ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 6: Capital allowances – plant and machinery

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 125

BA = balancing allowance

BC = balancing charge

TWDV = tax written down value: this represents the cost of the assets less the

capital allowances claimed on them so far. It is their written down value for tax

purposes.

3.3 Preparation of a capital allowances computation

There are seven key steps in preparing a computation of capital allowances. To

ensure that the rules for capital allowances are applied correctly, it is important to

follow these steps in the strict order shown below, and to set out the computations

for capital allowances using the proforma that is given here.

Step 1: Review additions to non-current assets in the accounting period

Decide whether the purchased asset is plant and machinery and therefore eligible

for capital allowances. Then decide the appropriate category of the asset and

therefore to which column the addition should be allocated.

If the asset does not qualify for an AIA or FYA, add the cost of the asset to the tax

written down value brought forward from the previous period (TWDV b/f) in the

appropriate column of the proforma.

The TWDV b/f, if applicable, will be given in the examination question.

Step 2: Bring in additions that qualify for the AIA and calculate the AIA

available

The cost of assets qualifying for the AIA should be entered as an addition in the

appropriate column, and the AIA entered as a deduction.

Step 3: Deal with disposals of plant and machinery in the accounting period

Capital allowances are given on the net cost of an asset. Therefore, when an asset

has been disposed of, the sale proceeds are deducted from the TWDV. This

deduction should be entered in the appropriate column of the proforma.

There are two exceptions to this rule:

If the asset was sold for more than its original cost, deduct the original cost

instead of the sale proceeds. (Never take out from a column more than the

amount that was originally put in.)

If the asset was given away (gifted) or sold for less than it was worth, the

amount of the deduction is the lower of:

− the full market value on the disposal date, and

− the original cost.

When a building is sold, the vendor and purchaser make a joint election to

determine how much of the sale proceeds is to be allocated to any fixtures included

Paper F6 (UK): Taxation FA2009

126 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

within the building. However, the amount allocated to the fixtures cannot exceed

their original cost.

Step 4: Calculate balancing allowances (BAs) and balancing charges (BCs)

Next, the balancing allowances and balancing charges should be calculated and

entered in the appropriate column of the proforma. The calculation of BAs and BCs

is explained later.

Step 5: Calculate the writing down allowances (WDAs) available

Next, the writing down allowances should be calculated, and entered (as a

deduction) in the appropriate column of the proforma. The calculation of WDVs is

explained later.

Step 6: Bring in additions that qualify for FYAs and calculate the FYAs

available

Enter the qualifying cost as an addition to the main pool and enter the FYA as a

deduction.

Step 7: Calculate the total capital allowances for the period

There is a column in the proforma for capital allowances for the period. The amount

of balancing allowances and balancing charges, WDAs, FYAs and the AIA are

recorded in this column. The capital allowances available for the period should be

totalled. (Total = BAs + WDAs + FYAs + AIA – BCs). This total should then be

deducted from the adjusted profits before capital allowances to calculate the trading

income assessment.

The TWDV is then calculated for each column and carried forward to the next

period.

Study the proforma carefully. It may seem complicated initially. You should keep

returning to the proforma as you learn more about calculating capital allowances.

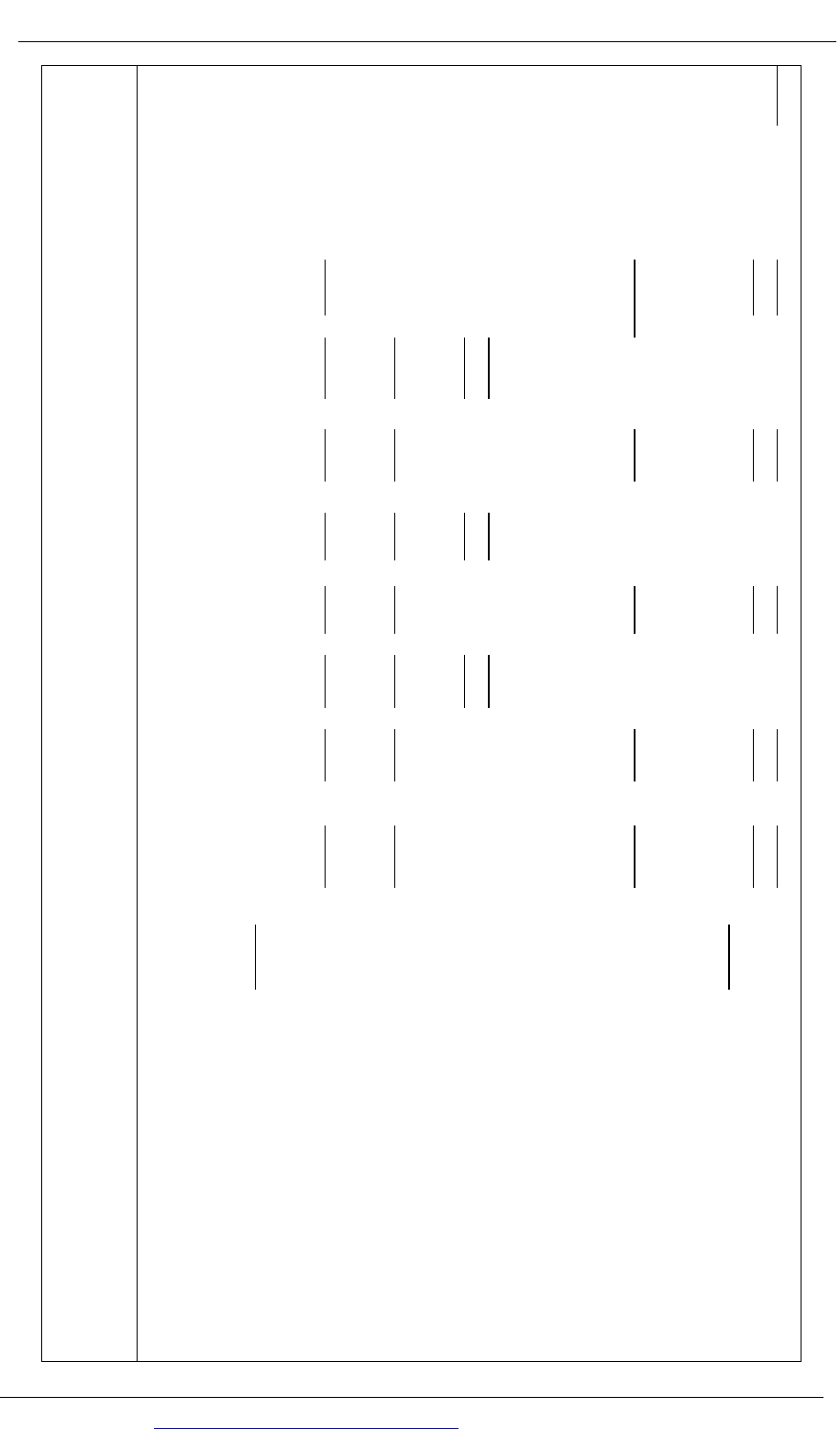

3.4 Proforma capital allowances computation

Proforma capital allowances computation

Note: This proforma is the same as for corporation tax, except for the private use assets (shown in bold) which are specific to income tax

Main

pool

Special

rate pool

Expensive cars Short life assets

Private use assets

Total allowances

A

B C

D

E

F

£

£

£

£

£

£

£

£

£

£

TWDV b/f

X

X

X

X

X

X

X

Acquisitions qualifying for AIA:

Additions

X

AIA

(X)

X

Acquisitions not qualifying for AIA:

Private use assets

X

Cars (depending on CO

2

emissions)

X

X

X

X

X

X

X

X

X

X

Disposals: Lower of (i) sale proceeds, or

(ii) original cost

(X)

(X)

(X)

(X)

(X)

X

X

(X)

X

X

X

(X)

Balancing charge

X

X × Bus %

(X)

Balancing allowance

(X)

X

Nil

Nil

Nil

WDA (scale up or down re-the length

of the accounting period)

20%

(X)

(X)

(X)

× Bus %

X

10%

(X)

X

X

Lower of (1) 20% or

(2) maximum £3,000

(X)

X

X

X

X

X

Acquisitions qualifying for FYA

Additions

X

FYA (100% or 40%) (X)

X

X

TWDV c/f

X

X

X

X

X

Total capital allowances

XX

Chapter 6: Capital allowances – plant and machinery

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 127

Paper F6 (UK): Taxation FA2009

128 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The main pool

The calculation of the AIA on main pool items

The calculation of FYAs on main pool items

The calculation of WDAs on main pool items

Rate of WDAs on main pool plant and machinery items

The calculation of balancing allowances and balancing charges on main pool

items

Small pools

4 The main pool

4.1 The calculation of the AIA on main pool items

The annual investment allowance (AIA) gives 100% relief for the first £50,000 of

capital expenditure on plant and machinery, excluding motor cars. The AIA is

given in the accounting period in which the asset is purchased.

The £50,000 limit is proportionally reduced or increased where a period of account

is shorter or longer than 12 months. For example, the AIA for a nine-month period

of account would be £37,500 (50,000 x 9/12).

Any expenditure in excess of the £50,000 limit will qualify immediately for either

writing-down allowances (WDA), or for the 40% first year allowance (FYA) if

incurred in the period 6 April 2009 to 5 April 2010 (1 April 2009 to 31 March 2010 for

companies).

If the full AIA is not used, the balance is lost. It cannot be carried forward or back.

4.2 The calculation of FYAs on main pool items

A 40% FYA is available for capital expenditure on plant and machinery, excluding

motor cars. To qualify, the expenditure must be incurred in the period 6 April 2009

to 5 April 2010 (1 April 2009 to 31 March 2010 for companies).

The 40% FYA is likely to be of benefit only to those businesses incurring capital

expenditure in excess of £50,000 a year as the first £50,000 of qualifying expenditure

is already covered by the AIA.

A business cannot claim both the FYA and a WDA in the same period in respect of

the same expenditure. Therefore, if the FYA is claimed, the unrelieved balance of

expenditure must not be added to the main pool until after the WDA has been

calculated.

The length of ownership of the asset in the accounting period is irrelevant. The

length of the accounting period is also irrelevant. The full FYA is available simply

for incurring qualifying expenditure within the relevant period.

Chapter 6: Capital allowances – plant and machinery

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 129

Date of expenditure

As a general rule, capital expenditure is treated as incurred on the date on which the

obligation to pay becomes unconditional. However, if payment is not due until four

months or more after that date, the expenditure is treated as incurred on the date on

which payment is due.

Pre-trading expenditure is generally treated as incurred on the date on which trade

commences. However, for the purpose of determining entitlement to the 40% FYA,

pre-trading expenditure does not qualify unless actually incurred between 6 April

2009 and 5 April 2010 (1 April 2009 to 31 March 2010 for companies).

4.3 The calculation of WDAs on main pool items

WDAs are given in each accounting period. They are calculated after bringing in

additions and after taking account of asset disposals.

WDAs are available on all main pool assets except those additions in the period on

which FYAs were claimed.

No WDA is available in the period of disposal. Therefore disposals of assets in the

period must be dealt with before calculating the WDA.

4.4 Rate of WDAs on main pool plant and machinery items

The rate of WDAs on main pool items is 20% for a 12-month accounting period,

calculated on the balance in the pool.

The length of ownership of the asset in the accounting period is irrelevant.

However, for WDAs the length of the accounting period is very important. If the

accounting period is less than 12 months, the WDA must be time-apportioned.

Example

Ulrika prepared her accounts for the seven months ended 31 October 2009. In the

period, she purchased the following items of plant and machinery:

£

Purchases Officefurnitureon25May2009–cost 40,000

Factoryequipmenton30June2009–cost 25,000

On 1 April 2009 the tax written down value on the main pool was £76,500.

Required

Calculate the capital allowances available for the seven months ended 31 October

2009.

Paper F6 (UK): Taxation FA2009

130 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

Ulrika‐Capitalallowancesforthe7monthsending31October2009

Mainpool

(TWDV)

Total

allowances

£ £ £

TWDVb/f76,500

AcquisitionsqualifyingforAIA

Officefurniture 40,000

Factoryequipment 25,000

–

–––––

–

––––––––––––––––––––––––––

–

–

65,000

AIA(50,000x7/12) (29,167)29,167

–

–––––

–

–––––––––––––

–

––––––––––––

–

–

35,833

FYA(35,833x40%) (14,333)14,333

–

–––––

–

––––––––

–

––––

–

–––––––––––––– –

21,500

Writingdownallowance(WDA)

(76,500x20%×7/12)

(8,925)

8,925

Transferredtopool (21,500) 21,500

–

–––––

–

–––––––

–

––––

–

––––––

–

–––––––––

–

–––––

–

–––––––

–

––––

–

––––––––––––––––

TWDVc/f89,075

–

–––––

–

––––––

–

––––

–

–––––––––––––––––

–––––––––––––––––––––––––––––

Totalallowancesavailable52,425

–––––––––––––––––––––––––––––

4.5 The calculation of balancing allowances and balancing charges on

main pool items

A balancing allowance (BA) is the tax equivalent of a loss on disposal in the

financial accounts. It will increase the capital allowances available in the accounting

period.

A balancing charge (BC) is the tax equivalent of a profit on disposal in the financial

accounts. It is additional taxable trading profit and is usually recognised by

reducing the capital allowances available in the accounting period.

BAs and BCs are usually referred to collectively as balancing adjustments.

Where a main pool asset is disposed of, deduct the following disposal value from

the pool:

Disposal value = Lower of:

Sale proceeds (or market value if gifted)

Original cost

(This is the application of Step 3, as explained earlier.)

Chapter 6: Capital allowances – plant and machinery

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 131

Disposal value more than the balance in the pool

If the disposal value exceeds the balance on the pool, a balancing charge arises (i.e. a

negative figure). A balancing charge means that allowances claimed in the past

exceed the net cost of the asset. These excess allowances are clawed back in the year

of disposal, by reducing the capital allowances in the year of disposal. A balancing

charge is therefore a negative allowance.

A balancing charge can arise in any accounting period. It reduces the capital

allowances claim for the accounting period.

Example

In the year ended 31 March 2010, Vera sells for £23,000 some plant and machinery

which originally cost £26,000 on 31 January 2009.

The TWDV b/f on the main pool on 1 April 2009 was £18,000. Additions not

qualifying for the AIA totalled £3,000, and those qualifying for the AIA totalled

£45,000.

Required

Calculate the capital allowances available for the year ended 31 March 2010.

Answer

Vera‐Capitalallowances–y/e31March2010

Main

pool

Total

allowances

£ £ £

TWDVb/f18,000

AcquisitionsnotqualifyingforAIA 3,000

–

–––––

–

––––––––––––––––––––––––––––

AcquisitionsqualifyingforAIA21,000

Cost 45,000

AIA (45,000)45,000

–

–––––

–

––––––––––––––––––––––––––

–

–

Nil

Disposals‐Lowerof (i)saleproceeds,or

(ii)originalcost

(23,000)

–

–––––

–

––––––––––––––––––––––––––––

(2,000)

Balancingcharge2,000 (2,000)

–

–––––

–

––––––––––––––––––––––––––––

Nil

Writingdownallowance(WDA)(Nil) Nil

–

–––––

–

––––––––––––––––––––––––––––

TWDVc/fNil

–

–––––

–

–––––––––––––––––––––––––––– –––––––––––––––––––––––––––––––––

–

Totalallowancesavailable43,000

––––––––––––––––––––

–

––––––––––

–

–

Paper F6 (UK): Taxation FA2009

132 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Disposal value less than the balance in the pool

If the disposal value is less than the balance on the pool, this means that allowances

claimed in the past have been less than the net cost of the asset. The rest of the net

cost can therefore be claimed as a capital allowance.

However, for the main pool assets, a balancing allowance does not arise at the time

of the disposal. Instead, the shortfall in the allowances claimed for the asset will be

claimed in the future by WDAs, in the normal way, on a reducing balance basis.

A BA will only arise in the main pool in the period in which the business ceases

to trade, (i.e. the last accounting period) when all the assets of the business are being

disposed of. In this case, all the shortfall of allowances is claimed in the final period

as a BA. This increases the capital allowances claim for the accounting period.

Example

William ceased trading on 31 December 2009 and produced a three-month final set

of accounts. On 1 October 2009 the TWDV b/f on William’s main pool was £64,000.

There were no additions in the final three months of trading.

On cessation William sold his plant and machinery for scrap, and realised proceeds

of £20,000.

Required

Calculate the capital allowances available for the three month accounting period to

31 December 2009.

Answer

William‐Capitalallowancesoncessationoftrade

–3monthsending31December2009

Mainpool

Total

allowances

£ £

TWDVb/f 64,000

Disposals‐Lowerof (i)saleproceeds,or

(ii)originalcost

(20,000)

–

–––––

–

––––––––––––––––––––––––––––

44,000

Balancingallowance (44,000) 44,000

–

–––––

–

––––––––––––––––––––––––––––

TWDVc/f Nil

–

–––––

–

–––––––––––––––––––––––––––– –––––––––––––––––––––––––––––––––

–

–

Totalallowancesavailable 44,000

–––––––––––––––––––––––––––––––––

–

–

4.6 Successions

Where a trade passes from one connected person to another, balancing adjustments

can be avoided by making a succession election. This election allows assets to be

transferred to the purchaser at their TWDVs.

Chapter 6: Capital allowances – plant and machinery

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 133

The election must be made within two years of the date the trade is transferred. If it

is not made, the assets are deemed to be sold to the successor at their market values.

(The definition of a connected person is covered in chapter 13.)

4.7 Small pools

Where the balance of unrelieved expenditure in the main pool is less than £1,000, it

can be written off immediately. The £1,000 limit is reduced or increased

proportionately if the accounting period is less than or more than 12 months.

Paper F6 (UK): Taxation FA2009

134 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The special rate pool

Introduction

Integral features

Long life assets

The AIA

FYAs

WDAs in the special rate pool

Balancing adjustments

5 The special rate pool

5.1 Introduction

The special rate pool contains the following categories of asset:

Features that are integral to a building

Long life assets

Thermal insulation of a building used for a qualifying activity (e.g. a trade)

Cars with CO

2

emissions of more than 160 g/km.

5.2 Integral features

The following items are treated as being integral to a building:

Electrical and lighting systems

Cold water systems

Space or water heating systems

Powered systems of ventilation, cooling or air purification

Lifts and escalators.

5.3 Long life assets

Long life assets are defined as plant (other than cars, ships, and plant and

machinery used in shops, showrooms, offices and hotels) with:

an expected working life of at least 25 years, and

a total purchase cost of more than £100,000 in a 12-month period.

The expected working life relates to the capability of the plant and machinery, not

just the expected useful life for the current owner.

The £100,000 limit must be time-apportioned in a short accounting period and is

divided equally between the number of associated companies where the company is

a member of a group.