Citibank: basic of corporate finance

Подождите немного. Документ загружается.

1-24 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

Income Statement

There are two accounts in the Income Statement that represent

sources of cash. The first, NET INCOME BEFORE PREFERRED DIVIDEND, is

the cash generated by the sale of the product or services that the

company has available for discretionary expenditures. We are

assuming that the costs and expenses related to production, interest,

and taxes are all non-discretionary expenses. For XYZ Corporation,

we will use the line:

Net Income Before Preferred Dividend $9.9 million

The other account we include in the Cash Flow Statement as a source of

cash is DEPRECIATION. Remember, depreciation is deducted as an operating

expense in the Income Statement. Since depreciation is

not actually a cash outflow, we must add XYZ's 1993 DEPRECIATION figure

of $8.9 million into the Cash Flow Statement so that the cash flow sources

are accurate.

Uses

Balance Sheet:

decreased

liabilities;

increased assets

As with the sources, there are two simple rules for calculating the

uses of cash in a company.

1. A decrease in a liability or equity account is a use of funds.

Paying off a loan is one example. In our XYZ Corporation

example, the OTHER CURRENT LIABILITIES account decreased by

$700,000 (from $5.6 million in 1992 to $4.9 million

in 1993). This means that XYZ paid off $700,000 of short-term

liabilities.

2. An increase in an asset account is a use of cash.

The increase indicates that funds were used to purchase

additional assets. XYZ purchased $22.6 million worth of FIXED

ASSETS during 1992 (from $136.2 million in 1992 to $158.8

million in 1993).

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-25

v05/15/94 v-1.1

p01/14/00

Financing Activities

Buying and

selling of capital

Financing activities are related to the buying and selling of capital.

Remember, a company has two alternatives for raising capital: debt

and equity. This section of the Cash Flow Statement is a summary of

the equity raised and the debt borrowed and paid off. Usually, only the

net changes of each account are listed.

Cash flow –

net increase /

(decrease)

For example, XYZ Corporation's LONG-TERM BONDS account was

$102.7 million in 1992 and $107.4 million in 1993. The company

may have paid off $25 million in bonds and issued $29.7 million in

new bonds, but the Cash Flow Statement will only show the net

increase of $4.7 million.

With that brief explanation about the sources and uses of funds, let's

take a look at XYZ Corporation's Cash Flow Statement.

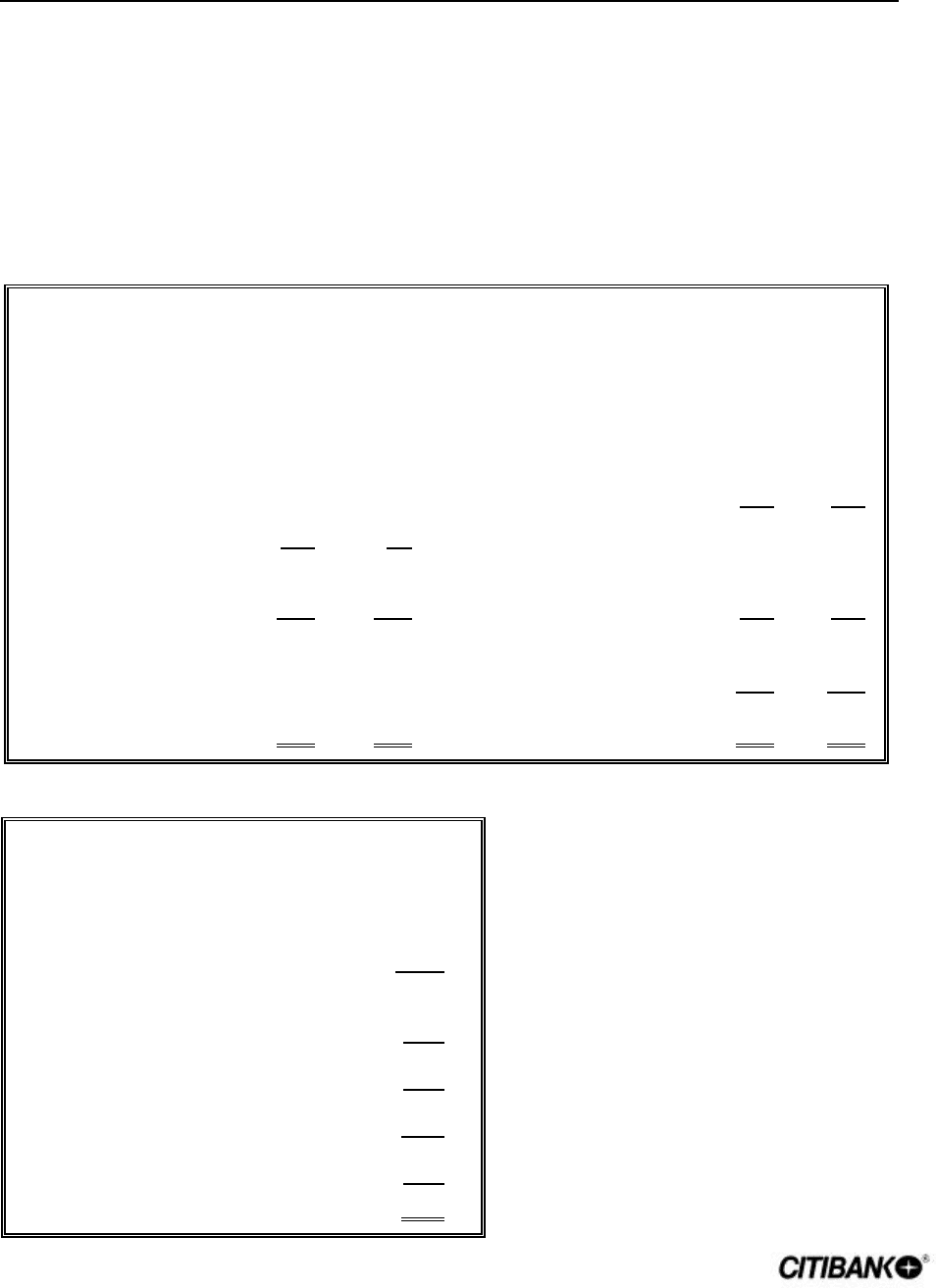

XYZ Corporation

December 31, 1993

(In Millions $)

OPERATING ACTIVITIES:

Sources:

Net Income Before Preferred Dividends 9.9

Depreciation 8.9

Incr. in Accounts Payable 2.5

Incr. in Accrued Wages and Taxes 0.2

Incr. in Other Current Liabilities (0.7)

Total Sources from Operations 20.8

Uses:

Incr. in Accounts Receivable (0.7)

Incr. in Inventories (3.7)

Incr. in Prepaid Expenses 0.8

Incr. in Other Current Assets 0.1

Incr. in Gross Fixed Assets 22.6

Total Uses from Operations 18.9

FINANCING ACTIVITIES:

Incr. in Notes Payable 1.9

Incr. in Long-term Bonds 4.7

Incr. in Preferred Stock 0.1

Incr. of Common Stock 0.0

Net Funds from Financing 6.7

Total Funds from Operations and Financing 8.6

Less Common and Preferred Dividends 7.7

Incr. (Decr.) in Cash and Mkt Sec. 0.9

Figure 1.5: XYZ Corporation Cash Flow Statement

www.LisAri.com

1-26 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

As you can see, the Cash Flow Statement is divided into OPERATING

ACTIVITIES, Sources and Uses, and FINANCING ACTIVITIES. The final

calculation is the NET INCREASE or DECREASE IN CASH AND MARKETABLE

SECURITIES. Let's see how we get there.

Operating

activities:

Sources

NET INCOME BEFORE PREFERRED DIVIDENDS ($9.9 million) and the

$8.9 million DEPRECIATION charge are taken directly from the 1993

Income Statement.

The current liabilities from the Balance Sheet are listed individually

(INCREASE IN ACCOUNTS PAYABLE, INCREASE IN ACCRUED WAGES AND TAXES,

INCREASE IN OTHER CURRENT LIABILITIES) with their net change from 1992

to 1993. TOTAL SOURCES FROM OPERATIONS ($20.8 million) is the sum of

these sources.

Operating

activities:

Uses

Next, the net change in each asset account except CASH and MARKETABLE

SECURITIES is listed: INCREASE IN ACCOUNTS RECEIVABLE, INCREASE IN

INVENTORIES, INCREASE IN PREPAID EXPENSES, INCREASE IN OTHER CURRENT

ASSETS, INCREASE IN GROSS FIXED ASSETS. GROSS FIXED ASSETS is used

instead of NET FIXED ASSETS because we have already adjusted for

DEPRECIATION and we do not want to double count. TOTAL USES FROM

OPERATIONS is the sum of these changes.

Financing

activities

Finally, we summarize the financing activities by listing each net change

from 1992 to 1993 for the potential sources of capital:

INCREASE IN NOTES PAYABLE, INCREASE IN LONG-TERM BONDS, INCREASE IN

PREFERRED STOCK, INCREASE OF COMMON STOCK. NET FUNDS FROM

FINANCING is the sum of the financing activities.

Total funds from

operations and

financing

TOTAL FUNDS FROM OPERATIONS AND FINANCING is calculated by

subtracting the uses from the sources and adding to that number the NET

FUNDS FROM FINANCING. In our XYZ example, that calculation is:

Total operating sources $20.8 million

- Total operating uses 18.9 million

+ Net financing sources 6.7 million

____________________________________________________________

Total funds from operations and financing $ 8.6 million

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-27

v05/15/94 v-1.1

p01/14/00

Increase

(Decrease) in

cash and

marketable

securities

Finally, we subtract the total value of the COMMON and PREFERRED

DIVIDENDS (from the Income Statement) to arrive at the net INCREASE

or DECREASE in CASH and MARKETABLE SECURITIES.

$8.6 million - $7.7 million = $0.9 million

Our check to make sure that the calculation is correct is to calculate the

net change in the Balance Sheet accounts for CASH and MARKETABLE

SECURITIES.

($5.7 million + $6.3 million) - ($6.2 million + $4.9 million) = $0.9 million

For our XYZ Corporation, we have calculated the sources and uses of

cash correctly.

Summary

The Cash Flow Statement is a summary of the sources and uses of cash

for a specified period of time. Different formats for presenting the

information have other names, such as "Statement of Changes in Financial

Position." Regardless of the format, the basic rules for calculating cash

flow remain the same. Any basic finance or accounting text will give

additional information on these other formats. The unit of the bank in

which you work will have specific instructions on the format you should

use for your analysis.

You have completed the "Cash Flow Statement" section of Financial Statement Analysis.

Please complete Progress Check 1.3, then continue to the next section that covers "Financial

Ratios." If you answer any questions incorrectly, please review the appropriate text.

www.LisAri.com

1-28 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

(This page is intentionally blank)

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-29

v05/15/94 v-1.1

p01/14/00

þ PROGRESS CHECK 1.3

Directions: Use the Balance Sheet and Income Statement information presented below

to answer the questions. Calculate the answer to each question, then check

your solution with the Answer Key on the next page.

Fruit Packing, Inc. — Balance Sheet

December 31, 1993 (In Millions $)

ASSETS 1992 1993 LIABILITIES AND EQUITY 1992 1993

Cash

Marketable Securities

Accounts Receivable

Raw Goods Inventory

Finished Goods Inventory

Prepaid Expenses

Other Current Assets

Total Current Assets

6.7

0.0

22.4

19.2

22.3

1.2

0.8

72.6

7.4

0.6

23.7

19.5

22.4

1.5

0.8

75.9

Accounts Payable - Fruit

Accounts Payable - Material

Notes Payable

Accrued Wages and Taxes

Other Current Liabilities

Total Current Liabilities

9.6

9.2

21.8

1.5

0.7

42.8

10.2

9.6

23.0

1.7

0.6

45.1

Gross Fixed Assets

Less Depreciation

Net Fixed Assets

97.5

16.8

80.7

101.2

19.9

81.3

Long-term Debt

Preferred Stock

Total Long-term Liabilities

46.1

7.8

96.7

45.1

7.8

98.0

Common Stock

Retained Earnings

Total Common Equity

15.1

41.5

56.6

15.1

44.1

59.2

Total Assets 153.3 157.2 Total Liabilities and Equity 153.3 157.2

Fruit Packing, Inc. — Income Statement

December 31, 1993 (In Millions $)

Net Sales 150.6

Operating Expenses 101.2

Depreciation 3.1

EBIT 46.3

Interest Expense 11.5

Earnings Before Taxes 34.8

Taxes (@ 40%) 13.9

Net Income to Shareholders 20.9

Preferred Dividends 6.3

Net Income to Common 14.6

Common Dividends 12.0

Earnings Retained 2.6

www.LisAri.com

1-30 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

(This page is intentionally blank)

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-31

v05/15/94 v-1.1

p01/14/00

PROGRESS CHECK 1.3

(Continued)

Assume you are building a Cash Flow Statement for Fruit Packing, Inc.

9. How much is the total cash SOURCE from operations?

_____a) $19.9 million

_____b) $23.6 million

_____c) $24.6 million

_____d) $25.1 million

_____e) $44.7 million

10. How much is the total cash USE from operations?

_____a) $0.3 million

_____b) $0.4 million

_____c) $1.3 million

_____d) $2.0 million

_____e) $5.7 million

11. What is the total of net funds from FINANCING?

_____a) ($1.0) million

_____b) $0.2 million

_____c) $1.0 million

_____d) $1.2 million

_____e) $1.3 million

www.LisAri.com

1-32 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

ANSWER KEY

9. How much is the total cash SOURCE from operations?

d) $25.1 million

(in millions $)

NET SALES 20.9

DEPRECIATION 3.1

INCREASE ACCOUNTS PAYABLE 1.0

INCREASE ACCRUED WAGES AND TAXES 0.2

INCREASE OTHER CURRENT LIABILITIES (0.1)

TOTAL SOURCES FROM OPERATIONS 25.1

10. How much is the total cash USE from operations?

e) $5.7 million

(in millions $)

INCREASE IN ACCOUNTS RECEIVABLE 1.3

INCREASE IN INVENTORIES 0.4

INCREASE IN PREPAID EXPENSES 0.3

INCREASE IN OTHER CURRENT ASSETS 0.0

INCREASE IN GROSS FIXED ASSETS 3.7

TOTAL USES FROM OPERATIONS 5.7

11. What is the total of net funds from FINANCING?

b) $0.2 million

(in millions $)

INCREASE IN NOTES PAYABLE 1.2

INCREASE IN LONG-TERM BONDS (1.0)

INCREASE IN COMMON STOCK 0.0

INCREASE IN PREFERRED STOCK 0.0

TOTAL FUNDS FROM FINANCING 0.2

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-33

v.05/13/94 v- 1.1

p.01/14/00

FINANCIAL RATIOS

Financial

statements used to

predict future

earnings

So far, we have seen how the Balance Sheet reports a company's

position at a point in time, how the Income Statement reports a

company's operations over a period of time, and how the Cash Flow

Statement reports a company's sources and uses of funds over that

period. The real value of financial statement analysis is to use these

statements to forecast a firm's future earnings.

From an investor's point of view, forecasting the future is the main

purpose of financial statement analysis. From a manager's viewpoint,

financial statement analysis is useful as a way to anticipate future

conditions and, most important, as a starting point for developing

strategies that influence a company's future course of business.

Ratios highlight

relationships

between accounts

An important step toward achieving these goals is to analyze the firm's

financial ratios. Ratios are designed to highlight relationships between

the financial statement accounts. These relationships begin to reveal

how well a company is doing in its primary goal of creating value for

its shareholders.

Useful with

application of

analytical

techniques

The ratios, alone, usually give the analyst very little information. There

are two ratio analysis techniques that provide additional insight into a

company. The first technique is to compare the ratios of one company

with other similar companies within the same industry. The second

technique is to observe trends of the ratios over a period of time.

These trends give clues about a company's performance.

Five ratio

categories

The most common financial ratios can be grouped into five broad

categories:

• Liquidity Ratios

• Asset Management Ratios

• Debt Management Ratios

• Profitability Ratios

• Market Value Ratios

www.LisAri.com