Dougherty С. Introduction to Econometrics, 3Ed

Подождите немного. Документ загружается.

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

2

)(Var

),(Cov

)(Var

),(Cov

22

X

uX

X

YX

b

+==

β

(9.2)

Now, if X is nonstochastic, so is Var(X), and the expected value of the error term can be written

E[Cov(X, u)]/Var(X). Furthermore, if X is nonstochastic, E[Cov(X, u)] is 0. Hence we have no trouble

proving that b

2

is an unbiased estimator of

β

2

. Although a proof was not supplied, the nonstochasticity

assumption was also used in deriving the expression for the population variance of the coefficient.

Fortunately, the desirable properties of the OLS estimators remain unchanged even if the

explanatory variables have stochastic components, provided that these components are distributed

independently of the disturbance term, and provided that their distributions do not depend on the

parameters

β

1

,

β

2

, or

σ

u

. We will demonstrate the unbiasedness and consistency properties and as

usual take efficiency on trust.

Unbiasedness

If X is stochastic, Var(X) cannot be treated as a scalar, so we cannot rewrite E[Cov(X,u)/Var(X)] as

E[Cov(X, u)]/Var(X). Hence the previous proof of unbiasedness is blocked. However, we can find

another route by decomposing the error term:

∑

∑

∑

=

=

=

−=

−

−

=

−−

=

n

i

ii

n

i

i

i

n

i

ii

uuXf

n

uu

X

XX

n

X

uuXX

n

X

uX

1

1

1

))((

1

)(

)(Var

)

1

)(Var

))((

1

)(Var

),(Cov

(9.3)

where

)(Var/)()( XXXXf

ii

−=

. Now, if X and u are independently distributed,

)])(([ uuXfE

ii

−

may be decomposed as the product of

)]([

i

xfE

and

)( uuE

i

−

(see the definition of independence in

the Review). Hence

0)]([)()]([)])(([

×=−=−

iiiii

XfEuuEXfEuuXfE

(9.4)

since E(u

i

) is 0 in each observation, by assumption. (This implies, of course, that E(

u

) is also 0).

Hence, when we take the expectation of

∑

=

−

n

i

ii

uuXf

n

1

))((

1

, each term within the summation has

expected value 0. Thus the error term as a whole has expected value 0 and b

2

is an unbiased estimator

of

β

2

.

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

3

Consistency

We know that, in general, plim (A/B) is equal to plim(A)/plim(B), where A and B are any two

stochastic quantities, provided that both plim(A) and plim(B) exist and that plim(B) is nonzero (see the

Review; "plim" simply means "the limiting value as the sample size becomes large"). We also know

that sample expressions tend to their population counterparts as the sample size becomes large, so plim

Cov(X, u) is the population covariance of X and u and plim Var(X) is

2

X

σ

, the population variance of

X. If X and u are independent, the population covariance of X and u is 0 and hence

2

2

222

0

)(Var plim

),(Cov plim

plim

β

σ

β

β

=+=+=

X

X

uX

b (9.5)

9.2 The Consequences of Measurement Errors

It frequently happens in economics that, when you are investigating a relationship, the variables

involved have been measured defectively. For example, surveys often contain errors caused by the

person being interviewed not remembering properly or not understanding the question correctly.

However, misreporting is not the only source of inaccuracy. It sometimes happens that you have

defined a variable in your model in a certain way, but the available data correspond to a slightly

different definition. Friedman's critique of the conventional consumption function, discussed in

Section 9.3, is a famous case of this.

Measurement Errors in the Explanatory Variable(s)

Let us suppose that a variable Y depends on a variable Z according to the relationship

Y

i

=

β

1

+

β

2

Z

i

+ v

i

(9.6)

where v is a disturbance term with mean 0 and variance

2

v

σ

, distributed independently of Z. We shall

suppose that Z cannot be measured absolutely accurately, and we shall use X to denote its measured

value. In observation i, X

i

is equal to the true value, Z

i

, plus the measurement error, w

i

:

X

i

= Z

i

+ w

i

(9.7)

We shall suppose that w has mean 0 and variance

2

w

σ

, that Z has population variance

2

Z

σ

, and that w is

distributed independently of Z and v.

Substituting from (9.7) into (9.6), we obtain

Y

i

=

β

1

+

β

2

(

X

i

– w

i

) + v

i

=

β

1

+

β

2

X

i

+ v

i

–

β

2

w

i

(9.8)

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

4

This equation has two random components, the original disturbance term v and the measurement error

(multiplied by –

β

2

). Together they form a composite disturbance term, which we shall call u:

u

i

= v

i

–

β

2

w

i

(9.9)

(9.8) may then be written

Y

i

=

β

1

+

β

2

X

i

+ u

i

(9.10)

You have your data on Y (which, for the time being, we shall assume has been measured accurately)

and X, and you unsuspectingly regress Y on X.

As usual, the regression coefficient b is given by

)(Var

),(Cov

)(Var

),(Cov

22

X

uX

X

YX

b

+==

β

. (9.11)

Looking at the error term, we can see that it is going to behave badly. By virtue of (9.7) and (9.9),

both X

i

and u

i

depend on w

i

. The population covariance between X and u is nonzero and so b

2

is an

inconsistent estimator of

β

2

. Even if you had a very large sample, your estimate would be inaccurate.

In the limit it would underestimate

β

2

by an amount

2

22

2

β

σσ

σ

wZ

w

+

. (9.12)

A proof of this is given below. First we will note its implications, which are fairly obvious. The

bigger the population variance of the measurement error, relative to the population variance of Z, the

bigger will be the bias. For example, if

2

w

σ

were equal to 0.25

2

Z

σ

, the bias would be

2

2

2

25.1

25.0

β

σ

σ

Z

Z

−

(9.13)

which is –0.2

β

2

. Even if the sample were very large, your estimate would tend to be 20 percent below

the true value if

β

2

were positive, 20 percent above it if

β

2

were negative.

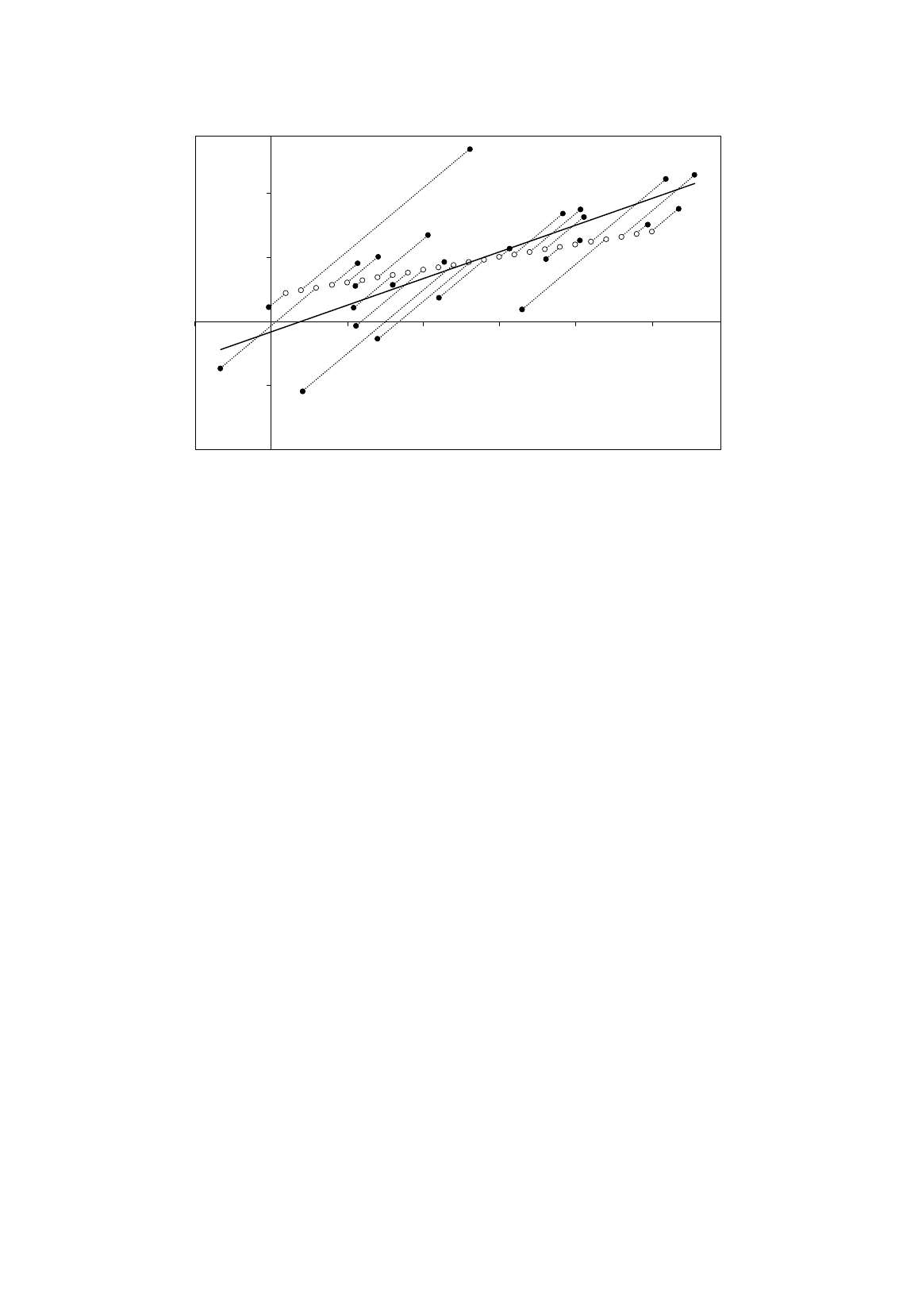

Figure 9.1 illustrates how measurement errors give rise to biased regression coefficients, using the

model represented by (9.6) and (9.7). The circles represent the observations on Z and Y, the values of Y

being generated by a process of type (9.6), the true relationship being given by the dashed line. The

solid markers represent the observations on X and Y, the measurement error in each case causing a

horizontal shift marked by a dotted line. Positive measurement errors tend to cause the observations to

lie under the true relationship, and negative ones tend to cause the observations to lie above it. This

causes the scatter of observations on X and Y to look flatter than that for Z and Y and the best-fitting

regression line will tend to underestimate the slope of the true relationship. The greater the variance of

the measurement error relative to that of Z, the greater will be the flattening effect and the worse the

bias.

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

5

Figure 9.1.

Effect of errors of measurement of the explanatory variable

Imperfect Proxy Variables

In Chapter 7 it was shown that, if we are unable to obtain data on one of the explanatory variables in a

regression model and we run the regression without it, the coefficients of the other variables will in

general be biased and their standard errors will be invalid. However, in Section 7.4 we saw that if we

are able to find a perfect proxy for the missing variable, that is, another variable that has an exact

linear relationship with it, and use that in its place in the regression, most of the regression results will

be saved. Thus, the coefficients of the other variables will not be biased, their standard errors and

associated t tests will be valid, and R

2

will be the same as if we had been able to include the

unmeasurable variable directly. We will not be able to obtain an estimate of the coefficient of the

latter, but the t statistic for the proxy variable will be the same as the t statistic for the unmeasurable

variable.

Unfortunately, it is unusual to find a perfect proxy. Generally the best that you can hope for is a

proxy that is approximately linearly related to the missing variable. The consequences of using an

imperfect proxy instead of a perfect one are parallel to those of using a variable subject to

measurement error instead of one that is free from it. It will cause the regression coefficients to be

biased, the standard errors to be invalid, and so on, after all.

You may nevertheless justify the use of a proxy if you have reason to believe that the degree of

imperfection is not so great as to cause the bias to be serious and the standard errors to be misleading.

Since there is normally no way of testing whether the degree of imperfection is great or small, the case

for using a proxy has to be made on subjective grounds in the context of the model.

Y

X, Z

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

6

Proof of the Inconsistency Expression

Since X and u are not distributed independently of each other, there is no simple way of summarizing

the behavior of the term Cov(X, u)/Var(X) in small samples. We cannot even obtain an expression for

its expected value. Rewriting it as (9.3) does not help because

)])(([ uuXfE

ii

−

cannot be

decomposed as

)]()]([ uuEXfE

ii

−

. The most we can do is to predict how it would behave if the

sample were very large. It will tend to plim Cov(X, u) divided by plim Var(X). We will look at these

separately.

Using the definitions of X and u, the sample variance between them may be decomposed as

follows:

Cov(X, u)= Cov[(Z + w), (v –

β

2

w)]

= Cov(Z, v) + Cov(w, v) – Cov(Z,

β

2

w) – Cov(w,

β

2

w) (9.14)

using the covariance rules. In large samples, sample variances tend towards their population

counterparts. Since we have assumed that v and w are distributed independently of each other and Z,

the population covariances of v and w, Z and v, and Z and

β

2

w are all 0. This leaves us with the

population covariance of w and

β

2

w, which is

2

2

w

σ

β

. Hence

plim Cov(X, u) =

2

2

w

σ

β

−

(9.15)

Now for plim Var(X). Since X is equal to (Z + w),

plim Var(X) = plim Var(Z + w)

= plim Var(Z) + plim Var(w) + 2 plim Cov(Z, w)

=

2

Z

σ

+

2

w

σ

. (9.16)

The sample variances tend to their population counterparts and the sample covariance tends to 0 if Z

and w are distributed independently. Thus

22

2

2

22

OLS

2

)(Var plim

),(Cov plim

+= plim

wZ

w

X

uX

b

σσ

σ

β

β

β

+

−=

(9.17)

Note that we have assumed that w is distributed independently of v and Z. The first assumption is

usually plausible because in general there is no reason for any measurement error in an explanatory

variable to be correlated with the disturbance term. However, we may have to relax the second

assumption. If we do,

OLS

2

b

remains inconsistent, but the expression for the bias becomes more

complex. See Exercise 9.4.

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

7

Measurement Errors in the Dependent Variable

Measurement errors in the dependent variable do not matter as much. In practice they can be thought

of as contributing to the disturbance term. They are undesirable, because anything that increases the

noise in the model will tend to make the regression estimates less accurate, but they will not cause the

regression estimates to be biased.

Let the true value of the dependent variable be Q, and the true relationship be

Q

i

=

β

1

+

β

2

X

i

+ v

i

, (9.18)

where v is a disturbance term. If Y

i

is the measured value of the dependent variable in observation i,

and r

i

is the measurement error,

Y

i

= Q

i

+ r

i

. (9.19)

Hence the relationship between the observed value of the dependent variable and X is given by

Y

i

– r

i

=

β

1

+

β

2

X

i

+ v

i

, (9.20)

which may be rewritten

Y

i

=

β

1

+

β

2

X

i

+ u

i

, (9.21)

where u is the composite disturbance term (v + r).

The only difference from the usual model is that the disturbance term in (9.21) has two

components: the original disturbance term and the error in measuring Y. The important thing is that

the explanatory variable X has not been affected. Hence OLS still yields unbiased estimates provided

that X is nonstochastic or that it is distributed independently of v and r. The population variance of the

slope coefficient will be given by

2

22

2

2

2

2

X

rv

X

u

b

nn

σ

σσ

σ

σ

σ

+

==

(9.20)

and so will be greater than it would have been in the absence of measurement error, reducing the

precision of the estimator. The standard errors remain valid but will be larger than they would have

been in the absence of the measurement error, reflecting the loss of precision.

Exercises

9.1

In a certain industry, firms relate their stocks of finished goods, Y, to their expected annual

sales, X

e

, according to a linear relationship

Y =

β

1

+

β

2

X

e

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

8

Actual sales, X, differ from expected sales by a random quantity u, that is distributed with mean

0 and constant variance:

X = X

e

+ u

u is distributed independently of X

e

. An investigator has data on Y and X (but not on X

e

) for a

cross-section of firms in the industry. Describe the problems that would be encountered if OLS

were used to estimate

β

1

and

β

2

, regressing Y on X.

9.2

In a similar industry, firms relate their intended stocks of finished goods, Y

*

, to their expected

annual sales, X

e

, according to a linear relationship

Y

*

=

β

1

+

β

2

X

e

Actual sales, X, differ from expected sales by a random quantity u, which is distributed with

mean 0 and constant variance:

X = X

e

+ u

u is distributed independently of X

e

. Since unexpected sales lead to a reduction in stocks, actual

stocks are given by

Y = Y

*

– u

An investigator has data on Y and X (but not on Y

*

or X

e

) for a cross-section of firms in the

industry. Describe analytically the problems that would be encountered if OLS were used to

estimate

β

1

and

β

2

, regressing Y on X. [Note: You are warned that the standard expression for

measurement error bias is not valid in this case.]

9.3*

A variable Q is determined by the model

Q =

β

1

+

β

2

X + v,

where X is a variable and v is a disturbance term that satisfies the Gauss–Markov conditions.

The dependent variable is subject to measurement error and is measured as Y where

Y = Q + r

and r is the measurement error, distributed independently of v. Describe analytically the

consequences of using OLS to fit this model if

(1) The expected value of r is not equal to 0 (but r is distributed independently of Q),

(2) r is not distributed independently of Q (but its expected value is 0).

9.4*

A variable Y is determined by the model

Y =

β

1

+

β

2

Z + v,

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

9

where Z is a variable and v is a disturbance term that satisfies the Gauss–Markov conditions.

The explanatory variable is subject to measurement error and is measured as X where

X = Z + w

and w is the measurement error, distributed independently of v. Describe analytically the

consequences of using OLS to fit this model if

(1) The expected value of w is not equal to 0 (but w is distributed independently of Z),

(2) w is not distributed independently of Z (but its expected value is 0).

9.5*

A researcher investigating the shadow economy using international cross-section data for 25

countries hypothesizes that consumer expenditure on shadow goods and services, Q, is related

to total consumer expenditure, Z, by the relationship

Q =

β

1

+

β

2

Z + v

where v is a disturbance term that satisfies the Gauss–Markov conditions. Q is part of Z and any

error in the estimation of Q affects the estimate of Z by the same amount. Hence

Y

i

= Q

i

+ w

i

and

X

i

= Z

i

+ w

i

where Y

i

is the estimated value of Q

i

, X

i

is the estimated value of Z

i

, and w

i

is the measurement

error affecting both variables in observation i. It is assumed that the expected value of w is 0

and that v and w are distributed independently of Z and of each other.

(1) Derive an expression for the large-sample bias in the estimate of

β

2

when OLS is used to

regress Y on X, and determine its sign if this is possible. [Note: You are warned that the

standard expression for measurement error bias is not valid in this case.]

(2) In a Monte Carlo experiment based on the model above, the true relationship between Q

and Z is

Q = 2.0 + 0.2Z

Sample b

1

s.e.(b

1

) b

2

s.e.(b

2

) R

2

1 –0.85 1.09 0.42 0.07 0.61

2 –0.37 1.45 0.36 0.10 0.36

3 –2.85 0.88 0.49 0.06 0.75

4 –2.21 1.59 0.54 0.10 0.57

5 –1.08 1.43 0.47 0.09 0.55

6 –1.32 1.39 0.51 0.08 0.64

7 –3.12 1.12 0.54 0.07 0.71

8 –0.64 0.95 0.45 0.06 0.74

9 0.57 0.89 0.38 0.05 0.69

10 –0.54 1.26 0.40 0.08 0.50

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

10

A sample of 25 observations is generated using the integers 1, 2, ..., 25 as data for Z . The

variance of Z is 52.0. A normally-distributed random variable with mean 0 and variance 25

is used to generate the values of the measurement error in the dependent and explanatory

variables. The results with 10 samples are summarized in the table. Comment on the

results, stating whether or not they support your theoretical analysis.

(3) The graph shows plots the points (Q, Z) and (Y, X) for the first sample, with each (Q, Z)

point linked to the corresponding (Y, X) point. Comment on this graph, given your answers

to parts (1) and (2).

9.3 Friedman's Critique of the Conventional Consumption Function

Now we come to the most celebrated application of measurement error analysis in the whole of

economic theory: Friedman's critique of the use of OLS to fit a consumption function (Friedman,

1957). We discuss here Friedman's analysis of the problem and in Section 12.3 we will discuss his

solution.

In Friedman's model, the consumption of individual (or household) i is related, not to actual

(measured) current income Y

i

, but to permanent income, which will be denoted Y

i

P

. Permanent income

is to be thought of as a medium-term notion of income: the amount that the individual can more or less

depend on for the foreseeable future, taking into account possible fluctuations. It is subjectively

determined by recent experience and by expectations about the future, and because it is subjective it

cannot be measured directly. Actual income at any moment may be higher or lower than permanent

income depending on the influence of short-run random factors. The difference between actual and

permanent income caused by these factors is described as transitory income, Y

i

T

. Thus

Y

i

= Y

i

P

+ Y

i

T

. (9.23)

-10

-5

0

5

10

-5 0 5 10 15 20 25

Z

, X

Q

,

Y

STOCHASTIC REGRESSORS AND MEASUREMENT ERRORS

11

In the same way, Friedman makes a distinction between actual consumption, C

i

, and permanent

consumption, C

i

P

. Permanent consumption is the level of consumption justified by the level of

permanent income. Actual consumption may differ from it as special, unforeseen circumstances arise

(unanticipated medical bills, for example) or as a consequence of impulse purchases. The difference

between actual and permanent consumption is described as transitory consumption, C

i

T

. Thus

C

i

= C

i

P

+ C

i

T

. (9.24)

Y

i

T

and C

i

T

are assumed to be random variables with mean 0 and constant variance, uncorrelated with

Y

i

P

and C

i

P

and each other. Friedman further hypothesizes that permanent consumption is directly

proportional to permanent income:

C

i

P

=

β

2

Y

i

P

(9.25)

If the Friedman model is correct, what happens if you ignorantly try to fit the usual simple

consumption function, relating measured consumption to measured income? Well, both the dependent

and the explanatory variables in the regression

i

C

ˆ

= b

1

+ b

2

Y

i

(9.26)

have been measured inappropriately, C

i

T

and Y

i

T

being the measurement errors. In terms of the

previous section,

Z

i

= Y

i

P

, w

i

= Y

i

T

, Q

i

= C

i

P

, r

i

= C

i

T

(9.27)

As we saw in that section, the only effect of the measurement error in the dependent variable is to

increase the variance of the disturbance term. The use of the wrong income concept is more serious.

It causes the estimate of

β

to be inconsistent. From (9.11), we can see that in large samples

2

22

2

22

plim

β

σσ

σ

β

TP

T

YY

Y

b

+

−=

(9.28)

where

2

T

Y

σ

is the population variance of Y

T

and

2

P

Y

σ

is the population variance of Y

P

. It implies that,

even in large samples, the apparent marginal propensity to consume (your estimate b

2

) will be lower

than the value of

β

2

in the true relationship (9.25). The size of the bias depends on the ratio of the

variance of transitory income to that of permanent income. It will be highest for those occupations

whose earnings are most subject to fluctuations. An obvious example is farming. Friedman's model

predicts that, even if farmers have the same

β

2

as the rest of the population, an OLS estimate of their

marginal propensity to consume will be relatively low, and this is consistent with the facts (Friedman,

1957, pp. 57 ff.).