Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

Model Risk and Liquidity Risk

363

the model assumes to be constant (or deterministic) as well movements in

variables that are assumed to be stochastic. This type of hedging is

imperfect, but hopefully the unhedged risks are largely diversified in a

large portfolio.

For products that are highly structured or do not trade actively models

are used for pricing. In this case choosing the right model is often more of

an art than a science. It is a good practice to use several models and

assumptions about the underlying parameters in order to obtain a

realistic range for pricing and understand the accompanying model risk.

Liquidity risk is the risk that the market will not be able to absorb the

trades a financial institution wants to do at the time it wants to do them.

In normal market conditions liquidity is characterized by a bid-offer

spread. This spread widens as the size of a transaction increases.

The most serious liquidity risks arise from what are sometimes termed

liquidity black holes. These occur when all traders want to be on the same

side of the market at the same time. This may be because they are using

similar models or are subject to similar regulations, or because of a herd

mentality that sometimes develops among traders. Traders that have

long-term objectives should avoid allowing themselves to be influenced

by the short-term overreaction of markets.

FURTHER READING

Derman, E., My Life as a Quant: Reflections on Physics and Finance. New York:

Wiley, 2004.

Persaud, A. D., (ed.), Liquidity Black Holes: Understanding, Quantifying and

Managing Financial Liquidity Risk. London: Risk Books, 1999.

QUESTIONS AND PROBLEMS (Answers at End of Book)

15.1. Give two explanations for the volatility skew observed for options on

equities.

15.2. Give two explanations for the volatility smile observed for options on a

foreign currency.

15.3. "The Black-Scholes model is nothing more than a sophisticated inter-

polation tool." Discuss this viewpoint.

15.4. Using Table 15.1, calculate the volatility a trader would use for an

8-month option with a strike price of 1.04.

364

Chapter 15

15.5. What is the key difference between the models of physics and the models

of finance.

15.6. How is a financial institution liable to find that it is using a model

different from its competitors for a particular type of derivatives product

15.7. What is a liquidity-adjusted VaR designed to measure?

15.8. Explain how liquidity black holes occur. How can regulation lead to

liquidity black holes?

15.9. Distinguish between within-model and outside-model hedging.

15.10. A stock price is currently $20. Tomorrow, news is expected to be

announced that will either increase the price by $5 or decrease the price

by $5. What are the problems in using Black-Scholes to value 1-month

options on the stock?

15.11. Suppose that a central bank's policy is to allow an exchange rate to

fluctuate between 0.97 and 1.03. What pattern of implied volatilities for

options on the exchange rate would you expect to see?

15.12. "For actively traded products traders can mark to market. For structured

products they mark to model." Explain this remark.

15.13. "Hedge funds can either be the solution to black holes or the cause of

black holes." Explain this remark.

ASSIGNMENT QUESTIONS

15.14. Suppose that all options traders decide to switch from Black-Scholes to

another model that makes different assumptions about the behavior of

asset prices. What effect do you think this would have on (a) the pricing

of standard options and (b) the hedging of standard options?

15.15. Using Table 15.1, calculate the volatility a trader would use for an

11-month option with a strike price of 0.98.

15.16. A futures price is currently $40. The risk-free interest rate is 5%. Some

news is expected tomorrow that will cause the volatility over the next

3 months to be either 10% or 30%. There is a 60% chance of the first

outcome and a 40% chance of the second outcome. Use the DerivaGem

software (available on the author's website) to calculate a volatility smile

for 3-month options.

Economic Capital

and RAROC

As we saw in Chapter 1, the role of capital in a bank is to protect

depositors against losses. The capital of a bank consists of common

shareholder's equity, preferred shareholder's equity, subordinated debt,

and other similar items.

In Chapter 7 we discussed the rules that the Basel Committee uses to

determine regulatory capital. These rules are the same for all banks and,

however carefully they have been chosen, it is inevitable that they will not

be exactly appropriate for any particular bank. This has led banks to

calculate economic capital (sometimes also referred to as risk capital).

Economic capital is a bank's own internal estimate of the capital it needs

for the risks it is taking. Economic capital can be regarded as a "cur-

rency" for risk-taking within a bank. A business unit can take a certain

risk only when it is allocated the appropriate economic capital for that

risk. The profitability of a business unit is measured relative to the

economic capital allocated to the unit.

In this chapter we discuss the approaches a bank uses to arrive at

estimates of economic capital for particular risk types and particular

business units and how these estimates are aggregated to produce a single

economic capital estimate for the whole bank. We also discuss risk-

adjusted return on capital or RAROC. This is the return earned by a

business unit on the capital assigned to it. RAROC can be used to assess

the past performance of business units. It can also be used to forecast

future performance of the units and decide on the most appropriate way

366

Chapter 16

of allocating capital in the future. It provides a basis for determining

whether some activities should be discontinued and others expanded.

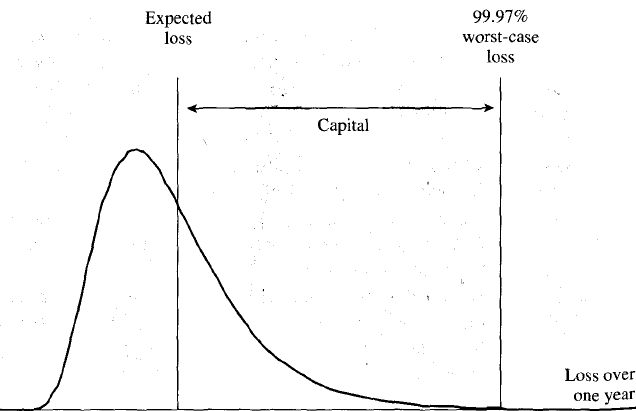

16.1 DEFINITION OF ECONOMIC CAPITAL

Economic capital is defined as the amount of capital a bank needs to

absorb losses over a certain time horizon with a certain confidence level.

The time horizon is usually chosen as one year. The confidence level

depends on the bank's objectives. A common objective for a large

international bank is to maintain an AA credit rating. Corporations rated

AA have a one-year probability of default of about 0.03%. This suggests

that the confidence level should be 99.97%. For a bank wanting to

maintain a BBB credit rating the confidence level is lower. A BBB-rated

corporation has a probability of about 0.2% of defaulting in one year so

that the confidence level is 99.80%.

Capital is required to cover unexpected loss. This is defined as the

difference between the actual loss and the expected loss. The idea here

is that expected losses should be taken account of in the way a bank prices

its products so that only unexpected losses require capital. As indicated in

Figure 16.1, the economic capital for a bank that wants to maintain an

Figure 16.1 Calculation of economic capital from one-year loss distribution

for a AA-rated bank.

Ecomomic Capital and RAROC

367

AA rating is the difference between expected losses and the 99.97 percen-

tile point on the probability distribution of losses.

Example 16.1

When lending in a certain region of the world an AA-rated bank estimates its

losses as 1% of outstanding loans per year on average. The 99.97% worst-case

loss (i.e., the loss exceeded only 0.03% of the time) is estimated as 5% of

outstanding loans. The economic capital required per $100 of loans is therefore

$4.0 (the difference between the 99.97% worst-case loss and the expected loss).

Approaches to Measurement

There are two broad approaches to measuring economic capital: the

"top-down" and "bottom-up" approaches. In the top-down approach

the volatility of the bank's assets is estimated and then used to calculate

the probability that the value of the assets will fall below the value of the

liabilities by the end of the time horizon. A theoretical framework that

can be used for the top-down approach is Merton's model, which was

discussed in Section 11.6.

The approach most often used is the bottom-up approach, where loss

distributions are estimated for different types of risk and different busi-

ness units and then aggregated. The first step in the aggregation can be to

calculate probability distributions for total losses by risk type or total

losses by business unit. A final aggregation gives a probability distribu-

tion of total losses for the whole financial institution.

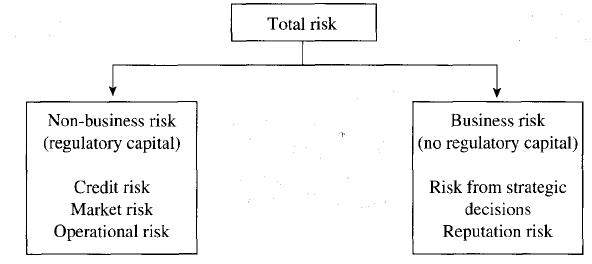

The various risks facing a bank are summarized in Figure 16.2. As we

saw in Chapter 14, regulators have chosen to define operational risk as

"the risk of loss resulting from inadequate or failed internal processes,

Figure 16.2 Categorization of risks faced by a bank in the Basel

II regulatory environment.

368

Chapter 16

people, and systems or from external events." Operational risk includes

model risk and legal risk, but not risks arising from strategic decisions or

business reputation. We will refer to the latter risks collectively as business

risk. Regulatory capital is not required for business risk under Basel II,

but some banks do assess economic capital for business risk.

16.2 COMPONENTS OF ECONOMIC CAPITAL

In earlier chapters we covered approaches used to calculate loss distribu-

tions for different types of risks. Here we review some of the key points.

Market Risk Economic Capital

In Chapters 9 and 10 we discussed the historical simulation and model-

building approaches for estimating the probability distribution of the loss

or gain from market risk. As explained, this distribution is usually calcu-

lated in the first instance with a one-day time horizon. Regulatory capital

for market risk is calculated as a multiple (at least 3.0) of the ten-day 99%

VaR and bank supervisors have indicated that they are comfortable

calculating the ten-day 99% VaR as times the one-day 99% VaR.

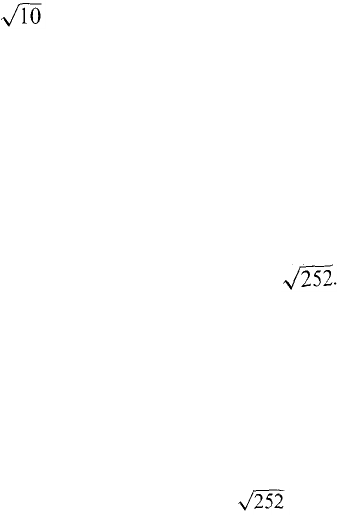

When calculating economic capital, we want to use the same time

horizon and confidence level for all risks. The time horizon is usually

one year and, as explained, the confidence level is often chosen as 99.97%

for an AA-rated bank. The simplest assumptions are (a) that the prob-

ability distribution of gains and losses for each day during the next year

will be the same as that estimated for the first day and (b) that the

distributions are independent. We can then use the central limit theorem

to argue that the one-year loss/gain distribution is normal. Assuming 252

business days in the year, the standard deviation of the one-year loss/gain

equals the standard deviation of the daily loss/gain multiplied by

The mean loss/gain is much more difficult to estimate than the standard

deviation. A reasonable, if somewhat conservative, assumption is that the

mean loss/gain is zero. The 99.97% worst-case loss is then 3.43 times the

standard deviation of the one-year loss/gain. The 99.8% worst-case loss is

2.88 times the standard deviation of the one-year loss/gain.

Example 16.2

Suppose that the one-day standard deviation of market risk losses/gains for a

bank is $5 million. The one-year 99.8% worst-case loss is 2.88 x x 5 =

228.6, or $228.6 million.

Economic Capital and RAROC

369

Note that we are not assuming that the daily losses/gains are normal.

All we are assuming is that they are independent and identically

distributed. The central limit theorem of statistics tells us that the

sum of many independent identically distributed variables is approxi-

mately normal. If losses on successive days are correlated, we can

assume first-order autocorrelation, estimate the correlation parameter

from historical data, and use the results in Section 8.4. When the

autocorrelation is not too high, it is still reasonable to assume that

the one-year loss distribution is normal. If a more complicated model

for the relationship between losses on successive days is considered

appropriate, then the one-year loss distribution can be calculated using

Monte Carlo simulation.

Credit Risk Economic Capital

Although Basel II gives banks that use the internal ratings based approach

for regulatory capital a great deal of freedom, it does not allow them to

choose their own credit correlation model and correlation parameters.

When calculating economic capital, banks are free to make the assump-

tions they consider most appropriate for their situation. As explained in

Section 12.6, CreditMetrics is often used to calculate the specific risk

capital charge for credit risk in the trading book. It is also sometimes used

when economic capital is calculated for the banking book. A bank's own

internal rating system can be used instead of that of Moody's or S&P when

this method is used.

Another approach that is sometimes used is Credit Risk Plus, which is

described in Section 12.5. This approach borrows a number of ideas from

actuarial science to calculate a probability distribution for losses from

defaults. Whereas CreditMetrics calculates the loss from downgrades and

defaults, Credit Risk Plus calculates losses from defaults only.

In calculating credit risk economic capital, a bank can choose to adopt

a conditional or unconditional model. In a conditional (cycle-specific)

model, the expected and unexpected losses take account of current

economic conditions. In an unconditional (cycle-neutral) model, they

are calculated by assuming economic conditions that are in some sense

an average of those experienced through the cycle. Rating agencies aim

to produce ratings that are unconditional. Moreover, when regulatory

capital is calculated using the internal ratings based approach, the PD

and LGD estimates should be unconditional. Obviously it is important

to be consistent when economic capital is calculated. If expected losses

370

Chapter 16

are conditional, unexpected losses should also be conditional. If ex-

pected losses are unconditional, the same should be true of unexpected

losses.

A particularly challenging task is to take counterparty risk on deriva-

tives into account when credit risk loss distributions are calculated. In

practice, banks often use approximations to the approach outlined in

Section 12.1. For example, they might develop look-up tables for expected

exposure during the life of an instrument and assume that exposure

remains constant at this level. When a bank has several different exposures

with the same counterparty and there are netting agreements, algorithms

for calculating expected exposure can be developed. Other features of

derivative contracts such as Collateralization and downgrade triggers can

be incorporated.

Operational Risk Economic Capital

Banks are given a great deal of freedom in the assessment of regulatory

capital for operational risk under the advanced measurement approach. It

is therefore likely that most banks using this approach will calculate

operational risk economic capital and operational risk regulatory capital

in the same way. As noted in Chapter 14, methods for calculating

operational risk capital are still evolving. Some approaches are statistical

and others are more subjective.

Business Risk Economic Capital

As mentioned earlier, business risk includes strategic risk (relating to a

bank's decision to enter new markets and develop new products) and

reputational risk. Business risk is even more difficult to quantify than

operational risk and estimates are likely to be largely subjective. It is

important that senior risk managers within a financial institution have a

good understanding of the portfolio of business risks being taken. This

should enable them to assess the capital required for the risks and, more

importantly, the marginal impact on total risk of new strategic initiatives

that are being contemplated.

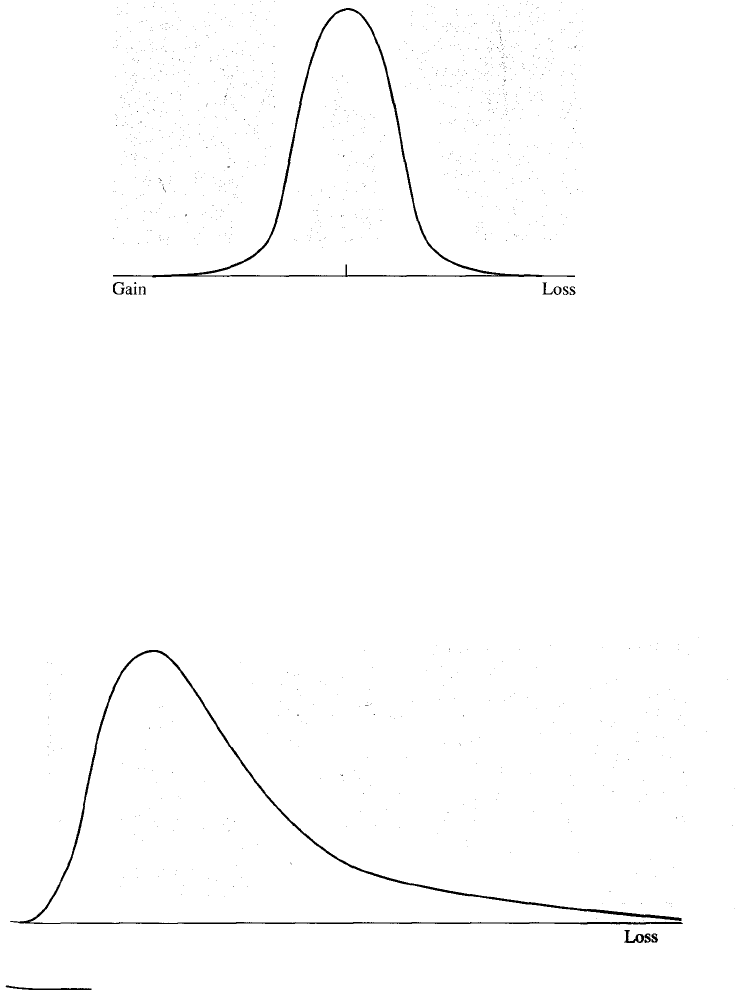

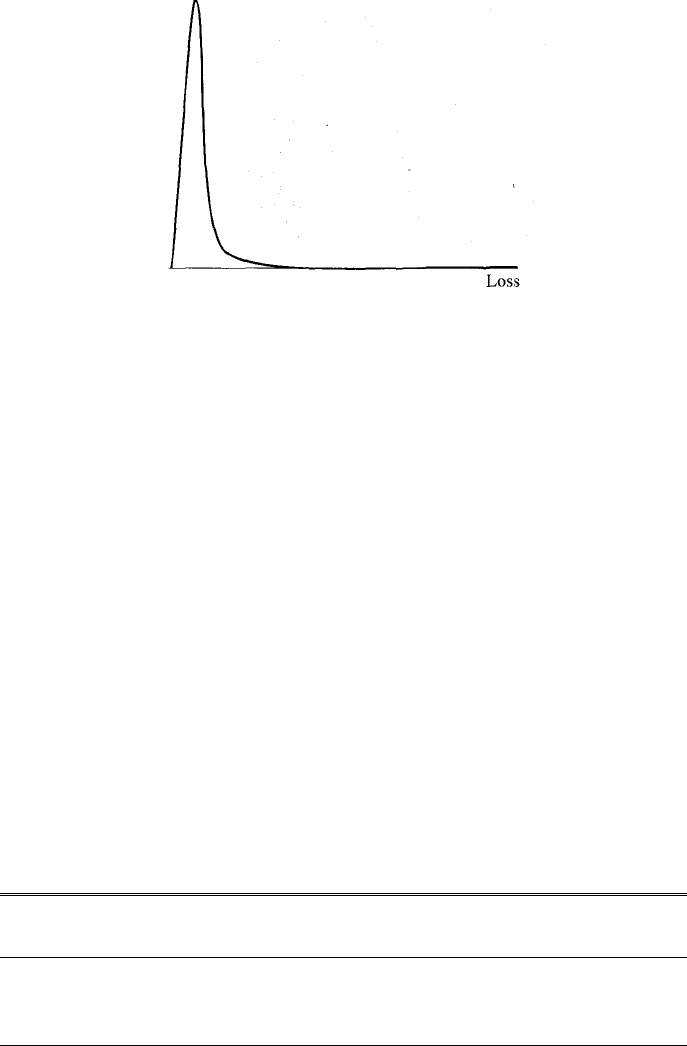

16.3 SHAPES OF THE LOSS DISTRIBUTIONS

The loss probability distributions for market, credit, and operational risk

are very different. Rosenberg and Schuermann used data from a variety of

Economic Capital and RAROC 371

Figure 16.3 Loss density distribution for market risk.

different sources to estimate typical shapes for these distributions.

1

These

are shown in Figures 16.3, 16.4, and 16.5. The market risk loss distribution

(see Figure 16.3) is symmetrical, but not perfectly normally distributed. A

t-distribution with 11 degrees of freedom provides a good fit. The credit

risk loss distribution in Figure 16.4 is quite skewed, as one would expect.

The operational risk distribution in Figure 16.5 has a quite extreme shape.

Most of the time losses are modest, but occasionally they are very large.

We can characterize a distribution by its second, third, and fourth

moments. Loosely speaking, the second moment measures standard

deviation (or variance), the third Skewness, and the fourth kurtosis

Figure 16.4 Loss density distribution for credit risk.

1

See J. V. Rosenberg and T. Schuermann, "A General Approach to Integrated Risk

Management with Skewed, Fat-Tailed Risks," Federal Reserve Bank of New York, Staff

Report No. 185, May 2004.

372

Chapter 16

Figure 16.5 Loss density distribution for

operational risk.

(i.e., the heaviness of tails). Table 16.1 summarizes the properties of

typical loss distributions for market, credit, and operational risk.

16.4 RELATIVE IMPORTANCE OF RISKS

The relative importance of different types of risks depends on the business

mix. For a bank whose prime business is taking deposits and making

loans, credit risk is of paramount importance. For an investment bank,

credit risk and market risk are both important. For an asset manager, the

greatest risk is operational risk. If rules on the ways funds are to be

invested are not followed, there are liable to be expensive investor law

suits. Business Snapshot 16.1 gives one example of this. Another high-

profile example is provided by the Unilever's pension plan. Mercury Asset

Management, owned by Merrill Lynch, pledged not to underperform a

benchmark index by more than 3%. Between January 1997 and March

1998 it underperformed the index by 10.5%. Unilever sued Merrill Lynch

for $185 million and the matter was settled out of court.

Table 16.1 Characteristics of loss distributions for different risk types.

Market risk

Credit risk

Operational risk

Second moment Third moment

(standard deviation) (skewness)

High Zero

Moderate Moderate

Low High

Fourth moment

(kurtosis)

Low

Moderate

High