Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

When a firm takes out insurance, it is simply transferring the risk to the insur-

ance company. Insurance companies have some advantages in bearing risk. First,

they may have considerable experience in insuring similar risks, so they are well

placed to estimate the probability of loss and price the risk accurately. Second, they

may be skilled at providing advice on measures that the firm can take to reduce the

risk, and they may offer lower premiums to firms that take this advice. Third, an

insurance company can pool risks by holding a large, diversified portfolio of poli-

cies. The claims on any individual policy can be highly uncertain, yet the claims on

a portfolio of policies may be very stable. Of course, insurance companies cannot

diversify away macroeconomic risks; firms use insurance policies to reduce their

specific risk, and they find other ways to avoid macro risks.

Insurance companies also suffer some disadvantages in bearing risk, and these

are reflected in the prices they charge. Suppose your firm owns a $1 billion offshore

oil platform. A meteorologist has advised you that there is a 1-in-10,000 chance that

in any year the platform will be destroyed as a result of a storm. Thus the expected

loss from storm damage is $ .

The risk of storm damage is almost certainly not a macroeconomic risk and can

potentially be diversified away. So you might expect that an insurance company

would be prepared to insure the platform against such destruction as long as the

premium was sufficient to cover the expected loss. In other words, a fair premium

for insuring the platform should be $100,000 a year.

4

Such a premium would make

insurance a zero-NPV deal for your company. Unfortunately, no insurance com-

pany would offer a policy for only $100,000. Why not?

• Reason 1: Administrative costs. An insurance company, like any other business,

incurs a variety of costs in arranging the insurance and handling any claims.

For example, disputes about the liability for environmental damage can eat up

millions of dollars in legal fees. Insurance companies need to recognize these

costs when they set their premiums.

• Reason 2: Adverse selection. Suppose that an insurer offers life insurance policies

with “no medical needed, no questions asked.” There are no prizes for

guessing who will be most tempted to buy this insurance. Our example is an

extreme case of the problem of adverse selection. Unless the insurance company

can distinguish between good and bad risks, the latter will always be most

eager to take out insurance. Insurers increase premiums to compensate.

• Reason 3: Moral hazard. Two farmers met on the road to town. “George,” said

one, “I was sorry to hear about your barn burning down.” “Shh,” replied the

other, “that’s tomorrow night.” The story is an example of another problem for

insurers, known as moral hazard. Once a risk has been insured, the owner may

be less careful to take proper precautions against damage. Insurance

companies are aware of this and factor it into their pricing.

When these extra costs are small, insurance may be close to a zero-NPV transac-

tion. When they are large, insurance may be a costly way to protect against risk.

Many insurance risks are jump risks; one day there is not a cloud on the hori-

zon and the next day the hurricane hits. The risks can also be huge. For example,

Hurricane Andrew, which devastated Florida, cost insurance companies $17 bil-

1 billion/10,000 $

ˇ 100,000

756 PART VIII Risk Management

4

This is imprecise. If the premium is paid at the beginning of the year and the claim is not settled

until the end, then the zero-NPV premium equals the discounted value of the expected claim or

$.100,000/1 1 r2

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

lion; the attack on the World Trade Center is likely to involve payments of more

than $35 billion.

Many in the industry worry that one day a major disaster will wipe out a large

proportion of the capital of the U.S. insurance industry. Therefore, insurance com-

panies have been looking for ways to share these risks with investors. One solution

is for the insurance company to issue catastrophe bonds (or Cat bonds). The payment

on a Cat bond depends on whether a catastrophe occurs and how much is lost.

5

The first public issue of a Cat bond was made by the Swiss insurance giant, Win-

terthur. As a major provider of automobile insurance, Winterthur wanted to pro-

tect itself against the risk that storm damage could lead to an unusually large num-

ber of claims. Therefore, when it issued its bond, the company stated that it would

not pay the annual interest if ever there was a hailstorm in Switzerland which dam-

aged at least 6,000 cars that it had insured. In effect, owners of the Winterthur Cat

bonds coinsured the company’s risks.

How British Petroleum (BP) Changed Its Insurance Strategy

6

Major public companies typically buy insurance against large potential losses and

self-insure against routine ones. The idea is that large losses can trigger financial

distress. On the other hand, routine losses for a corporation are predictable, so

there is little point paying premiums to an insurance company and receiving back

a fairly constant proportion as claims.

BP Amoco has challenged this conventional wisdom. Like all oil companies, BP

is exposed to a variety of potential losses. Some arise from routine events such as

vehicle accidents and industrial injuries. At the other extreme, they may result

from catastrophes such as a major oil spill or the loss of an offshore oil rig. In the

past BP purchased considerable external insurance.

7

During the 1980s it paid out

an average of $115 million a year in insurance premiums and recovered $25 million

a year in claims.

BP then took a hard look at its insurance strategy. It decided to allow local man-

agers to insure against routine risks, for in those cases insurance companies have

an advantage in assessing and pricing risk and compete vigorously against one an-

other. However, it decided not to insure against most losses above $10 million. For

these larger, more specialized risks BP felt that insurance companies had less abil-

ity to assess risk and were less well placed to advise on safety measures. As a re-

sult, BP concluded, insurance against large risks was not competitively priced.

How much extra risk did BP assume by its decision not to insure against major

losses? BP estimated that large losses of above $500 million could be expected to

occur once in 30 years. But BP is a huge company with equity worth about $180 bil-

lion. So even a $500 million loss, which could throw most companies into bank-

ruptcy, would translate after tax into a fall of less than 1 percent in the value of

CHAPTER 27

Managing Risk 757

5

For a discussion of Cat bonds and other techniques to spread insurance risk, see N. A. Doherty, “Fi-

nancial Innovation in the Management of Catastrophe Risk,” Journal of Applied Corporate Finance 10 (Fall

1997), pp. 84–95; and K. Froot, “The Market for Catastrophe Risk: A Clinical Examination,” Journal of Fi-

nancial Economics 60 (2001), pp. 529–571.

6

Our description of BP’s insurance strategy draws heavily on N. A. Doherty and C. W. Smith, Jr., “Cor-

porate Insurance Strategy: The Case of British Petroleum,” Journal of Applied Corporate Finance 6 (Fall

1993), pp. 4–15.

7

However, with one or two exceptions insurance has not been available for the very largest losses of

$500 million or more.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

BP’s equity. BP concluded that this was a risk worth taking. In other words, it con-

cluded that for large, low-probability risks the stock market was a more efficient

risk-absorber than the insurance industry.

BP Amoco is not the only company that has looked at the package of risks that

it faces and the way that these risks should be managed. Here is how The Economist

summarized risk management in Duke Energy:

8

Duke’s risk managers are currently designing a model that examines different types

of risk together: movements in exchange rates, changes in raw material prices,

downtime caused by distribution failures, and so on. This is supposed to produce

an “aggregate loss distribution,” which estimates the likelihood that several events

could happen at once and sink the company. With this better understanding of the

company’s aggregate risk, Duke’s managers can make a more informed decision

about how much of this potential loss should be absorbed by shareholders, how

much hedged in the financial markets, and how much transferred to insurers.

758 PART VIII Risk Management

8

“Meet the Riskmongers,” The Economist, July 18, 1998, p. 93.

9

“Side bet” conjures up an image of wicked speculators. Derivatives attract their share of speculators, some

of whom may be wicked, but they are also used by sober and prudent businesspeople to reduce risk.

10

We oversimplify. For example, the miller won’t reduce risk if bread prices vary in proportion to the

postharvest wheat price. In this case the miller is in the hazardous position of having fixed her cost but

not her selling price. This point is discussed in A. C. Shapiro and S. Titman, “An Integrated Approach

to Corporate Risk Management,” Midland Corporate Finance Journal 3 (Summer 1985), pp. 41–56.

27.2 HEDGING WITH FUTURES

Hedging involves taking on one risk to offset another. We will explain shortly how

to set up a hedge, but first we will give some examples and describe some tools that

are specially designed for hedging. These are futures, forwards, and swaps. To-

gether with options, they are known as derivative instruments or derivatives because

their value depends on the value of another asset. You can think of them as side

bets on the value of the underlying asset.

9

We start with the oldest actively traded derivative instruments, futures con-

tracts. Futures were originally developed for agricultural and other commodities.

For example, suppose that a wheat farmer expects to have 100,000 bushels of wheat

to sell next September. If he is worried that the price may decline in the interim, he

can hedge by selling 100,000 bushels of September wheat futures. In this case he

agrees to deliver 100,000 bushels of wheat in September at a price that is set today.

Do not confuse this futures contract with an option, in which the holder has a

choice whether to make delivery; the farmer’s futures contract is a firm promise to

deliver wheat.

A miller is in the opposite position. She needs to buy wheat after the harvest. If

she would like to fix the price of this wheat ahead of time, she can do so by buying

wheat futures. In other words, she agrees to take delivery of wheat in the future at

a price that is fixed today. The miller also does not have an option; if she holds the

contract to maturity, she is obliged to take delivery.

Both the farmer and the miller have less risk than before.

10

The farmer has

hedged risk by selling wheat futures; this is termed a short hedge. The miller has

hedged risk by buying wheat futures; this is known as a long hedge.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

The price of wheat for immediate delivery is known as the spot price. When the

farmer sells wheat futures, the price that he agrees to take for his wheat may be

very different from the spot price. But as the date for delivery approaches, a futures

contract becomes more and more like a spot contract and the price of the future

snuggles up to the spot price.

The farmer may decide to wait until his futures contract matures and then de-

liver wheat to the buyer. In practice such delivery is very rare, for it is more con-

venient for the farmer to buy back the wheat futures just before maturity.

11

If he is

properly hedged, any loss on his wheat crop will be exactly offset by the profit on

his sale and subsequent repurchase of wheat futures.

Commodity and Financial Futures

Futures contracts are bought and sold on organized futures exchanges. Table 27.1

lists the principal commodity futures contracts and the exchanges on which they are

traded. Notice that our farmer and miller are not the only businesses that can hedge

CHAPTER 27

Managing Risk 759

Future Exchange Future Exchange

Barley WPG Orange juice NYBOT

Corn CBT, MCE Sugar LIFFE, NYBOT

Oats CBT

Wheat CBT, KC, MCE, MPLS Aluminum LME

Copper COMEX, LME

Gold COMEX

Soybeans CBT, MCE Lead LME

Soybean meal CBT Nickel LME

Soybean oil CBT Silver COMEX

Tin LME

Live cattle CME Zinc LME

Lean hogs CME

Crude oil IPE, NYMEX

Cocoa LIFFE, NYBOT Gas oil IPE

Coffee LIFFE, NYBOT Heating oil NYMEX

Cotton NYBOT Natural gas IPE, NYMEX

Lumber CME Unleaded gasoline NYMEX

TABLE 27.1

Some commodity futures and the principal exchanges on which they are traded.

Key to abbreviations:

CBT Chicago Board of Trade LME London Metal Exchange

CME Chicago Mercantile Exchange MCE MidAmerica Commodity Exchange

COMEX Commodity Exchange Division of NYMEX MPLS Minneapolis Grain Exchange

IPE International Petroleum Exchange of London NYBOT New York Board of Trade

KC Kansas City Board of Trade NYMEX New York Mercantile Exchange

LIFFE London International Financial WPG Winnipeg Commodity Exchange

Futures and Options Exchange

11

In the case of some of the financial futures described below, you cannot deliver the asset. At maturity

the buyer simply receives (or pays) the difference between the spot price and the price at which he or

she agreed to purchase the asset.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

risk with commodity futures. The lumber company and the builder can hedge

against changes in lumber prices, the copper producer and the cable manufacturer

can hedge against changes in copper prices, the oil producer and the trucker can

hedge against changes in gasoline prices, and so on.

12

For many firms the wide fluctuations in interest rates and exchange rates

have become at least as important a source of risk as changes in commodity

prices. Financial futures are similar to commodity futures, but instead of plac-

ing an order to buy or sell a commodity at a future date, you place an order to

buy or sell a financial asset at a future date. Table 27.2 lists some important fi-

nancial futures. It is far from complete. You can trade futures on the Thailand

stock market index, the South African rand, Finnish government bonds, and

many other financial assets.

Financial futures have been a remarkably successful innovation. They were in-

vented in 1972; within a few years, trading in financial futures significantly ex-

ceeded trading in commodity futures.

760 PART VIII

Risk Management

12

By the time you read this, the list of futures contracts will almost certainly be out of date. Unsuccess-

ful contracts are regularly dropped, and at any time the exchanges may be seeking approval for liter-

ally dozens of new contracts.

Future Exchange Future Exchange

U.S. Treasury bonds CBT Dow Jones Industrial Average CBT

U.S. Treasury notes CBT S&P 500 Index CME

U.S. agency notes CBT European equity index (Dow Jones Eurex

German government bonds (bunds) Eurex Euro Stoxx)

Japanese government bonds (JGBs) Simex, TSE French equity index (CAC) MATIF

British government bonds (gilts) LIFFE German equity index (DAX) Eurex

Japanese equity index (Nikkei) CME, OSE,

U.S. Treasury bills CME Simex

UK equity index (FTSE) LIFFE

LIBOR CME Individual stocks LIFFE

Eurodollar deposits CME Euro CME

Euroyen deposits CME, Simex,

TIFFE Japanese yen CME

TABLE 27.2

Some financial futures and the principal exchanges on which they are traded.

Key to abbreviations:

CBT Chicago Board of Trade

CME Chicago Mercantile Exchange

LIFFE London International Financial Futures and Options Exchange

MATIF Marché à Terme d’Instruments Financiers

OSE Osaka Securities Exchange

SIMEX Singapore International Monetary Exchange

TIFFE Tokyo International Financial Futures Exchange

TSE Tokyo Stock Exchange

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

The Mechanics of Futures Trading

When you buy or sell a futures contract, the price is fixed today but payment is not

made until later. You will, however, be asked to put up margin in the form of either

cash or Treasury bills to demonstrate that you have the money to honor your side

of the bargain. As long as you earn interest on the margined securities, there is no

cost to you.

In addition, futures contracts are marked to market. This means that each day any

profits or losses on the contract are calculated; you pay the exchange any losses

and receive any profits. For example, suppose that our farmer agreed to deliver

100,000 bushels of wheat at $2.80 a bushel. The next day the price of wheat futures

declines to $2.75 a bushel. The farmer now has a profit on his sale of

. The exchange’s clearinghouse therefore pays this $5,000 to the farmer.

You can think of the farmer as closing out his position every day and then opening up

a new position. Thus after the first day the farmer has realized a profit of $5,000 on his

trade and now has an obligation to deliver wheat for $2.75 a bushel. The $.05 that the

farmer has already been paid plus the $2.75 that remains to be paid equals the $2.80

selling price at which the farmer originally agreed to deliver wheat.

Of course, our miller is in the opposite position. The fall in the futures price

leaves her with a loss of $.05 a bushel. She must, therefore, pay over this loss to the

exchange’s clearinghouse. In effect the miller closes out her initial purchase at a

$.05 loss and opens a new contract to take delivery at $2.75 a bushel.

13

Spot and Futures Prices—Financial Futures

If you want to buy a security, you have a choice. You can buy it for immediate de-

livery at the spot price. Alternatively, you can place an order for later delivery; in

this case you buy at the futures price. When you buy a financial future, you end up

with exactly the same security that you would have if you bought in the spot mar-

ket. However, there are two differences. First, you don’t pay for the security up

front, and so you can earn interest on its purchase price. Second, you miss out on

any dividend or interest that is paid in the interim. This tells us something about

the relationship between the spot and futures prices:

14

Here is the t-period risk-free interest rate. An example will show how and why

this formula works.

Example: Stock Index Futures Suppose six-month stock index futures trade at

1,205 when the index is 1,190. The six-month interest rate is 4 percent, and the av-

erage dividend yield of stocks in the index is 1.6 percent per year. Are these num-

bers consistent?

r

f

Futures price

11 r

f

2

t

spot

price

PV q

dividends or

interest payments

forgone

r

$ˇ .05 $ˇ 5,000

100,000

CHAPTER 27 Managing Risk 761

13

Notice that neither the farmer nor the miller need be concerned about whether the other party will

honor his or her side of the bargain. The futures exchange guarantees the contract and protects itself by

settling up profits and losses each day.

14

This relationship is strictly true only if the contract is not marked to market. Otherwise the value of

the future depends on the path of interest rates up to the delivery date. In practice this qualification is

usually unimportant. See J. C. Cox, J. E. Ingersoll, and S. A. Ross, “The Relationship between Forward

and Futures Prices,” Journal of Financial Economics 9 (1981), pp. 321–346.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

Suppose you buy the futures contract and set aside the money to exercise it. At

a 4 percent annual rate, you’ll earn about 2 percent interest over the next six

months. Thus you invest

What do you get in return? Everything you would have gotten by buying the in-

dex now at the spot price, except for the dividends paid over the next six months.

If we assume, for simplicity, that a half-year’s dividends are paid in month six

(rather than evenly over six months), your payoff is

You get what you pay for.

Spot and Futures Prices—Commodities

The difference between buying commodities today and buying commodity futures is

more complicated. First, because payment is again delayed, the buyer of the future

earns interest on her money. Second, she does not need to store the commodities and,

therefore, saves warehouse costs, wastage, and so on. On the other hand, the futures

contract gives no convenience yield, which is the value of being able to get your hands

on the real thing. The manager of a supermarket can’t burn heating oil futures if

there’s a sudden cold snap, and he can’t stock the shelves with orange juice futures if

he runs out of inventory at 1

P

.

M

. on a Saturday. All this means that for commodities,

No one would be willing to hold the futures contract at a higher futures price or to

hold the commodity at a lower futures price.

15

It’s interesting to compare the formulas for futures prices of commodities to the

formulas for securities. PV(convenience yield) plays the same role as PV(dividends

or interest payments forgone). But financial assets cost nothing to store, so PV(stor-

age costs) does not appear in the formula for financial futures.

You can’t observe PV(convenience yield) or PV(storage) separately, but you can

infer the difference between them by comparing the spot price to the discounted

futures price. This difference—that is, convenience yield less storage cost—is

called net convenience yield.

Here is an example using quotes for August 2001. At that time the spot price

of coffee was about 51 cents per pound. The futures price for March 2002 was

58.7 cents. Of course, if you bought and held the futures, you would not pay until

March. The present value of this outlay is 57.4 cents, using a one-year interest rate

of 4 percent. So PV(net convenience yield) is negative at 6.4 cents a pound:

51 57.4 6.4 cents

PV1net convenience yield2 spot price

futures price

1 r

f

Futures price

11 r

f

2

t

spot price PV a

storage

costs

bPV a

convenience

yield

b

Spot price PV1dividends2 1,190

1,190 1.0082

1.02

1,181

Futures price

11 r

f

2

t

1,205

1.02

1,181

762 PART VIII Risk Management

15

Our formula could overstate the futures price if no one is willing to hold the commodity, that is, if in-

ventories fall to zero or some absolute minimum.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

Sometimes the net convenience yield is expressed as a percentage of the spot

price, in this case as , or percent. Coffee in 2001 was in

ample supply and evidently roasters had no worries that they would run short

in the months ahead.

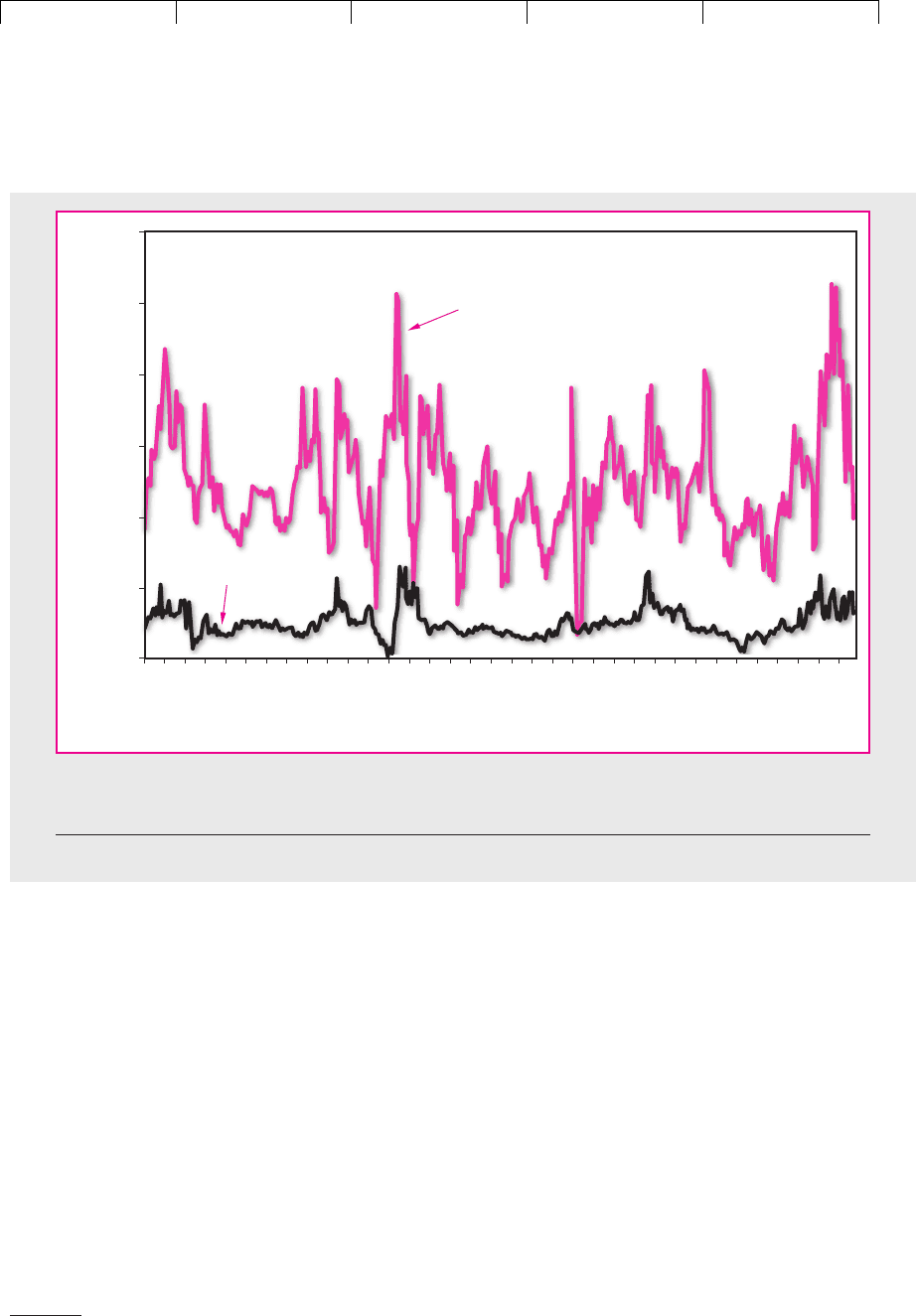

Figure 27.1 plots percentage net convenience yields for crude oil and gas oil

(used for heating). Notice how much the spread between the spot and futures

price for gas oil bounces around. When there are shortages or fears of an inter-

ruption of supply, traders may be prepared to pay 2 or more percent per week

for the convenience of having oil in the tanks rather than the promise of future

delivery.

16

There is one further complication that we should note. There are some com-

modities that cannot be stored at all. You can’t store electricity, for example. As a

result, electricity supplied in, say, six-months’ time is effectively a different com-

modity from electricity available now, and there is no simple link between today’s

price and that of a futures contract to buy or sell at the end of six months. Of course,

12.56.4/51 .125

CHAPTER 27

Managing Risk 763

16

For evidence that the net convenience yield is related to the level of inventories, see M. J. Brennan, “The

Price of Convenience and the Valuation of Commodity Contingent Claims,” in D. Lund and B. Øksendal

(eds.), Stochastic Models and Option Values, North-Holland Publishing Company, Amsterdam, 1991.

Gas oil

Crude oil

0

0.5

1

1.5

2

2.5

3

01/02/85

06/19/85

12/04/85

05/21/86

11/05/86

04/22/87

10/07/87

03/23/88

09/07/88

02/22/89

08/09/89

01/24/90

12/26/90

06/12/91

11/27/91

05/13/92

10/28/92

04/14/93

09/29/93

03/16/94

08/31/94

02/15/95

08/02/95

01/17/96

07/03/96

12/18/96

06/04/97

11/19/97

05/06/98

10/21/98

04/07/99

09/22/99

03/08/00

08/23/00

07/11/90

Weekly net convenience yields, percent

FIGURE 27.1

Weekly percentage net convenience yield (convenience yield less storage costs) for two commodities.

Source: R. S. Pindyck, “The Present Value Model of Rational Commodity Pricing,” Economic Journal 103 (May 1993),

pp. 511–530. We thank Professor Pindyck for updating the data.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

generators and consumers will have their own views of what the spot price is likely

to be when those six months have elapsed, and they may be more or less eager to

fix today the price at which they buy or sell.

764 PART VIII

Risk Management

27.3 FORWARD CONTRACTS

Each day billions of dollars of futures contracts are bought and sold. This liquidity

is possible only because futures contracts are standardized and mature on a lim-

ited number of dates each year.

Fortunately there is usually more than one way to skin a financial cat. If the

terms of futures contracts do not suit your particular needs, you may be able to buy

or sell a forward contract. Forward contracts are simply tailor-made futures con-

tracts. The main forward market is in foreign currency. We will discuss forward ex-

change rates in the next chapter.

It is also possible to enter into a forward interest rate contract. For example,

suppose that you know that at the end of six months you are going to need a

three-month loan. You worry that interest rates will rise over the six-month pe-

riod. You can lock in the interest rate on that loan by buying a forward rate agree-

ment (FRA) from a bank.

17

For example, the bank might offer to sell you a six-

month forward rate agreement on three-month LIBOR at 7 percent.

18

If at the end

of six months the three-month LIBOR rate is greater than 7 percent, the bank will

pay you the difference; if three-month LIBOR is less than 7 percent, you pay the

bank the difference.

19

Homemade Forward Contracts

Suppose that you borrow $90.91 for one year at 10 percent and lend $90.91 for two

years at 12 percent. These interest rates are for loans made today; therefore, they

are spot interest rates.

The cash flows on your transactions are as follows:

17

Note that the party which profits from a rise in rates is described as the “buyer.” In our example you

would be said to “buy six against nine months” money, meaning that the forward rate agreement is for

a three-month loan in six months’ time.

18

LIBOR (London interbank offered rate) is the interest rate at which major international banks in Lon-

don lend each other dollars.

19

Unlike futures contracts, forwards are not marked to market. Thus all profits or losses are settled

when the contract matures.

Year 0 Year 1 Year 2

Borrow for 1 year at 10% 90.91 100

Lend for 2 years at 12% 90.91 114.04

Net cash flow 0 100 114.04

Notice that you do not have any net cash outflow today but you have contracted

to pay out money in year 1. The interest rate on this forward commitment is

14.04 percent. To calculate this forward interest rate, we simply worked out the

extra return for lending for two years rather than one:

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VIII. Risk Management 27. Managing Risk

© The McGraw−Hill

Companies, 2003

In our example you manufactured a forward loan by borrowing short-term and

lending long. But you can also run the process in reverse. If you wish to fix today

the rate at which you borrow next year, you borrow long and lend the money un-

til you need it next year.

11.122

2

1.10

1 .1404, or 14.04%

Forward interest rate

11 2-year spot rate2

2

1 1-year spot rate

1

CHAPTER 27 Managing Risk 765

27.4 SWAPS

Some company cash flows are fixed. Others vary with the level of interest rates,

rates of exchange, prices of commodities, and so on. These characteristics may not

always result in the desired risk profile. For example, a company that pays a fixed

rate of interest on its debt might prefer to pay a floating rate, while another com-

pany that receives cash flows in euros might prefer to receive them in yen. Swaps

allow them to change their risk in these ways.

The market for swaps is huge. In 2000 the total notional amount of swaps out-

standing was estimated at over $50 trillion. The major part of this figure consisted

of interest rate swaps, but it is also possible to swap different currencies, equity in-

dexes, and commodities.

20

We will show first how interest rate swaps work, and

then describe a currency swap. We conclude with a brief look at default swaps. The

default swap is an example of a credit derivative, a relatively new box of tools for

managing risk.

Interest Rate Swaps

Friendly Bancorp has made a five-year, $50 million loan to fund part of the con-

struction cost of a large cogeneration project. The loan carries a fixed interest rate

of 8 percent. Annual interest payments are therefore $4 million. Interest payments

are made annually, and all the principal will be repaid at year 5.

Suppose that instead of receiving fixed interest payments of $4 million a year, the

bank would prefer to receive floating-rate payments. It can do so by swapping the

$4 million, five-year annuity (the fixed interest payments) into a five-year floating-

rate annuity. We will show first how Friendly Bancorp can make its own homemade

swap. Then we will describe a simpler procedure.

The bank can borrow at a 6 percent fixed rate for five years.

21

Therefore, the

$4 million interest it receives can support a fixed-rate loan of mil-

lion. The bank can now construct the homemade swap as follows: It borrows $66.67

million at a fixed interest rate of 6 percent for five years and simultaneously lends

4/.06 $

ˇ 66.67

20

Data on swaps are provided by the Bank for International Settlements (see www.bis.org/statistics).

Equity swaps typically involve one party receiving the dividends and capital gains on an equity index,

while the other party receives a fixed or floating rate of interest. Similarly, in a commodity swap one

party receives a payment linked to the commodity price and the other receives the interest rate.

21

The spread between the bank’s 6 percent borrowing rate and the 8 percent lending rate is the bank’s

profit on the project financing.