ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 315

The purpose of these paragraphs is to provide additional communication in the

audit report when the auditor wishes to draw the attention of users to a particular

matter in the financial statements. They do not modify the audit opinion.

An emphasis of matter paragraph draws the attention of users to an item (or

‘matter’) that is included in the financial statements and which the auditor

considers fundamental to an understanding of the financial statements.

An other matter paragraph deals with a matter which is not included in the

financial statements but which is relevant to an understanding of the audit,

the auditor’s responsibilities or the audit report.

3.3 Emphasis of matter paragraphs

An ‘emphasis of matter’ paragraph is used to draw the reader’s attention to a matter

presented or disclosed in the financial statements which is fundamental to an

understanding of those financial statements.

When an audit report contains an emphasis of matter paragraph, the opinion is not

modified. It can therefore only be used where the auditor has obtained sufficient

appropriate audit evidence that the matter is not materially misstated in the

financial statements. (If the matter is materially misstated, a modified opinion is

required.)

When the auditor includes as emphasis of matter paragraph in the audit report the

auditor is required to:

include it immediately after the opinion paragraph

use the heading ‘emphasis of matter’ for the paragraph (or another appropriate

heading)

include a clear reference to the matter being emphasised and to where relevant

disclosures that fully describe the matter can be found in the financial statements

indicate that his opinion is not modified in respect of the matter being

emphasised.

Circumstances in which an emphasis of matter paragraph may be necessary

ISA 706 gives the following examples of circumstances in which an emphasis of

matter paragraph may be necessary:

Where there is an uncertainty relating to the future outcome of exceptional

litigation or regulatory action.

Where the entity has adopted a new IFRS early and that has had a pervasive

effect on the financial statements.

To draw attention to a major catastrophe that has had, or continues to have, a

significant effect on the entity’s financial position.

Paper P7: Advanced audit and assurance (International)

316 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example: Emphasis of matter paragraph

The following illustrative wording is given in ISA 706.

Emphasis of matter

We draw attention to Note X to the financial statements which describes the

uncertainty related to the outcome of the lawsuit filed against the company by

XYZ company. Our opinion is not qualified in respect of this matter.

ISAs requiring emphasis of matter paragraphs

There are currently two ISAs which require the auditor to use an emphasis of

matter paragraph in certain circumstances.

ISA 560 Subsequent events requires an emphasis of matter paragraph to be used in

two specific circumstances. These were set out in a previous chapter.

ISA 570 Going concern requires an emphasis of matter paragraph to be used to

highlight the existence of a material uncertainty relating to a going concern

problem. The following illustrative wording for this type of emphasis of matter

paragraph is from ISA 570.

(Note that this is only appropriate where the issues relating to the going concern of

the entity are not such that a modified audit report should be given. Such matters

are considered later in this chapter.)

Emphasis of matter

Without qualifying our opinion, we draw attention to Note X to the financial

statements which indicates that the company incurred a net loss of $… during the

year ended 31 December 20X1 and, as of that date, the company’s current

liabilities exceeded its total assets by $…. These conditions, along with other

matters as set forth in Note X, indicate the existence of a material uncertainty

which may cast significant doubt about the company’s ability to continue as a

going concern.

3.4 Other matter paragraphs

As stated above, an ‘other matter’ paragraph is used if the auditor considers it

necessary to communicate a matter other than those included in the financial

statements that, in his opinion, is relevant to users’ understanding of the audit, the

auditor’s responsibilities or the audit report. In this case the auditor is required to:

include the other matter paragraph immediately after the opinion paragraph

(and any emphasis of matter paragraph), or

elsewhere in the report if its content is relevant to the other reporting

responsibilities section.

Circumstances in which an other matter paragraph may be necessary

ISA 706 gives the following examples of circumstances in which an ‘other matter’

paragraph may be necessary:

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 317

Where the auditor is unable to resign from the engagement even though the

possible effect of a limitation of scope imposed by management is pervasive

(relevant to users’ understanding of the audit). This should be rare in practice.

Where local law or custom allows the auditor to elaborate on his

responsibilities in his report (relevant to users’ understanding of the auditor’s

responsibilities or audit report).

3.5 The modified opinion: ISA 705

When the auditor must issue a modified opinion

ISA 705 Modifications to the opinion in the independent auditor’s report requires the

audit to modify his opinion in the audit report in two situations:

Material misstatement. This occurs when the auditor concludes that, based on

the audit evidence obtained, the financial statements as a whole are ‘not free

from material misstatement’. In other words the auditor considers that there is a

material misstatement in the financial statements.

Limitation on scope. This occurs when the auditor is unable to obtain sufficient

appropriate evidence to conclude that the financial statements as a whole are

free from material misstatement. In other words, the auditor has been unable to

obtain sufficient appropriate audit evidence to reach an opinion that the

financial statements give a true and fair view; therefore the financial statements

may contain a material misstatement.

ISA 705 lists three types of modified opinions:

a qualified opinion

an adverse opinion, and

a disclaimer of opinion.

Each of these types of modifications are explained below.

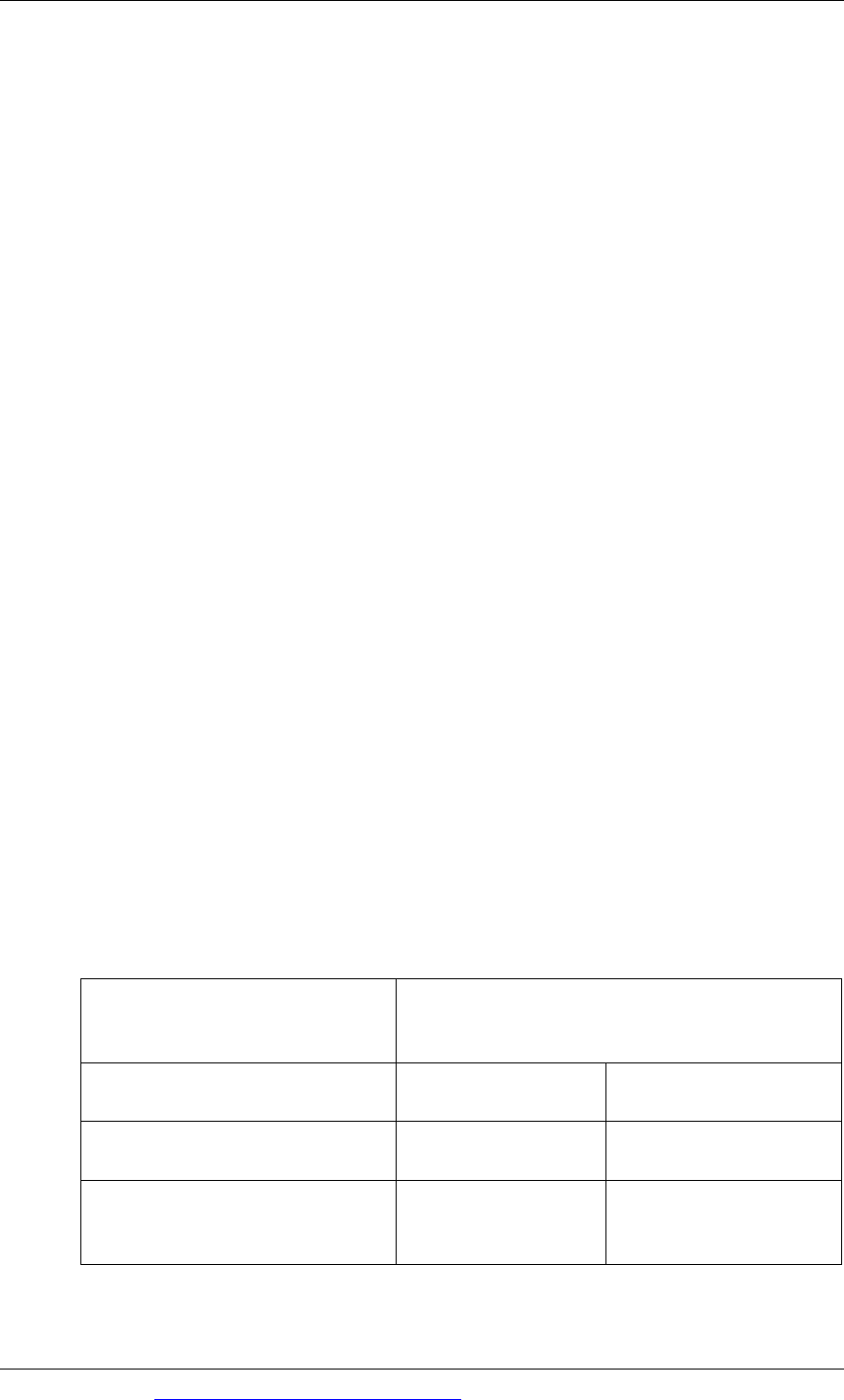

Deciding the type of modified opinion required

The following table from ISA 705 provides a useful summary of when each type of

modified opinion is required to be given in the audit report:

Auditor’s judgement about the pervasiveness

of the effects (or possible effects) on the

financial statements

Nature of matter giving rise to

the modification

Material but not

pervasive

Material and pervasive

Financial statements are

materially misstated

Qualified opinion Adverse opinion

Inability to obtain sufficient

appropriate audit evidence

(limitation on scope)

Qualified opinion Disclaimer of opinion

Paper P7: Advanced audit and assurance (International)

318 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Qualified opinions

A qualified audit opinion should be given when, in the opinion of the auditor, there

is a material misstatement or a limitation on scope, and the effect on the financial

statements is material but not pervasive.

Qualified audit opinions are sometimes called ‘except for’ opinions, because the

audit report should state that in the auditor’s opinion the financial statements give a

true and fair view except for the matter or matters described in the report.

The meaning of pervasive: disclaimer of opinion or adverse opinion

Generally, a matter will be material but not pervasive when the auditor encounters

a material problem with one or more specific items in the financial statements (such

as a problem with inventory or revenue), but the remaining items and the financial

statements as a whole provide a true and fair view.

‘Pervasive’ effects on the financial statements are defined by ISA 705 as those that,

in the auditor’s judgement:

are not confined to specific elements, accounts or items of the financial

statements, or

are confined to specific elements in the financial statements, but these represent

(or could represent) a substantial proportion of the financial statements, or

in relation to disclosures in the financial statements, are fundamental to users’

understanding of those statements.

The difference between a ‘material’ and a ‘pervasive’ modification is a matter of

judgement. There are no absolute cut-off points or dividing lines that separate one

from the other.

Limitations on scope

ISA 705 suggests that a limitation on scope may occur as a result of:

circumstances beyond the control of the entity, such as when the entity’s

accounting records have been destroyed

circumstances relating to the nature or timing of the auditors work: an example

is when the auditor is appointed too late to enable him to attend the physical

inventory count

limitations imposed by management. The management of the client entity may

prevent the auditor from obtaining the audit evidence required, for example by:

- preventing the auditor from observing the physical inventory count

- preventing the auditor from asking for confirmation of specific account

balances (for example, a receivables circularisation).

Management imposed limitations on scope

If, after accepting the engagement, the auditor becomes aware that management has

imposed a limitation on the scope of the audit which is likely to result in a qualified

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 319

or disclaimer of opinion, the auditor is required to ask management to remove the

limitation. If management refuse to do this, the auditor must:

communicate the matter to those charged with governance

consider whether it is possible to perform alternative audit procedures in order

to obtain sufficient appropriate audit evidence.

If it is not possible to obtain audit evidence in another way and the matter is

material but not pervasive the auditor must give a qualified opinion.

If it is not possible to obtain audit evidence in another way and the matter is

material and pervasive the auditor must:

resign from the audit where practicable and not prohibited by law or regulation,

or

if not practicable or possible, issue a disclaimer of opinion.

3.6 Form and content of a modified opinion

The form and content of a modified audit report with a modified opinion differs

from an unmodified audit report in several ways. ISA 705 includes the following

requirements.

Basis for modified opinion paragraph

When a modified opinion is issued, the audit report must include a ‘basis for

opinion’ paragraph, which should appear just before the audit opinion in the report.

The paragraph is headed ‘Basis for qualified opinion’, ‘Basis for adverse opinion’,

or ‘Basis for disclaimer of opinion’, as appropriate. Examples of these types of

opinion are shown later.

This ‘basis for opinion’ paragraph must include the following:

For a material misstatement relating to specific amounts – a description and

quantification of the impact on the financial statements (or a statement that

quantification is not possible).

For a material misstatement relating to narrative disclosures – an explanation of

how the disclosures are misstated.

For a material misstatement relating to the non-disclosure of information that

should have been disclosed – the nature of the omitted information and, unless

prohibited by law or regulation, the omitted disclosures.

If the modification results from an inability to obtain sufficient appropriate

audit evidence – the reasons for that inability.

Opinion paragraph

This paragraph in the audit report must be headed ‘Qualified opinion’, ‘Adverse

opinion’, or ‘Disclaimer of opinion’, as appropriate.

Paper P7: Advanced audit and assurance (International)

320 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Specific wording is prescribed for the different types of modified opinions which is

best illustrated by the examples shown later.

Auditor’s responsibility paragraph

The auditor’s responsibility paragraph appears earlier in the audit report, after the

statement about management responsibilities for the financial statements. For a

qualified or adverse opinion this paragraph is amended to state that the auditor

believes that the audit evidence obtained is sufficient and appropriate to provide a

basis for the modified opinion.

Where there auditor gives a disclaimer of opinion, more extensive amendments are

required by ISA 705.

3.7 Examples of modified opinions

Illustrative examples of the different types of modified opinion are shown below.

They are all taken from ISA 705. Where paragraphs in the examples are incomplete,

the wording of the report commences or concludes in the same way as in the

example of the unmodified report, shown in an earlier section of this chapter.

Example 1: Qualified opinion – limitation on scope

This is an example of a qualified opinion, arising from the auditor’s inability to

obtain sufficient appropriate audit evidence. The only paragraphs from the report

that are shown here are those that are relevant to the modified opinion.

Auditor’sresponsibility

… We believe that the audit evidence that we have obtained is sufficient and

appropriatetoprovideabasisforourqualifiedauditopinion.

Basisforqualifiedopinion

ABCCompany’sinvestmentinXYZcompany,aforeignassociateacquiredduring

the year and accounted for by the equity method, is carried at $XXX on the

statement of financial position at 31 December 20X1, and ABC’s share of XYZ’s

netincomeisincludedinABC’sincomefor

theyearthen ended.Wewereunable

to obtain sufficient appropriate audit evidence about the carrying amount of

ABC’s investment in XYZ at 31 December 20X1 and ABC’s share of XYZ’s net

income for the year because we were denied access to the financial information,

management and the auditors of

XYZ. Consequently, we were unable to

determinewhetheranyadjustmentstotheseamountswerenecessary.

Qualifiedopinion

Inouropinion,exceptforthepossibleeffectsofthematterdescribedintheBasis

for Qualified Opinion paragraph, the financial statements give a true and fair

view….

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 321

Example 2: Qualified opinion – material misstatement

This is an e xample of a qualified opinion, arising from a material misstatement of

the financial statements:

Auditor’s responsibility

… We believe that the audit evidence that we have obtained is sufficient and

appropriate to provide a basis for our qualified audit opinion.

Basis for qualified opinion

The company’s inventories are carried in the statement of financial position at

$XXX. Management has not stated the inventories at the lower of cost and net

realisable value but has stated them solely at cost, which constitutes a departure

from International Financial Reporting Standards. The company’s records

indicate that had management stated the inventories at the lower of cost and net

realisable value, an amount of $XXX would have been required to write the

inventories down to their net realisable value. Accordingly, cost of sales would

have been increased by $XXX, and income tax, net income and shareholders’

equity would have been reduced by $XXX, $XXX and $XXX, respectively.

Qualified opinion

In our opinion, except for the possible effects of the matter described in the Basis

for Qualified Opinion paragraph, the financial statements give a true and fair

view….

Example 3: Disclaimer of opinion – limitation on scope

This is an example of a disclaimer of opinion where the auditor has been unable to

obtain sufficient appropriate audit evidence about a single element of the financial

statements:

This is an example of a disclaimer of opinion where the auditor has been unable to

obtain sufficient appropriate audit evidence about multiple elements of the

financial statements:

We were engaged to audit the accompanying financial statements of ABC

Company….

Management is responsible for…..

Auditor’s responsibility

Our responsibility… International Standards on Auditing. Because of the matter

described in the Basis for Disclaimer of Opinion paragraph, however, we were not

able to obtain sufficient appropriate audit evidence to provide a basis for an audit

opinion.

Basis for disclaimer of opinion

We were not appointed as auditors of the company until after 31 December 20X1

and thus did not observe the counting of physicals inventories at the beginning

Paper P7: Advanced audit and assurance (International)

322 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

and end of the year. We were unable to satisfy ourselves by alternative means

concerning the inventory quantities held at31 December 20X0 and 20X1 which are

stated in the statement of financial position at $XXX and $XXX, respectively. IN

addition, the introduction of a new computerised accounts receivable system in

September 20X1 resulted in numerous errors in accounts receivable. As of the date

of our audit report, management was still in the process of rectifying the system

deficiencies and correcting the errors. We were unable to confirm or verify by

alternative means accounts receivable included in the statement of financial

position at a total amount of $XXX as at 31 December 20X1. As a result of these

matters, we were unable to determine whether any adjustments might have been

found to be necessary in respect of recorded or unrecorded inventories and

accounts receivable, and the elements making up the income statement, statement

of changes in equity and statement of cash flows.

Disclaimer of opinion

Because of the significance of the matter described in the Basis for Disclaimer of

Opinion paragraph, we have not been able to obtain sufficient appropriate audit

evidence to provide a basis for an audit opinion. Accordingly, we do not express

an opinion on the financial statements.

Example 4: Adverse opinion – material misstatements

Thisisanexampleofanadverseopinionisofagroupauditreport.Althoughgroup

auditreportsarenotexaminableinthispaper,itstillprovidesausefulillustration:

Auditor’s responsibility

… We believe that the audit evidence that we have obtained is sufficient and

appropriate to provide a basis for our adverse audit opinion.

Basis for adverse opinion

As explained in Note X, the company has not consolidated the financial

statements of subsidiary XYZ Company it acquired during 20X1 because it has

not yet been able to ascertain the fair values of certain of the subsidiary’s material

assets and liabilities at the acquisition date. This investment is therefore

accounted for on a cost basis. Under International Financial Reporting Standards,

the subsidiary should have been consolidated because it is controlled by the

company. Had XYZ been consolidated, many elements in the accompanying

financial statements would have been materially affected. The effects on the

financial statements of the failure to consolidate have not been determined.

Adverse opinion

In our opinion, because of the significance of the matter discussed in the Basis for

Adverse Opinion paragraph, the consolidated financial statements do not give a

true and fair view….

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 323

3.8 Deciding to give a modified opinion

The auditor will give a modified opinion only if he is satisfied that:

the reasons for giving a modified opinion are justified, and

the management of the client entity are unable or unwilling to take action to

remove the necessity for a modified opinion.

For example, suppose that the management of a client entity decides that a material

non-current asset should not be depreciated. The auditor should first of all satisfy

himself that there is no acceptable reason for the management’s view, and that the

asset should be depreciated.

The auditor should review the audit file and check for any information about

this matter from previous audits.

He should consider whether there might be an acceptable reason for a departure

from the requirements of international financial reporting standards and GAAP,

in order to give a true and fair view.

If the auditor is still satisfied that management is incorrect in their opinion, he

should meet with the management and:

Discuss their reasons for not depreciating the asset

Obtain a representation from them confirming that the asset will not be

depreciated

Decide whether the effect of this action by management on the financial

statements is material or ‘material and pervasive’ and so what form of modified

opinion is necessary

Warn management that the audit opinion will be modified unless management

change their view

If management still refuse to change their view, issue a modified opinion, which

will be either a qualified opinion or an adverse opinion.

3.9 Audit reports and the exam

For the exam, you may be expected to study an audit report that contains errors and

identify and explain what those errors are. Alternatively, you may be asked to

discuss what audit opinion would be appropriate.

The key issues to consider are as follows.

Do the financial statements give a true and fair view? (Misstatements do not

affect the true and fair view if they are immaterial.)

If they do, the audit opinion will be unmodified.

If the draft financial statements give a true and fair view, is there any item that

justifies an ‘emphasis of matter’ paragraph? Usually, an emphasis of matter

paragraph is something that could affect the going concern assumption.

If the financial statements do not give a true and fair view, what is the item of

contention? Is it something that involves a disagreement with management (a

misstatement) or is there inadequate audit evidence (a limitation on scope)?

Paper P7: Advanced audit and assurance (International)

324 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Is the matter material but not pervasive? If so, a qualified audit opinion is

appropriate (‘except for…’).

If the matter is material and pervasive, either an adverse opinion or a disclaimer

of opinion is appropriate. (These are rare in practice, but of course they could

feature in an exam question!)

Here are some examples.

Example 1

You are the manager in charge of the audit of Colorosso, a limited liability company.

Your auditors’ report for the previous financial year to 31 December Year 7 was

signed, without modification, in February Year 8.

The scope of the audit for the year to 31 December Year 8 has been limited. This is

because the company’s chief executive officer fled the country in April Year 8,

taking the accounting records with him.

You have identified a valuable training opportunity for Robin, one of your audit

team. As a training exercise, you have asked Robin to draft the extracts for the basis

of opinion and opinion paragraphs that would not be standard wording in an

unmodified auditor’s report.’

Robin’s draft extracts were produced as follows:

‘Basis of opinion (extract)

However, the evidence available to us was limited because accounting records were

missing at the beginning of the year and it was not possible to reconstruct them

completely.

Opinion (extract)

Because of the possible effect of the limitations in the information available to us, we

do not express an opinion on the financial statements.’

Requirement

(a) Identify and comment on the principal matters relevant to forming an

appropriate opinion on the financial statements of Colorosso for the year

ended 31 December Year 8.

(b) Discuss the suitability of Robin’s draft extracts.

Answer

Tutorial note

To answer this requirement, you need to:

identify the principal matters relevant to forming an appropriate opinion

comment on these matters

identify whether Robin’s report indicates that Robin has identified and

considered these matters