Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

250

Chapter 10

the effect of giving a higher value to the probability that extreme values

for several variables occur simultaneously.

We can assume any set of distributions for the in conjunction with

a copula model.

11

Suppose, for example, that we use a Gaussian copula

model. As explained in Chapter 6, this means that, when the changes

in market variables are transformed on a percentile-to-percentile basis to

normally distributed variables u

i

the u

i

are multivariate normal. We can

follow the five steps given earlier except that Step 2 is changed and a step

is inserted between Steps 2 and 3 as follows:

2. Sample once from the multivariate probability distribution for

the u

i

.

2a. Transform each u

i

to on a percentile-to-percentile basis.

If a bank has already implemented the Monte Carlo simulation approach

for calculating VaR assuming percentage changes in market variables are

normal, it should be relatively easy to modify calculations to implement

the approach we describe here. Just before the portfolio is valued it is

necessary to insert a line or two of code into the computer program to do

the transformation in Step 2a. The marginal distributions of the can

be calculated by fitting a more general distribution than the normal

distribution to empirical data.

10.9 MODEL BUILDING vs. HISTORICAL SIMULATION

In the last chapter and this one, we have discussed two methods for

estimating VaR: the historical simulation approach and the model-build-

ing approach. The advantages of the model-building approach are that

results can be produced very quickly and it can easily be used in

conjunction with volatility and correlation updating schemes such as

those described in Chapters 5 and 6. As mentioned in Section 9.3,

volatility updating can be incorporated into the historical simulation

approach—but in a rather more artificial way. The main disadvantage

of the model-building approach is that (at least in the simplest version of

the approach) it assumes that the market variables have a multivariate

normal distribution. In practice, daily changes in market variables often

have distributions that are quite different from normal (see, for example,

Table 5.2). A user of the model-building approach is hoping that some

See J. Hull and A. White, "Value at Risk When Daily Changes Are Not Normally

Distributed," Journal of Derivatives, 5, No. 3 (Spring 1998), 9-19.

VaR: Model-Building Approach 251

form of the central limit theorem of statistics applies to the portfolio, so

that the probability distribution of daily gains/losses on the portfolio is

normally distributed—even though the gains/losses on the component

parts of the portfolio are not normally distributed.

The historical simulation approach has the advantage that historical

data determines the joint probability distribution of the market variables.

It is also easier to handle interest rates in a historical simulation because

on each trial a complete zero-coupon yield curve for both today and

tomorrow can be calculated. The somewhat messy cash-flow-mapping

procedure described in Section 10.3 is avoided. The main disadvantage

of historical simulation is that it is computationally much slower than the

model-building approach. It is sometimes necessary to use an approxima-

tion such as equation (10.7) when using the historical simulation ap-

proach. This is because a full revaluation for each of the 500 different

scenarios is not possible.

12

The model-building approach is often used for investment portfolios.

(It is after all closely related to the popular Markowitz mean-variance

method of portfolio analysis.) It is less commonly used for calculating the

VaR for the trading operations of a financial institution. This is because,

as explained in Chapter 3, financial institutions like to maintain their

deltas with respect to market variables close to zero. Neither the linear

model nor the quadratic model work well when deltas are low and

portfolios are nonlinear.

SUMMARY

Whereas historical simulation lets the data determine the joint probability

distribution of daily percentage changes in market variables, the model-

building approach assumes a particular form for this distribution. The

most common assumption is that percentage changes in the variables have

a multivariate normal distribution. For situations where the change in the

value of the portfolio is linearly dependent on percentage changes in the

market variables, VaR can be calculated exactly in a straightforward way.

In other situations approximations are necessary. One approach is to use a

quadratic approximation for the change in the value of the portfolio as a

12

This is particularly likely to be the case if Monte Carlo simulation is the numerical

Procedure used by the financial institution to value a deal. Monte Carlo simulations

within historical simulations lead to extremely time-consuming computations.

252

Chapter 10

function of percentage changes in the market variables. Another (much

slower) approach is to use Monte Carlo simulation.

The model-building approach is frequently used for investment port-

folios. It is less popular for the trading portfolios of financial institutions

because it does not work well when deltas are low.

FURTHER READING

Frye, J., "Principals of Risk: Finding VAR through Factor-Based Interest Rate

Scenarios," in VAR: Understanding and Applying Value at Risk, pp. 275-288.

London: Risk Publications, 1997.

Hull, J.C., and A. White, "Value at Risk When Daily Changes in Market

Variables Are Not Normally Distributed," Journal of Derivatives, 5 (Spring

1998): 9-19.

Jamshidian, F., and Y. Zhu, "Scenario Simulation Model: Theory and

Methodology," Finance and Stochastics, 1 (1997): 43-67.

Rich, D., "Second Generation VaR and Risk-Adjusted Return on Capital,"

Journal of Derivatives, 10, No. 4 (Summer 2003): 51-61.

QUESTIONS AND PROBLEMS (Answers at End of Book)

10.1. Consider a position consisting of a $100,000 investment in asset A and a

$100,000 investment in asset B. Assume that the daily volatilities of both

assets are 1 % and that the coefficient of correlation between their returns

is 0.3. What is the 5-day 99% VaR for the portfolio?

10.2. Describe three ways of handling interest-rate-dependent instruments

when the model building approach is used to calculate VaR.

10.3. Explain how an interest rate swap is mapped into a portfolio of zero-

coupon bonds with standard maturities for the purposes of a VaR

calculation.

10.4. A financial institution owns a portfolio of options on the USD/GBP

exchange rate. The delta of the portfolio is 56.0. The current exchange

rate is 1.5000. Derive an approximate linear relationship between the

change in the portfolio value and the percentage change in the exchange

rate. If the daily volatility of the exchange rate is 0.7%, estimate the ten-

day 99% VaR.

10.5. Suppose you know that the gamma of the portfolio in Problem 10.4 is 16.2.

How does this change your estimate of the relationship between the change

in the portfolio value and the percentage change in the exchange rate?

VaR: Model-Building Approach

253

10.6. Suppose that the 5-year rate is 6%, the seven year rate is 7% (both

expressed with annual compounding), the daily volatility of a 5-year zero-

coupon bond is 0.5%, and the daily volatility of a 7-year zero-coupon

bond is 0.58%. The correlation between daily returns on the two bonds is

0.6. Map a cash flow of $1,000 received at time 6.5 years into a position

in a 5-year bond and a position in a 7-year bond. What cash flows in 5

and 7 years are equivalent to the 6.5-year cash flow?

10.7. Verify that the 0.3-year zero-coupon bond in the cash-flow-mapping

example in Table 10.2 is mapped into a $37,397 position in a 3-month

bond and a $11,793 position in a 6-month bond.

10.8. Suppose that the daily change in the value of a portfolio is, to a good

approximation, linearly dependent on two factors, calculated from a

principal components analysis. The delta of a portfolio with respect to

the first factor is 6 and the delta with respect to the second factor is -4.

The standard deviations of the factor are 20 and 8, respectively. What is

the 5-day 90% VaR?

10.9. The text calculates a VaR estimate for the example in Table 4.11

assuming two factors. How does the estimate change if you assume

(a) one factor and (b) three factors.

10.10. A bank has a portfolio of options on an asset. The delta of the options is

-30 and the gamma is -5. Explain how these numbers can be interpreted.

The asset price is 20 and its volatility is 1 % per day. Using the quadratic

model calculate the first three moments of the change in the portfolio

value. Calculate a 1-day 99% VaR using (a) the first two moments and

(b) the first three moments.

10.11. Suppose that in Problem 10.10 the vega of the portfolio is —2 per 1%

change in the annual volatility. Derive a model relating the change in the

portfolio value in 1 day to delta, gamma, and vega. Explain, without doing

detailed calculations, how you would use the model to estimate a VaR.

10.12. Explain why the linear model can provide only approximate estimates of

VaR for a portfolio containing options.

10.13. Some time ago a company entered into a forward contract to buy

£1 million for $1.5 million. The contract now has 6 months to maturity.

The daily volatility of a 6-month zero-coupon sterling bond (when

its price is translated to dollars) is 0.06% and the daily volatility of

a 6-month zero-coupon dollar bond is 0.05%. The correlation between

returns from the two bonds is 0.8. The current exchange rate is 1.53.

Calculate the standard deviation of the change in the dollar value of the

forward contract in 1 day. What is the 10-day 99% VaR? Assume that

the 6-month interest rate in both sterling and dollars is 5% per annum

with continuous compounding.

254

Chapter 1()

ASSIGNMENT QUESTIONS

10.14. Consider a position consisting of a $300,000 investment in gold and a

$500,000 investment in silver. Suppose that the daily volatilities of these

two assets are 1.8% and 1.2% respectively, and that the coefficient of

correlation between their returns is 0.6. What is the 10-day 97.5% VaR

for the portfolio? By how much does diversification reduce the VaR?

10.15. Consider a portfolio of options on a single asset. Suppose that the delta

of the portfolio is 12, the value of the asset is $10, and the daily volatility

of the asset is 2%. Estimate the 1-day 95% VaR for the portfolio from

the delta.

10.16. Suppose you know that the gamma of the portfolio in Problem 10.15 is

-2.6. Derive a quadratic relationship between the change in the portfolio

value and the percentage change in the underlying asset price in 1 day.

(a) Calculate the first three moments of the change in the portfolio value.

(b) Using the first two moments and assuming that the change in the

portfolio is normally distributed, calculate the 1-day 95% VaR for the

portfolio, (c) Use the third moment and the Cornish-Fisher expansion to

revise your answer to (b).

10.17. A company has a long position in a 2-year bond and a 3-year bond as

well as a short position in a 5-year bond. Each bond has a principal of

$100 and pays a 5% coupon annually. Calculate the company's exposure

to the 1-year, 2-year, 3-year, 4-year, and 5-year rates. Use the data in

Tables 4.8 and 4.9 to calculate a 20-day 95% VaR on the assumption that

rate changes are explained by (a) one factor, (b) two factors, and (c) three

factors. Assume that the zero-coupon yield curve is flat at 5%.

10.18. A company has a position in bonds worth $6 million. The modified

duration of the portfolio is 5.2 years. Assume that only parallel shifts

in the yield curve can take place and that the standard deviation of the

daily yield change (when yield is measured in percent) is 0.09. Use the

duration model to estimate the 20-day 90% VaR for the portfolio.

Explain carefully the weaknesses of this approach to calculating VaR

Explain two alternatives that give more accuracy.

10.19. A bank has written a call option on one stock and a put option on

another stock. For the first option the stock price is 50, the strike price is

51, the volatility is 28% per annum, and the time to maturity is 9 months.

For the second option the stock price is 20, the strike price is 19, the

volatility is 25% per annum, and the time to maturity is 1 year. Neither

stock pays a dividend, the risk-free rate is 6% per annum, and the

correlation between stock price returns is 0.4. Calculate a 10-day 99%

VaR (a) using only deltas, (b) using the partial simulation approach, and

(c) using the full simulation approach.

Credit Risk:

Estimating Default

Probabilities

This is the first of three chapters concerned with credit risk. Credit risk

arises from the possibility that borrowers, bond issuers, and counter-

parties in derivatives transactions may default. As explained in Chapter 7,

regulators have for a long time required banks to keep capital for credit

risk. In Basel II, banks can, with approval from bank supervisors, use

their own estimates of default probabilities to determine the amount of

capital they are required to keep. This has led banks to devote a lot of

resources to developing better ways of estimating default probabilities.

In this chapter we discuss a number of different approaches to estimating

default probabilities and explain the key difference between risk-neutral

and real-world estimates. The material we cover will be used in both

Chapters 12 and 13. In Chapter 12 we examine the nature of the credit

risk in over-the-counter derivatives transactions and discuss the calculation

of credit value at risk. In Chapter 13 we cover credit derivatives.

11.1 CREDIT RATINGS

Rating agencies such as Moody's and S&P are in the business of provid-

ing ratings describing the creditworthiness of corporate bonds. Using the

Moody's system, the best rating is Aaa. Bonds with this rating are

considered to have almost no chance of defaulting. The next best rating

is Aa. Following that comes A, Baa, Ba, B, and Caa. Only bonds with

256

Chapter \\

ratings of Baa or above are considered to be investment grade. The S&P

ratings corresponding to Moody's Aaa, Aa, A, Baa, Ba, B, and Caa are

AAA, AA, A, BBB, BB, B, and CCC, respectively. To create finer rating

measures, Moody's divides the Aa rating category into Aal, Aa2, and

Aa3; it divides A into Al, A2 and A3; and so on. Similarly S&P divides

its AA rating category into AA+, AA, and AA-; it divides its A rating

category into A+, A, and A-; and so on. (Only the Aaa category for

Moody's and the AAA category for S&P are not subdivided.)

A credit rating is designed to provide information about default

probabilities. As such one might expect frequent changes in a company's

credit rating as positive and negative information reaches the market.

1

In

fact, ratings change relatively infrequently. When rating agencies assign

ratings, one of their objectives is ratings stability. For example, they want

to avoid ratings reversals where a company is downgraded and then

upgraded a few weeks later. Ratings therefore change only when there

is reason to believe that a long-term change in the company's credit-

worthiness has taken place. The reason for this is that bond traders are

major users of ratings. Often they are subject to rules governing what the

credit ratings of the bonds they hold must be. If these ratings changed

frequently they might have to do a large amount of trading (and incur

high transactions costs) just to satisfy the rules.

A related point is that rating agencies try to "rate through the cycle".

Suppose that the economy exhibits a downturn and this has the effect of

increasing the probability of a company defaulting in the next six months,

but makes very little difference to the company's cumulative probability

of defaulting over the next three to five years. A rating agency would not

change the company's credit rating.

Internal Credit Ratings

Most banks have procedures for rating the creditworthiness of their

corporate and retail clients. This is a necessity. The ratings published

by rating agencies are only available for relatively large corporate clients-

Many small and medium-sized businesses do not issue publicly traded

bonds and therefore are not rated by rating agencies. As explained in

Chapter 7, the internal ratings based (IRB) approach in Basel II allows

banks to use their internal ratings in determining the probability of

1

In theory, a credit rating is an attribute of a bond issue, not a company. However, in

most cases all bonds issued by a company have the same rating. A rating is therefor

often referred to as an attribute of a company.

Credit Risk: Estimating Default Probabilities 257

default, PD. Under the advanced IRB approach, they are also allowed to

use their own internal procedures for estimating the loss given default,

LGD, the exposure at default, EAD, and the maturity, M.

Internal ratings based approaches for PD typically involve profitability

ratios, such as return on assets, and balance-sheet ratios, such as the

current ratio and the debt-to-equity ratio. Banks recognize that it is cash

rather than profits that is necessary to repay a loan. They typically take

the financial information provided by a company and convert it to the

type of cash-flow statement that allows them to estimate how easy it will

be for a company to service its debt.

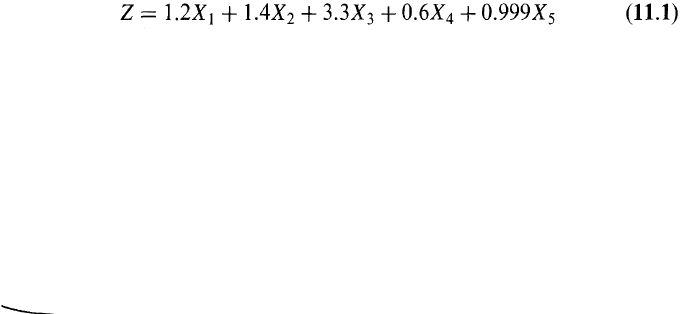

Altman's Z-Score

Edward Altman has pioneered the use of accounting ratios to predict

default. In 1968 he developed what has become known as the Z-score.

2

Using a statistical technique known as discriminant analysis, he attempted

to predict defaults from five accounting ratios:

X

1

: Working capital/Total Assets

X

2

: Retained earnings/Total assets

X

3

: Earnings before interest and taxes/Total assets

X

4

: Market value of equity/Book value of total liabilities

X

5

: Sales/Total assets

The Z-score was calculated as

If the Z-score is greater than 3.0, the company is unlikely to default. If it is

between 2.7 and 3.0, we should be "on alert". If it is between 1.8 and 2.7,

there is a good chance of default. If it is less than 1.8, the probability of a

financial embarrassment is very high. The Z-score was calculated from a

sample of 66 publicly traded manufacturing companies. Of these, 33 failed

within one year and 33 did not fail. The model proved very accurate when

tested on a sample of firms different from that used to obtain equation

(11.l). Both Type I errors (companies that were predicted not to go

bankrupt but did do so) and Type II errors (companies that were predicted

to go bankrupt, but did not do so) were small.

3

Variations on the model

2

See E.I. Altman, "Financial Ratios, Discriminant Analysis, and the Prediction of

Corporate Bankruptcy," Journal of Finance, 23, No. 4 (September 1968), 589-609.

Clearly Type I errors are much more costly to the lending department of a commercial

bank than Type II errors.

258

Chapter 11

have been developed for manufacturing companies that are not publicly

traded and nonmanufacturing companies.

Example 11.1

Consider a company for which working capital is 170,000, total assets are

670,000, earnings before interest and taxes is 60,000, sales are 2,200,000, the

market value of equity is 380,000, total liabilities is 240,000, and retained

earnings is 300,000. In this case X

1

= 0.254, X

2

= 0.448, X

3

= 0.0896,

X

4

= 1.583, and X

5

= 3.284. The Z-score is

1.2 x 0.254 + 1.4 x 0.448 + 3.3 x 0.0896 + 0.6 x 1.583 + 0.999 x 3.284 = 5.46

The Z-score indicates that the company is not in danger of defaulting in the

near future.

11.2 HISTORICAL DEFAULT PROBABILITIES

Table 11.1 is typical of the data that is produced by rating agencies. It

shows the default experience through time of companies that started with

a certain credit rating. For example, Table 11.1 shows that a bond issue

with an initial credit rating of Baa has a 0.20% chance of defaulting by

the end of the first year, a 0.57% chance of defaulting by the end of the

second year, and so on. The probability of a bond defaulting during a

particular year can be calculated from the table. For example, the

probability that a bond initially rated Baa will default during the second

year of its life is 0.57 - 0.20 = 0.37%.

Table 11.1 shows that, for investment-grade bonds, the probability of

default in a year tends to be an increasing function of time. (For example,

Rating

Aaa

Aa

A

Baa

Ba

B

Caa

1

0.00

0.02

0.02

0.20

1.26

6.21

23.65

Term (years)

2

0.00

0.03

0.09

0.57

3.48

13.76

37.20

3

0.00

0.06

0.23

1.03

6.00

20.65

48.02

4

0.04

0.15

0.38

1.62

8.59

26.66

55.56

5

0.12

0.24

0.54

2.16

11.17

31.99

60.83

7

0.29

0.43

0.91

3.24

15.44

40.79

69.36

10

0.62

0.68

1.59

5.10

21.01

50.02

77.91

15

1.21

1.51

2.94

9.12

30.88

59.21

80.23

20

1.55

2.70

5.24

12.59

38.56

60.73

80.23

Table 11.1 Average cumulative default rates (%), 1970-2003

(Source: Moody's).

Credit Risk: Estimating Default Probabilities 259

the probability of an A-rated bond defaulting during years 1, 2, 3, 4, and 5

are 0.02%, 0.07%, 0.14%, 0.15%, and 0.16%, respectively.) This is

because the bond issuer is initially considered to be creditworthy, and

the more time that elapses, the greater the possibility that its financial

health will decline. For bonds with a poor credit rating, the probability of

default is often a decreasing function of time. (For example, the probabil-

ities that a Caa-rated bond will default during years 1, 2, 3, 4, and 5 are

23.65%, 13.55%, 10.82%, 7.54%, and 5.27%, respectively.) The reason

here is that, for a bond with a poor credit rating, the next year or two may

be critical. If the issuer survives this period, its financial health is likely to

have improved.

Default Intensities

From Table 11.1 we can calculate the probability of a Caa bond default-

ing during the third year as 48.02 - 37.20 = 10.82%. We will refer to this

as the unconditional default probability. It is the probability of default

during the third year as seen at time zero. The probability that the Caa-

rated bond will survive until the end of year 2 is 100 - 37.20 = 62.80%.

The probability that it will default during the third year, conditional on

no earlier default, is therefore 0.1082/0.6280, or 17.23%.

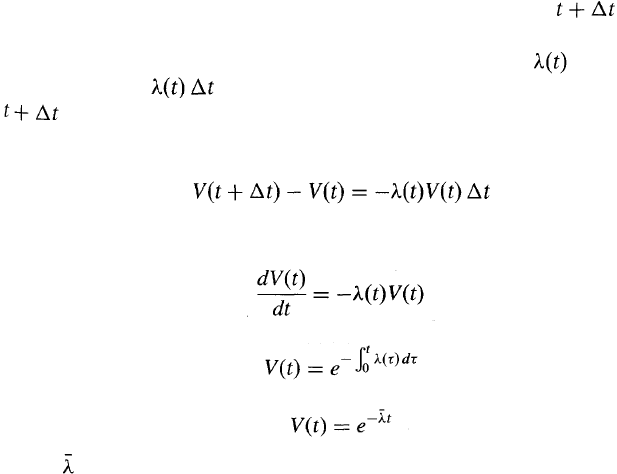

The 17.23% we have just calculated is for a one-year time period. By

considering the probability of default between times t and condi-

tional on no earlier default, we obtain what is known as the default

intensity or hazard rate at time t. The default intensity at time t is

defined so that is the probability of default between time t and

conditional on no default between time 0 and time t. If V(t) is the

cumulative probability of the company surviving to time t (i.e., no default

by time t), then

Taking limits, we obtain

from which we get

or

where is the average default intensity between time zero and time t.