ACCA P7 (INT) Advanced Audit & Assurance - Study Text - 2010 (Emile Woolf Publishing)

Подождите немного. Документ загружается.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 335

by-product of a statutory audit, and is not the result of a full review of systems and

controls. As a consequence, other weaknesses may exist that are not mentioned in

the report.

The auditor will also usually state that such communication has been provided for

the purposes of those charged with governance, and that it may not be suitable for

other purposes.

7.2 The management letter

Although now a requirement of both ISA 315 and ISA 265, the management letter

or letter of weakness has long been seen as an extra service provided to the client

by the external auditor. If management address the points in the letter, the controls

in place will be improved. This may enable future audits to focus on the more

efficient systems-based approach. This in turn may reduce the cost of the audit to

the client.

The report is prepared and sent after the results of the tests of control are known –

usually after the interim audit.

The report may later be updated after the final audit, if further weaknesses have

been found, or if weaknesses that were reported to previously have not yet been

dealt with.

In line with ISA 265’s requirement to give a description of the deficiencies and an

explanation of their potential effects, the report will usually identify the following

information for each weakness reported:

The nature of the weakness in the present system, in terms of both design and

operation. (In other words, is there a control weakness ‘on paper’? If there is no

control weakness ‘on paper’, are the controls applied effectively in practice?)

The implication of this weakness in controls.

Recommendations for improvement.

The auditor should ask management to provide a response and action plan for each

weakness identified in the report. He should also mention that the contents of the

report will be followed up in future audits.

Paper P7: Advanced audit and assurance (International)

336 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Special purpose audit reports

Introduction

The summary financial statement

Revised accounts

Distributions following an audit qualification

ISA 800 Audits of financial statements prepared in accordance with special

purpose frameworks

8 Special purpose audit reports

8.1 Introduction

The external auditor may be called upon to report on the contents of documents

other than the annual financial statements of an entity. For the purposes of your

examination, you need to be aware of the reporting principles in relation to:

summary financial statements

revised accounts

distributions following an audit qualification.

The relevant ISAs are:

ISA 800 Special considerations – audits of financial statements prepared in accordance

with special purpose frameworks

ISA 810 Engagements to report on summary financial statements

although only ISA 800 is listed as examinable.

8.2 The summary financial statement

Many local jurisdictions allow entities to provide certain users, perhaps employees,

with financial statements in a summarised form. These summarised statements

present only the main aspects of the entity’s financial performance and financial

position. The entity may ask its auditors to issue a report on these statements to add

credibility to the information contained in the document. ISA 810 Engagements to

report on summary financial statements provides guidance on this area.

The objectives of the auditor, per ISA 810 are to:

determine whether it is appropriate to accept the engagement to report on

summary financial statements (SFS)

and, if engaged to:

- form an opinion on the SFS based on evidence obtained, and

- express that opinion clearly in a written report that also describes the basis

for that opinion.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 337

Requirements of ISA 810

The auditor should not report on the SFS unless he has already issued an opinion

on the full financial statements from which the SFS are derived.

Before accepting an engagement to report on SFS the auditor should:

decide whether the criteria applied by management in the preparation of the SFS

are acceptable

obtain management’s agreement that it is responsible for:

- preparing the SFS in accordance with the above criteria

- making the “full” (i.e. audited) financial statements available to the users of

the SFS

- including the auditor’s report on the SFS in any document which contains

the SFS.

The “applied criteria” may be established by law or regulation. For example, in the

UK the criteria would be the relevant sections of the Companies Act 2006.

The auditor should perform the following procedures as a basis for his opinion on

the SFS:

Evaluate whether the SFS adequately disclose:

- their summarised nature and identify the full financial statements

- the criteria applied in the preparation of the SFS.

When the SFS are not accompanied by the full financial statements, consider

whether the SFS describe clearly where the full financial statements are available

or the law or regulation which states that they need not be.

Compare the SFS to the full financial statements to ensure they agree with or can

be derived from the latter.

Evaluate whether:

- the SFS have been prepared in accordance with the applied criteria

- the SFS contain sufficient information so as not to be misleading

- the full financial statements are readily available (unless not required to be).

Where the auditor is able to give an unmodified opinion on the SFS one of the

following phrases should be used:

“The SFS are consistent, in all material respects, with the audited financial

statements, in accordance with [applied criteria]”, or

“The SFS are a fair summary of the audited financial statements, in accordance

with [applied criteria]”.

The term ‘true and fair’ (or its equivalent) is not used in the report, because the SFS

will not contain all the information required by a recognised financial reporting

framework.

Paper P7: Advanced audit and assurance (International)

338 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The auditor’s report on the SFS should include the following elements:

Title

Addressee

An introductory paragraph that:

- identifies the SFS on which the auditor is reporting

- identifies the full financial statements

- refers to the auditor’s report on the above, its date and the type of opinion

given in that report (e.g. unmodified)

- (if the report on the SFS is dated later than the audit report on the full

financial statements – note that it cannot be dated earlier) states that nether

set of financial statements reflects the effect of events that occurred after the

date of the audit report on the full financial statements

- states that the SFS do not contain all the disclosures required by the

financial reporting framework applied in the preparation of the full

financial statements and that reading the SFS is no substitute for reading

the full financial statements.

A description of management’s responsibility for the SFS (the preparation of the

SFS in accordance with the applied criteria).

A statement that the auditor is responsible for expressing an opinion on the SFS

based on the procedures required by this ISA.

An opinion.

Date of the report.

Auditor’s address.

Auditor’s signature.

Note that the auditor might have issued a qualified opinion on the full financial

statements or used an emphasis of matter or other matter paragraph but may

nevertheless be satisfied with that the SFS are properly derived from those full

financial statements. In this situation, the auditor’s report should also describe:

the basis for the opinion

any effect of the opinion on the SFS.

If the opinion was an adverse or disclaimer of opinion the auditor’s report on the

SFS should state that it is inappropriate to express an opinion on the SFS.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 339

Example

An example of a report on SFS is set out below. This example is based on

circumstances where an unmodified opinion was expressed on the full financial

statements and the auditor’s report on the SFS is dated later than the “full” auditor’s

report.

REPORT OF THE INDEPENDENT AUDITOR ON THE SUMMARY FINANCIAL

STATEMENTS

[Appropriate Addressee]

The accompanying summary financial statements, which comprise the summary

statement of financial position as at 31

st

December

20X1, the summary statement

of comprehensive income, summary statement of changes in equity and summary

statement of cash flows for the year then ended, and related notes, are derived

from the audited financial statements of ABC Company for the year ended 31

st

December 20X1. We expressed an unmodified audit opinion on those financial

statements in our report dared 15

th

February 20X2. Those financial statements,

and the summary financial statements, do not reflect the effects of events that

occurred subsequent to the date of our report on those financial statements.

The summary financial statements do not contain all the disclosures required by

[describe financial reporting framework applied in the preparartion of the audited

financial statements]. Reading the summary financial statement, therefore, is not a

substitute for reading the audited financial statements of ABC Company.

Management’s responsibility for the summary financial statements

Management is responsible for the preparation of a summary of the audited

financial statements in accordance with [decribe established criteria].

Auditor’s responsibility

Our responsibility is to express an opinion on the summary financial statements

based on our procedures, which were conducted in accordance with International

Standard on Auditing 810 “Engagements to report on summary financial

statements”.

Opinion

In our opinion, the summary financial statements derived from the audited

financial statements of ABC Company for the year ended 31

st

December 20X1.are

consistent, in all material respects, with those financial statements.

[Auditor’s signature]

[Date]

Auditor’s address

8.3 Revised accounts

On rare occasions, it may be discovered that there are defects in audited financial

statements which have already been presented to the shareholders of the company.

When this happens, national laws or regulations may or may not allow the incorrect

financial statements to be revised.

Paper P7: Advanced audit and assurance (International)

340 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Revisions should relate to:

matters arising before the original accounts were approved

that result from fundamental errors of fact.

Any revision that is made may take the form of:

withdrawing the original financial statements and issuing a revised version, or

making the necessary revision in a supplementary note to the financial

statements.

The duties of the auditor in respect of revised accounts are to ensure that:

the revisions comply with the appropriate accounting framework, and

there is good reason for the revision, and

the revised accounts show a true and fair view.

Audit procedures in relation to checking revised accounts might include the

following:

The auditor should assess the nature of the revision, and the audit work

necessary to reach an audit conclusion.

The auditor should obtain audit evidence relating to the adjustments that have

been necessary to make the revision.

The auditor should perform a final review of the revised financial statements.

The auditor should also consider any legal implications or other implications of

the revision.

Revisions to financial statements require a revision to the opinion paragraph in the

audit report, as illustrated below.

In our opinion, the revised financial statements give a true and fair view as at the

date the original financial statements were approved, of the financial position of

the company as of ……………………

8.4 Distributions following an audit qualification

Although national laws vary in detail, there is a general principle that companies

may only distribute as dividends ‘profits available for distribution’.

‘Profits available for distribution’ will generally consist of the excess of accumulated

realised profits over accumulated realised losses. They will normally be determined

by reference to the latest audited accounts. If there is a modification to the audit

opinion on those accounts, local law will often require the directors to ask the

auditors to state whether, in their opinion, the modification is material for deciding

whether the proposed distribution is lawful.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 341

Example

A company has distributable profits of $2 million

The directors have refused to write off trade receivables of $0.3 million.

As a result the auditor has given a qualified opinion.

The directors wish to pay a dividend of $1.5 million.

Although the opinion was qualified, the matter is not material for deciding whether

the proposed dividend is lawful. Even if the directors had written off these

receivables, there would still be sufficient profits for the dividend to be paid.

A report would therefore be issued as set out below.

AUDITORS' STATEMENT TO THE MEMBERS OF ………

We have audited the financial statements of ……………………..….. for the year

ended 31

st

December 20X6 in accordance with International Standards on

Auditing …………………. and have expressed a qualified opinion thereon in our

report dated …….

Basis of opinion

We have carried out such procedures as we consider necessary to evaluate the

effect the qualified opinion has for the determination of profits available for

distribution.

Opinion

In our opinion, this qualification is not material for the purpose of determining

whether the distribution of $….……. proposed by the company is permitted

under (reference to local law).

Auditor

Address

Date

8.5 ISA 800 Audits of financial statements prepared in accordance with

special purpose frameworks

ISAs in the 100 to 700 series apply to an audit of financial statements. ISA 800 deals

with special considerations in the application of those ISAs to an audit of financial

statements prepared in accordance with a special purpose framework.

Although such special considerations cover:

acceptance of the engagement

planning and performance of the engagement, and

forming an opinion and reporting on the engagement

Paper P7: Advanced audit and assurance (International)

342 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

the bulk of the ISA is concerned with reporting. An audit report on such financial

statements will add credibility to those financial statements.

Considerations when accepting the engagement

The auditor is required to determine the acceptability of the financial reporting

framework applied by obtaining an understanding of:

the purpose for which the financial statements have been prepared

the intended users of those financial statements

the steps taken by management to determine that the framework is acceptable in

the circumstances.

The special purpose framework could be a fair presentation framework or a

compliance framework, as discussed under ISA 700 above.

Considerations when planning and performing the audit

ISA 200 requires the auditor to comply with all ISAs relevant to the audit. ISA 800

requires the auditor to determine whether any special consideration is needed.

ISA 315 requires the auditor to obtain an understanding of the entity’s selection and

application of accounting policies. If the special purpose financial statements have

been prepared in accordance with the provisions of a contract then ISA 800

requires him to obtain an understanding of any significant interpretation of the

contract that management has made in the preparation of those financial statements.

Forming an opinion and reporting considerations

When forming an opinion and reporting on special purpose financial statements the

auditor is required to follow ISA 700 and other relevant reporting ISAs. The table

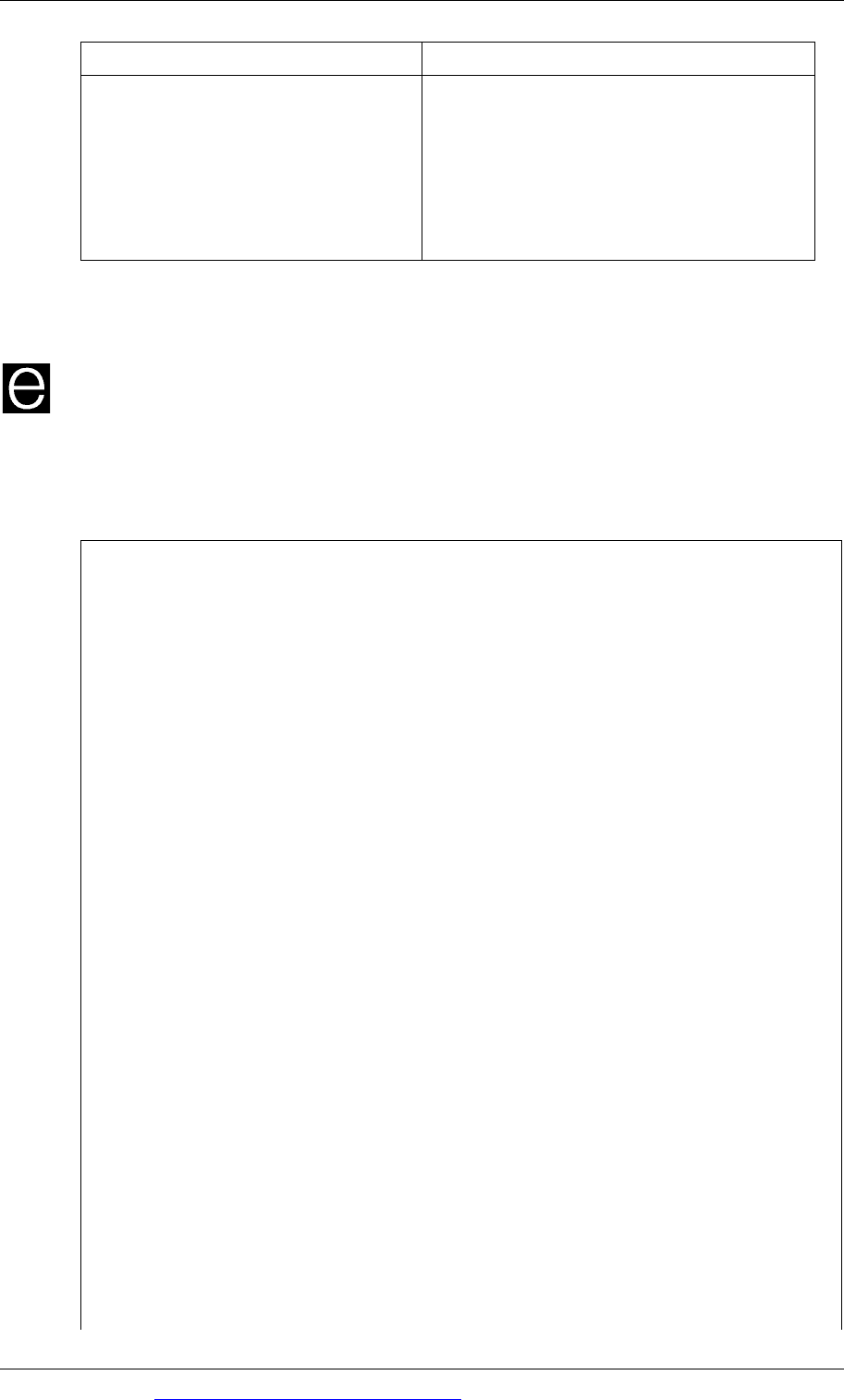

below shows how the requirements of ISA 700 (and ISA 706) are applied by ISA 800.

ISA 700/706 requirements How applied by ISA 800

The auditor must evaluate whether

the financial statements adequately

refer to or describe the applicable

financial reporting framework (ISA

700).

For financial statements prepared in

accordance with the provisions of a

contract the auditor must evaluate

whether the financial statements

adequately describe any significant

interpretations of the contract on which

the financial statements are based.

Provisions covering the form and

content of audit reports (ISA 700)

The report must also describe the

purpose for which the financial

statements are prepared and, if

necessary, the intended user (or refer to a

note which gives that information).

If management has a choice of financial

reporting frameworks in this instance,

the section on management’s

responsibilities must refer to its

responsibility for making an acceptable

choice.

Chapter 14: Reporting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 343

ISA 700/706 requirements How applied by ISA 800

Use of an emphasis of matter

paragraph (ISA 706)

The report must include an emphasis of

matter paragraph alerting users to the

fact that the financial statements have

been prepared in accordance with a

special purpose framework and that, as a

result, they might not be suitable for

another purpose.

The example report below shows how the usual ISA 700 report would be adapted

for a report on special purpose financial statements.

Example

An example of an audit report on special purpose financial statements prepared in

accordance with the financial reporting provisions established by a regulator (in this

example a fair presentation framework) is set out below. The additional wording,

per ISA 800, is shown in square brackets.

INDEPENDENT AUDITOR’S REPORT

(Appropriate addressee)

Report on the financial statements

We have audited the accompanying financial statements of ABC Company, which

comprise the statement of financial position as at December 31

st

, 20X7, and the

statement of comprehensive income, statement of changes in equity, and statement of

cash flows for the year then ended, and a summary of significant accounting polices

and other explanatory information. [The financial statements have been prepared by

management based on the financial reporting provisions of Section Y of Regulation Z.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial

statements in accordance with [the financial reporting provisions of Section Y or

Regulation Z], and for such internal control as management determines is necessary

to enable the preparation of financial statements that are free from material

misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our

audit. We conducted our audit in accordance with International Standards on

Auditing. Those standards require that we comply with ethical requirements and

plan and perform the audit to obtain reasonable assurance about whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts

and disclosures in the financial statements. The procedures selected depend on the

auditor’s judgement, including the assessment of the risks of material misstatement of

the financial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the entity’s preparation

and fair presentation of the financial statements in order to design audit procedures

that are appropriate in the circumstances, but not for the purpose of expressing an

opinion on the effectiveness of the entity’s internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of

accounting estimates made by management, as well as evaluating the overall

Paper P7: Advanced audit and assurance (International)

344 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

presentation of the financial statements.

We believe that the audit evidence that we have obtained is sufficient and appropriate

to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements give a true and fair view (or present fairly, in

all material respects,) of the financial position of ABC Company as of December 31

st

,

20X7, and of its financial performance and its cash flows for the year then ended in

accordance with [the financial reporting provisions of Section Y of Regulation Z].

[Basis of accounting

Without modifying our opinion, we draw attention to Note X to the financial

statements, which describes the basis of accounting. The financial statements are

prepared to assist ABC Company to meet the requirements of Regulator DEF. As a

result, the financial statements may not be suitable for another purpose.

Other matter

ABC Company has prepared a separate set of financial statements for the year ended

December 31

st

, 20X7 in accordance with International Financial Reporting Standards

on which we issued a separate auditor’s report to the shareholders of ABC Company

dated March 31

st

, 20X7.]

(Auditor’s signature)

(Date of the report)

(Auditor’s address)