Gerver R.K., Sgroi R.J. Financial Algebra

Подождите немного. Документ загружается.

194 Chapter 4 Consumer Credit

A charge card is a special type of credit card. It allows the card-

holder to make purchases in places that accept the card. The monthly

bill for all purchases must be paid in full. There is no interest charged.

Popular charge cards used today include Diner’s Club and certain types of

American Express cards. Most people informally use the words charge card

and credit card interchangeably.

Using credit cards is both a convenience and a responsibility.

There is a temptation to overspend, and the card also can be lost. The

Truth-in-Lending Act protects you if your card is lost or stolen. If this

happens, notify the creditor who issued the card immediately. You may

be partially responsible for charges made by unauthorized users of cards

you lose. The maximum liability is $50. You are not responsible for any

charges that occur after you notify the creditor.

If the card number, and not the actual card, is stolen, you are not

responsible for any purchases. It is the responsibility of the person selling

the merchandise to make sure the purchaser is actually the card owner.

Cardholders receive a monthly statement of their purchases, and any

payments they made to the creditor. The

Fair Credit Billing Act pro-

tects you if there are any errors in your monthly statement.

It is your responsibility to notify the creditor about the error. You do

not have to pay the amount that is disputed or any fi nance charge based

on that amount, until the problem is cleared up.

If you fi nd yourself unable to meet payments required by a creditor,

notify that creditor immediately. The

Fair Debt Collection Practices

Act

prohibits the creditor from harassing you or using unfair means

to collect the amount owed. As you can see, you need

to be knowledgeable to responsibly use credit and

charge cards.

Another type of plastic card is known as a debit card.

A

debit card is not a credit or charge card, because

there is no creditor extending credit. If you open a debit

account, you deposit money into your account, and the

debit card acts like an electronic check. You are deduct-

ing money directly from your account each time you

make a purchase using the debit card.

You cannot make purchases that exceed the bal-

ance in your debit card account. Keeping a record of

your debit card activity is exactly like keeping the

check register you learned about in Lesson 3-1. The

Electronic Funds Transfer Act protects debit card

users against unauthorized use of their cards. They

are not responsible for purchases made with a lost or

stolen card after the card is reported missing.

Most debit cards carry the Visa or MasterCard

logo and the holder can choose, at the time of a pur-

chase, if the purchase acts as a debit card purchase or

a credit card purchase. At some retailers, when you

use a debit card you are charged a fee, similar to the

fees charged at an ATM.

t

o

b

cha

A

d

t

h

a

c

d

e

i

n

m

a

y

c

E

u

© JASON STITT, 2009/USED UNDER LICENSE FROM SHUTTERSTOCK.COM

49657_04_ch04_p172-215.indd Sec2:19449657_04_ch04_p172-215.indd Sec2:194 12/24/09 12:23:03 AM12/24/09 12:23:03 AM

4-4 Credit Cards 195

Skills and Strategies

Revolving credit cards can have high interest rates, so it is important to

verify that the fi nance charge on your monthly statement is correct.

EXAMPLE 1

Frank lost his credit card in a local mall. He notifi ed his creditor before

the card was used. However, later in the day, someone found the card

and charged $700 worth of hockey equipment on it. How much is

Frank responsible for paying?

SOLUTION By the Truth in Lending Act, Frank is responsible for zero

dollars, because he reported it lost before it was used.

CHECK

■

YOUR UNDERSTANDING

Carrie’s credit card was stolen. She didn’t realize it for days, at which

point she notifi ed her creditor. During that time, someone charged

$2,000. How much is Carrie responsible for paying?

EXAMPLE 2

Credit card companies issue a monthly statement, therefore APR

(annual percentage rate) must be converted to a monthly percentage

rate. If the APR is 21.6%, what is the monthly interest rate?

SOLUTION To change to a monthly interest rate, divide the APR by 12.

21.6 ÷ 12 = 1.8

The monthly APR is 1.8%. This is the percent that will be used to com-

pute the monthly fi nance charge.

CHECK

■

YOUR UNDERSTANDING

If a monthly statement shows a monthly interest rate of x percent,

express the APR algebraically.

The average daily balance is the average of the amounts you owed

each day of the billing period. It changes due to purchases made and

payments made.

EXAMPLE 3

Rebecca did not pay last month’s credit card bill in full. Below a list of

Rebecca’s daily balances for her last billing cycle.

For seven days she owed $456.11.

For three days she owed $1,177.60.

For six days she owed $990.08.

For nine days she owed $2,115.15.

For fi ve days show owed $2,309.13.

Find Rebecca’s average daily balance.

49657_04_ch04_p172-215.indd Sec2:19549657_04_ch04_p172-215.indd Sec2:195 12/24/09 12:23:08 AM12/24/09 12:23:08 AM

196 Chapter 4 Consumer Credit

SOLUTION The average daily balance is an arithmetic average. The

arithmetic average is also called the

mean. To fi nd this average, you

add the balances for the entire billing period, and divide by the num-

ber of days.

Add the number of days in the list to fi nd the number of days in

the cycle.

7 + 3 + 6 + 9 + 5 = 30

There were 30 days in Rebecca’s billing cycle.

To fi nd the sum of the daily balances, multiply the number of days by

the amount owed. Then add these products.

7(456.11) = 3,192.77

3(1,177.60) = 3,532.80

6(990.08) = 5,940.48

9(2,115.15) = 19,036.35

5(2,309.13) = 11,545.65

Total 43,248.05

Divide the total by 30, and round to the nearest cent.

43,248.05 ÷ 30 ≈ 1,441.60

The average daily balance is $1,441.60.

CHECK

■

YOUR UNDERSTANDING

Last month, Paul had a daily balance of x dollars for 6 days, y dollars

for 12 days, w dollars for q days, and d dollars for 2 days. Express the

average daily balance algebraically.

Finance charges are not charged if, in the previous month, the revolv-

ing credit card bill was paid in full. If you pay your card in full every

month, you will never pay a fi nance charge.

EXAMPLE 4

Rebecca (from Example 3) pays a fi nance charge on her average daily

balance of $1,441.60. Her APR is 18%. What is her fi nance charge for

this billing cycle?

SOLUTION Finance charges are computed monthly, so the 18% APR

must be divided by 12 to get a monthly percentage rate of 1.5%. Take

1.5% of the average daily balance to get the fi nance charge.

Change 1.5% to an equivalent decimal, multiply, and round to the

nearest cent.

0.015(1,441.60) ≈ 21.62

The fi nance charge is $21.62.

CHECK

■

YOUR UNDERSTANDING

Steve owes a fi nance charge this month because he didn’t pay his bill

in full last month. His average daily balance is d dollars and his APR is

p percent. Express his fi nance charge algebraically.

49657_04_ch04_p172-215.indd Sec6:19649657_04_ch04_p172-215.indd Sec6:196 12/24/09 12:23:08 AM12/24/09 12:23:08 AM

4-4 Credit Cards 197

1. Interpret the quote in the context of what you learned.

2. Janine’s credit card was stolen, and the thief charged a $44 meal

using it before she reported it stolen. How much of this is Janine

responsible for paying?

3. Dan’s credit card was lost on a vacation. He immediately reported it

missing. The person who found it days later used it, and charged $x

worth of merchandise on the card, where x > $200. How much of

the $x is Dan responsible for paying?

4. Felix and Oscar applied for the same credit card from the same bank.

The bank checked both of their FICO scores. Felix had an excellent

credit rating, and Oscar had a poor credit rating.

a. Felix was given a card with an APR of 12%. What was his

monthly percentage rate?

b. Oscar was given a card with an APR of 15%. What was his

monthly payment?

c. If each of them had an average daily balance of $800 and had to

pay a fi nance charge, how much more would Oscar pay than Felix?

5. Vincent had these daily balances on his credit card for his last bill-

ing period. He did not pay the card in full the previous month, so he

will have to pay a fi nance charge. The APR is 19.2%.

nine days @ $778.12

eight days @ $1,876.00

four days @ $2,112.50

ten days @ $1,544.31

a. What is the average daily balance?

b. What is the fi nance charge?

6. Express the average daily balance algebraically given this set of daily

balances.

x days @ y dollars w days @ d dollars

r days @ q dollars m days @ p dollars

7. Suzanne’s average daily balance for last month was x dollars. The

fi nance charge was y dollars.

a. What was the monthly percentage rate?

b. What was the APR?

8. Jared’s average daily balance for last month was $560. The fi nance

charge was $8.12.

a. What was the monthly percentage rate?

b. What was the APR?

Life was a lot simpler when what we honored was father and

mother rather than all major credit cards.

Robert Orben, American Comedy Writer

Applications

49657_04_ch04_p172-215.indd Sec6:19749657_04_ch04_p172-215.indd Sec6:197 12/24/09 12:23:09 AM12/24/09 12:23:09 AM

198 Chapter 4 Consumer Credit

9. Helene’s credit card has an APR of 16.8%. She never pays her balance

in full, so she always pays a fi nance charge. Her next billing cycle

starts today. The billing period is 30 days. Today’s balance is $712.04.

She is only going to use the credit card this month to make a $5,000

down payment on a new car.

a. If she puts the down payment on the credit card today, what will

her daily balance be for each of the 30 days of the cycle?

b. Find her average daily balance for the 30-day period if she puts

the down payment on the credit card today.

c. Find the fi nance charge for this billing period based on the aver-

age daily balance from part a.

d. Find her average daily balance for the 30-day period if she puts the

down payment on the credit card on the last day of the billing

cycle.

e. Find the fi nance charge on the average daily balance from

part d.

f. How much can Helene save in fi nance charges if she makes the

down payment on the last day, as compared to making it on the

fi rst day?

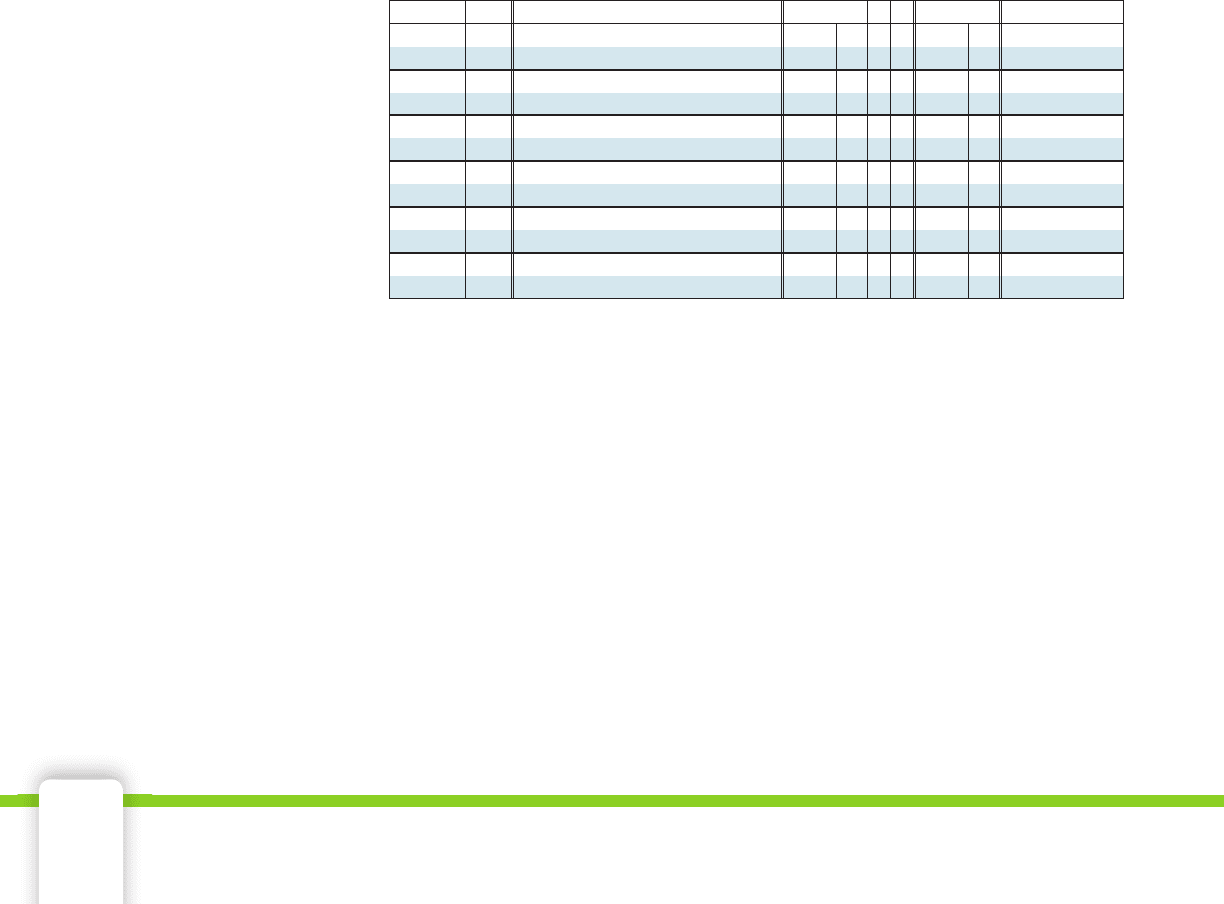

10. Gino has a debit card. The account pays no interest. He keeps track

of his purchases and deposits in this debit card register. Find the

missing entries a–f.

11. Ron did not pay his credit card bill in full last month. He wants to

pay it in full this month. On this month’s bill, there is a mistake in

the average daily balance. The credit card company lists the average

daily balance on his bill as $510.50. Ron computed it himself and

found that it is $410.50.

a. The APR is 18%. What fi nance charge did the credit card com-

pany compute on Ron’s bill?

b. If Ron’s average daily balance is correct, what should the fi nance

charge be?

12. The terms of Medina’s credit card state that the APR is 12.4%, and if

a payment is not received by the due date, the APR will increase by

w%. The credit card company received Medina’s payment three days

after the due date in February. Write the interest rate, in decimal

form that she will be charged in March, assuming she carried a bal-

ance from February.

CODE

NUMBER OR

DATE TRANSACTION DESCRIPTION

AMOUNT

PAYMENT

AMOUNT

DEPOSIT

$

$

BALANCE

8/4

8/5

8/7

8/7

8/7

Baseball Bat

Gas

Deposit

Gas

Dinner at Spooner’s

92 19

51 00

25 00

71 12

FEE

400 00

778.19

92.19

a.

51.00

b.

400.00

c.

25.00

d.

71.12

e.

On the Beach

8/11 Books for Fall Semester 491 51

491.51

f.

49657_04_ch04_p172-215.indd Sec6:19849657_04_ch04_p172-215.indd Sec6:198 12/24/09 12:23:09 AM12/24/09 12:23:09 AM

4-4 Credit Cards 199

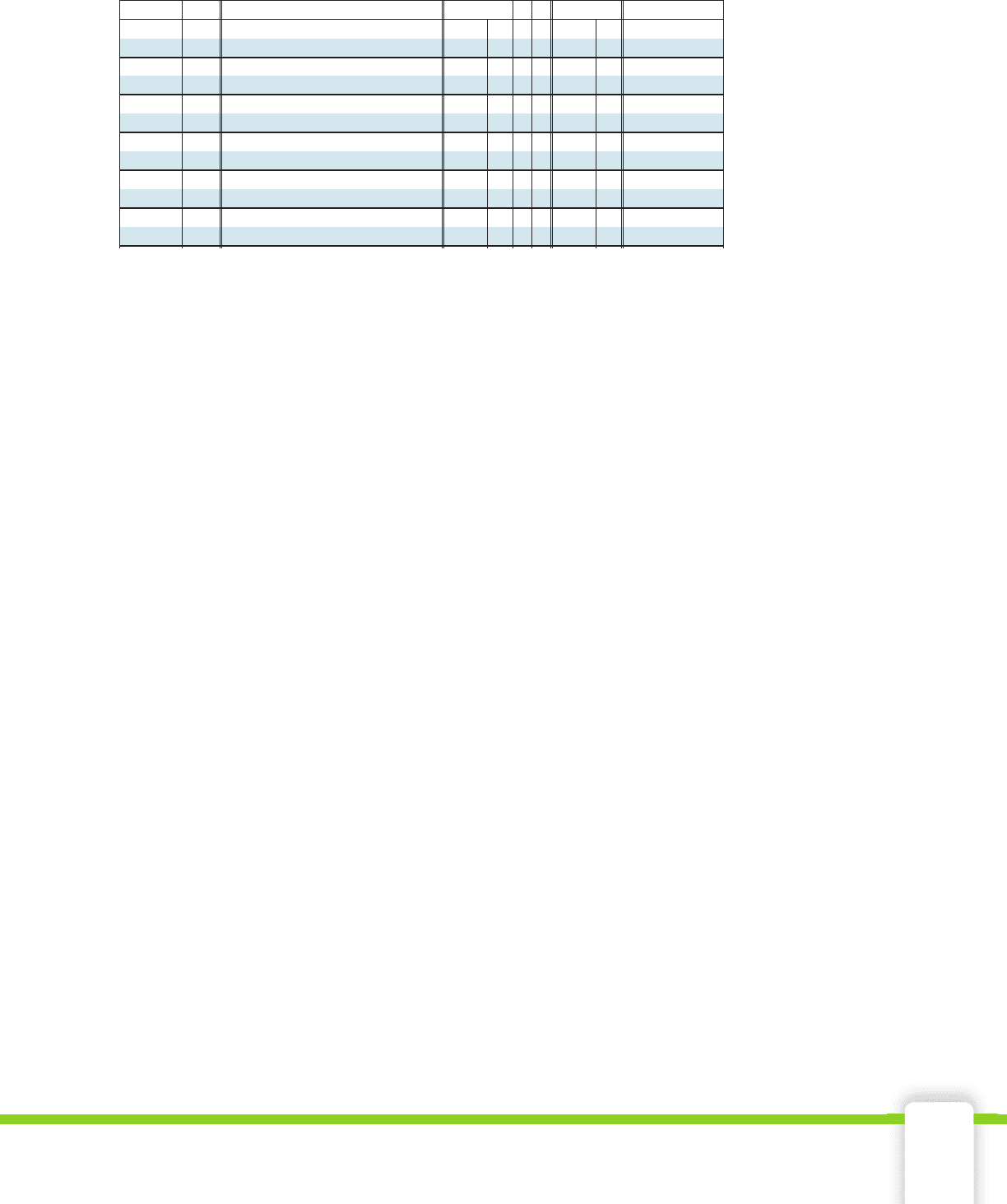

13. Express the missing entries in the debit card register algebraically.

14. Jill’s credit card was stolen. The thief charged a $900 kayak on the

card before she reported it stolen.

a. How much of the thief’s purchase is Jill responsible for?

b. Jill’s average daily balance would have been $1,240 without the

thief’s purchase. What was the sum of her daily balances for the

30-day billing period? Explain.

c. The thief’s purchase was on her daily balances for 10 out of the

30 days during the billing cycle. What was the sum of Jill’s daily

balances with the thief’s purchase included?

d. What was the average daily balance with the thief’s purchase

included?

15. Kristin’s credit rating was lowered, and the credit card company

raised her APR from 12% to 13.2%. If her average daily balance this

month is x dollars, express algebraically the increase in this month’s

fi nance charge due to the higher APR.

16. It is important to check your credit card bill each month. In the next

lesson, you will carefully examine a credit card statement and learn

how to look for errors. Most people would notice a major, expensive

purchase that they did not make. A smaller, incorrect charge of $6 for

example, might go unnoticed unless the entire statement was checked

with a calculator. If one million credit card holders were each over-

charged $6 each month for fi ve years, what would be the total amount

that debtors were overcharged, not including the extra fi nance charges?

17. Naoko has these daily balances on his credit card for September’s

billing period. He paid his balance from the August billing in full.

two days @ $99.78

fi fteen days @ $315.64

eleven days @ $515.64

two days @ $580.32

a. His APR is 15.4%. How much is the fi nance charge on his

September bill?

b. Does the credit card company need to calculate his average daily

balance? Explain.

c. Naoko calculated his average daily balance to be $377.85. Is he

correct? If not, what was his average daily balance?

d. What mistake did Naoko make when calculating this average

daily balance?

CODE

NUMBER OR

DATE TRANSACTION DESCRIPTION

AMOUNT

PAYMENT

AMOUNT

DEPOSIT

$

$

BALANCE

12/3

12/6

12/7

12/11

12/12

Arloff’s Gifts

Bonnie’s Boutique

Gas

Cable TV

x

y

v

FEE

a.

b.

c.

d.

r

e.

12/14 Gas g

f.

Deposit

z

m

49657_04_ch04_p172-215.indd Sec6:19949657_04_ch04_p172-215.indd Sec6:199 12/24/09 12:23:10 AM12/24/09 12:23:10 AM

200 Chapter 4 Consumer Credit

Objectives

To identify and use •

the various entries

in a credit card

statement.

debit/credit•

previous balance•

payments/credits•

new purchases•

late charge•

fi nance charge•

new balance•

minimum •

payment

Key Terms

billing cycle•

credit card •

statement

account number•

credit line•

available credit•

billing date•

payment due date•

transactions •

Credit Card Statement

4-5

Credit card companies pay college students generously to

stand outside dining halls, dorms, and academic buildings and

encourage their fellow students to apply for credit cards.

Louise Slaughter, American Congresswoman

What information does a credit

card statement give you?

Credit cards can be used when making purchases in person, by mail, by

phone, online, and more. In most situations you get a receipt for each

transaction, but it can be diffi cult to keep track of the transactions over a

billing cycle.

A

billing cycle is a predetermined amount of time set by the credit

card company that is used for calculating your credit card bill. This cycle

can be adjusted by the company based upon your credit worthiness. For

example, a college student with little or no track record of being able

to keep up credit card payments may initially be given a 21-day billing

cycle. A seasoned credit card holder who has proven to be fi nancially

responsible might get a longer billing cycle.

At the end of every cycle, the credit card company takes an account-

ing of your credits and debits and sends you that information in the

form of a

credit card statement. You should read the statement

carefully and verify the charges. All credit card companies have a pro-

cess through which the credit card holder can dispute errors on the

statement.

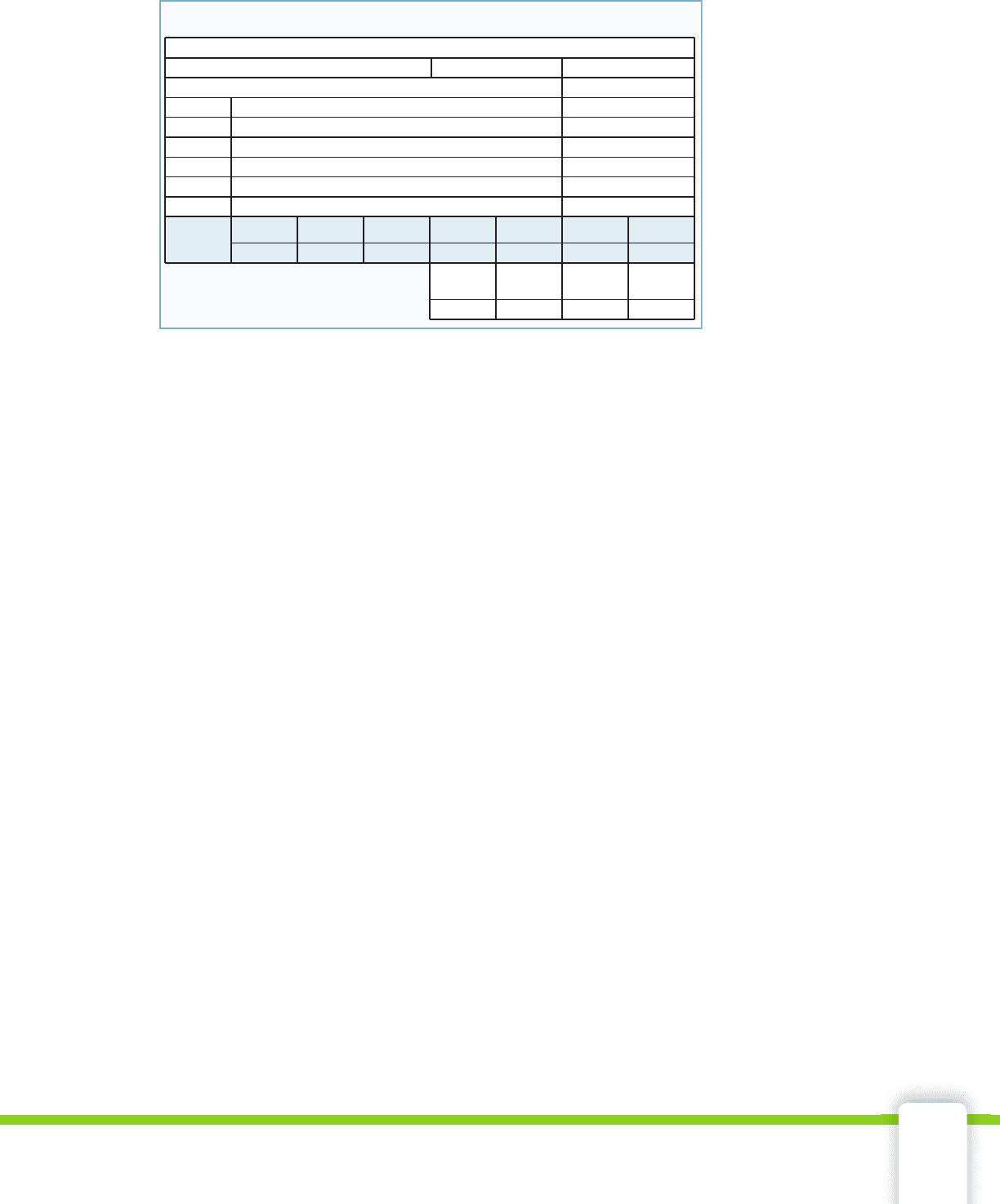

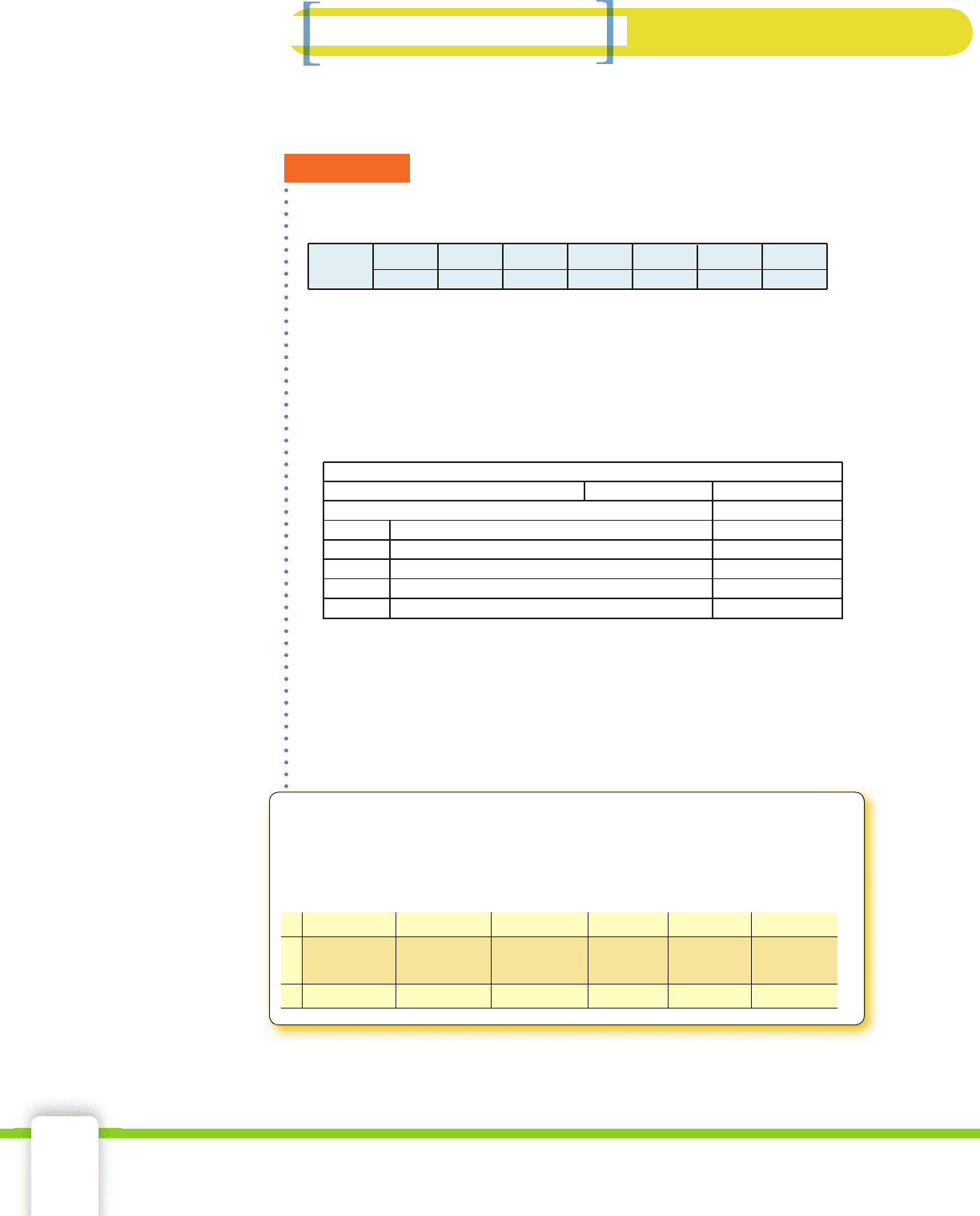

Jane Sharp has a FlashCard revolving credit card. At the end of a

30-day cycle, Jane receives her FlashCard statement listing all of her pur-

chases and the payments the company has received during that 30-day

cycle. Jane’s credit card statement is shown on the next page.

average daily •

balance

number of days •

in billing cycle

APR•

monthly •

periodic rate

49657_04_ch04_p172-215.indd Sec6:20049657_04_ch04_p172-215.indd Sec6:200 12/24/09 12:23:10 AM12/24/09 12:23:10 AM

4-5 Credit Card Statement 201

Locate each of the terms explained below on Jane’s statement.

Account Number• Each credit card account has a unique number.

Credit Line• The maximum amount you can owe at any time.

Available Credit• The difference between the maximum amount

you can owe and the actual amount you owe.

Billing Date• The date the bill (statement) was written.

Payment Due Date• On this date the monthly payment must be

received by the creditor.

Transactions • Lists where purchases were made and the date. Some

companies use the date posted, which indicates when the creditor

received its notifi cation of the charge and processed it. Some compa-

nies list the date of transaction, which shows when purchases were

made or payments were received. Some companies list both the

posted and the transaction dates.

Debits/Credits• A debit is the amount charged to your account.

A credit is a payment made to reduce your debt. Credits are identi-

fi ed by a negative (−) sign.

Previous Balance• Any money owed before current billing period.

Payments/Credits• Total amount received by the creditor.

New Purchases• The sum of purchases (debits) on the current bill.

Late Charge• The penalty for late payments from a previous month.

Finance Charge• The cost of using the credit card for the current

billing period.

New Balance• The amount you currently owe.

Minimum Payment• This amount is the lowest payment the credit

card company will accept for the current billing period.

Average Daily Balance• The average amount owed per day

during the billing cycle.

Number of Days in Billing Cycle• The amount of time, in days,

covered by the current bill.

APR• The yearly interest rate.

Monthly Periodic Rate• The APR divided by 12.

Previous

SUMMARY

$150.50

Balance

Payments

/ Credits

New

Late

Charge

Finance

Charge

New

Balance

Minimum

Payment

$75.00 $284.45 $0.00 $3.53 $363.48 $20.00

TRANSACTIONS

2 Jan Candida’s Gift Shop

3 Jan Skizza’s Pizzas

DEBITS / CREDITS (⫺)

$75.00

$31.85

5 Jan Beekman Department Store

10 Jan Festival Book Store

$139.10

$38.50

21 Jan Payment ⫺$75.00

Average

Daily

# Days

in Billing APR

Monthly

Periodic

Balance Cycle Rate

$235.10 30 18% 1.5%

ACCOUNT INFORMATION

Account Number 2653 8987 6098 Billing Date 23 Jan Payment Due 2 Feb

Total Credit Line

Total Available Credit

$ 8,000.00

$ 7,636.52

Jane Sharp 25 Main Street

Sunrise, NY

Purchases

49657_04_ch04_p172-215.indd Sec6:20149657_04_ch04_p172-215.indd Sec6:201 12/24/09 12:23:11 AM12/24/09 12:23:11 AM

202 Chapter 4 Consumer Credit

Here you will learn how to read and verify entries on a credit card

statement.

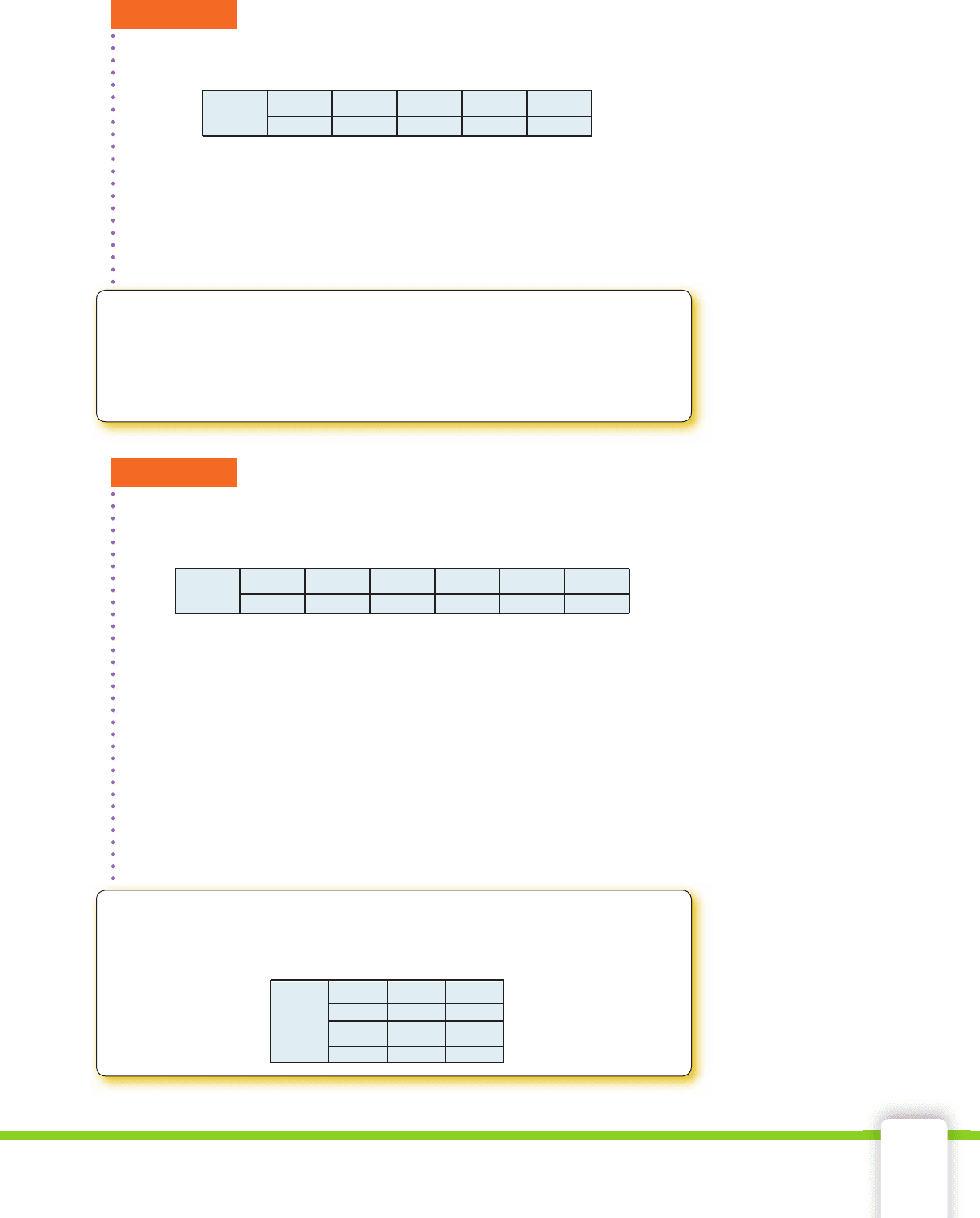

EXAMPLE 1

The summary portion of Jane Sharp’s credit card statement shown on

the previous page looks as follows:

a. Explain how the new purchases amount was determined.

b. Explain how the new balance amount was determined.

SOLUTION

a. The new purchases amount is the sum of the purchases that

appear as debits. This sum must equal the amount $284.45 listed

in the New Purchases section of the statement summary.

New purchases = 75 + 31.85 + 139.10 + 38.50 = 284.45

b. The new balance amount is determined by using the formula given

below.

Previous − Payments + New + Finance + Late = New

Balance Purchases Charge Charge Balance

150.50 − 75 + 284.45 + 3.53 + 0 = 363.48

CHECK

■

YOUR UNDERSTANDING

Suppose you create the following spreadsheet that models the state-

ment summary and input the values in row 2. Write the spreadsheet

formula to compute the new balance in cell F2.

ABCDEF

1

Previous

Balance Payments

New

Purchases

Late

Charge

Finance

Charge

New

Balance

2

Previous

SUMMARY

$150.50

Balance

Payments

/ Credits

Late

Charge

Finance

Charge

New

Balance

Minimum

Payment

$75.00 $284.45 $0.00 $3.53 $363.48 $20.00

New

Purchases

TRANSACTIONS

2 Jan Candida’s Gift Shop

3 Jan Skizza’s Pizzas

DEBITS / CREDITS (⫺)

$75.00

$31.85

5 Jan Beekman Department Store

10 Jan Festival Book Store

$139.10

$38.50

21 Jan Payment ⫺$75.00

ACCOUNT INFORMATION

Account Number 2653 8987 6098 Billing Date 23 Jan Payment Due 2 Feb

Skills and Strategies

49657_04_ch04_p172-215.indd Sec6:20249657_04_ch04_p172-215.indd Sec6:202 12/24/09 12:23:11 AM12/24/09 12:23:11 AM

4-5 Credit Card Statement 203

EXAMPLE 2

Pascual has a credit line of $15,000 on his credit card. His summary

looks as follows. How much available credit does Pascual have?

SOLUTION Pascual needs to determine his new balance and then sub-

tract that from his credit line in order to fi nd his available credit.

4,598.12 − 4,000.00 + 1,368.55 + 20.00 + 5.78 = $1,992.45

He has a new balance of $1,992.45. Subtracting this from his credit

line of $15,000 leaves him with an available credit of $13,007.55.

CHECK

■

YOUR UNDERSTANDING

Rhonda had a previous balance of $567.91 and made an on-time

credit card payment of $567.91. She has a credit line of x dollars and

made purchases totaling y dollars. Write an algebraic expression that

represents her current available credit.

EXAMPLE 3

Myrna is examining the summary section of her credit card statement.

Myrna has checked all the entries on her bill and agrees with every-

thing except the new balance. Determine where the error was made.

SOLUTION Add the amounts that show money Myrna must pay to

the credit card company.

$1,748.00

previous balance

800.00 purchases

9.15 fi nance charge

+ 19.00 late charge

$2,576.15 total to be paid

Subtract the $100 payment, and Myrna’s new balance will be

$2,476.16. It appears that Myrna was not credited for her payment.

Under the Fair Credit Billing Act, Myrna must notify her creditor in

writing within 60 days from the statement date on her bill.

CHECK

■

YOUR UNDERSTANDING

Determine the error that was made using the following summary

statement.

Previous

SUMMARY

$4,598.12

Balance

Payments

/ Credits

Late

Charge

Finance

Charge

$4,000.00 $1,368.55 $20.00 $5.78

New

Purchases

Previous

SUMMARY

$1,748.00

Balance

Payments

/ Credits

Late

Charge

Finance

Charge

New

Balance

$100.00 $800.00 $9.15 $19.00 $2,576.15

New

Purchases

Previous

SUMMARY

$850.00

Balance

Payments

/ Credits

Late

Charge

Finance

Charge

New

Balance

$300.00

$3.00 $4.78

$504.78

New

Purchases

$560.00

49657_04_ch04_p172-215.indd Sec5:20349657_04_ch04_p172-215.indd Sec5:203 12/24/09 12:23:11 AM12/24/09 12:23:11 AM