ACCA Paper P5 (INT) Advanced Performance management - Pocket notes - Kaplan - 2010

Подождите немного. Документ загружается.

Approaches to budgets

Approaches to budgets Chapter 3

kaplanpublishing 51

Performance evaluation

usingabudgetforperformance•

evaluationcanincreasethe

emphasisonachievementof

targets.

itcanalsoincreasethepotential•

fordysfunctionalperformance.

individualsmayconcentrate•

ontheitemsmeasuredand

rewardedtothedetrimentof

otheritems.

unmeasuredaspectsofthejob•

maybeneglected.

Managerial style

Therearedifferentmanagement•

stylesofbudgetuse:

– budget-constrained,afocus

onachievingshort-term

budgettargets

– profit-conscious,afocusis

onachievinglonger-term

budgettargets

– non-accounting,where

performanceevaluationis

notlinkedtobudgetary

targets.

1

Approaches to budgets

52 kaplanpublishing

Notes:

53

Changes in business

structure and management

accounting

In this chapter

The relevance of traditional management •

accounting.

Performance management in different •

business structures.

Business integration.•

Business process re-engineering.•

Activity-based management.•

Staff empowerment.•

chapter

4

Changes in business structure and management accounting

54 kaplanpublishing

Changes in business structure and management accounting Chapter 4

You need to be able to assess and discuss the relationship between business structure and

management accounting requirements. This may be in the context of a case study.

The relevance of traditional management accounting

Exam focus

Changes in

the business

environment:

Competition•

globalisation•

increased•

complexity

increased•

risk.

newapproachestostrategic•

planning.

awarenessoftheneed•

forclear,sustainable

competitivestrategy.

agreateremphasisonquality.•

adriveforcostreductions.•

useofgreaterautomation•

inmanufacturingsystems.

aneedforgreaterflexibility.•

anincreaseinthestrategic•

significanceofiTandis.

aswitchtomoreflexible•

organisationalforms.

new•

management

accounting

practices.

Changes•

toexisting

practices.

lessrelevance•

oftraditional

methodssuch

asstandard

costing.

leadingto

leadingto

Changes in business structure and management accounting

Changes in business structure and management accounting Chapter 4

kaplanpublishing 55

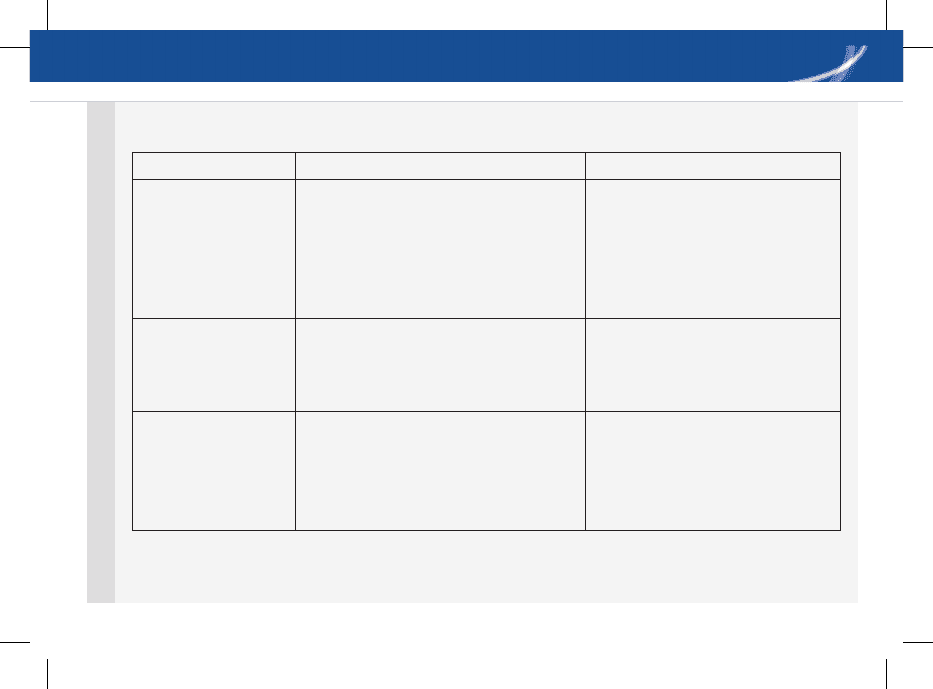

Performance management in different business structures

Functional organisations Divisional organisations

Information needs Centralised.•

Performance information required •

by top of organisation for planning

and control.

Data aggregated at the highest •

level before feedback given.

Decentralised.•

Greater participation lower •

down the organisation.

Information needs to be •

available lower down

organisation.

Advantages for

performance

management

Easier to assess and control •

performance of functions.

Easier to assess divisional/•

SBU performance.

Performance management •

can be tailored to local needs.

Problems for

performance

management

Difficult to assess performance of •

individual products or markets.

Unsuitable for diversified •

organisations.

Transfer pricing issues.•

Issue of allocation of central •

costs.

Potential problems with lack •

of goal congruence.

Changes in business structure and management accounting

56 kaplanpublishing

Changes in business structure and management accounting Chapter 4

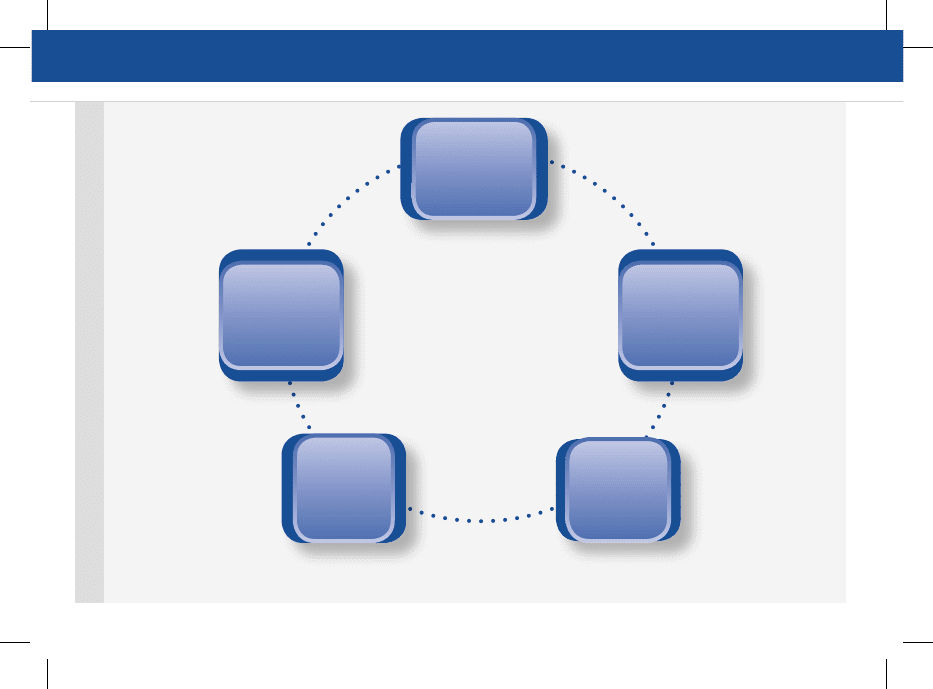

NETWORK

ORGANISATION

Controlis

exercised

through

shared

goals

information

isneededby

thecore

company

systemsneed

tofacilitateco-

ordinationand

communication.

Organisational

structure

isatter

Eachparty

needsfeedback

onitsrelative

performance

Changes in business structure and management accountingChanges in business structure and management accounting Chapter 4

kaplanpublishing 57

Business integration

Business integration means that all aspects

of the business must be aligned to secure

the most efficient use of the organisation’s

resources so that it can achieve its objectives

effectively.

Processes are viewed as complete entities

from initial order to final delivery.

Definition

Changes in business structure and management accounting

58 kaplanpublishing

Changes in business structure and management accounting Chapter 4

Porter’s value chain

The value chain model

Shows how each activity adds to competitive advantage.•

Emphasises linkages and critical success factors within activities and for the value chain as a •

whole.

The value chain

Firminfrastructure

humanresourcemanagement

Technologydevelopment

procurement

Operations service

M

a

R

g

i

n

primaryactivities

support

activities

inbound

logistics

Outbound

logistics

Marketing

andsales

Changes in business structure and management accounting

Changes in business structure and management accounting Chapter 4

kaplanpublishing 59

BPR PROCESS

identification•

rationalisation•

redesign•

reassembly.•

Business process

re-engineering (BPR)

Business process re-engineering is the

fundamental rethinking and radical redesign

of business processes to achieve dramatic

improvements in critical, contemporary

measures of performance, such as cost,

quality, service and speed.

Improved customer satisfaction is often the

primary aim.

Definition

Changes in business structure and management accounting

60 kaplanpublishing

Changes in business structure and management accounting Chapter 4

Advantages Criticisms

Focused on customer needs.•

Provides cost advantages.•

Asks radical questions about •

how processes can be

improved.

Focused on entire processes •

across functional boundaries.

Elimination of unnecessary •

activities.

Common misconceptions of BPR:•

that it is just about making small changes to existing –

processes

that it is a cost-cutting exercise. –

BPR requires major commitment by the whole organisation.•

Needs a focus on the entire process to avoid efficiency •

in one department being improved at the expense of the

whole organisation.

Attention can become diverted from competitors activities •

and market developments.

Some implementations of BPR have just been about •

automation rather than redesign of processes.

Activity-based management

Activity-based costing (ABC)

The practice of attributing overhead costs to products in a manner linked to the activities that •

give rise to the overhead costs (cost drivers) and how far those activities relate to cost units at

the product and batch level.

Definition