CIMA - C2 Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

370 25: Interpreting company accounts ⏐ Part D Interpretation of accounts

2.4 Relationship between ratios

You may already have realised that there is a mathematical connection between return on capital employed, profit margin

and asset turnover, since sales in the right-hand side of the equation below cancel out.

Profit

Capitalemployed

=

Profit

Sales

×

Sales

Capitalemployed

ROCE = Profit margin × Asset turnover

You

must

learn these formulae, as they will not be given in the assessment.

This is important. If we accept that ROCE is the most important single measure of business performance, comparing

profit with the amount of capital invested, we can go on to say that business performance is dependent on two separate

'

subsidiary

'

factors, each of which contributes to ROCE.

(a) Profit margin.

(b) Asset turnover.

For this reason, just as ROCE is sometimes called the

primary ratio

, the profit margin and asset turnover ratios are

sometimes called the

secondary ratios.

The implications of this relationship must be understood. Suppose that a return on capital employed of 20% is thought

to be a good level of business performance in the retail trade for electrical goods.

(a) Company A might decide to sell its products at a fairly high price and make a profit margin on sales of

10%. It would then need only an asset turnover of 2.0 times to achieve a ROCE of 20%:

20% = 10%

× 2

(b) Company B might decide to cut its prices so that its profit margin is only 2½%. Provided that it can

achieve an asset turnover of 8 times a year, attracting more customers with its lower prices, it will still

make the desired ROCE:

20% = 2½%

× 8

Company A might be a department store and company B a discount warehouse. Each will have a different selling price

policy, but each, in its own way, can be effective in achieving a target ROCE. In this example, if we supposed that both

companies had capital employed of $100,000 and a target return of 20% or $20,000.

(a) Company A would need annual sales of $200,000 to give a profit margin of 10% and an asset turnover of

2 times

2

000,200$

000,20$

000,100$

000,20$

×=

(b) Company B would need annual sales of $800,000 to give a profit margin of only 2½% but an asset

turnover of 8 times.

8

000,800$

000,20$

000,100$

000,20$

×=

The interpretation of financial statements requires a large measure of common sense.

Formula to

learn

FA

S

T F

O

RWAR

D

Assessment

focus point

391465 www.ebooks2000.blogspot.com

Part D Interpretation of accounts ⏐ 25: Interpreting company accounts 371

Clearly, a higher return on capital employed can be obtained by increasing the profit margin or the asset turnover ratio.

The profit margin can be increased by reducing costs or by raising selling prices.

However, if selling prices are raised, it is likely that sales demand will fall, with the possible consequence that the asset

turnover will also decline. If higher prices mean lower sales turnover, the increase in profit margin might be offset by the

fall in asset turnover, so that total return on capital employed might not improve.

2.5 Example: profit margin and asset turnover

Suppose that Swings and Roundabouts Ltd achieved the following results in 20X6.

Sales $100,000

Profit $5,000

Capital employed $20,000

The company

'

s management wish to decide whether to raise its selling prices. They think that if they do so, they can

raise the profit margin to 10% and by introducing extra capital of $55,000, sales turnover would be $150,000.

Evaluate the decision in terms of the effect on ROCE, profit margin and asset turnover.

Solution

Currently the ratios are

Profit margin (5/100) 5%

Asset turnover (100/20) 5 times

ROCE (5/20) 25%

With the proposed changes, the profit would be 10%

× $150,000 = $15,000, and the asset turnover would be:

)000,55000,20$(

000,150$

+

= 2 times, so that the ratios would be

Profit margin

× Asset turnover = ROCE

0%

× 2 times = 20%

⎟

⎠

⎞

⎜

⎝

⎛

$75,000

$15,000

In spite of increasing the profit margin and raising the total volume of sales, the extra assets required ($55,000) only

raise total profits by $(15,000 – 5,000) = $10,000.

The return on capital employed falls from 25% to 20% because of the sharp fall in asset turnover from 5 times to 2

times.

Question

Ratios

A trader has the following results.

$

Sales 200,000

Profit 36,000

Capital employed 120,000

392465 www.ebooks2000.blogspot.com

372

25: Interpreting company accounts ⏐ Part D Interpretation of accounts

Fill in the blanks.

Profit margin = _________________

Asset turnover = _________________

ROCE = _________________

Answer

Profit margin =

%18

000,200$

000,36$

=

Asset turnover =

000,120

000,200

= 1

2

/

3

times

ROCE =

%30

000,120

000,36

=

2.6 Different definitions of 'profit' and 'capital employed'

ROCE can be calculated in a number of ways. Unless told otherwise in the exam, use:

employed capital Average

interest andtax before profit Net

where capital employed includes long-term finance.

We have calculated Return on Capital Employed as a measure of how well a company is performing. What do we mean

by 'return' and by capital employed?

Return is a reward for investing in a business.

Capital employed means the funds that finance a business.

The providers of finance to a business expect some return on their investment.

(a) Trade payables and most other current liabilities merely expect to be paid what they are owed.

(b) A bank charges interest on overdrafts.

(c) Interest must be paid to the holders of loan stock.

(d) Preference shareholders expect a dividend at a fixed percentage rate of the nominal value of their shares.

(e) Ordinary shareholders also expect a dividend, and, any retained profits kept in the business also represent

funds

'owned' or 'provided' by them.

So, when calculating return on capital employed, what measure of 'return' and what measure of 'capital employed'

should be used?

Key terms

FA

S

T F

O

RWAR

D

393465 www.ebooks2000.blogspot.com

Part D Interpretation of accounts ⏐ 25: Interpreting company accounts 373

For a company, ROCE =

Netprofitbeforeinterest andtax

Share capital reserves longtermdebt++

which is the same as, ROCE =

Netprofitbeforeinterestandtax

Non current assetsplusnet current assets

−

2.7 Example: ROCE

For example, suppose that Draught reports the following income statement and statement of financial position.

INCOME STATEMENT FOR 20X4 (EXTRACT)

$

Profit before interest and tax

120,000

Interest

(20,000

)

Profit before tax

100,000

Taxation

(40,000

)

Profit after tax (earnings)

60,000

Note. An ordinary dividend of $50,000 was paid during the period.

STATEMENT OF FINANCIAL POSITION AT 31 DECEMBER 20X4

$

Non-current assets: tangible assets

350,000

Current assets

400,000

750,000

Capital and reserves

Called up share capital (ordinary shares of $1)

100,000

Retained profits

300,000

400,000

Non-current liabilities

10% debenture loans

200,000

Current liabilities

150,000

750,000

Solution

ROCE =

sliabilitie current less assets Total

taxand interest before Profits

×

100%

Where, total assets less current liabilities is equal to share capital plus reserves plus long term finance (ie the 10%

debenture loan).

If assets financed by debt capital are included below the line, it is more appropriate to show profits before interest above

the line because interest is the return on debt capital.

$600,000

$120,000

×

100% = 20%

Average capital employed = (capital employed at beginning of the accounting period + capital employed at the end of

the accounting period)

÷

2

Formula to

learn

Formula to

l

ea

rn

394465 www.ebooks2000.blogspot.com

374

25: Interpreting company accounts ⏐ Part D Interpretation of accounts

Question

Return on capital employed

Using the information in the last example for Draught Co, calculate ROCE.

Relevant figures as at 31 December 20X3 are as follows.

$

10% loans

200,000

Ordinary share capital

100,000

Retained earnings

290,000

590,000

Answer

Average capital employed = (590 + 600)

÷

2 = $595,000

ROCE =

595,000

120,000

= 20.2%

3 Working capital

Working capital is the difference between current assets (mainly inventory, receivables and cash) and current liabilities

(such as trade payables and a bank overdraft).

3.1 Current assets and liabilities

Current assets are items which are either cash already, or which will soon lead to the receipt of cash. Inventories will be

sold to customers and create receivables; and receivables will soon pay in cash for their purchases.

Current liabilities are items which will soon have to be paid for with cash. Trade payables will have to be paid and bank

overdraft is usually regarded as a short-term borrowing which may need to be repaid fairly quickly (or on demand, ie

immediately).

In statements of financial position, the word

'current' is applied to inventories, receivables, short-term investments and

cash (current assets) and amounts due for payment within one year

's time (current liabilities).

3.2 Working capital and trading operations

Current assets and current liabilities are a necessary feature of a firm's trading operations. There is a repeated cycle of

buying and selling which is carried on all the time. For example, suppose that on 1 April a firm has the following items.

$

Inventories

3,000

Receivables

0

Cash

2,000

5,000

Payables

0

Working capital

5,000

FA

S

T F

O

RWAR

D

395465 www.ebooks2000.blogspot.com

Part D Interpretation of accounts ⏐ 25: Interpreting company accounts 375

It might sell all the inventories for $4,500, and at the same time obtain more inventories from suppliers at a cost of

$3,500. The statement of financial position items would now be

$

Inventories

3,500

Receivables

4,500

Cash

2,000

10,000

Payables

(3,500

)

Working capital

6,500

(The increase in working capital to $6,500 from $5,000 is caused by the profit of $1,500 on the sale of the inventories.)

The receivables for $4,500 will eventually pay in cash and the payables for $3,500 must also be paid. This would give us

$

Inventories

3,500

Receivables

0

Cash (2,000 + 4,500 – 3,500)

3,000

6,500

Payables

0

Working capital

6,500

However, if the inventories are sold on credit for $5,500 and further purchases of inventories costing $6,000 are made,

the cycle of trading will continue as follows.

$

Inventories

6,000

Receivables

5,500

Cash

3,000

14,500

Payables

(6,000

)

Working capital (boosted by further profit of $2,000)

8,500

From this basic example you might be able to see that working capital items are part of a continuous flow of trading

operations. Purchases add to inventories and payables at the same time, payables must be paid and receivables will pay

for their goods. The cycle of operations always eventually comes back to cash receipts and cash payments.

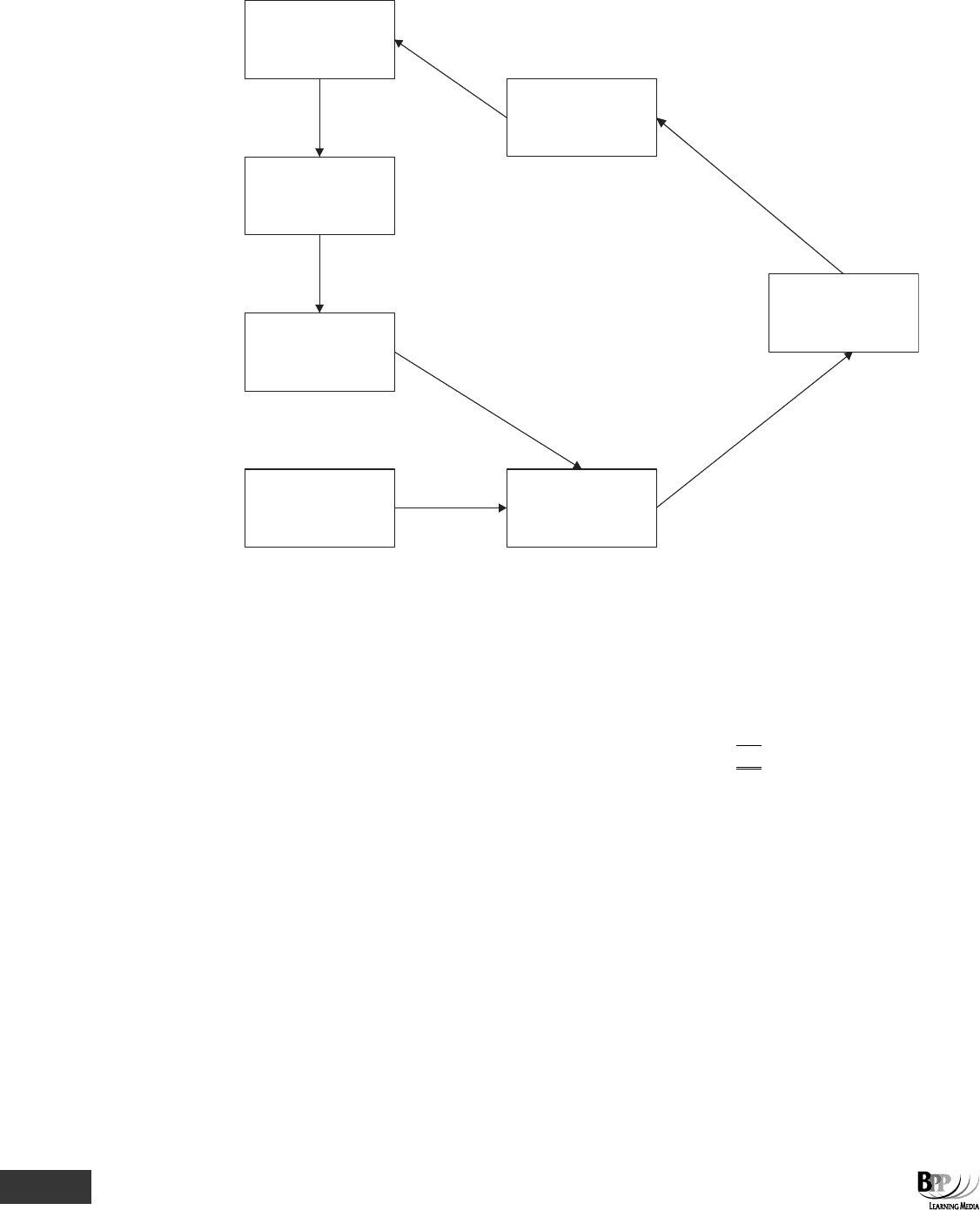

3.3 The operating cycle or cash cycle

The operating cycle (or cash cycle) is a term used to describe the time taken from the purchase of raw materials to the

sale of finished goods.

A firm buys raw materials, probably on credit. The raw materials might be held for some time in stores before being

issued to the production department and turned into an item of finished goods. The finished goods might be kept in a

warehouse for some time before they are eventually sold to customers. By this time, the firm will probably have paid for

the raw materials purchased. If customers buy the goods on credit, it will be some time before the cash from the sales is

eventually received.

The cash cycle, or operating cycle, measures the period of time between the time cash is paid out for raw materials and

the time cash is received in from receivables.

This cycle of repeating events is shown diagrammatically below.

Key term

396465 www.ebooks2000.blogspot.com

376

25: Interpreting company accounts ⏐ Part D Interpretation of accounts

RAW

MATERIALS

WORK IN

PROGRESS

FINISHED

GOODS

PROFIT IN RECEIVABLES

PAYA BL ES

CASH

CASH CYCLE

OR

OPERATING

CYCLE

Suppose that a firm buys raw materials on 1½ months

'

credit, holds them in store for 1 month and then issues them to

the production department. The production cycle is very short, but finished goods are held for 1 month before they are

sold. Receivables take two months

'

credit. The cash cycle would be

Months

Raw material inventory turnover period

1.0

Less: credit taken from suppliers

(1.5)

Finished goods inventory turnover period

1.0

Receivable's payment period

2.0

Cash cycle

2.5

There would be a gap of 2½ months between paying cash for raw materials and receiving cash (including profits) from

receivables. A few dates might clarify this point. Suppose the firm purchases its raw materials on 1 January. The

sequence of events would then be as follows.

Date

Purchase of raw materials 1 Jan

Issue of materials to production (one month after purchase) 1 Feb

Payment made to suppliers (1½ months after purchase) 15 Feb

Sale of finished goods (one month after production begins) 1 Mar

Receipt of cash from receivables (two months after sale) 1 May

The cash cycle is the period of 2½ months from 15 February, when payment is made to suppliers, until 1 May, when

cash is received from customers.

397465

www.ebooks2000.blogspot.com

Part D Interpretation of accounts ⏐ 25: Interpreting company accounts 377

3.4 Turnover periods

A 'turnover' period is an (average) length of time.

(a) In the case of inventory turnover, it is the length of time an item of inventory is held in stores before it is

used.

(i) A raw materials inventory turnover period is the length of time raw materials are held before being

issued to the production department.

(ii) A work in progress turnover period is the length of time it takes to turn raw materials into finished

goods in the factory.

(iii) A finished goods inventory turnover period is the length of time that finished goods are held in a

warehouse before they are sold.

(iv) When a firm buys goods and re-sells them at a profit, the inventory turnover period is the time

between their purchase and their resale.

(b) The receivables

' turnover period, or debt collection period, is the length of the credit period taken by

customers

– it is the time between the sale of an item and the receipt of cash for the sale from the

customer.

(c) Similarly, the payables

' turnover period, or period of credit taken from suppliers, is the length of time

between the purchase of materials and the payment to suppliers.

Turnover periods can be calculated from information in a firm

's income statement and statement of financial position.

Inventory turnover periods are calculated as follows.

(a) Raw materials:

(Average)rawmaterialinventoriesheld

Totalrawmaterialconsumedinone year

×

12 months

(b) Work in progress (the length of the production period):

(Average)WIP

Totalcost ofproductioninthe year

×

12 months

(c) Finished goods:

(Average)inventories

Totalcost of goodssoldinone year

×

12 months

(d) Inventories of items bought for re-sale:

(Average)inventories

Total(materials)cost of goods

bought andsoldinone year

×

12 months

The word 'average' is put in brackets because although it is strictly correct to use average values, it is more common to

use the value of inventories shown in a single statement of financial position

– at one point in time – to estimate the

turnover periods. But if available use opening and closing balances divided by two.

3.5 Example

A company buys goods costing $620,000 in one year and uses goods costing $600,000 in production (in regular

monthly quantities) and the cost of material in inventory at 1 January is $100,000.

Key term

Formula to

learn

398465 www.ebooks2000.blogspot.com

378

25: Interpreting company accounts ⏐ Part D Interpretation of accounts

Solution

The inventory turnover period could be calculated as:

000,600$

000,100$

×

12 months = 2 months

In other words, inventories are bought two months before they are used or sold.

3.6 Trade receivables collection period

The debt collection period is calculated as:

Average receivables

Annual credit sales

×

12 months

3.7 Example

If a company sells goods for $1,200,000 per annum in regular monthly quantities, and if receivables are $150,000.

Solution

The trade receivables collection period is

000,200,1$

000,150$

×

12 months = 1.5 months

In other words, receivables will pay for goods 1

1

/2 months on average after the time of sale.

3.8 Trade payables payment period

The period of credit taken from suppliers is calculated as:

Average trade payables

Totalpurchasesinone year

×

12 months

Notice that the payables are compared with materials bought whereas for raw material inventory turnover, raw material

inventories are compared with materials used in production. This is a small, but very significant difference.

3.9 Example

For example, if a company sells goods for $600,000 and makes a gross profit of 40% on sales, and if the amount of

trade payables is $30,000.

Solution

The period of credit taken from the suppliers is:

)000,600£of%60(

000,30£

×

12 months = 1 month

In other words, suppliers are paid in the month following the purchase of goods.

Formula to

learn

Formula to

learn

399465 www.ebooks2000.blogspot.com

Part D Interpretation of accounts ⏐ 25: Interpreting company accounts 379

Question

Cash cycle

Legion's 20X4 accounts show the following.

$

Sales 360,000

Cost of goods sold 180,000

Inventories 30,000

Receivables 75,000

Trade payables 45,000

Calculate the length of the cash cycle.

Answer

Inventory turnover Debt collection period Credit taken from suppliers

12

180,000

30,000

× 12

360,000

75,000

× 12

180,000

45,000

×

= 2 months = 2

1

/2 months = 3 months

The cash cycle is

Months

Inventory turnover period

2.0

Credit taken from suppliers

(3.0)

Debt collection period

2.5

Cash cycle

1.5

In this example, Legion pays its suppliers one month after the inventories have been sold, since the inventory turnover is

two months but credit taken is three months.

3.10 Turnover periods and the total amount of working capital

If the inventory turnover period gets longer or if the debt collection period gets longer, the total amount of inventories or

of receivables will increase. Similarly, if the period of credit taken from the suppliers gets shorter, the amount of

payables will become smaller. The effect of these changes would be to increase the size of working capital (ignoring

bank balances or overdrafts).

3.11 Example

Suppose that a company has annual sales of $480,000 (in regular monthly quantities, all on credit) and a materials cost

of sales of $300,000. (

Note

. A

'

materials cost of sales

'

is the cost of materials in the cost of sales.)

(a) If the inventory turnover period is 2 months, the debt collection period 1 month and the period of credit taken

from suppliers is 2 months, the company

'

s working capital (ignoring cash) would be

$

Inventories (2/12

× $300,000)

50,000

Receivables (1/12

× $480,000)

40,000

90,000

Payables (2/12

× $300,000)

(50,000)

40,000

The cash cycle would be (2 + 1 – 2) = 1 month.

400465 www.ebooks2000.blogspot.com