval, then the number of

roots in the subintervals

[-IIAII

2

,

A

O

]

and

[A

o

,

IIA11

2

]

can be determined

by counting the sign changes in the Sturm sequence. By successive

subdivision

of

intervals the position

of

the roots (the eigenvalues) can

be determined to any desired accuracy. This method

of

solving the

eigenvalue problem is known as the

Givens-

Householder algorithm.

Once the eigenvalues have been determined, the eigenvectors x

can be computed by solving the equation (A -

AiI)x

i

= 0 for each

eigenvalue. These equations are underdetermined, since only the

directions and not the overall magnitudes

of

the eigenvectors are

determined. If

Gauss-Jordan

reduction isused to solve the equations,

then some pivoting algorithm must be employed to avoid division

by near-zero numbers. Another possibility is to solve the equation

[A -

(Ai+

<5)I]x{

= x{-l iteratively, where the initial guess

of

the

eigenvector x? is any random vector and

<5

-e: Aisome small number,

PI

(A)

I

+

• A

•

I

P

2(A)

I

+ +

• A

•

I

P3

(A)

I

+

+

• A

•

P4

(A)

J

+ + +

• A

I

I

-IIAII

2

+IIAII

2

Fig. 13.5. Roots (dots) of the Sturm ploynomials p.().). Note that the roots of

p._

1

separate (interleave with) the roots of pn :

254

13

Numerical Algorithms

to prevent the equations from becoming completely singular. This

iteration typically converges to the eigenvector in only three iterations.

Once the eigenvectors have been determined, they are transformed

back into the original coordinate system by inverting the sequence of

Householder transformations.

13.6

The Singular-Value Decomposition

of

a

Matrix

The first step in this decomposition process is to apply Householder

transformations to reduce the matrix

G

to bi-diagonal form (in the

4

X

4

case) (see Section 13.5):

pl

"2

0

0

1

(13.1

1)

LO

0

0

44-I

where

4,

and

0,

are the nonzero diagonals. The problem is essentially

solved, since the squares ofthe singular values of

G

are the eigenvalues

of

GTG,

which is tri-diagonal with diagonal elements

a,

=

q'

and

off-diagonal elements

b,

=

c,

=

e,q,-,

.

We could therefore proceed by

the symmetric matrix algorithm of Section 13.5. However, since this

algorithm would

be

computing the squares of the singular values,

it

would not

be

very precise. Instead, it is appropriate to deal with the

matrix

G

directly, using the

Golith-

Reinch

mcrhod.

We shall examine the computation of the eigenvalues

of

a

tri-diago-

nal matrix by transformation into

a

diagonal matrix first. Suppose that

the symmetric, tri-diagonal

N

X

N

matrix

A

is transformed by a

unitary transformation into another symmetric tri-diagonal matrix

A'

=

TATT.

It is possible

to

choose this transformation

so

that the

h;

=

ch

elements become smaller in absolute magnitude. Repeated

application of this procedure eventually reduces these elements to

zero. leaving

a

matrix consisting of an

N

-

I

X

N

-

1

tri-diagonal

block and

a

1

X

I

block. The latter is its own eigenvalue. The whole

process can then be repeated on the

N

-

1

X

N

-

I

matrix to yield an

N

-

2

X

N

-

2

block and another eigenvalue. The transformation

A'

=

?'ATT

is accomplished by a coordinate shift. For any

sh$ppuram-

c"cr

a,

A'

=

TATT

=

T[A

-

aI]TT

+

aI.

It can be shown that

if

a

is

13.6

The Singular-Value Decomposition

of

a Matrix

255

chosen to be the eigenvalue of the lower-right

2

X

2

submatrix of

A

that is closest in value to

A,,

and

if

T

is chosen to make

T[A

-

a11

upper triangular, then

A’

is triangular and the

ch

=

6;

elements of

A’

are smaller than the corresponding elements of

A.

The singular values of

G

are found by using the Householder-

Reinch algorithm to diagonalize

A

=

GTG.

All of the operations are

performed on the matrix

G,

and

A

is never explicitly computed. The

shift parameter is first computed by finding the eigenvalues of the

2

X

2

matrix

and selecting the eigenvalue closest to

(4;

+

pi).

A

transformation

must then be found that makes

T(A

-

crT)

upper-triangular. It can be

shown [Ref. 141 that if

A

and

TATT

are symmetric, tri-diagonal

matrices and

if

all but the first element of the first column of

T(A

-

01)

are zero, then

T(A

-

01)

is upper triangular. The effect

T

has on

G

can

be controlled

by

introducing another unitary transformation

R

and

noting that if

G’

=

RTGTT,

then

A’

=

GT’G’

=

TGTRRTGTT

=

TGTGTT

is not a function of

R.

The transformations

T

and

R

are constructed out of a series

of

Givens transformations. These transformations are a special case of

Householder transformations designed to change only two elements of

a vector, one of which is annihilated. Suppose that the elements

u,

and

uJ

are to be altered,

uJ

being annihilated. Then the transformation

TI,

=

q,

=

c,

7;,

=

-

=

s

(all other elements being zero) will

transform

v:

=

(of

+

$)I/*,

u(

=

0

if

c

=

~,/(uf

+

uf!)II2

and

s

=

vJ/(vf

+

u;)’/~.

The first Givens transformation in

T

is chosen to

annihilate the subdiagonal element of the first column

ofT(A

-

GI),

[4:

-

(T.

4,c,,

0,

0,

.

. .

.

OIT.

Now

GT:

is no longer bi-diagonal,

so

a

series of pre- and postmultiplied Givens transformations are applied

which bi-diagonalize it. These transformations define the rest of

’I’

and

R.

Their application is sometimes called

cliusing

since. after each

application

of

a transformation, a nonzero element appears at a new

(off-bi-diagonal) position in

G.

This step assures that

TATT

is tri-diag-

onal. The whole process is iterated until the last subdiagonal element

of

TATT

becomes sufficiently small to be ignored. At this stage

ch

must also be

zero.

so

one singular value

4,

has been found. The whole

process is then repeated on a

G

the size of which has been reduced

by

one row and one column.

256

13

Numerical

Algorithms

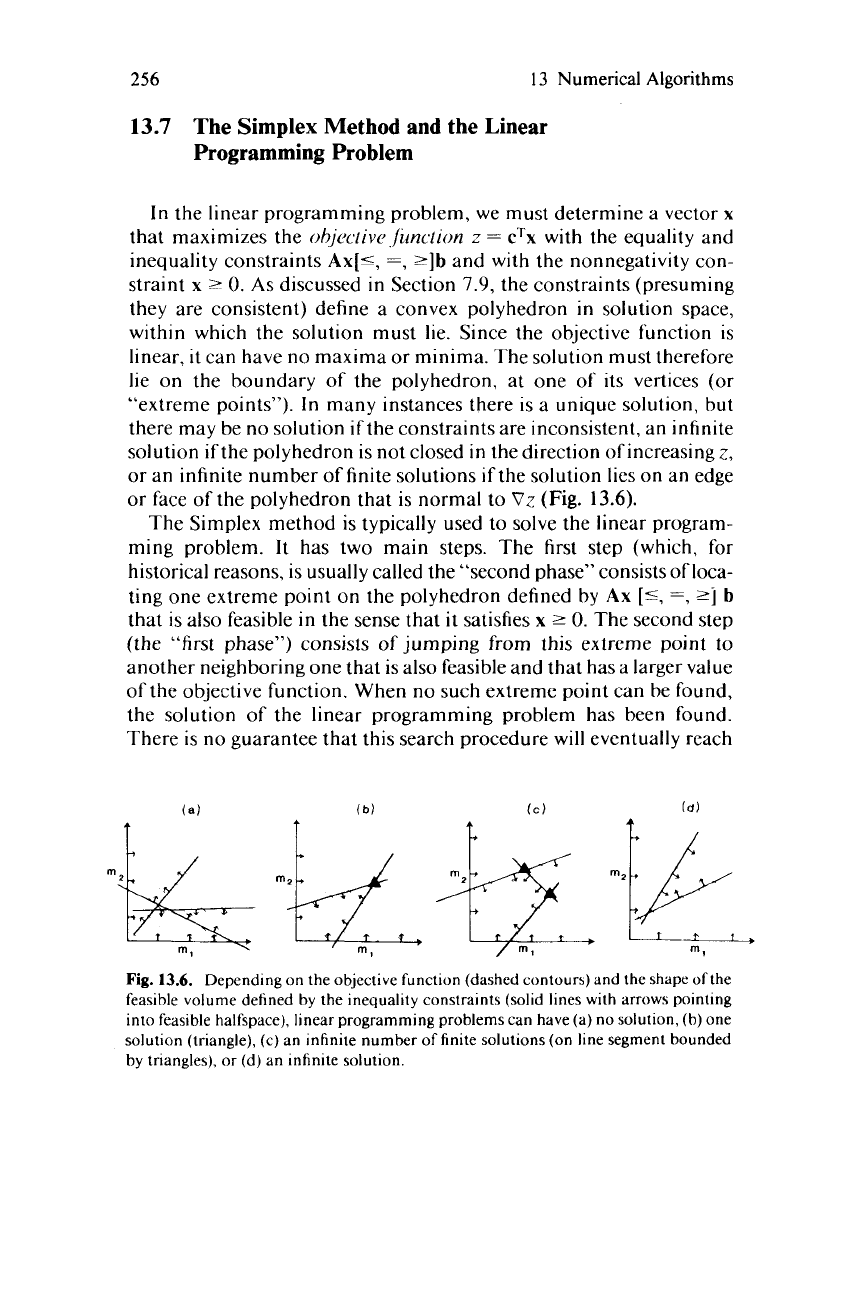

13.7

The Simplex Method and the Linear

Programming Problem

In

the linear programming problem, we must determine a vector

x

that maximizes the

ohjecfive

function

z

=

cTx

with the equality and

inequality constraints

Ax[<,

=,

z]b

and with the nonnegativity con-

straint

x

2

0.

As

discussed in Section

7.9,

the constraints (presuming

they are consistent) define a convex polyhedron in solution space,

within which the solution must lie. Since the objective function is

linear, it can have no maxima or minima. The solution must therefore

lie on the boundary of the polyhedron, at one of its vertices (or

“extreme points”).

In

many instances there is a unique solution, but

there may

be

no solution ifthe constraints are inconsistent, an infinite

solution

if

the polyhedron is not closed in the direction

of

increasing

z,

or an infinite number of finite solutions

if

the solution lies on an edge

or face of the polyhedron that is normal to

Dz

(Fig.

13.6).

The Simplex method is typically used to solve the linear program-

ming problem.

It

has two main steps. The first step (which, for

historical reasons, is usually called the “second phase” consists of loca-

ting one extreme point on the polyhedron defined by

Ax

[s,

=,

2j

b

that is also feasible in the sense that it satisfies

x

2

0.

The second step

(the “first phase”) consists of jumping from this extreme point to

another neighboring one that is also feasible and that has a larger value

of the objective function. When no such extreme point can be found,

the solution of the linear programming problem has been found.

There is no guarantee that this search procedure will eventually reach

m2

kq

mkt,

&,

m/b

Fig.

13.6.

Depending

on

the objective function (dashed contours) and the shape

of

the

feasible volume defined by the inequality constraints (solid lines with arrows pointing

into feasible halfspace), linear programming problems can have (a) no solution,

(b)

one

solution (triangle), (c) an infinite number of finite solutions (on line segment bounded

by triangles),

or (d) an infinite solution.

u

m,

ml

m,

13.7

The Simplex Method and the Linear Programming Problem

257

the “optimum” extreme point (closed loops are possible), but it

usually does.

The inequality constraints

Ax

[s,

=,

21

b

can be converted to

equality constraints by changing all the

2

constraints to

5

constraints

by multiplication by

-

1,

and then changing all the

5

constraints to

equality constraints by increasing the number of unknowns. For

example, if the problem originally has two unknowns and a constraint

x,

+

2x2

I

4,

it can be converted into the equality constraint

x,

+

2x2

+

x3

=

4

by adding the unknown

x3

and requiring that

x3

2

0.

The

transformed linear programming problem therefore has, say,

M

un-

knowns (original ones plus the new “slack” variables)

x,

objective

function

z

=

cTx

(where

c

has been extended with zeros), and, say,

N

linear equality constraints

Ax

=

b.

Since one slack variable was added

for each inequality constraint, these equations will usually be under-

determined

(M

>

N).

If

the ith column

of

A

is denoted by the vector

vi,

the equations

Ax

=

b

can be rewritten as

(13.13)

The vector

b

is of length

N.

It can be represented by a linear combina-

tion of only

N

<

M

of the

vi.

We can find one solution to the constraint

equation by choosing

N

linearly independent columns

of

A,

expand-

ing

b

on this basis, and noting that

N

components of the solution

vector are the expansion coefficients (the rest being zero):

Any solution that can be represented by a sum of precisely Mcolumns

of

A

is

said to be a basic

solution,

and the

N

vectors

vi

are said to form

the basis of the problem. If all the

x,’s

are also nonnegative, the

problem is then said to be basicTeasible.

The key observations used by the Simplex algorithm are that all

basic-feasible solutions are extreme points of the polyhedron and that

all extreme points of the polyhedron are basic-feasible solutions. The

first assertion is proved by contradiction. Assume that

x

is both

basic-feasible and

not

an extreme point. If

x

is not an extreme point,

then it lies along a line segment bounded by two distinct vectors

xI

and

x2

that are feasible points (that is, are within the polyhedron):

x=Ax,

+(I

-A)x2

where

O<A<

1

(1

3.15)

Since

x

is basic, all but Nof its elements are zero. Let the unknowns

be