Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

Model Risk and Liquidity Risk

353

One danger in model building is Overfitting. Consider the problem

posed by the volatility surface in Table 15.1. We can exactly match the

volatility surface with a single model by extending Black-Scholes so that

volatility is a complex function of the underlying asset price and time.

7

But when we do this, we may find that other properties of the model are

less reasonable than those of simpler models. In particular, the joint

probability of the asset prices at two or more times may be unrealistic.

8

Another danger in model building is Overparameterization. The Black-

Scholes model can be extended to include features such as a stochastic

volatility or jumps in the asset price. This invariably introduces extra

parameters that have to be estimated. It is usually claimed that the

parameters in complex models are more stable those in simpler models

and do not have to be adjusted as much from day to day. This may be

true, but we should remember that we are not dealing with physical

processes. The parameters in a complex model may remain relatively

constant for a period of time and then change, perhaps because there

has been what economists refer to as a regime shift. A financial institution

may find that a complicated model is an improvement over a simple

model until the parameters change. At that time it may not have the

flexibility to cope with changing market conditions.

As we have mentioned, traders like simple models that have just one

unobservable parameter. They are skeptical of more complex models

because they are "black boxes" and it is very difficult to develop intuition

about them. In some situations their skepticism is well founded for the

reasons we have just mentioned.

15.6 DETECTING MODEL PROBLEMS

The risk management function within a financial institution should care-

fully monitor the financial institution's trading patterns. In particular it

7

This is the implied volatility function model proposed by B. Dupire, "Pricing with a

Smile," Risk, 7 (February 1994), 18-20; E. Derman and I. Kani, "Riding on a Smile,"

Risk, 7 (February 1994), 32-39; M. Rubinstein, "Implied Binomial Trees," Journal of

Finance, 49, 3 (July 1994), 771-818.

8

Instruments such as barrier options and compound options depend on the joint

Probability distribution of the asset price at different times. Hull and Suo find that the

implied volatility function model works reasonably well for compound options, but

sometimes gives serious errors for barrier options. See J. C. Hull and W. Suo, "A

Methodology for the Assessment of Model Risk and its Application to the Implied

Volatility Function Model," Journal of Financial and Quantitative Analysis, 37, 2 (June

2002), 297-318.

354

Chapter 15

should keep track of the following:

1. The type of trading the financial institution is doing with other

financial institutions

2. How competitive it is in bidding for different types of structured

transactions

3. The profits being recorded from the trading of different products

Getting too much of a certain type of business or making huge profits

from relatively simple trading strategies can be a warning sign. Another

clear indication that something is wrong is when the financial institution

is unable to unwind trades at close to the prices given by its computer

models.

The high profits being recorded for Joseph Jett's trading at Kidder

Peabody (see Business Snapshot 15.1) should have been a warning sign.

9

Furthermore, if in the mid-1990s a financial institution's risk manage-

ment team discovered that traders were entering into a large number of

LIBOR-in-arrears swaps with other financial institutions (see Business

Snapshot 15.2) where they were receiving fixed and paying floating, they

could have alerted modelers to a potential problem and directed that

trading in the product be temporarily stopped.

There are other ways in which a derivatives dealer might find that one of

its models is out of line with that used by other market participants.

Dealers often subscribe to services that are designed to provide market

quotes for representative trades. Typically the company providing this

service periodically asks its dealer clients for quotes on specific hypo-

thetical transactions. It then averages the quotes (possibly after eliminating

the highest and lowest) and feeds the results back to the dealers.

15.7 TRADITIONAL VIEW OF LIQUIDITY RISK

Liquidity is liable to affect both the funding and trading activities of a

financial institution. We start by considering trading activities and move

on to consider funding activities in Section 15.10.

The traditional view of liquidity risk in trading is that there is a

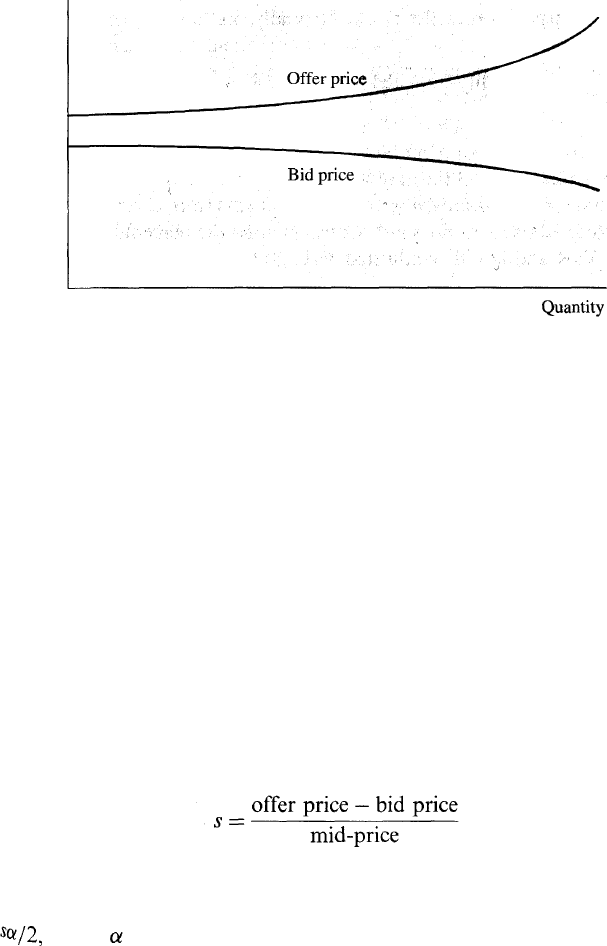

relationship between price and quantity. This relationship is shown in

Figure 15.3. When the quantity of an asset that is traded is relatively

9

Barry Finer, risk manager for the government bond desk at Kidder Peabody, did point

out the difficulty of making large arbitrage profits from a market as efficient as the US

government bond market, but his concerns were dismissed out of hand.

Model Risk and Liquidity Risk

355

Figure 15.3 Bid and offer prices as a function of quantity

transacted.

small, bid-offer spreads are low. As the quantity increases, the price paid

by the buyer of the asset increases and the price received by the seller of

the asset decreases.

How can a financial institution manage liquidity in the trading book?

One way is by using position limits. If the size of the financial institution's

position is limited, the size of a trade it has to do to unwind a position is

also limited. It is often argued that the time horizon in a VaR calculation

should reflect the time necessary to unwind a position. If a position can

be unwound very quickly, a one-day time horizon is appropriate; in other

circumstances, time horizons as long as one month may be needed.

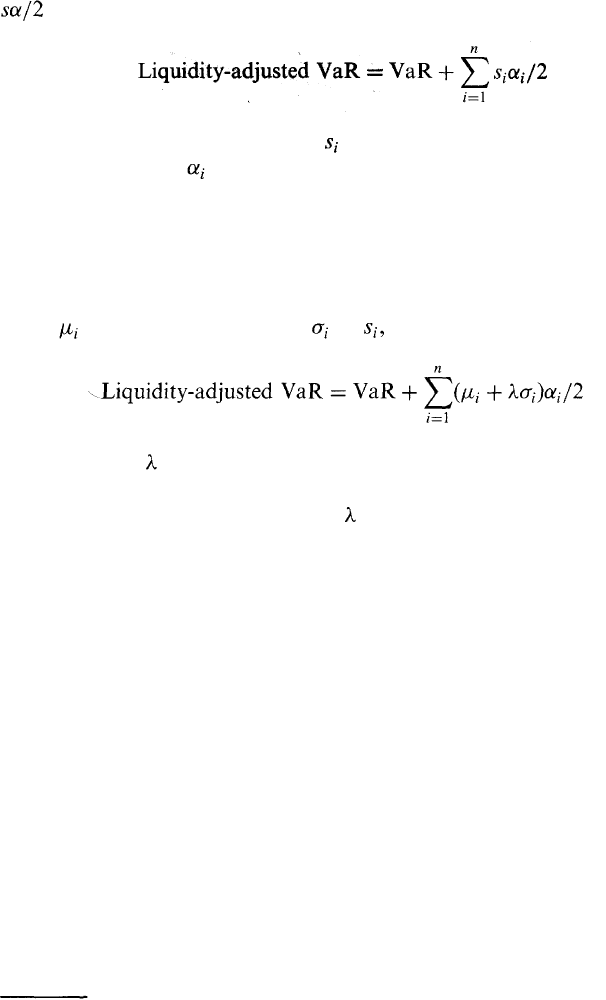

Liquidity-Adjusted VaR

The percentage bid-offer spread for an asset can be defined as

where the mid-price is halfway between the bid and the offer. In liquidat-

ing a position in the asset, a financial institution incurs a cost equal to

where is the dollar value of the position. This reflects the fact that

trades are not done at the mid-market price. A buy trade is done at a

Proportional amount s/2 above the market price and a sell trade is done

at a proportional amount s/2 below the market price.

Risk managers sometimes calculate a liquidity-adjusted VaR by adding

356

Chapter 15

for each position in the book. Formally, we have

where n is the number of positions, is the percentage bid-offer spread for

the ith position and is the amount of money invested in the ith position.

As the number of positions, n, grows, VaR benefits from diversification but

the liquidity adjustment does not. Consequently, the percentage difference

between VaR and liquidity-adjusted VaR grows as n grows.

A variation on this calculation that takes account of uncertainty in the

spread has been suggested by Bangia et al.

10

This involves estimating the

mean and standard deviation of and defining

The parameter gives the required confidence level for the spread on the

assumption that spreads are normally distributed. For example, if a 95%

confidence level is required, then = 1.64. Bangia et al.'s equation

assumes (conservatively) that spreads in all instruments are perfectly

correlated.

15.8 LIQUIDITY BLACK HOLES

The liquidity risk we have just described is real. Banks cannot trade at

mid-market prices and the bigger the size of their transaction the higher

the bid-offer spread that they face. However, there is a more serious

liquidity risk. This is the risk that liquidity in a particular market will dry

up completely because everyone wants to buy and no-one wants to sell, or

vice versa.

It is sometimes argued that technological and other developments have

led to a steady improvement in the liquidity of financial markets. This is

questionable. It is true that bid-offer spreads have on average declined.

However, there has been an increasing tendency toward "herd behavior

where almost everyone wants to do the same type of trade at particular

10

See A. Bangia, F. Diebold, T. Schuermann, and J. Stroughair, "Liquidity on the

Outside," Risk, 12 (June), 68-73.

Model Risk and Liquidity Risk 357

times. The result has been what Persaud refers to as "liquidity black

holes" occurring with increasing frequency.

11

In a well-functioning market, the market may change its opinion about

the price of an asset because of new information. However, the price does

not overreact. If a price decrease is too great, traders will quickly move in

and buy the asset and a new equilibrium price will be established. A

liquidity black hole is created when a price decline causes more market

participants to want to sell, driving prices well below where they will

eventually settle. During the sell-off, liquidity dries up and the asset can

be sold only at a fire-sale price.

12

Among the reasons for herd behavior and the creation of liquidity

black holes are:

1. The computer models used by different traders are similar.

2. All financial institutions are regulated in the same way and respond

in the same way to changes in volatilities and correlations.

3. There is a natural tendency to feel that if other people are doing a

certain type of trade then they must know something that you do not.

Computer Models

A classic example of computer models causing a liquidity black hole is

the stock market crash of October 1987. In the period leading up to the

crash, the stock market had performed very well. Increasing numbers of

portfolio managers were using commercially available programs to

synthetically create put options on their portfolios. These programs told

them to sell part of their portfolio immediately after a price decline and

buy it back immediately after a price increase. The result, as indicated in

Business Snapshot 15.4, was prices plunging well below their long-run

equilibrium levels on October 19, 1987.

As another example of computer models leading to liquidity black

holes, consider the situation where financial institutions are on one side

of the market for a derivative and their clients are on the other side. When

the price of the underlying asset moves, all financial institutions execute

the same trades to maintain a delta-neutral position. This causes the price

of the asset to move further in the same direction. An example of this is

outlined in Business Snapshot 15.5.

11

See A. D. Persaud (ed.), Liquidity Black Holes: Understanding, Quantifying and

Managing Financial Liquidity Risk, Risk Books, 1999.

12

Liquidity black holes tend to be associated with price decreases, but it is possible for

thern to occur when there are price increases.

\

358 Chapter 15

The Impact of Regulation

In many ways it is a laudable goal on the part of regulators to seek to

ensure that banks and other financial institutions throughout the world

are regulated in the same way. As we explained in Chapter 7, capital

requirements and the extent to which they were enforced varied from

country to country prior to Basel I. Banks were competing globally and

as a result a bank subject to low capital requirements, or capital require-

ments that were not strictly enforced, had a competitive edge.

However, a uniform regulatory environment comes with costs. All

banks tend to respond in the same way to external events. Consider,

for example, market risk. When volatilities and correlations increase,

market VaR and the capital required for market risks increase. As a

result, banks tend to take steps to reduce their exposures. Since banks

Business Snapshot 15.4 The Crash of 1987

On Monday, October 19, 1987, the Dow J ones Industrial Average dropped by

more than 20%. Portfolio insurance played a major role in this crash. In

October 1987 between $60 billion and $90 billion of equity assets were subject

to portfolio insurance schemes where put options were created synthetical

using a type of "stop-loss" trading strategy.

During the period Wednesday, October 14, 1987, to Friday, October

1987, the market declined by about 10%, with much of this decline take

place on Friday afternoon. The portfolio insurance schemes should have

generated at least $12 billion of equity or index futures sales as a result

this decline. In fact, portfolio insurers had time to sell only $4 billion and then

approached the following week with huge amounts of selling already dictated

by their models. It is estimated that, on Monday, October 19, sell programs

three portfolio insurers accounted for almost 10% of the sales on the New

York Stock Exchange, and that portfolio insurance sales amounted to 21.3%

of all sales in index futures markets. It is likely that the decline in equity pri???

was exacerbated by investors other than portfolio insurers selling heavily

anticipation of the actions of portfolio insurers.

As the market declined so fast and the stock exchange systems were over-

loaded, many portfolio insurers were unable to execute the trades generated

their models and failed to obtain the protection they required. Needless to say ,

the popularity of portfolio insurance schemes has declined significantly since

1987. One of the morals of this story is that it is dangerous to follow a

particular trading strategy—even a hedging strategy—when many other mar-

ket participants are doing the same thing.

Model Risk and Liquidity Risk

359

often have similar positions to each other, they try to do similar trades. A

liquidity black hole can then develop.

Consider next credit risk. During the low point of the economic cycle,

default probabilities are relatively high and capital requirements for loans

under the Basel II internal ratings based models tend to be high. As a

result banks may be less willing to make loans, creating a liquidity black

hole for small and medium-sized businesses. The Basel Committee has

recognized this as a problem and has dealt with it by asserting that the

probability of default should be an average of the probability of default

through the economic or credit cycle, rather than an estimate applicable

to one particular point in time.

The Importance of Diversity

Economic models usually assume that market participants act independ-

ently. We have argued that this is often not the case. It is this lack of

independence that causes liquidity black holes. To solve the problem of

liquidity black holes, we need more diversity in financial markets.

One conclusion from the arguments we have put forward is that a

contrarian investment strategy has some merit. If markets overreact an

investor can do quite well by buying when everyone else is selling and

there is very little liquidity. However, it can be quite difficult for a fund to

follow such a strategy if it is subject to the VaR-based risk management

measures that have become standard.

Business Snapshot 15.5 British Insurance Companies

In the late 1990s, British insurance companies had entered into many contracts

promising that the rate of interest applicable to an annuity received by an

individual on retirement would be the greater of the market rate and a

guaranteed rate. At about the same time, largely because of regulatory

pressures, all insurance companies decided to hedge part of their risks on

these contracts by buying long-dated swap options from financial institutions.

The financial institutions they dealt with hedged their risks by buying large

numbers of long-dated sterling bonds. As a result, bond prices rose and

sterling long-term interest rates declined. More bonds had to be bought to

maintain the dynamic hedge, long-term sterling interest rates declined further,

and so on. Financial institutions lost money and, because long-term interest

rates declined, insurance companies found themselves in a worse position on

the risks that they had chosen not to hedge.

360

Chapter 15

Volatilities and correlations tend to be "mean reverting". They some-

times increase but over time they get pulled back to long-run average

levels. One way of creating diversity is to recognize in regulation and in

risk management practices that not all market participants should be

concerned about short-term changes in volatilities and correlations. Asset

managers, for example, should base their decisions on long-term average

volatilities and correlations. They should not join the herd when liquidity

holes develop.

Hedge Funds

Hedge funds have become important participants in financial markets in

recent years. A hedge fund is similar to a mutual fund in that it invests

money on behalf of clients. However, unlike mutual funds hedge funds

are not required to register under US federal securities law. This is

because they accept funds only from financially sophisticated individuals

and do not publicly offer their securities. Mutual funds are subject to

regulations requiring that shares in the funds be fairly priced, that the

shares be redeemable at any time, that investment policies be disclosed,

that the use of leverage be limited, that no short positions be taken, and

so on. Hedge funds are relatively free of these regulations. This gives them

a great deal of freedom to develop sophisticated, unconventional, and

proprietary investment strategies. The fees charged by hedge fund man-

agers are dependent on the fund's performance and are relatively high—

typically 1 to 2% of the amount invested plus 20% of the profits.

Hedge funds have grown in popularity with about $1 trillion being

invested throughout the world for clients in 2004. "Funds of funds" have

been set up to invest in a portfolio of other hedge funds. At the time of

writing, hedge funds are still largely unregulated. This means that they do

not have to assess risk in the same way as other financial institutions. As a

result, hedge funds are in an ideal position to provide liquidity when black

holes show signs of developing. If hedge funds are regulated in the future, it

is to be hoped that the regulations will not be the same as those applying to

other financial institutions.

15.9 LONG-TERM CAPITAL MANAGEMENT

Hedge funds themselves can run into liquidity problems and create or

exacerbate liquidity black holes. The most famous example here is Long-

Model Risk and Liquidity Risk

361

Term Capital Management (LTCM) which was discussed in Business

Snapshot 12.1.

LTCM's problems were exacerbated by the fact that its leverage was

huge. It had about $125 billion of assets (plus large numbers of off-

balance-sheet derivatives transactions such as swaps) and only $5 billion

of capital. It was unable to make the payments required under its Collater-

alization agreements. There was a great deal of concern about the ability of

the financial system to cope with a potential failure of LTCM. What

actually happened was a cash injection by a group of banks and an orderly

liquidation that led to a total loss of about $4 billion. If the fund had been

less highly leveraged, it would probably have been able to survive the flight

to quality and could have waited for the previous relationship between the

prices of the liquid and illiquid securities to resume.

Why was the flight to quality so large? One reason is that there were

rumors in the market that LTCM was experiencing financial difficulties.

These rumors led people to anticipate the sort of trades LTCM would

have to do to close out its positions and the likely effect of those trades on

market prices. When everyone anticipates that something will happen in

financial markets it tends to happen. Another reason is that LTCM had

been highly successful during the 1995 to 1997 period. As a result there

were many other hedge funds trying to imitate its strategy. These hedge

funds also experienced financial difficulties and tried to close out their

positions. This accentuated market movements.

15.10 LIQUIDITY vs. PROFITABILITY

Finally it should be noted that there can be liquidity problems without

profitability problems. For example, a profitable bank can experience a

run on deposits and run into liquidity problems. Banking is to a large

extent about confidence. A bank relies on the withdrawal of deposits

being roughly balanced by new deposits so that funding from liabilities

remains roughly constant (see Section 1.3). If there is a temporary short-

fall, it is handled by interbank borrowing.

13

However, if there is a loss of

confidence in the bank—however unjustified this might be—the bank is

liable to experience catastrophic liquidity problems.

Liquidity funding problems can be experienced by all sorts of com-

panies. We have all heard stories about profitable companies that for

13

Across the whole banking system the funds on deposit should remain roughly constant

as a withdrawal from one bank usually becomes a deposit with another bank.

362

Chapter 15

some reason "fell through the cracks" when trying to arrange venture

capital funding or bank loans. An extreme example of a liquidity funding

problem is provided by a German company, Metallgesellschaft, that

entered into profitable fixed-price oil and gas contracts with its customers

(see Business Snapshot 15.6).

Liquidity funding problems can in part be avoided by carrying out

scenario analyses and taking steps to avoid the possibility of outcomes

where short-term cash drains are difficult to fund.

SUMMARY

Since the publication of the Black-Scholes model in 1973 a huge amount

of effort has been devoted to the development of improved models for the

behavior of asset prices. It might be thought that it is just a matter of time

before the perfect model is produced. Unfortunately, this is not the case.

Models in finance are different from those in the physical sciences because

they are ultimately models of human behavior. They are always likely to

be at best approximations to the way market variables behave. Further-

more, from time to time there are regime shifts where there are funda-

mental changes in the behavior of market variables.

For products that trade actively, models are used primarily for com-

municating prices, interpolating between market prices, and hedging-

When hedging, traders use both within-model hedging and outside-model

hedging. This means that they hedge against movements in variables that

Business Snapshot 15.6 Metallgesellschaft

In the early 1990s, Metallgesellschaft (MG) sold a large volume of five- to

ten-year heating oil and gasoline fixed-price supply contracts to its customers

at 6 to 8 cents above market prices. It hedged its exposure with long positions

in short-dated futures contracts that were rolled forward. As it turned out, the

price of oil fell and there were margin calls on the futures positions. Con-

siderable short-term cash-flow pressures were placed on MG. Those at MG

who devised the hedging strategy argued that these short-term cash outflows

were offset by positive cash flows that would ultimately be realized on the

long-term fixed-price contracts. However, the company's senior management

and its bankers became concerned about the huge cash drain. As a result, the

company closed out all the hedge positions and agreed with its customers that

the fixed-price contracts would be abandoned. The outcome was a loss to

MG of $1.33 billion.