ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 165

Step 1

Work out which tax year is the tax year of change.

This is the earlier of the first tax year where:

the accounts are prepared to the new accounting date, or

the accounts are not prepared to the old accounting date.

Usually these two events happen in the same tax year, but they could occur in

different tax years.

Step 2

Work out the trading income assessment of the year before the tax year of change

on a normal CYB basis using the old accounting date.

Step 3

Work out the trading income assessment of the year after the tax year of change on

a normal CYB basis using the new accounting date.

Step 4

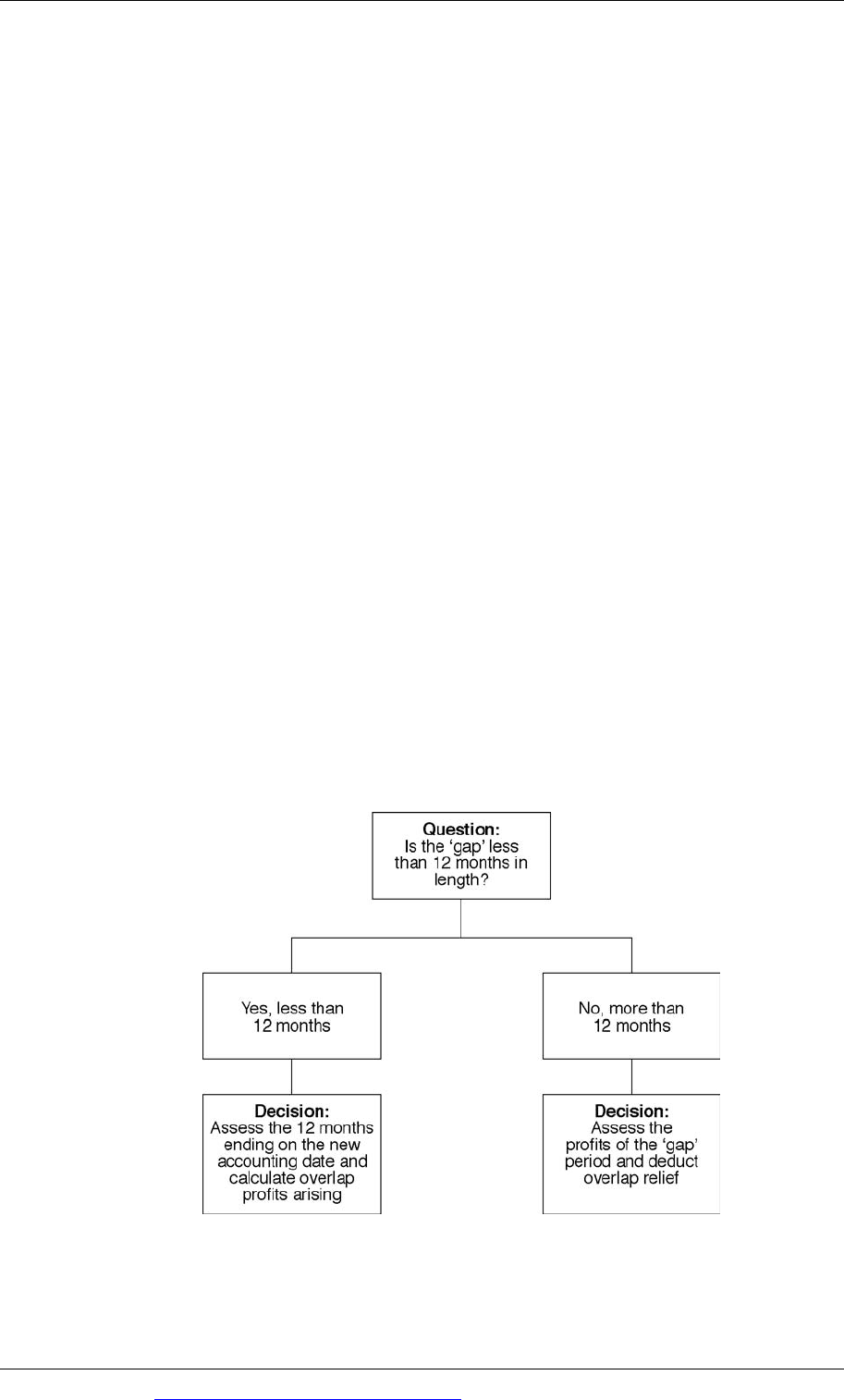

Work out the length of the relevant period, often referred to as the gap period.

This is the period that is not assessed in step 2 or step 3.

Step 5

Work out the trading income assessment in the tax year of change as follows:

If the gap period is less than 12 months, some profits will be assessed more than

once. Relief is given for these overlap profits in the last tax year on the cessation of

trade (or possibly earlier if there is another change of accounting date).

Paper F6 (UK): Taxation FA2009

166 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Where the gap period is more than 12 months, overlap relief is available. This is

because the basis of assessment rules only seek to assess 12 months’ profits each tax

year. As the gap profits exceed 12 months, the appropriate number of months of

overlap profits can be deducted so that only 12 months are assessed in the tax year

of the change.

Overlap relief is calculated as follows:

profits overlap of months of Number

months 12 — period gap the ofLength

profits Overlap ×

From these rules there are three main scenarios that could occur. These are

illustrated in the examples that follow.

Example 1

Paul prepared his accounts to 31 December each year until 2009 when he changed

his accounting date by preparing a short set of accounts to 30 September 2009. His

adjusted profits after capital allowances are as follows:

Adjustedprofitaftercapitalallowances

£

Yearended31December2008 42,000

9monthsended30September2009

37,800

Yearended30September2010

63,000

In his opening years, Paul had three months of overlap profits of £12,000.

Required

Calculate the trading income assessments arising from these accounting profits, and

state how much overlap profits are carried forward for relief in the future.

Answer

Step 1. Work out the tax year of change

The tax year of change = 2009/10 = the earlier of the first tax year where the

accounts are:

(1) prepared to the new accounting date (i.e. 2009/10), or

(2) not prepared to the old accounting date (i.e. also 2009/10 in this example)

Step 2. Work out the trading income assessment for the year before the tax year of

change

This is tax year 2008/09.

CYB: Trading income assessed on profits for the year ended 31.12.2008: £42,000.

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 167

Step 3. Work out the trading income assessment for the year after the tax year of

change

In this example, the year after the tax year of change is 2010/11

Trading income assessed on profits for the year ended 30.09.2010: = £63,000.

Step 4: Work out the length of the gap period

The period not assessed under steps 2 and 3 = 1 January 2009 to 30 September 2009.

Gap period = 9 months.

Step 5: Work out the trading income assessment in the tax year of change

Gap period is less than 12 months. Therefore assess the 12 months ending on the

new accounting date in the tax year 2009/10.

Taxyear

Basisperiod

Workings(nearestmonth)

Trading

income

assessment

£

2009/10 1.10.2008–30.9.2009 (3/12×£42,000)+£37,800 48,300

Step 6: Calculate the overlap profits

£

Openingyears

12,000

Onchangeofaccountingdate 1.10.2008–31.12.2008 (3/12×£42,000) 10,500

Overlapprofitstocarryforward

22,500

Example 2

Rosemary prepared her accounts to 31 December each year until 2009 when she

changed her accounting date by preparing a long set of accounts to 28 February

2010. Her adjusted profits after capital allowances are as follows:

Adjustedprofitaftercapitalallowances

£

Yearended31December2008 54,600

14monthsended28February2010

63,000

Yearended28February2011

52,500

In her opening years, Rosemary had three months of overlap profits of £12,000.

Required

Calculate the trading income assessments arising from these accounting profits, and

state how much overlap profits are carried forward for relief in the future.

Paper F6 (UK): Taxation FA2009

168 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

The tax year of change = 2009/10.

This is the earlier of the first tax year where the accounts are

(1) prepared to the new accounting date (i.e. 2009/10), or

(2) not prepared to the old accounting date (i.e. also in 2009/10 in this example).

Trading income assessment for the year before the change: 2008/09

CYB: Trading income assessed on profits for the year ended 31.12.2008: £54,600.

Trading income assessment for the year after the change: 2010/11

CYB: Trading income assessed on profits for the year ended 28.02.2011 £52,500.

Period not assessed = 1 January 2009 to 28 February 2010

Gap period = 14 months.

Gap period is more than 12 months

Therefore assess the profits of the gap period and deduct overlap relief

£

Profitsofthegapperiod(1.1.2009–28.2.2010)

63,000

Minusoverlaprelief

3

1214

00012

‐

, ×

(8,000)

Tradingincomeassessmentfor2009/10 55,000

Overlap profits

£

Openingyears

12,000

Onchangeofaccountingdate –amountrelieved

(8,000)

Overlapprofitstocarryforward

4,000

Note

If Rosemary had chosen 31 March 2010 as her new accounting date, she could have

relieved all of her overlap profits.

Example 3

Simon prepared his accounts to 30 September each year until 2010 when he changed

his accounting date by preparing a short set of accounts to 31 March 2010. His

adjusted profits after capital allowances are as follows:

Chapter 8: The basis of assessment rules for unincorporated businesses

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 169

Adjustedprofitaftercapitalallowances

£

Yearended30September2008 15,000

Yearended30September2009

12,000

6monthsended31March2010

8,500

Yearended31March2011

10,000

In his opening years, Simon had six months of overlap profits of £9,000.

Required

Calculate the trading income assessments arising from these accounting profits, and

state how much overlap profits are carried forward for relief in the future.

Answer

The tax year of change = 2009/10 = the earlier of the first tax year where the

accounts are:

(1) prepared to the new accounting date (i.e. 2009/10), or

(2) not prepared to the old accounting date (i.e. 2010/11 in this example).

Trading income assessment for the year before the change: 2008/09

CYB: Trading income assessed on profits for the year ended 30.09.2008: £15,000.

Trading income assessment for the year after the change: 2010/11

CYB: Trading income assessed on profits for the year ended 31.03.2011: £10,000.

Period not assessed = 1 October 2008 to 31 March 2010. Gap period = 18 months.

Gap period is more than 12 months therefore assess the profits of the gap period

and deduct overlap relief.

£

Profitsofthegapperiod(1.10.2008–31.3.2010)

Yearended30September2009 12,000

6monthsended31March2010 8,500

Minusoverlaprelief

6

1218

0009

‐

, ×

(9,000)

––––––––––––––––––––––––––––––

–

–

Tradingincomeassessmentfor2009/10 11,500

––––––––––––––––––––––––––––––

–

–

Overlap profits

£

Openingyears

9,000

Onchangeofaccountingdate –amountrelieved

(9,000)

–––––––––––––––––––––––––––

–

–

Overlapprofitstocarryforward Nil

––––––––––––––––––––

–

––––––

–

–

Paper F6 (UK): Taxation FA2009

170 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 171

Paper F6 (UK)

Taxation FA2009

CHAPTER

9

Trading losses of an

unincorporated business

Contents

1 Overview of trading losses

2 The carry forward of trading losses

3 Relief against total income

4 Loss relief in the opening years

5 Loss relief in the closing years

6 Tax planning

Paper F6 (UK): Taxation FA2009

172 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Overview of trading losses

The calculation of trading losses

The loss relief available

1 Overview of trading losses

1.1 The calculation of trading losses

A trading loss occurs when a sole trader or a partnership has:

an adjusted trading loss before capital allowances that is increased by the

addition of capital allowances, or

an adjusted trading profit before capital allowances that becomes a loss when

capital allowances are deducted.

If a trading loss occurs, the trading income assessment for the appropriate tax year

is £Nil.

1.2 The loss relief available

A range of loss reliefs is available to individuals who incur a trading loss.

The reliefs available depend on whether or not the business is:

in its opening years,

in its closing years, or

neither starting to trade nor closing down (an ongoing business).

An individual will choose to make use of his trading loss in the best way, by

applying the tax planning principles described at the end of this chapter.

Ongoing business

The following reliefs for trading losses are available to an ongoing unincorporated

business.

(1) Carry forward the trading loss and set it off against the first available profits

from the trade that produced the loss.

(2) Make a claim to set off the trading loss against the total income of the

individual:

− in the tax year of the loss, and/or

− in the preceding tax year.

(3) Make a claim as in 2 above and then claim additional relief against trading

profits of the three preceding tax years. (This additional form of loss relief

only applies to losses incurred in 2009/10.)

Chapter 9: Trading losses of an unincorporated business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 173

(4) Make a claim to extend the relief in 2 above to set off the trading loss against

the net gains of the individual:

− in the tax year of the loss, and/or

− in the preceding tax year.

Business in its opening years

In addition to the options for an ongoing business, an individual whose business is

in its opening years can claim the following relief.

(5) Make a claim to set off the trading loss against the total income of the three tax

years preceding the tax year of the loss.

Business in its closing years

The following reliefs for trading losses are available to an individual whose business

is in its closing years:

(1) Make a claim to set off the trading loss against the total income of the

individual:

− in the tax year of the loss, and/or

− in the preceding tax year.

(2) Make a claim to extend the relief in 2 above, to set off the trading loss against

the net gains of the individual:

− in the tax year of the loss, and/or

− in the preceding tax year.

(3) Make a claim to set off the trading loss against the trading income of the

individual:

− in the tax year of the loss and

− in the preceding three tax years.

(4) If the cessation of trade is due to the transfer of the business to a company (i.e.

the incorporation of the business), unrelieved losses can be carried forward

against future income derived by the individual from the new company.

These rules are explained in the rest of this chapter, except for relief against net

gains which is explained in a later chapter.

Note: section numbers and the Income Tax Act 2007

The rules on reliefs for trading losses are now contained in the Income Tax Act 2007.

Knowledge of section numbers is not required for the examination. However, using

section numbers can useful in an income tax loss computation, and so they are used

in this text. You will not be penalised if you quote section numbers incorrectly in an

answer to an examination question.

Paper F6 (UK): Taxation FA2009

174 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The carry forward of trading losses

The rules of s83 ITA 2007

2 The carry forward of trading losses

2.1 The rules of s83 ITA 2007

The rules for the carry forward of trading losses for an unincorporated business are

contained in section 83 of the ITA 2007.

Income tax trading losses can be carried forward indefinitely, but the following

rules apply.

The trading loss must

be set off against:

Explanation:

The first available They must be set off in the next tax year if possible.

An individual cannot choose to miss out a tax year,

for example to obtain a higher rate of tax relief.

Trading profits Set-off is against trading income only.

Trading losses carried forward cannot be set off

against other income or gains.

Of the trade which

produced the loss

If an individual operates more than one type of

trading activity, trading losses carried forward can

only be set off against future profits from the activity

that produced the loss. They cannot be set off against

profits of a different trading activity.

Using as much as

possible of the trading

loss

In each future tax year, the maximum amount of

trading loss must be set off until relief has been given

for the total trading loss.

The effect of this is that the loss to be relieved in any

tax year is the lower of:

- the loss available, and

- the trading profit of the tax year.

Trading losses will be carried forward automatically and relieved in this way,

unless the individual claims another type of loss relief.

The amount of trading loss available to carry forward under s83 must be agreed

with HMRC within four years of the end of the tax year in which the loss was

incurred.