ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Chapter 12: Assurance services

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 285

Date, address and signature of the accountant/auditor.

Example: report on PFI

An audit firm has been the auditor of Entity AZ for a number of years.

REPORT ON A FINANCIAL FORECAST

To the Board of Directors of The Penguin Company

We have examined the profit forecast for the year to 31

st

December 20X6 set out

on pages… to… Our examination was made in accordance with International

Standard on Assurance Engagements 3400.

Management is responsible for the forecast, including the assumptions set out

in Note XX on which the forecast is based.

Based on our examination of the evidence supporting the assumptions, nothing

has come to our attention that causes us to believe that these assumptions do

not provide a reasonable basis for the forecast. Further, in our opinion, the

forecast is properly prepared on the basis of the assumptions.

Actual results are likely to be different from the forecast, since anticipated

events frequently do not occur as expected and the variation may be material.

Auditor

Address

Date

The auditor may not be in a position to issue an unqualified report. In these

circumstances, and after due consideration, the auditor may issue:

a qualified report, or

an adverse report, or

he may decide to withdraw from the engagement.

Example: qualified report on PFI

REPORT ON A FINANCIAL PROJECTION

To the Board of Directors of The Pen and Pencil Supply Company

We have examined the projection of the profits of the Pen and Pencil Supply

Company for the five years ended 31

st

December 20X9 set out on pages… to… of

this document in accordance with International Standards on Assurance

Engagements applicable to the examination of prospective financial information.

Management is responsible for the projection, including the assumptions set

out in Note XX on which the projection is based.

Paper P7: Advanced audit and assurance (International)

286 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The projection has been prepared for the purpose of a loan application to the

XYZ National Bank.

As the loan is to be used to finance a new international venture to be undertaken

by the company in an emerging market, the projection has been made using a set

of assumptions, including hypothetical assumptions about future events and

management actions that are not necessarily expected to occur. As a result,

readers are warned that the projections may not be appropriate for purposes

other than that described above.

Based on our examination of the evidence supporting the assumptions, nothing

has come to our attention that causes us to believe that these assumptions do

not provide a reasonable basis for the projection, assuming that market share of

3% per annum is gained over the five year period. Further, in our opinion, the

projection is properly prepared on the basis of the assumptions and is

presented in accordance with generally accepted accounting principles.

Even if the events anticipated under the hypothetical assumptions described

above occur, actual results are likely to be different from the projection, since

other anticipated events frequently do not occur as expected and the variation

may be material.

Auditor

Address

Date

Chapter 12: Assurance services

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 287

Forensic audits

Forensic accounting, forensic investigations and forensic auditing

The nature of forensic investigations and audits

Application of ethical principles to forensic investigations

Procedures in forensic investigations

Reporting on forensic audits

5 Forensic audits

5.1 Forensic accounting, forensic investigations and forensic auditing

In general terms, ‘forensic’ means used in connection with courts of law. In

accounting, the term ‘forensic’ therefore refers to the use of accounting information

for legal purposes, in the resolution of legal disputes or in disputes that are resolved

by a court of law. It may be used in both criminal cases (for example fraud cases)

and civil cases.

Forensic accounting

Forensic accounting involves preparing financial information for use as evidence by

a court of law. Examples include the provision of financial information relating to:

loss of earnings

settlement of a legal dispute involving the valuation of a business

losses relating to an insurance claim

a divorce settlement.

There are two aspects to forensic accounting:

forensic investigations

forensic audits.

Forensic investigations

A forensic investigation is a forensic audit carried out in response to a suspicion of

wrong-doing, usually to prove or disprove certain assumptions, for example, ‘X

person is carrying out a fraud’ or ‘Y person was negligent in carrying out that piece

of work’.

The objective of a forensic investigation is to obtain evidence that might be used in

legal proceedings to resolve a dispute or prove innocence/guilt in a criminal case,

such as providing evidence of money laundering.

Often forensic investigations are usually reactive, meaning that they seek to prove

or disprove suspicions of wrongdoing and provide evidence for legal proceedings.

Paper P7: Advanced audit and assurance (International)

288 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

However, investigations can also be proactive or preventative. Techniques of

forensic auditing can be used to identify risks of wrongdoing and then steps can be

taken to improve the situation.

Forensic audit

Forensic audit is an element in forensic investigations. It refers to the methods and

procedures used to obtain audit evidence in a forensic investigation. Forensic

auditing may be defined as the process of:

gathering, analysing and reporting on data, much of it financial in nature, in the

pre-defined context of legal dispute or investigation into suspected irregularities

and

in some cases, giving preventative advice in this area..

The terms ‘forensic accounting’, ‘forensic investigations’ and ‘forensic audits’ are

closely connected, and an exam question may refer to any of these three terms.

5.2 The nature of forensic investigations and audits

Forensic investigations and audits are associated with situations where disputes

arise or wrongdoing has occurred such that criminal or civil action is being taken in

a court of law. The following general areas may give rise to forensic auditing:

Fraud investigation

Negligence investigation

Insurance claims, and the assessment of losses.

In any of the above examples, a forensic accountant might be called on by the court

to act in the capacity of expert witness, providing evidence to that court on the

financial implications of a situation, or on whether there is evidence to substantiate

claims of fraud or negligence.

Example: fraud investigation

In the case of a fraud investigation, a forensic accountant may be engaged to:

investigate whether fraud has actually occurred, and if so to obtain evidence to

support that assertion in a court of law

identify the individual or individuals who have committed the fraud, and obtain

evidence that can be used in a court of law to link them to the fraud: this work

will also involve obtaining evidence to show how the individual or individuals

had an opportunity to commit the fraud

estimate the financial loss that has occurred because of the fraud.

The forensic accountant is not a policemen and it is not his job to prosecute

individuals for alleged fraud. However, he will be engaged by the criminal

investigation authorities to obtain evidence that can be used to pursue a criminal

prosecution (or to conclude that sufficient evidence cannot be obtained).

Chapter 12: Assurance services

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 289

5.3 Application of ethical principles to forensic investigations

The ethical principles set out earlier apply to accountants carrying out forensic work

as they do to accountants in every situation.

Integrity. In legal disputes and criminal investigations, individuals may be

dishonest and tell lies. However the forensic accountant must act with integrity

and honesty at all times.

Objectivity. The forensic accountant is paid by a client to carry out an

investigation, and the client will presumably be hoping for a particular outcome

to the investigation. For example in a fraud investigation, the criminal

investigators who use a forensic accountant may be hoping for evidence of guilt.

However the forensic accountant must remain independent (in spite of the

advocacy threat) and should seek to obtain evidence to reach a fair opinion.

Professional competence and due care. Forensic accounting is a specialised area

of work, and individuals should be sufficiently competent to do the work.

Confidentiality. The normal ethical rule is that accountants should maintain

client confidentiality, and should not disclose information without the client’s

consent. An exception is that the duty of confidentiality is overridden by the

requirement to provide evidence when requested to a court of law. Legal

requirements for disclosure override the rules of client confidentiality.

Professional behaviour. Forensic accountants often appear as witnesses in court,

ad in the public eye they should display professional behaviour and act in a way

that is not detrimental to the image of the accounting profession.

There are some particular considerations that accountants will have to bear in mind

when carrying out forensic work:

to whom a duty of confidentiality is owed (particularly when acting as an expert

witness in relation to both sides of a legal claim)

duties to the court

legal privilege in the context of money laundering.

This last area is a particularly important one for forensic accountants. Most

accountancy work, for example, auditing or accounts preparation, gives rise to the

duties to report suspicions of money laundering.

However, when an accountant is working in a legal capacity, it may be that

information obtained during the course of that work is subject to legal privilege. If

so the accountant would be wrong to make a report of suspicion of money

laundering. Whether or not legal privilege applies in a particular situation is a

complicated question, and the accountant should take legal advice on his position.

5.3 Procedures in forensic investigations

The procedures that a forensic accountant will carry out will depend on the terms

and the objectives of the engagement.

In many cases, procedures will be similar to auditing procedures and will depend

on exactly what is being proved or disproved. In others, the accountant may be

preparing financial information from a number of sources to substantiate a claim.

Paper P7: Advanced audit and assurance (International)

290 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

In the exam you may be asked to describe the procedures in a forensic investigation.

In answering a question on this topic, it may be useful to think about the elements in

a normal audit investigation:

Establish the objectives of the investigation.

Plan the investigation with a view to achieving the objectives. For example in an

investigation into suspected fraud, the auditor should plan how to establish

whether fraud has occurred, how it could have happened and how long has it

been going on – as well as who has committed the fraud and how much has

been lost.

The audit work should therefore be planned in a way that will provide sufficient

appropriate evidence to achieve the objectives of the audit. The evidence should

be strong enough to ‘stand up’ in court if required: in fraud cases, audit evidence

should therefore try to establish a motive for the alleged fraudster, identify the

opportunity that the fraudster had to commit the fraud and also any evidence of

measures by the fraudster to conceal his crime.

Note that audit evidence may be gathered in various ways – similar to the

methods used in a normal audit. This includes interviewing individuals

(including individuals suspected of fraud).

The auditor should use the evidence obtained to reach an opinion. If the

evidence is insufficient, he should try to obtain additional evidence.

At the end of the investigation a report is prepared for the client.

Examples

If an accountant is asked to give evidence of whether an audit file has been prepared

negligently, he will review the file comparing the procedures carried out with the

requirements of auditing standards.

If an accountant is asked to give evidence of whether inventory has been

misappropriated, he may carry out analytical review (comparing margins year on

year), he may carry out tests on cut-off and inventory counting to ensure that the

figures are not misstated (giving the impression of a fraud), he may carry out tests

of controls to establish whether they are capable of preventing frauds and whether

they have been applied.

5.4 Reporting on forensic audits

Key issues in reporting will be:

Whom the report is intended for and restriction of liability to other parties

The type of assurance required (as for any assurance engagement, this will affect

the level of evidence obtained)

What purpose the report is required for, for example, to substantiate an

insurance claim or to provide evidence to a court of law

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 291

Paper P7 (INT)

Advanced audit and assurance

CHAPTER

13

Internal audit and outsourcing

Contents

1 The nature and development of internal auditing

2 Types of internal audit

3 Outsourcing

Paper P7: Advanced audit and assurance (International)

292 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The nature and development of internal auditing

Definition of internal audit

Reasons for the development of internal auditing

Typical functions of internal audit

Comparison of external and internal audit

1 The nature and development of internal auditing

1.1 Definition of internal audit

The role of the internal audit function has been defined as:

‘….an appraisal system established by management for the review of the accounting and

internal control systems as a service to the entity.’

There are several parts to this definition:

Internal auditing is an appraisal system.

It is established by management as a service to the entity.

It involves the review of accounting systems.

It also involves the review of internal control systems, which are systems for

financial controls, operational controls and compliance controls.

Internal auditing is a separate and distinct branch of the accounting profession. The

role of internal auditing has become more significant in larger entities and is now

seen as an important management tool.

1.2 Reasons for the development of internal auditing

The main reasons for the importance of the internal audit function are as follows:

Internal audit helps management to monitor the controls within their entity. As

entities increase in size and complexity, and become global in nature, the task of

monitoring controls becomes more difficult. An internal audit function helps

management to monitor these controls.

Similarly, as markets become increasingly competitive, it is important that

entities should be very competitive themselves. This means using resources

efficiently and effectively. An internal audit function can be used to monitor the

efficiency of operations.

In many countries there is a large amount of statutory and accounting

regulation, including corporate governance regulation. An internal audit

function can be used by management to check on compliance with laws and

regulations.

Chapter 13: Internal audit and outsourcing

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 293

Many entities use complex IT systems. Specialist internal auditors can help

management to review the effectiveness of controls within IT systems (by means

of IT audits).

The increasing cost of the external auditor’s services means that it may be

cheaper to use internal auditors to perform audit tasks whenever possible. (The

reliance of external auditors on work done by internal auditors is considered

later. However, an internal audit department may be used for work not related

to the external audit that might otherwise be given to an external firm of

accountants as non-audit work.)

There is no legal requirement for an entity to establish an internal audit function.

The fact that many organisations do so indicates that there are significant benefits to

be gained.

For companies that operate over multiple sites, internal audit may be an essential

tool for effective management. Senior management can use an internal audit

department to carry out ‘external’ checks on its operational departments. Random

visits or surprise visits by internal auditors may be used to confirm that all locations

are applying internal controls properly, and are complying with relevant laws and

regulations. The largest locations, or locations where there is a high risk of control

failure, may be visited more frequently by the internal auditors.

1.3 Typical functions of internal audit

The scope and objectives of internal audit vary widely, and depend on:

the size and structure of the entity, and

the requirements of its management.

However, internal audit activities usually include one or more of the following:

Monitoring of internal control. Senior management need to reassure themselves

that internal controls are functioning effectively. In a large organisation, they do

not have the time to carry out this task personally, for example through

observation. Monitoring controls, and making sure that the controls are working

properly, needs attention on a continuous basis. An internal audit department is

usually given the specific responsibility by management for reviewing controls,

monitoring their operation and recommending improvements.

Examination of financial and operating information. An internal audit

department might be given the responsibility for a detailed examination of

financial and operating information, and in particular, its reliability and

usefulness. Internal auditors may investigate how information is identified,

measured, classified and reported, and recommend improvements where

appropriate. The audit work may involve investigations into specific items of

information, including the detailed testing of transactions, balances and

procedures.

Review of the economy, efficiency and effectiveness of operations, including

non-financial controls of an entity. Audits of economy, efficiency and

effectiveness can be carried out on any aspect of operations, and are usually

called value for money (VFM) audits.

Paper P7: Advanced audit and assurance (International)

294 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Review of compliance. Senior management may ask the internal auditors to

check that operational departments are complying properly with certain laws,

regulations and other external requirements, or with management policies and

directives and other internal requirements. These investigations are often called

‘compliance audits’.

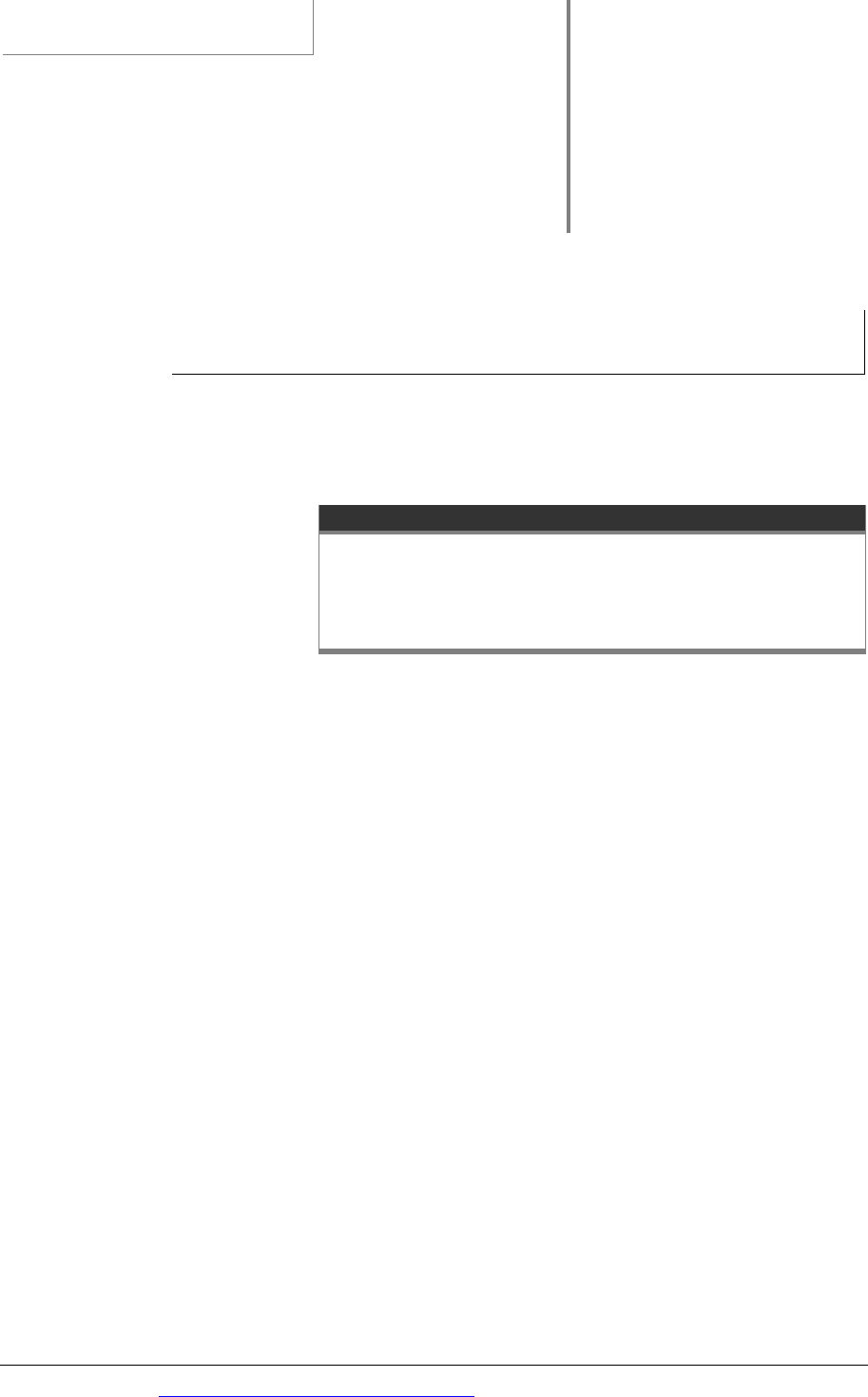

1.4 Comparison of external and internal audit

Internal and external auditors will often carry out their work using similar

procedures. However, there are a number of fundamental differences between the

two audit roles. These are summarised in the following table:

Factor External audit Internal audit

Role

To express an opinion on the

truth and fairness of the

annual financial statements

To examine systems and

controls and assess risks in

order to make

recommendations to

management for

improvement.

Qualification to

act

Set out by statute. No statutory requirements –

management select a suitably

competent person.

Appointed by

The shareholders Management

Duties set out

by

Statute Management

Report to

The shareholders Management