ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 155

The opening year rules

The need for special opening year rules

Calculating the opening year assessments

2 The opening year rules

2.1 The need for special opening year rules

When an individual starts to trade, he must choose a convenient ending date for the

accounting period. Having chosen his accounting period closing date, his first set of

accounts may be of any length:

more than 12 months,

less than 12 months, or

exactly equal to 12 months.

As a result, if the CYB rule explained above is applied, it would be possible for a

trader to avoid paying tax in the first tax year of trading. For example, if a trader

commences trade on 1 January 2010 and prepares the first set of accounts to 31

December 2010, he was trading in the tax year 2009/10. However, as there are no

accounts which end in that tax year, application of the CYB rule would mean there

is no assessment to tax for 2009/10.

To ensure that some profits of the business are taxed in every tax year in which the

individual is in business, the CYB rule is not used:

in the opening year itself, and

usually the next few years as well.

Instead, special opening year rules are applied.

2.2 Calculating the opening year assessments

The opening year assessment rules are summarised below.

Tax year Basis period

First tax year

Assess on an actual tax year basis

(i.e. from the date the trade started to the following

5 April)

Second tax year

See the decision table below

Third tax year

Assess the 12 months to the accounting date

ending in the third tax year

Fourth tax year onwards

Assess using CYB rules as described above

Paper F6 (UK): Taxation FA2009

156 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

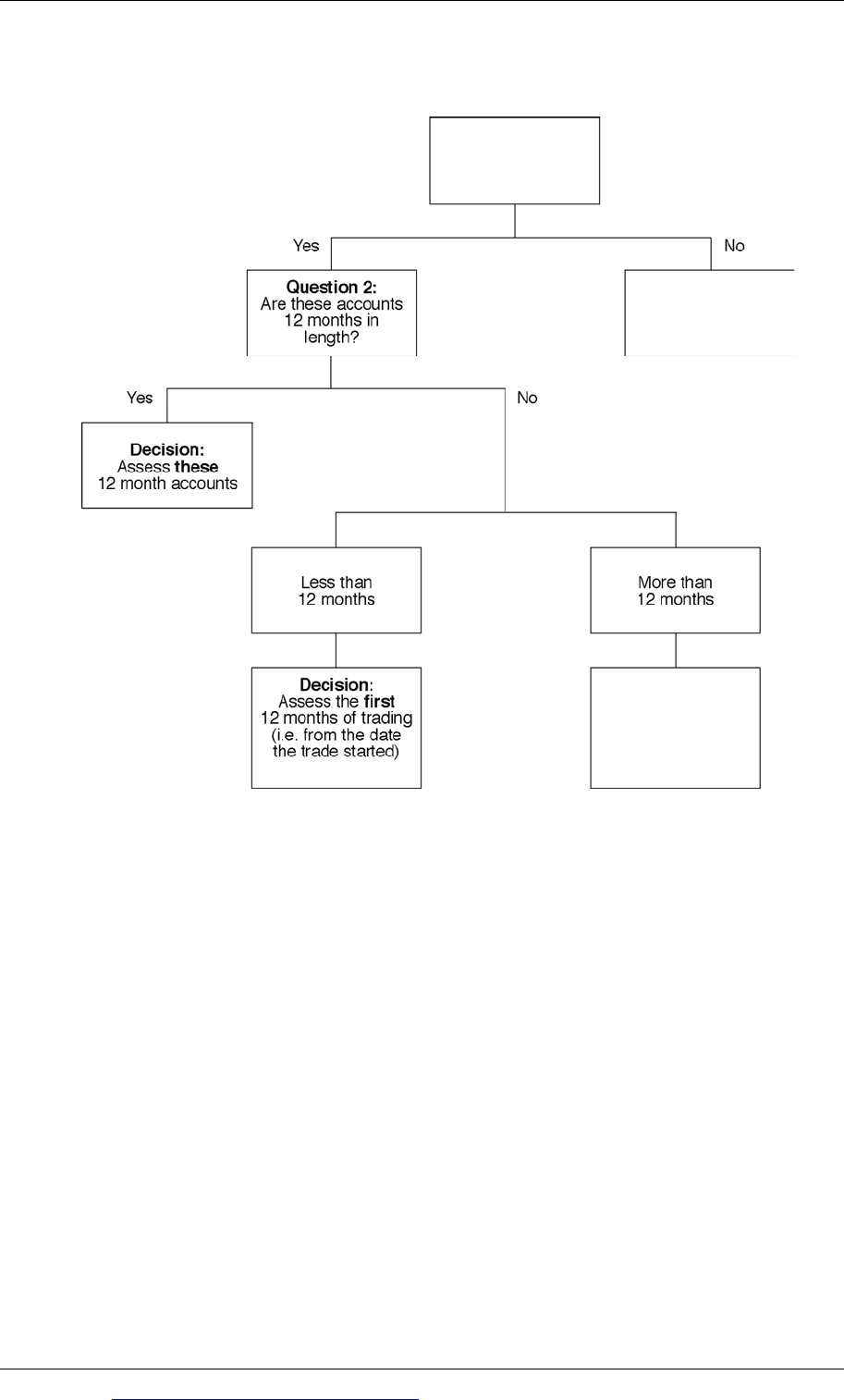

The rules for the second tax year are set out in the following decision table. The

approach is based on the answers to two questions

Question 1:

Are there accounts

which end in the

tax year?

Decision:

Assess on an actual

tax year basis

(i.e. 6 April to 5 April)

Decision:

Assess the

12 months to the

accounting date

ending in the

second tax year

In applying these assessment rules it is assumed that profits accrue evenly over

time. Therefore, where calculations to obtain an assessment require profits to be

taken from more than one set of accounts, the profits must be time-apportioned.

The tax legislation requires apportionment in days, but in the examination

calculations should be made to the nearest month.

A consequence of applying the opening year rules is that some profits will be

assessed to tax more than once. These profits are known as overlap profits.

Relief is given for overlap profits in the final tax year on the cessation of trade, or

possibly earlier if the business changes its accounting date.

Second tax year

From the decision table above, it can be seen that there are four possible decisions

for the second tax year.

Each of the four possible scenarios is illustrated on the following examples.

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 157

Example 1

Katie started to trade on 1 October 2008 and decided to prepare her accounts to 30

September each year. Her results for the first two years are as follows:

Yearended Adjustedprofitbefore

capitalallowances

Capitalallowances

£ £

30September2009 21,600 5,600

30September2010 64,800 6,500

Required

Calculate Katie’s trading income assessments for the first three tax years, and the

overlap profits arising from the application of the opening year rules.

Answer

Step 1. Calculate the adjusted profit after capital allowances for each accounting

period

Yearended Adjustedprofitaftercapital

allowances

£

30Sept2009 (£21,600‐£5,600) 16,000

30Sept2010 (£64,800‐£6,500) 58,300

Step 2. Work out the basis period for the first tax year of trading

Trading starts on 1 October 2008 = In tax year 2008/09 = First tax year.

Tax year 1: Tax the profits from 1 October 2008 to 5 April 2009.

Step 3. Work out the basis period for the second tax year

Second tax year = 2009/10. Ask two questions:

Are there accounts which end in the tax year? Yes = Year ended 30 September 2009

Are these accounts 12 months in length? Yes

Decision Assess the profits of those 12 months

Step 4. Summarise and calculate the trading income assessments

Tax

year

Basisof

assessment

Basisperiod

Workings

Trading

income

assessment

£

2008/09 Actual 1.10.2008–5.4.2009 6/12×£16,0008,000

2009/10 12monthsending

insecondyear

Yearended30.9.2009

16,000

2010/11 12monthsending

inthirdyear

Yearended30.9.2010 58,300

Paper F6 (UK): Taxation FA2009

158 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Step 5. If required, calculate the overlap profits

Profits are assessed more than once for the period 1.10.2008 – 5.4.2009.

Overlap profits = 6/12 × £16,000 = £8,000.

Example 2

Len started to trade on 1 November 2007 and decided to prepare his accounts to 31

May each year. His results for the first two accounting periods are as follows:

Periodended

Adjustedprofitaftercapitalallowances

£

31May2008 13,400

31May2009 51,470

Required

Calculate the trading income assessments for Len for the first three tax years and

calculate the overlap profits.

Answer

Trading starts on 1 November 2007 = In tax year 2007/08 = First tax year.

First tax year: Assess profits from 1 November 2007 to 5 April 2008.

Second tax year = 2008/09. Ask two questions:

Are there accounts which end in the tax year? Yes = 7 months ended 31 May 2008

Are these accounts 12 months in length? No: less than 12 months

Decision Assess the profits of the first 12 months

Tax

year

Basisof

assessment

Basisperiod

Workings

(nearest

month)

Trading

income

assessment

£

2007/08 Actual 1.11.2007–5.4.2008 5/7×£13,400 9,571

2008/09 First12months 1.11.2007–31.10.2008 £13,400+

(5/12×£51,470)

34,846

2009/10 12monthsending

inthirdyear

Yearended31.5.2009

51,470

Overlap profits

£

1.11.2007–5.4.2008

5/7×£13,400 9,571

1.6.2008–31.10.2008 5/12×£51,470 21,446

31,017

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 159

Example 3

Mary started to trade on 1 June 2007 and decided to prepare her first accounts to 31

August 2008 and then to 31 August each year. Her results for the first two

accounting periods are as follows:

Periodended

Adjustedprofitaftercapitalallowances

£

31August2008 20,110

31August2009

77,200

Required

Calculate Mary’s first three years’ trading income assessments and the overlap

profits.

Answer

Trading starts on 1 June 2007 = In tax year 2007/08 = First tax year.

First tax year: Assess the profits from 1 June 2007 to 5 April 2008.

Second tax year = 2008/09. Ask two questions:

Are there accounts which end in the tax

year?

Yes = 15 months ended 31 August 2008

Are these accounts 12 months in length? No: More than 12 months

Decision Assess profits for the 12 months ending

on 31 August 2008

Tax

year

Basisof

assessment

Basisperiod

Workings(to

nearestmonth)

Trading

income

assessment

£

2007/08 Actual 1.6.2007–5.4.2008 10/15×£20,110 13,407

2008/09 12monthsending

insecondyear

1.9.2007–31.8.2008

12/15×£20,110

16,088

2009/10 12monthsending

inthirdyear

Yearended

31.8.2009

77,200

Overlap profits

1.9.2007 – 5.4.2008: 7/15 × £20,110 = £9,385.

Example 4

Nicholas started to trade on 1 January 2007 and decided to prepare his first accounts

to 30 April 2008 and thereafter to 30 April each year. His results for the first two

accounting periods are as follows:

Paper F6 (UK): Taxation FA2009

160 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Periodended Adjustedprofitaftercapitalallowances

£

30April2008 34,140

30April2009

51,250

Required

Calculate Nicholas’ first four years’ trading income assessments and the overlap

profits.

Answer

Trading starts on 1 January 2007 = In tax year 2006/07 = First tax year.

First tax year: Assess the profits from 1 January 2007 to 5 April 2007.

Second tax year = 2007/08. Ask two questions:

Are there accounts which end in the tax year? No

Decision Assess the actual profits of the tax

year: from 6 April 2007 to 5 April

2008

Third tax year = 2008/09. The 16-month accounts to 30 April 2008 end in the third

tax year.

Decision = Assess the 12 months running up to the accounting end date that ends in

the third tax year (i.e. the 12 months to 30 April 2008).

Tax

year

Basisof

assessment

Basisperiod

Workings

(tonearest

month)

Trading

income

assessment

£

2006/07 Actual 1.1.2007–5.4.2007 3/16×£34,140 6,401

2007/08 Actual 6.4.2007–5.4.2008 12/16×£34,140 25,605

2008/09 12monthsending

inthirdyear

1.5.2007–30.4.2008 12/16×£34,140 25,605

2009/10 CYB Yearended30.4.2009 51,250

Overlap profits

1.5.2007 – 5.4.2008: 11/16 × £34,140 = £23,471.

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 161

The closing year rules

The need for special closing year rules

Calculating the closing year assessments

3 The closing year rules

3.1 The need for special closing year rules

The primary aim of the basis of assessment rules is that the business should be taxed

on the exact amount of adjusted profits after capital allowances earned over the

entire life of the business.

In the opening years, overlap profits are assessed to tax more than once. To ensure

that no more than the exact amount of adjusted profits is assessed to tax, relief is

given for the overlap profits in the final tax year.

3.2 Calculating the closing year assessments

The closing year rules and approach are summarised as follows:

Step 1. Work out which tax year is the final tax year.

Step 2. Work out the trading income assessment of the penultimate year using

the normal CYB rules.

Step 3. Work out the final trading income assessment as follows:

£

All profits not yet assessed (i.e. profits from the end of the accounting

period ending in the penultimate year to the date of cessation)

X

Minus: Overlap relief (X)

Closing year trading income assessment X

Example

Owen has been trading for many years preparing accounts to 31 May each year. His

overlap profits are £3,650. Owen ceased to trade on 30 September 2009 and has

provided the following results for the last three accounting periods:

Periodended

Adjustedprofit

beforecapital

allowances

Capital

allowances

£ £

31May2008 38,610 13,160

31May2009

23,200 10,000

30September2009

15,300 12,350

Required

Calculate Owen’s last two trading income assessments.

Paper F6 (UK): Taxation FA2009

162 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

The adjusted profit after capital allowances for each accounting period

Yearended

Adjustedprofitaftercapital

allowances

£

31May2008 (£38,610‐£13,160) 25,450

31May2009 (£23,200‐£10,000) 13,200

30Sept2009 (£15,300‐£12,350) 2,950

Step 1: Work out the final tax year

Cessation of trade: 30 September 2009 = In tax year 2009/10 = Last tax year.

Step 2: Work out the trading income assessment of the penultimate year

2008/09 CYB Yearended31.5.2008 £25,450

Step 3: Work out the final trading income assessment

£

Profitsnotyetassessed(1.6.2008–30.9.2009)

Yearended31May2009 13,200

Periodended30September2009 2,950

Minusoverlaprelief

(3,650)

Closingyeartradingincomeassessment

12,500

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 163

Choice of accounting date

A date early in the tax year

A date late in the tax year

4 Choice of accounting date

4.1 A date early in the tax year

A trader has a choice of accounting date. If he picks a date early in the tax year, for

example 30 April, this will have the advantage of maximising the gap between

earning profits and paying the tax on them. In 2009/10, for example, the assessment

will be based on the profits of the year ended 30 April 2009. If profits are rising, this

will produce a lower assessment than an accounting date of 31 March 2010.

However, a date early in the tax year may result in the assessment of more than 12

months’ profits in the final year. See the previous example in which Owen was

assessed on the profits of both the year ended 31 May 2009 and the period ended 30

September 2009 in 2009/10.

4.2 A date late in the tax year

A date late in the tax year, for example 31 March, will avoid the bunching of profits

in the final tax year. So, in the previous example, if Owen had had an accounting

date of 31 March instead of 31 May, his final tax year would have been based only

on the profits of the period ended 30 September 2009 as the profits for the year

ended 31 March 2009 would have been assessed in the penultimate year.

Choosing 31 March as the accounting date would also avoid overlap profits under

the commencement rules. In addition, it has the advantage of being easy for the

taxpayer to understand. However, its drawback is that it minimises the gap between

earning profits and paying tax on them.

Paper F6 (UK): Taxation FA2009

164 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The rules on a change of accounting date

The need for special change of accounting date rules

The conditions for a valid change of accounting date

Calculating the change of accounting date assessments

5 The rules on a change of accounting date

5.1 The need for special change of accounting date rules

Apart from in the first and last tax years, the basis of assessment rules seek to assess

12 months’ worth of profits every tax year.

However, when an unincorporated business decides to change its accounting date,

it will need to produce a set of accounts that is either more than or less than 12

months in length.

The normal current year basis of assessment cannot be used, as the accounts ending

in the tax year will not be exactly 12 months. Therefore special rules are required to

deal with a change in accounting date.

Certain conditions must be satisfied for a business to be allowed to treat a change of

accounting date as valid for tax purposes. These conditions exist primarily to

prevent businesses changing their accounting date frequently in an attempt to gain

a tax advantage.

5.2 The conditions for a valid change of accounting date

For a change of accounting date to be valid for tax purposes, the following

conditions must be satisfied:

The first accounting period to the new accounting end date must not exceed 18

months in length.

The business must not have changed its accounting date in the previous five

years or, if it has, it must have justifiable commercial reasons for making a

further change in the five year period.

HMRC must be notified of the change by 31 January following the tax year in

which the first accounting period to the new date ends.

If the conditions are not satisfied, HMRC will ignore the new accounting date for

taxation purposes and continue to assess profits based on the old date. If necessary,

profit figures will be apportioned accordingly.

5.3 Calculating the change of accounting date assessments

The change of accounting date rules and approach are summarised below.