Citibank: basic of corporate finance

Подождите немного. Документ загружается.

1-14 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

• COSTS AND EXPENSES

LABOR AND MATERIALS – total amount spent on labor wages and

material costs to produce the items sold for the period. It is

common for these costs to be separated into two accounts:

material costs listed as COST OF GOODS SOLD and labor listed as

DIRECT LABOR COST.

DEPRECIATION – amount charged by the company for the use of

fixed assets to produce the items sold. This is not a cash

expenditure. It is an estimate of the decline in value of the plant and

equipment resulting from its use during the period.

SELLING EXPENSES – amount spent to sell the products or

services produced (includes advertising, sales commissions,

promotions, etc.)

GENERAL AND ADMINISTRATIVE – amount spent to manage the

production and sales of the company's products or services

(includes management salaries, office equipment, support staff,

etc.)

LEASE PAYMENTS – amount spent on leasing plants, equipment,

office space, etc.

• NET OPERATING INCOME – amount earned by the company's

operations during the reporting period. The calculation is NET SALES

minus COSTS AND EXPENSES. This value is also known as EARNINGS

BEFORE INTEREST AND TAXES (EBIT).

The Income Statement format varies between companies. The COST AND

EXPENSES section may have more or less detail than our example. Common

variations may include combining SELLING EXPENSES with GENERAL AND

ADMINISTRATIVE EXPENSES or combining DEPRECIATION EXPENSES with COST

OF LABOR AND MATERIALS.

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-15

v05/15/94 v-1.1

p01/14/00

The remaining Income Statement accounts are as follows.

• INTEREST EXPENSES – amount of interest paid on the company's

loans, notes, and bonds during the period

• EARNINGS BEFORE TAXES – NET OPERATING INCOME minus INTEREST

EXPENSES

• TAXES – amount of taxes paid by the company during the period.

Many companies provide the total tax assessment percentage on the

Income Statement.

• NET INCOME BEFORE PREFERRED DIVIDEND – amount of income

available for distribution to shareholders; calculated as EARNINGS

BEFORE TAXES minus TAXES

• PREFERRED DIVIDEND – amount distributed to preferred shareholders

during the period

• NET INCOME TO COMMON – amount available for distribution to

common shareholders or for internal use

• COMMON DIVIDEND – amount distributed to common shareholders

during the period

• EARNINGS RETAINED – amount held by the business to continue

operations

Shareholder Return on Investment

Appreciation in

value / dividends

There are two ways that a shareholder can receive a return on

investment. One is the appreciation in value of the shares of the

company (based on the future prospects of the company). The

other is a cash payment (dividend) paid by the company to the

shareholders. Many companies do not pay dividends to common

shareholders, especially growing companies with lots of investment

opportunities. We will discuss the methodology for determining the

value of stocks later in the course.

www.LisAri.com

1-16 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

Depreciation

DEPRECIATION in the Income Statement is a charge against income based

on an estimate of the percentage of the original cost for fixed assets

that has been used up in the production process during the period

covered by the Income Statement.

For example, suppose that a piece of equipment is purchased for

$500,000. For tax purposes, most governments do not allow companies

to charge the entire $500,000 as a business expense

at the time of purchase. Instead, they require the purchase to be

"capitalized," which means it is carried on the books as an asset.

However, equipment has a finite useful life to the company, so

governments allow a portion of the equipment purchase price to

be deducted from operating expenses each year of its useful life.

Typically, governments will provide depreciation schedules that classify

each type of equipment and dictate its estimated useful life.

Straight-line

depreciation

In our example, the piece of equipment may have an estimated useful

life of five years and, therefore, will have no value at the end of the five

years. Using a straight-line depreciation method, the annual amount that

the company may deduct is ($500,000 - $0) /

5 yrs. = $100,000. There are several different depreciation methods

and any accounting text can provide a more detailed discussion of their

calculations and uses.

Non-cash

bookkeeping

entry

Remember, DEPRECIATION is not a cash expense like LABOR AND

MATERIAL costs; it is simply a bookkeeping entry on the Balance Sheet

and on the Income Statement. The cash expense for fixed assets is

incurred at the time of purchase.

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-17

v05/15/94 v-1.1

p01/14/00

• On the Balance Sheet, GROSS FIXED ASSETS (capitalized

purchases of property, plants, and equipment) are listed at their

purchase price. Accumulated DEPRECIATION (sum of all

depreciation charges over the life of the assets currently on the

company's Balance Sheet) is deducted to arrive at NET FIXED

ASSETS. NET FIXED ASSETS can be considered as an estimate of the

value of those assets for the remainder of their useful lives.

These principles will also be important in the next section as we

analyze the Cash Flow Statement.

• On the Income Statement, the total DEPRECIATION for the

period for all CAPITALIZED ASSETS is deducted from earnings as

an OPERATING COST.

Summary

The Income Statement summarizes a company's operational expenses

and profitability over a given period of time. The total value of goods

and services sold by a company after deducting all operating costs is the

NET OPERATING INCOME. The deduction of interest, taxes, and

shareholder dividends results in the amount of earnings retained by the

company to support operations.

DEPRECIATION is a non-cash bookkeeping entry on the Balance Sheet and

on the Income Statement. On the Balance Sheet, it is the sum of all

depreciation charges over the life of the fixed assets. On the Income

Statement, it represents the portion of the value of a fixed asset that has

been used up for operations during the period.

You have completed the "Income Statement" section of Financial Statement Analysis. Please

complete the Progress Check and then continue with the section on "Cash Flow Statement." If

you answer any questions incorrectly, please review the appropriate text.

www.LisAri.com

1-18 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

(This page is intentionally blank)

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-19

v05/15/94 v-1.1

p01/14/00

þ PROGRESS CHECK 1.2

Directions: Select the correct answer for each question. Check your solution with the

Answer Key on the next page.

6. Suppose that a company has NET SALES of $332 million, INTEREST EXPENSES of $16

million, DEPRECIATION of $6 million, $225 million expenses for LABOR AND

MATERIALS, and ADMINISTRATIVE EXPENSES of $42 million. What is the EBIT for that

company?

_____a) $43 million

_____b) $49 million

_____c) $59 million

_____d) $65 million

_____e) $91 million

7. Use the information in question 6, and apply a tax rate of 40%. What is the NET

INCOME available for distribution to the shareholders of this company?

_____a) $23.6 million

_____b) $25.8 million

_____c) $35.4 million

_____d) $43.0 million

_____e) $59.0 million

8. XYZ Corporation purchases a widget maker for $750,000. The piece of equipment has an

estimated useful life of ten years. Using a straight-line depreciation method, the annual

amount the company can deduct as an OPERATING COST is:

_____a) $7,500 per year

_____b) $150,000 per year

_____c) $1,500 per year

_____d) $75,000 per year

www.LisAri.com

1-20 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

ANSWER KEY

6. Suppose that a company has NET SALES of $332 million, INTEREST EXPENSES of

$16 million, DEPRECIATION of $6 million, $225 million expenses for LABOR AND

MATERIALS, and ADMINISTRATIVE EXPENSES of $42 million. What is the EBIT for

that company?

c) $59 million

EBIT = NET SALES - OPERATING COSTS

(in millions)

Net Sales $332

Less:

LABOR AND MATERIALS $225

DEPRECIATION 6

ADMINISTRATIVE 42

EBIT $ 59

INTEREST EXPENSE is not an OPERATING COST

7. Use the information in question 6, and apply a tax rate of 40%. What is the NET INCOME

available for distribution to the shareholders of this company?

b) $25.8 million

Start with EBIT and deduct INTEREST and TAXES

(in millions)

EBIT $59.0

Less:

INTEREST $16.0

TAXES (@40%) 17.2 (59.0 - 16.0) x 0.40

NET INCOME $25.8

8. XYZ Corporation purchases a widget maker for $750,000. The piece of equipment

has an estimated useful life of ten years. Using a straight-line depreciation method, the

annual amount the company can deduct as an OPERATING COST is:

d) $75,000 per year

($750,000

÷

10 years)

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-21

v05/15/94 v-1.1

p01/14/00

CASH FLOW STATEMENT

Sources and uses

of funds

The financial statement that is used to show the sources and uses of a

company's funds is called a Cash Flow Statement. It also may be called

the "Statement of Changes in Financial Position" or the "Sources and

Uses Statement," depending on its structure. The analyst uses the Cash

Flow Statement to examine the flow of funds into a company and the

use of those funds. We will use the terms "funds" and "cash"

interchangeably throughout this section.

An analyst may have difficulty gaining access to the applicable

information needed to determine a company's sources and uses of cash.

This is especially true when studying a competitor. One solution is to

construct a Cash Flow Statement based on publicly available

information (such as the Income Statement and Balance Sheet from a

company's annual report). The objective is to develop a framework that

provides an accurate estimate of the company's cash flows. It is

important for you to learn to construct a Cash Flow Statement as

preparation for Unit Three – Time Value of Money.

We will continue to use the XYZ Corporation as our example. The

company's Balance Sheet for the past two years is shown again in Figure

1.3 and the Income Statement is shown again in Figure 1.4. These two

financial statements provide the information for the Cash Flow

Statement, and you will want to refer to them as we move through the

process.

www.LisAri.com

1-22 FINANCIAL STATEMENT ANALYSIS

v-1.1 v05/15/94

p01/14/00

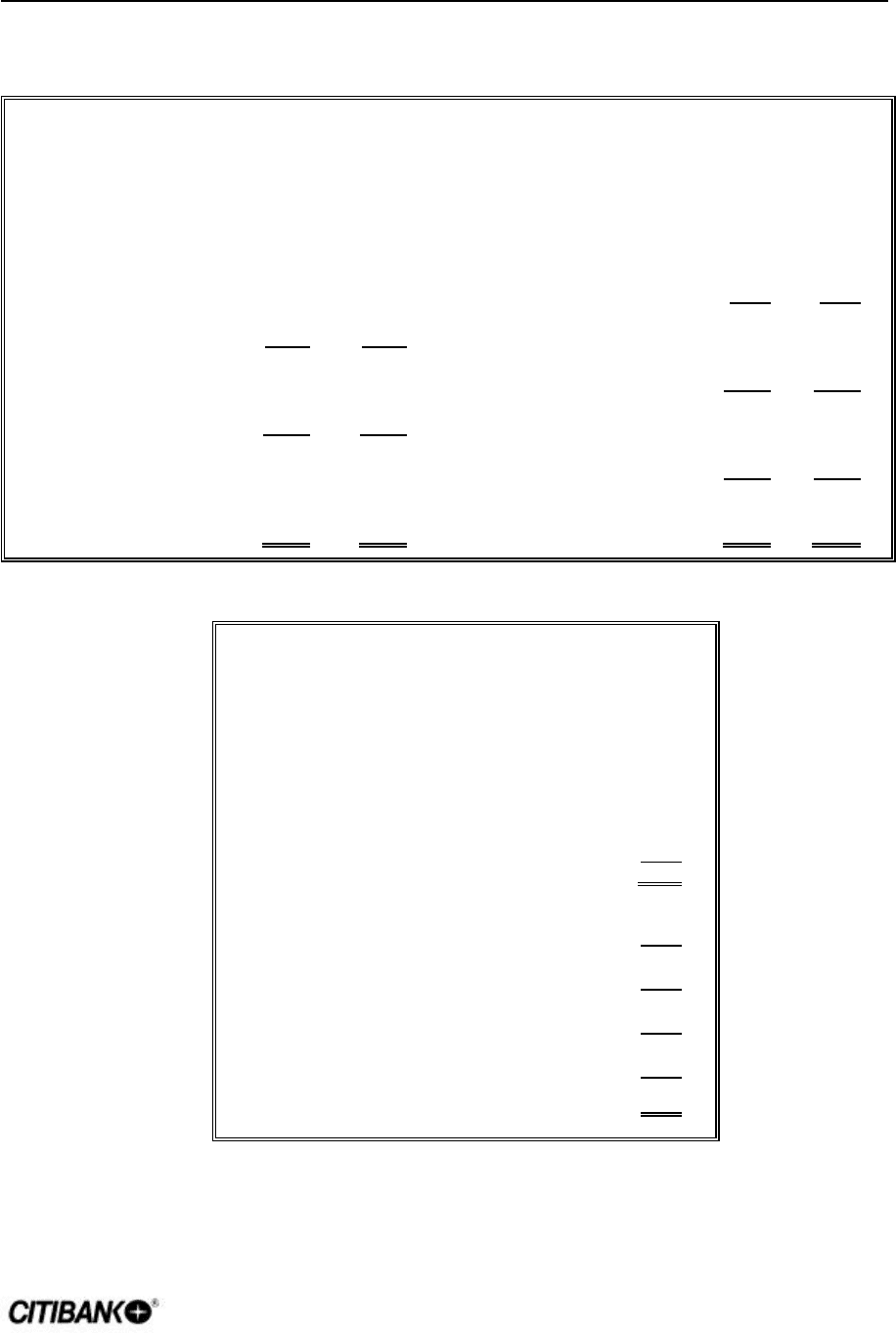

XYZ Corporation

December 31, 1993 (In Millions $)

ASSETS 1992 1993 LIABILITIES AND EQUITY 1992 1993

Cash 6.2 5.7 Accounts Payable 20.2 22.7

Marketable Securities 4.9 6.3 Notes Payable 29.6 31.5

Accounts Receivable 51.8 50.9 Accrued Wages and Taxes 2.1 2.3

Inventories 92.4 88.7 Other Current Liabilities 5.6 4.9

Prepaid Expenses 0.3 1.1 Total Current Liabilities 57.5 61.4

Other Current Assets 0.2 0.3

Total Current Assets 155.8 153.0 Long-term Debt 102.7 107.4

Preferred Stock 12.2 12.3

Gross Fixed Assets 136.2 158.8 Total Long-term Liabilities 172.4 181.1

Less Depreciation 16.0 24.9

Net Fixed Assets 120.2 133.9 Common Stock (8 Mil. Outst.) 10.4 10.4

Retained Earnings 93.2 95.4

Total Common Equity 103.6 105.8

Total Assets 276.0 286.9 Total Liabilities and Equity 276.0 286.9

Figure 1.3: XYZ Corporation – Balance Sheet for Two Years

XYZ Corporation

December 31, 1993 (In Millions $)

Net Sales 287.6

Cost and Expenses:

Labor and Materials

Depreciation

Selling Expenses

General and Administrative

Lease Payments

249.3

8.9

1.6

3.2

2.1

Total Operating Costs 265.1

Net Operating Income (EBIT)

Interest Expenses

22.5

6.0

Earnings Before Taxes

Taxes (at 40%)

16.5

6.6

Net Income Before Preferred Dividend

Preferred Dividend

9.9

3.7

Net Income to Common

Common Dividend

6.2

4.0

Earnings Retained 2.2

Figure 1.4: XYZ Corporation – Income Statement

www.LisAri.com

FINANCIAL STATEMENT ANALYSIS 1-23

v05/15/94 v-1.1

p01/14/00

Now, let's see how we build the Cash Flow Statement. It is grouped into

two main sections:

• Funds generated and used by operating activities

• Funds generated by financing activities

Operating Activities

We begin by identifying the operating activities that contribute to the

company's cash flow. Then we classify each activity as a source or a

use of cash.

Sources

Balance Sheet:

increased

liabilities;

decreased assets

First, let's see which accounts in the Balance Sheet represent sources

of cash from operating activities. There are two general rules to

determine if a change in a Balance Sheet account is a source of cash:

1. An increase in a liability or equity account is a source

of cash.

For example, an increase in ACCOUNTS PAYABLE (from $20.2

million in 1992 to $22.7 million in 1993) indicates that in 1993,

XYZ Company borrowed $2.5 million more from creditors than

it paid off. The company had access to that $2.5 million for use

in the business.

2. A decrease in an asset account is a source of cash.

For example, the decrease in the INVENTORY account (from $92.4

million in 1992 to $88.7 million in 1993) indicates that XYZ

Corporation reduced its investment in inventories by $3.7

million over the period. XYZ then had $3.7 million to use in

some other part of the company's operations.

www.LisAri.com