Dougherty С. Introduction to Econometrics, 3Ed

Подождите немного. Документ загружается.

HETEROSCEDASTICITY

9

Exercises

8.1

The table gives data on government recurrent expenditure, G, investment, I, gross domestic

product, Y, and population, P, for 30 countries in 1997 (source: 1999 International Monetary

Fund Yearbook). G, I¸and Y are measured in U.S.$ billion and P in million. A researcher

investigating whether government expenditure tends to crowd out investment fits the regression

(standard errors in parentheses):

I

ˆ

= 18.10 –1.07G + 0.36YR

2

= 0.99

(7.79) (0.14) (0.02)

She sorts the observations by increasing size of Y and runs the regression again for the 11

countries with smallest Y and the 11 countries with largest Y. RSS for these regressions is 321

and 28101, respectively. Perform a Goldfeld–Quandt test for heteroscedasticity.

Country I G Y P Country I G Y P

Australia

94.5 75.5 407.9 18.5

Netherlands

73.0 49.9 360.5 15.6

Austria

46.0 39.2 206.0 8.1

New Zealand

12.9 9.9 65.1 3.8

Canada

119.3 125.1 631.2 30.3

Norway

35.3 30.9 153.4 4.4

Czech Republic

16.0 10.5 52.0 10.3

Philippines

20.1 10.7 82.2 78.5

Denmark

34.2 42.9 169.3 5.3

Poland

28.7 23.4 135.6 38.7

Finland

20.2 25.0 121.5 5.1

Portugal

25.6 19.9 102.1 9.8

France

255.9 347.2 1409.2 58.6

Russia

84.7 94.0 436.0 147.1

Germany

422.5 406.7 2102.7 82.1

Singapore

35.6 9.0 95.9 3.7

Greece

24.0 17.7 119.9 10.5

Spain

109.5 86.0 532.0 39.3

Iceland

1.4 1.5 7.5 0.3

Sweden

31.2 58.8 227.8 8.9

Ireland

14.3 10.1 73.2 3.7

Switzerland

50.2 38.7 256.0 7.1

Italy

190.8 189.7 1145.4 57.5

Thailand

48.1 15.0 153.9 60.6

Japan

1105.9 376.3 3901.3 126.1

Turkey

50.2 23.3 189.1 62.5

Korea

154.9 49.3 442.5 46.0

U.K.

210.1 230.7 1256.0 58.2

Malaysia

41.6 10.8 97.3 21.0

U.S.A.

1517.7 1244.1 8110.9 267.9

8.2

Fit an earnings function using your EAEF data set, taking EARNINGS as the dependent variable

and S, ASVABC, and MALE as the explanatory variables, and perform a Goldfeld–Quandt test

for heteroscedasticity in the S dimension. (Remember to sort the observations by S first.)

8.3

*

The following regressions were fitted using the Shanghai school cost data introduced in Section

6.1 (standard errors in parentheses):

STOC

ˆ

= 24,000 + 339NR

2

= 0.39

(27,000) (50)

STOC

ˆ

= 51,000 – 4,000OCC + 152N + 284NOCC R

2

= 0.68.

(31,000) (41,000) (60) (76)

where COST is the annual cost of running a school, N is the number of students, OCC is a

dummy variable defined to be 0 for regular schools and 1 for occupational schools, and NOCC

HETEROSCEDASTICITY

10

is a slope dummy variable defined as the product of N and OCC. There are 74 schools in the

sample. With the data sorted by N, the regressions are fitted again for the 26 smallest and 26

largest schools, the residual sum of squares being as shown in the table.

26 smallest 26 largest

First regression 7.8

×

10

10

54.4

×

10

10

Second regression

6.7

×

10

10

13.8

×

10

10

Perform a Goldfeld–Quandt test for heteroscedasticity for the two models and, with reference to

Figure 6.5, explain why the problem of heteroscedasticity is less severe in the second model.

8.4*

The file educ.dta in the heteroscedastic data sets folder on the website contains international

cross-section data on aggregate expenditure on education, EDUC, gross domestic product,

GDP, and population, POP, for a sample of 38 countries in 1997. EDUC and GDP are

measured in U.S. $ million and POP is measured in thousands. Download the data set, plot a

scatter diagram of EDUC on GDP, and comment on whether the data set appears to be subject

to heteroscedasticity. Sort the data set by GDP and perform a Goldfeld–Quandt test for

heteroscedasticity, running regressions using the subsamples of 14 countries with the smallest

and greatest GDP.

8.3 What Can You Do about Heteroscedasticity?

Suppose that the true relationship is

Y

i

=

β

1

+

β

2

X

i

+ u

i

(8.6)

Let the standard deviation of the disturbance term in observation i be

i

u

σ

. If you happened to know

i

u

σ

for each observation, you could eliminate the heteroscedasticity by dividing each observation by

its value of

σ

. The model becomes

iiii

u

i

u

i

uu

i

uXY

σσ

β

σ

β

σ

++=

21

1

(8.7)

The disturbance term u

i

/

i

u

σ

is homoscedastic because the population variance of

i

i

u

σ

is

1

1

)(

1

2

2

2

2

2

===

i

ii

i

u

u

i

u

u

i

uE

u

E

σ

σσ

σ

(8.8)

Therefore, every observation will have a disturbance term drawn from a distribution with population

variance 1, and the model will be homoscedastic. The revised model may be rewritten

HETEROSCEDASTICITY

11

Y

i

' =

β

1

h

i

+

β

2

X

i

' + u

i

', (8.9)

where Y

i

' = Y

i

/

i

u

σ

, X

i

' = X

i

/

i

u

σ

, h

is a new variable whose value in observation i is 1/

i

u

σ

, and u

i

' =

u

i

/

i

u

σ

. Note that there should not be a constant term in the equation. By regressing Y

' on h and X

',

you will obtain efficient estimates of

β

1

and

β

2

with unbiased standard errors.

A mathematical demonstration that the revised model will yield more efficient estimates than the

original one is beyond the scope of this text, but it is easy to give an intuitive explanation. Those

observations with the smallest values of

i

u

σ

will be the most useful for locating the true relationship

between Y and X because they will tend to have the smallest disturbance terms. We are taking

advantage of this fact by performing what is sometimes called a weighted regression. The fact that

observation i is given weight 1/

i

u

σ

automatically means that the better its quality, the greater the

weight that it receives.

The snag with this procedure is that it is most unlikely that you will know the actual values of the

i

u

σ

. However, if you can think of something that is proportional to it in each observation, and divide

the equation by that, this will work just as well.

Suppose that you can think of such a variable, which we shall call Z, and it is reasonable to

suppose that

i

u

σ

is proportional to Z

i

:

i

u

σ

=

λ

Z

i

. (8.10)

for some constant,

λ

. If we divide the original equation through by Z, we have

i

i

i

i

ii

i

Z

u

Z

X

ZZ

Y

++=

21

1

β

β

(8.11)

The model is now homoscedastic because the population variance of

i

i

Z

u

is

2

2

22

2

2

2

2

2

1

)(

1

λ

λ

σ

====

i

i

u

i

i

i

i

i

Z

Z

Z

uE

Z

Z

u

E

i

(8.12)

We do not need to know the value of

λ

, and indeed in general will not know it. It is enough that it

should be constant for all observations.

In particular, it may be reasonable to suppose that

i

u

σ

is roughly proportional to X

i

, as in the

Goldfeld–Quandt test. If you then divide each observation by its value of X, the model becomes

i

i

ii

i

X

u

XX

Y

++=

21

1

β

β

, (8.13)

HETEROSCEDASTICITY

12

and, with a little bit of luck, the new disturbance term u

i

/X

i

will have constant variance. You now

regress Y/X on 1/X, including a constant term in the regression. The coefficient of 1/X will be an

efficient estimate of

β

1

and the constant will be an efficient estimate of

β

2

. In the case of the

manufacturing output example in the previous section, the dependent variable would be manufacturing

output as a proportion of GDP, and the explanatory variable would be the reciprocal of GDP.

Sometimes there may be more than one variable that might be used for scaling the equation. In

the case of the manufacturing output example, an alternative candidate would be the size of the

population of the country, POP. Dividing the original model through by POP, one obtains

i

i

i

i

ii

i

POP

u

POP

X

POPPOP

Y

++=

21

1

β

β

, (8.14)

and again one hopes that the disturbance term, u

i

/POP

i

, will have constant variance across

observations. Thus now one is regressing manufacturing output per capita on GDP per capita and the

reciprocal of the size of the population, this time without a constant term.

In practice it may be a good idea to try several variables for scaling the observations and to

compare the results. If the results are roughly similar each time, and tests fail to reject the null

hypothesis of homoscedasticity, your problem should be at an end.

Examples

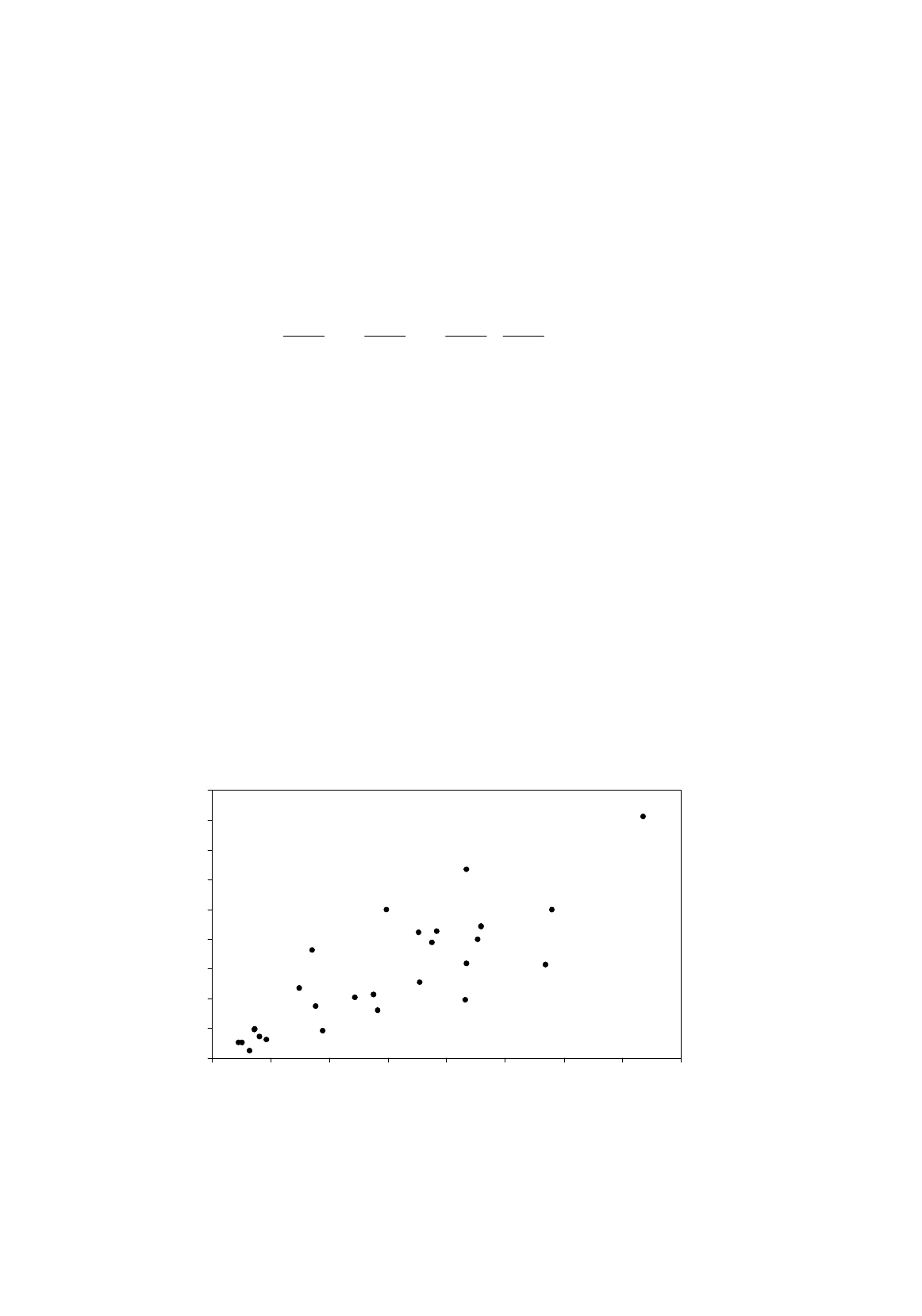

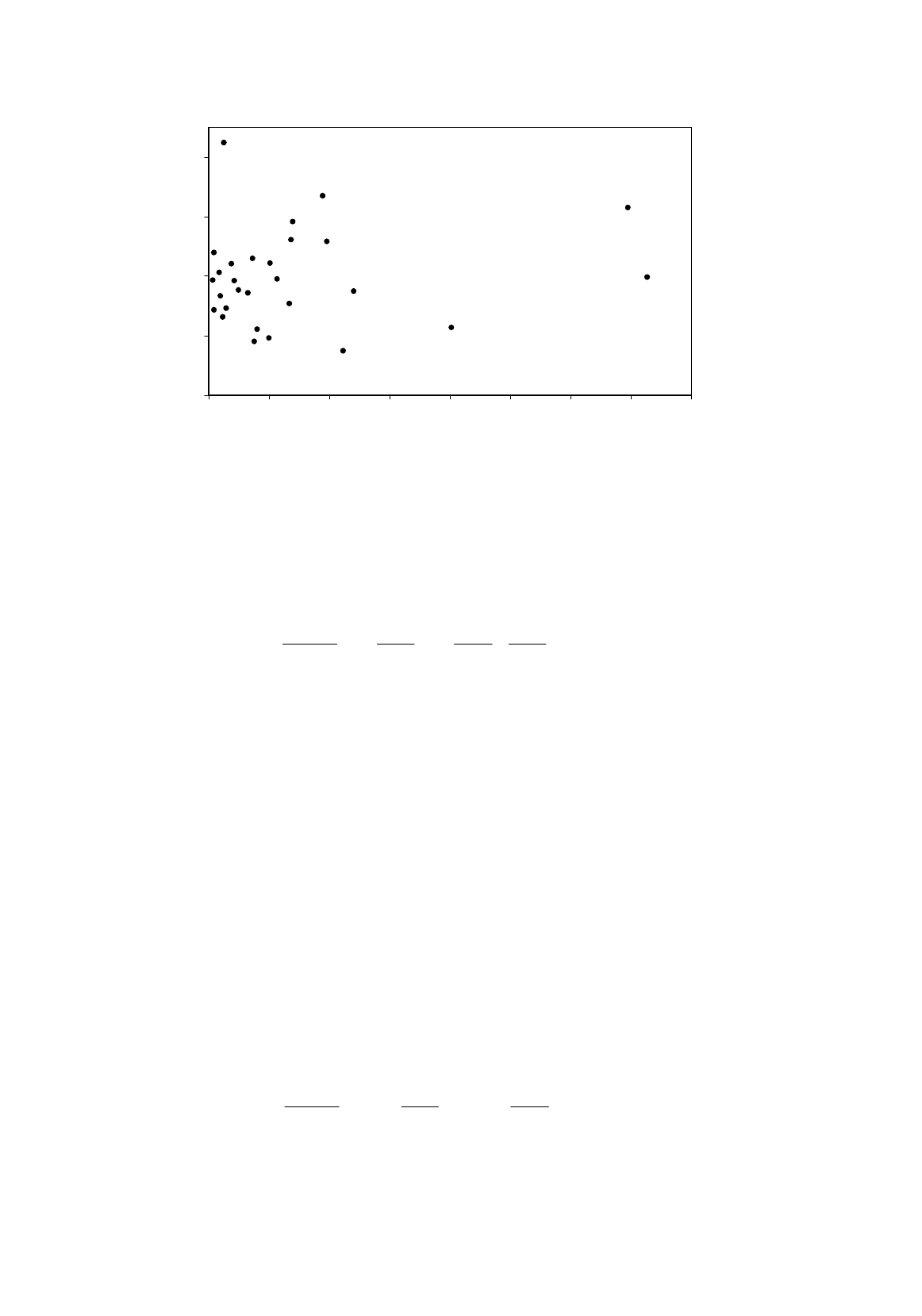

In the previous section it was found that a linear regression of MANU on GDP using the data in Table

8.1 and the model

MANU =

β

1

+

β

2

GDP + u (8.15)

Figure 8.5.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

0 5000 10000 15000 20000 25000 30000 35000 40000

GDP per capita

Manufacturing output per capita

HETEROSCEDASTICITY

13

Figure 8.6.

was subject to severe heteroscedasticity. One possible remedy might be to scale the observations by

population, the model becoming

POP

u

POP

GDP

POPPOP

MANU

++=

21

1

β

β

, (8.16)

Figure 8.5 provides a plot of MANU/POP on GDP/POP. Despite scaling, the plot still looks

heteroscedastic. When (8.16) is fitted using the 11 countries with smallest GDP per capita and the 11

countries with the greatest, the residual sums of squares are 5,378,000 and 17,362,000. The ratio, and

hence the F statistic, is 3.23. If the subsamples are small, it is possible to obtain high ratios under the

null hypothesis of homoscedasticity. In this case, the null hypothesis is just rejected at the 5 percent

level, the critical value of F(9, 9) being 3.18.

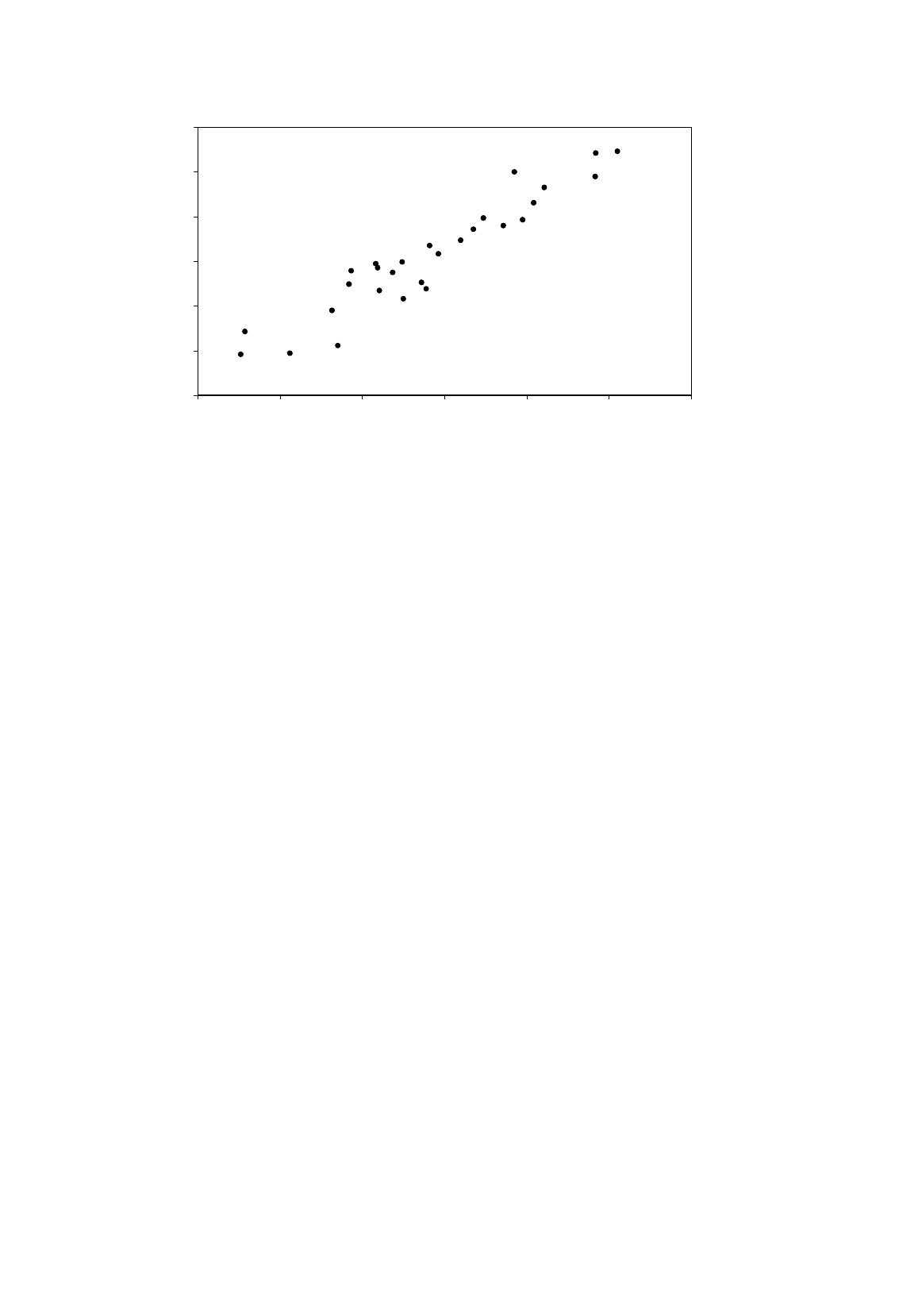

Figure 8.6 shows the result of scaling through by GDP itself, manufacturing as a share of GDP

being plotted against the reciprocal of GDP. In this case the residual sums of squares for the

subsamples are 0.065 and 0.070, and so finally we have a model where the null hypothesis of

homoscedasticity is not rejected.

We will compare the regression results for the unscaled model and the two scaled models,

summarized in equations (8.17) – (8.19) (standard errors in parentheses):

NUAM

ˆ

= 604 + 0.194 GDP R

2

= 0.89 (8.17)

(5,700) (0.013)

POP

NU

A

M

= 612

POP

1

+ 0.182

POP

GDP

R

2

= 0.70 (8.18)

(1,370) (0.016)

0.00

0.10

0.20

0.30

0.40

0 1020304050607080

1/GDP x 1,000,000

Manufacturing/GDP

HETEROSCEDASTICITY

14

GDP

NU

A

M

= 0.189 + 533

GDP

1

R

2

= 0.02 (8.19)

(0.019) (841)

First, note that the estimate of the coefficient of GDP is much the same in the three regressions:

0.194, 0.182, and 0.189 (remember that it becomes the intercept when scaling through by the X

variable). One would not expect dramatic shifts since heteroscedasticity does not give rise to bias.

The estimator in the third estimate should have the smallest variance and therefore ought to have a

tendency to be the most accurate. Perhaps surprisingly, its standard error is the largest, but then the

standard errors in the first two regressions should be disregarded because they are invalidated by the

heteroscedasticity.

In this model the intercept does not have any sensible economic interpretation. In any case its

estimate in the third equation, where it has become the coefficient of 1/GDP, is not significantly

different from 0. The only apparent problem with the third model is that R

2

is very low. We will

return to this in the next subsection.

Nonlinear Models

Heteroscedasticity, or perhaps apparent heteroscedascity, may be a consequence of misspecifying the

model mathematically. Suppose that the true model is nonlinear, for example

vXY

2

1

β

β

=

(8.20)

with (for sake of argument)

β

1

and

β

2

positive so that Y is an increasing function of X. The

multiplicative disturbance term v has the effect of increasing or reducing Y by a random proportion.

Suppose that the probability distribution of v is the same for all observations. This implies, for

example, that the probability of a 5 percent increase or decrease in Y due to its effects is just the same

when X is small as when X is large. However, in absolute terms a 5 percent increase has a larger effect

on Y when X is large than when X is small. If Y is plotted against X, the scatter of observations will

therefore tend to be more widely dispersed about the true relationship as X increases, and a linear

regression of Y on X may therefore exhibit heteroscedasticity.

The solution, of course, is to run a logarithmic regression instead:

log Y = log

β

1

+

β

2

log X + log v (8.21)

Not only would this be a more appropriate mathematical specification, but it makes the regression

model homoscedastic. log v now affects the dependent variable, log Y, additively, so the absolute size

of its effect is independent of the magnitude of log X.

Figure 8.7 shows the logarithm of manufacturing output plotted against the logarithm of GDP

using the data in Table 8.1. At first sight at least, the plot does not appear to exhibit

heteroscedasticity. Logarithmic regressions using the subsamples of 11 countries with smallest and

greatest GDP yield residual sums of squares 2.14 and 1.04, respectively. In this case the conventional

Goldfeld–Quandt test is superfluous. Since the second RSS is smaller than the first, it cannot be

significantly greater. However the Goldfeld–Quandt test can also be used to test for

heteroscedasticity where the standard deviation of the distribution of the disturbance term is inversely

HETEROSCEDASTICITY

15

Figure 8.7.

proportional to the size of the X variable. The F statistic is the same, with RSS

1

and RSS

2

interchanged. In the present case the F statistic if 2.06, which is lower than the critical value of F at

the 5 percent level, and we do not reject the null hypothesis of homoscedasticity. Running the

regression with the complete sample, we obtain (standard errors in parentheses):

ANUM

ˆ

log = –1.694 + 0.999 log GDP R

2

= 0.90 (8.22)

(0.785)

(0.066)

implying that the elasticity of MANU with respect to GDP is equal to 1.

We now have two models free from heteroscedasticity, (8.19) and (8.22). The latter might seem

more satisfactory, given that it has a very high R

2

and (8.19) a very low one, but in fact, in this

particular case, they happen to be equivalent. (8.22) is telling us that manufacturing output increases

proportionally with GDP in the cross-section of countries in the sample. In other words,

manufacturing output accounts for a constant proportion of GDP. To work out this proportion, we

rewrite the equation as

999.099.0694.1

184.0

ˆ

GDPGDPeNUAM

==

−

(8.23)

(8.19) is telling us that the ratio MANU/GDP is effectively a constant, since the 1/GDP term appears to

be redundant, and that the constant is 0.189. Hence in substance the interpretations coincide.

White’s Heteroscedasticity-Consistent Standard Errors

It can be shown that the population variance of the slope coefficient in a simple OLS regression with a

heteroscedastic disturbance term is given by

7

8

9

10

11

12

13

9 101112131415

lo

g

GDP

log Manufacturing output

HETEROSCEDASTICITY

16

)(Var

1

2

2

OLS

2

Xn

w

n

i

ui

b

i

∑

=

=

σ

σ

(8.24)

where

2

i

u

σ

is the variance of the disturbance term in observation i and w

i

, its weight in the numerator, is

given by

∑

=

−

−

=

n

j

j

i

i

XX

XX

w

1

2

2

)(

)(

(8.25)

White (1980) demonstrated that a consistent estimator of

2

OLS

2

b

σ

is obtained if the squared residual in

observation i is used as an estimator of

2

i

u

σ

. Thus in a situation where heteroscedasticity is suspected,

but there is not enough information to identify its nature, it is possible to overcome the problem of

biased standard errors, at least in large samples, and the t tests and F tests are asymptotically valid.

Two points, need to be kept in mind, however. One is that, although the White estimator is consistent,

it may not perform well in finite samples (MacKinnon and White, 1985). The other is that the OLS

estimators remain inefficient.

How Serious Are the Consequences of Heteroscedasticity?

This will depend on the nature of the heteroscedasticity and there are no general rules. In the case of

the heteroscedasticity depicted in Figure 8.3, where the standard deviation of the disturbance term is

proportional to X and the values of X are the integers from 5 to 44, the population variance of the OLS

estimator of the slope coefficient is approximately double that of the estimator using equation (8.13),

where the heteroscedasticity has been eliminated by dividing through by X. Further, the standard

errors of the OLS estimators are underestimated, giving a misleading impression of the precision of

the OLS coefficients.

Exercises

8.5

The researcher mentioned in Exercise 8.1 runs the following regressions as alternative

specifications of her model (standard errors in parentheses):

P

I

ˆ

= –0.03

P

1

– 0.69

P

G

+ 0.34

P

Y

R

2

= 0.97 (1)

(0.28) (0.16) (0.03)

Y

I

ˆ

= 0.39 + 0.03

Y

1

– 0.93

Y

G

R

2

= 0.78 (2)

(0.04) (0.42) (0.22)

HETEROSCEDASTICITY

17

Ig

ˆ

lo

= –2.44 – 0.63 log G + 1.60 log YR

2

= 0.98 (3)

(0.26) (0.12) (0.12)

She sorts the sample by Y/P, G/Y, and log Y, respectively, and in each case runs the regression

again for the subsamples of of observations with the 11 smallest and 11 greatest values of the

sorting variable. The residual sums of squares are as shown in the table:

11 smallest 11 largest

(1) 1.43 12.63

(2) 0.0223 0.0155

(3) 0.573 0.155

Perform a Goldfeld–Quandt test for each model specification and discuss the merits of each

specification. Is there evidence that investment is an inverse function of government

expenditure?

8.6

Using your EAEF data set, r

epeat Exercise 8.2 with LGEARN as the dependent variable. Is

there evidence that this is a preferable specification?

8.7*

Repeat Exercise 8.4, using the Goldfeld–Quandt test to investigate whether scaling by

population or by GDP, or whether running the regression in logarithmic form, would eliminate

the heteroscedasticity. Compare the results of regressions using the entire sample and the

alternative specifications.

C. Dougherty 2001. All rights reserved. Copies may be made for personal use. Version of 06.05.01.

9

STOCHASTIC REGRESSORS AND

MEASUREMENT ERRORS

In the basic least squares regression model, it is assumed that the explanatory variables are

nonstochastic. This is typically an unrealistic assumption, and it is important to know the

consequences of relaxing it. We shall see that in some contexts we can continue to use OLS, but in

others, for example when one or more explanatory variables are subject to measurement error, it is a

biased and inconsistent estimator. The chapter ends by introducing an alternative technique,

instrumental variables estimation, that may have more desirable properties.

9.1 Stochastic Regressors

So far we have assumed that the regressors – the explanatory variables – in the regression model are

nonstochastic. This means that they do not have random components and that their values in the

sample are fixed and unaffected by the way the sample is generated. Perhaps the best example of a

nonstochastic variable is time, which, as we will see when we come to time series analysis, is

sometimes included in the regression model as a proxy for variables that are difficult to measure, such

as technical progress or changes in tastes. Nonstochastic explanatory variables are actually unusual in

regression analysis. In the

EAEF

data sets provided for practical work, there are similar numbers of

individuals with different amounts of schooling, but the numbers do vary from sample to sample and

hence when an earnings function is fitted it has to be conceded that the schooling variable has a

random component. However, if stratified random sampling has been used to generate a sample, then

the variable that has been used for stratification may be nonstochastic. For example, the sex variable

in the

EAEF

data sets is nonstochastic because by construction each sample has exactly 325 males and

245 females. But such examples are relatively uncommon and nearly always confined to dummy

variables.

The reason for making the nonstochasticity assumption has been the technical one of simplifying

the analysis of the properties of the regression estimators. For example, we saw that in the regression

model

Y

=

β

1

+

β

2

X

+

u

, (9.1)

the OLS estimator of the slope coefficient may be decomposed as follows: