ACCA F7 (INT) Financial Reporting - Study text - 2010 - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 13: Provisions, contingent liabilities and contingent assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 235

Contingent asset

A contingent asset is:

a possible asset

arising from past events

whose existence will be confirmed only by the occurrence or non-occurrence of

one or more uncertain future events.

An example of a contingent asset might be a possible gain arising from an

outstanding legal action against a third party. The existence of the asset (the money

receivable) will only be confirmed by the outcome of the legal dispute.

2.2 Recognising contingent liabilities or contingent assets

Unlike provisions, contingent liabilities and assets:

are not recognised in the financial statements and

are not recorded in the ledger accounts of an entity. (They are not included in the

double entry ledger accounting system.)

In some circumstances, information about the existence of a contingent asset or a

contingent liability should be disclosed in the notes to the financial statements

Contingent liabilities should be disclosed unless the possibility of any outflow

in settlement is remote (the meaning of ‘remote’ is not defined in IAS37).

Contingent assets should be disclosed only if an inflow in settlement is

probable. ’Probable’ is defined by IAS37 as ‘more likely than not’. (And if an

inflow is certain, the item is an actual asset that should be recognised in the

statement of financial position.)

2.3 Disclosures about contingent liabilities and contingent assets

Where disclosure of a contingent liability or a contingent asset is appropriate, IAS37

requires the following disclosures in notes to the financial statements.

A brief description of the nature of the contingent liability/asset

Where practicable:

− an estimate of its financial effect

− an indication of the uncertainties.

For contingent liabilities, the possibility of any reimbursement.

Paper F7: Financial reporting (International)

236 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

2.4 Summary: liabilities, provisions, contingent liabilities and contingent

assets

The following table provides a summary of the rules about whether items should be

treated as liabilities, provisions, contingent liabilities or contingent assets.

Liability

Provision

Contingent liability

Contingent

asset

Present

obligation/

asset arising

from past

events?

Yes Yes Yes Only a

possible

obligation

Only a

possible

asset

Will

settlement

result in

outflow/

inflow of

economic

benefits?

Expected

outflow

Probable

outflow –

and a

reliable

estimate

can be

made of the

obligation

Not

probable

outflow – or

a reliable

estimate

cannot be

made of the

obligation

Outflow

to be

confirmed

by

uncertain

future

events

Inflow to be

confirmed

by

uncertain

future

events

Treatment in

the financial

statements

Set up a

liability

Set up a

provision (a

type of

liability)

Disclose as a contingent

liability (unless the

possibility of outflow is

remote)

Only

disclose if

inflow is

probable

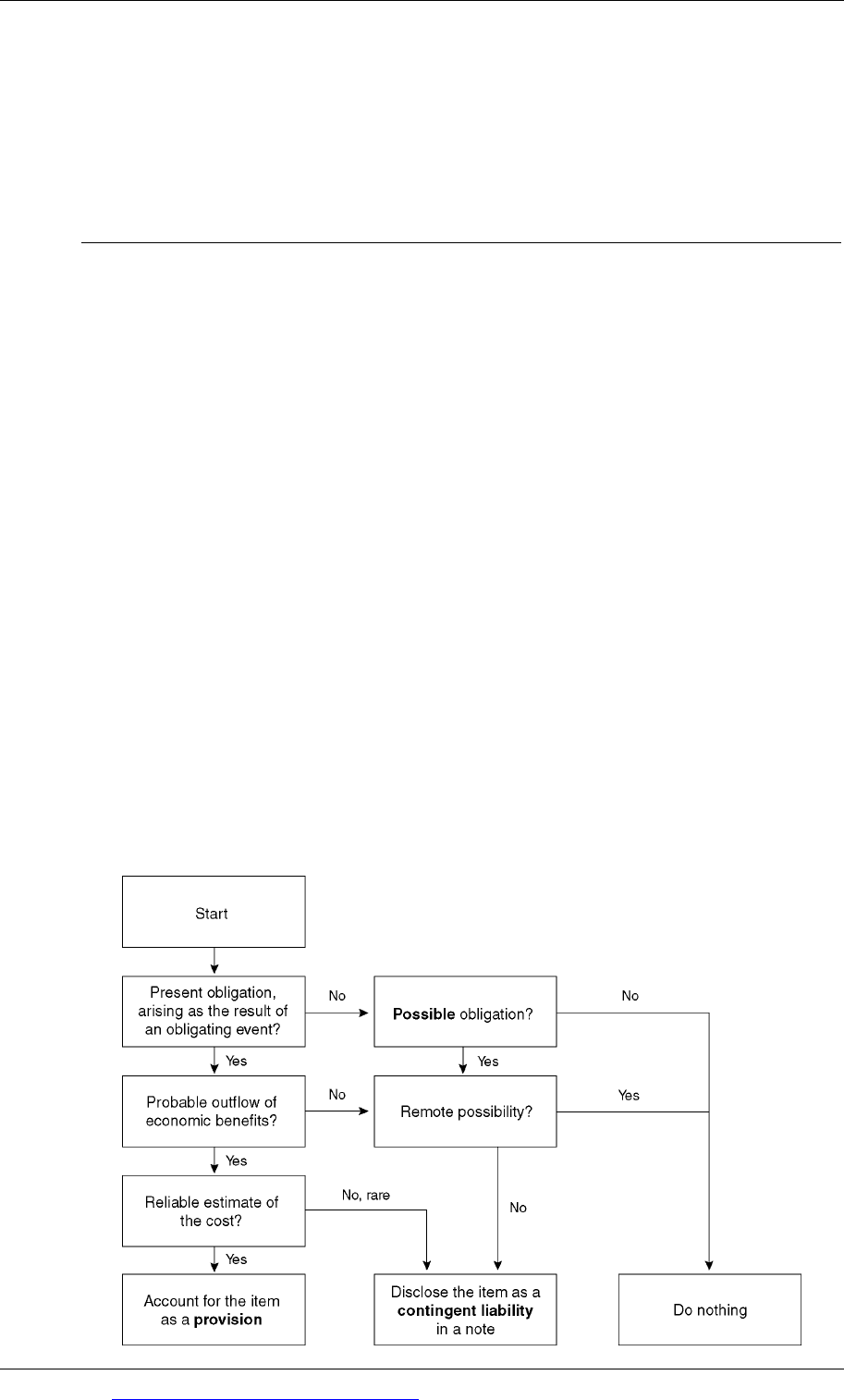

Decision tree

An Appendix to IAS37 has a decision tree, showing the rules for deciding whether

an item should be recognised as a provision, reported as a contingent liability, or

not reported at all in the financial statements.

Chapter 13: Provisions, contingent liabilities and contingent assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 237

Events after the reporting period: IAS10

Purpose of IAS10

Definitions

Accounting for adjusting events after the reporting period

Disclosures for non-adjusting events after the reporting period

Dividends

The going concern assumption

3 Events after the reporting period: IAS10

3.1 Purpose of IAS10

IAS10 Events after the reporting period has two main objectives:

to specify when an entity should adjust its financial statements for events that

occur after the end of the reporting period, but before the financial statements

are authorised for issue, and

to specify the disclosures that should be given about events that have occurred

after the end of the reporting period but before the financial statements were

authorised for issue.

IAS10 also includes a requirement that the financial statements should disclose

when the statements were authorised for issue, and who gave the authorisation.

3.2 Definitions

IAS10 sets out the following key definitions.

Events after the reporting period are those events, favourable and unfavourable

that occur between the end of the reporting period and the date the financial

statements are authorised for issue.

There are two types of event after the reporting period:

Adjusting events. These are events that provide evidence of conditions that

already existed as at the end of the reporting period.

Non-adjusting events. These are events that have occurred due to conditions

arising after the end of the reporting period.

3.3 Accounting for adjusting events after the reporting period

IAS10 states that if an entity obtains information about an adjusting event after the

reporting period, it should update the financial statements to allow for this new

information.

Paper F7: Financial reporting (International)

238 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

‘An entity shall adjust the amounts recognised in its financial statements to reflect

adjusting events after the reporting period.’

IAS10 gives the following examples of adjusting events.

The settlement of a court case after the end of the reporting period, confirming

that the entity had a present obligation as at the end of the reporting period as a

consequence of the case.

The receipt of information after the reporting period indicating that an asset was

impaired as at the end of the reporting period. For example, information may be

obtained about the bankruptcy of a customer, indicating the need to make a

provision for a bad (irrecoverable) debt against a trade receivable in the year-end

statement of financial position. Similarly, information might be obtained after

the reporting period has ended indicating that as at the end of the reporting

period the net realisable value of some inventory was less than its cost, and the

inventory should therefore be written down in value.

The determination after the end of the reporting period of the purchase cost of

an asset, where the asset had already been purchased before the end of the

reporting period, but the purchase price had not been finally agreed or decided.

Similarly, the determination after the reporting period of the sale price for a non-

current asset, where the sale had been made before the end of the reporting

period but the sale price had not yet been finally agreed.

The discovery of fraud or errors showing that the financial statements are

incorrect.

Example

On 31 December Year 1, Entity G is involved in a court case. It is being sued by a

supplier. On 15 April Year 2, the court decided that Entity G should pay the

supplier $45,000 in settlement of the dispute. The financial statements for Entity G

for the year ended 31 December Year 1 were authorised for issue on 17 May Year 2.

The settlement of the court case is an adjusting event after the reporting period:

It is an event that occurred between the end of the reporting period and the date

the financial statements were authorised for issue.

It provided evidence of a condition that existed at the end of the reporting

period. In this example, the court decision provides evidence that the entity had

an obligation to the supplier as at the end of the reporting period.

Since it is an adjusting event after the reporting period, the financial statements for

Year 1 must be adjusted to include a provision for $45,000. The alteration to the

financial statements should be made before they are approved and authorised for

issue.

3.4 Disclosures for non-adjusting events after the reporting period

Non-adjusting events after the reporting period are treated differently. A non-

adjusting event relates to conditions that did not exist at the end of the reporting

Chapter 13: Provisions, contingent liabilities and contingent assets

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 239

period, therefore the financial statements must not be updated to include the effects

of the event. IAS10 states quite firmly: ‘An entity shall not adjust the amounts

recognised in the financial statements to reflect non-adjusting events after the

reporting period’.

However, IAS10 goes on to say that if a non-adjusting event is material, a failure by

the entity to provide a disclosure about it could influence the economic decisions

taken by users of the financial statements. For material non-adjusting events IAS10

therefore requires disclosure of:

the nature of the event, and

an estimate of its financial effect, or a statement that such an estimate cannot be

made.

This information should be disclosed in a note to the financial statements.

(Note: There are no disclosure requirements for adjusting events as they have

already been reflected in the financial statements.)

IAS10 gives the following examples of non-adjusting events.

A fall in value of an asset after the end of the reporting period, such as a large

fall in the market value of some investments owned by the entity, between the

end of the reporting period and the date the financial statements are authorised

for issue. A fall in market value after the end of the reporting period will

normally reflect conditions that arise after the reporting period, not conditions

already existing as at the end of the reporting period.

The acquisition or disposal of a major subsidiary.

The formal announcement of a plan to discontinue a major operation.

Announcing or commencing the implementation of a major restructuring.

The destruction of a major plant by a fire after the end of the reporting period.

The ‘condition’ is the fire, not the plant, and the fire didn’t exist at the end of the

reporting period. The plant should therefore be reported in the statement of

financial position at its carrying amount as at the end of the reporting period.

The fire, and the financial consequences of the fire, should be disclosed in a note

to the financial statements.

3.5 Dividends

IAS10 also contains specific provisions about proposed dividends and the going

concern presumption on which financial statements are normally based.

If equity dividends are declared after the reporting period, they should not be

recognised, because they did not exist as an obligation at the end of the reporting

period.

Dividends proposed after the reporting period (but before the financial statements

are approved) should be disclosed in a note to the financial statements, in

accordance with IAS1.

Paper F7: Financial reporting (International)

240 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

3.6 The going concern assumption

There is one important exception to the normal rule that the financial statements

reflect conditions as at the end of the reporting period.

A deterioration in operating results and financial position after the end of the

reporting period may indicate that the going concern presumption is no longer

appropriate. If management decides after the end of the reporting period but before

the financial statements are approved that it intends to liquidate the entity or to

cease trading, the financial statements for the year just ended should be prepared on

some other basis (for example, on a break-up basis).

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 241

Paper F7 (INT)

Financial reporting

CHAPTER

14

Taxation

Contents

1 Sales taxes

2 Current tax: IAS12

3 Deferred tax: IAS12

4 Presentation and disclosure requirements of IAS12

Paper F7: Financial reporting (International)

242 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Sales taxes

The nature of sales tax

Accounting for sales tax

1 Sales taxes

1.1 The nature of sales tax

You should be familiar with sales tax from your previous studies. Many countries have

a sales tax or ‘value added’ tax. Sales of goods and services are taxed at a percentage

amount of the sales price. Businesses selling goods and services are required to add the

tax to their selling price and collect the tax from their customers.

Some items of goods or services might be either:

exempt from sales tax (and so outside the scope of the tax), or

‘zero-rated’ (and so within the scope pf the tax rules, but with a tax rate of 0%).

Business entities also pay sales tax on most of the goods and services they buy from

their suppliers. Businesses are therefore both collectors of tax as the seller, and

payers of tax as the buyer. Sales tax on goods or services sold is commonly referred

to as output tax. Sales tax suffered on purchases is commonly referred to as input

tax.

The sales tax collected by businesses is paid to the tax authorities. The amount that

businesses are required to pay is calculated as set out below.

$

Sales tax on goods or services sold (output tax) X

Minus: Sales tax paid on purchases (input tax) (X)

–

–––

Net payment of tax to the tax authorities X

–

–––

A business must pay the difference between its output tax and its input tax to the

tax authorities, at periodic intervals specified by the tax regulations.

1.2 Accounting for sales tax

Businesses keep a sales tax account in their main ledger (nominal ledger). This is

used to record amounts of sales tax due to or from the tax authorities. Usually, the

balance on the account is a credit balance, representing the net amount of tax

currently payable to the government. This balance is shown within ’Trade and other

payables’ as a current liability in the statement of financial position.

Occasionally, there might be an amount due to the business entity from the tax

authorities.

Chapter 14: Taxation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 243

This will happen, for example, if most or all of an entity’s sales are ‘zero-rated’ but

the entity is still able to claim back the input sales tax on its purchases. In this case

the closing balance on the account will be a receivable, appearing within ‘Trade and

other receivables’ in current assets in the statement of financial position.

In the statement of comprehensive income:

sales revenue excludes sales tax

purchases and expenses exclude sales tax where this is recoverable

any irrecoverable sales tax is included in the cost of the item that it relates to, i.e.

purchases and expenses include sales tax if the sales tax cannot be recovered

from the tax authorities.

Paper F7: Financial reporting (International)

244 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Current tax: IAS12

Definitions

Basic accounting for current tax

Current tax paid before the end of the reporting period

Tax withheld at source

Under-provision or over-provision of tax in the previous period

Current tax and other comprehensive income

2 Current tax: IAS12

Definitions

Companies pay tax on their profits. Current tax is the amount of tax payable in

respect of the taxable profit for a period. If there has been a taxable loss, as opposed

to a profit, then current tax is the amount of tax recoverable.

Taxable profits are not the same as accounting profits.

Accounting profit is the profit or loss for the period, before deducting the tax

expense.

Taxable profit is determined by adjusting the accounting profit, according to

rules established by the tax authorities.

If accounting profits are $1,000,000 and the tax rate is 25%, it might be expected that

tax will be $250,000 and profit after tax will be $750,000. However this is not correct.

The differences between taxable profits and accounting profits are considered in

more detail later.

2.2 Basic accounting for current tax

Current tax appears in the financial statements:

as an expense for the period (since it reduces profits) and

as a liability in the statement of financial position (since the tax is payable to the

government).

Suppose that Entity X has taxable profits for Year 1 of $300,000 and the current tax

rate is 30%. It has not yet paid any tax on its Year 1 profits. Current tax would

appear in the financial statements as follows:

As a tax expense of $90,000, below the figure for profit before tax

As current tax payable of $90,000: this is a current liability in the statement of

financial position.