ACCA F5 Performance Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 335

Performance measurement in service industries: the building block

model of Fitzgerald and Moon

The characteristics of services and service industries

Performance in service industries: Fitzgerald and Moon

Dimensionsof performance

Standards of performance

Rewards for performance

6 Performance measurement in service industries: the

building block model of Fitzgerald and Moon

6.1 The characteristics of services and service industries

Many organisations provide services rather than manufacture products. There are

many examples of service industries: hotels, entertainment, the holiday and travel

industries, professional services, banking, cleaning services, and so on.

Performance measurement for services may differ from performance measurement

in manufacturing in several ways:

Simultaneity. With a service, providing the service (‘production’) and receiving

consumption the service (‘consumption’ by the customer) happen at the same

time. In manufacturing, the making of the product happens before the customer

buys it.

Perishability. It is impossible to store a service for future consumption: unlike

manufacturing and retailing, there is no inventory of unused services. The

service must be provided when the customer wants it.

Heterogeneity. A product can be made to a standard specification. With a

service provided by humans, there is variability in the standard of performance.

The service is different in some way each time that it is provided. For example,

even if they perform the same songs at several concerts, the performance of a

rock band at a series of concerts will be different each time.

Intangibility. With a service, there are many intangible elements of service that

the customer is given, and that individual customer might value. For example, a

high quality of service in a restaurant is often intangible, but noticed and valued

by the customer.

Since services differ to some extent from products, should performance setting and

performance measurement be different in service companies, compared with

manufacturing companies?

Paper F5: Performance management

336 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

6.2 Performance in service industries: Fitzgerald and Moon

Fitzgerald and Moon (1996) suggested that a performance management system in a

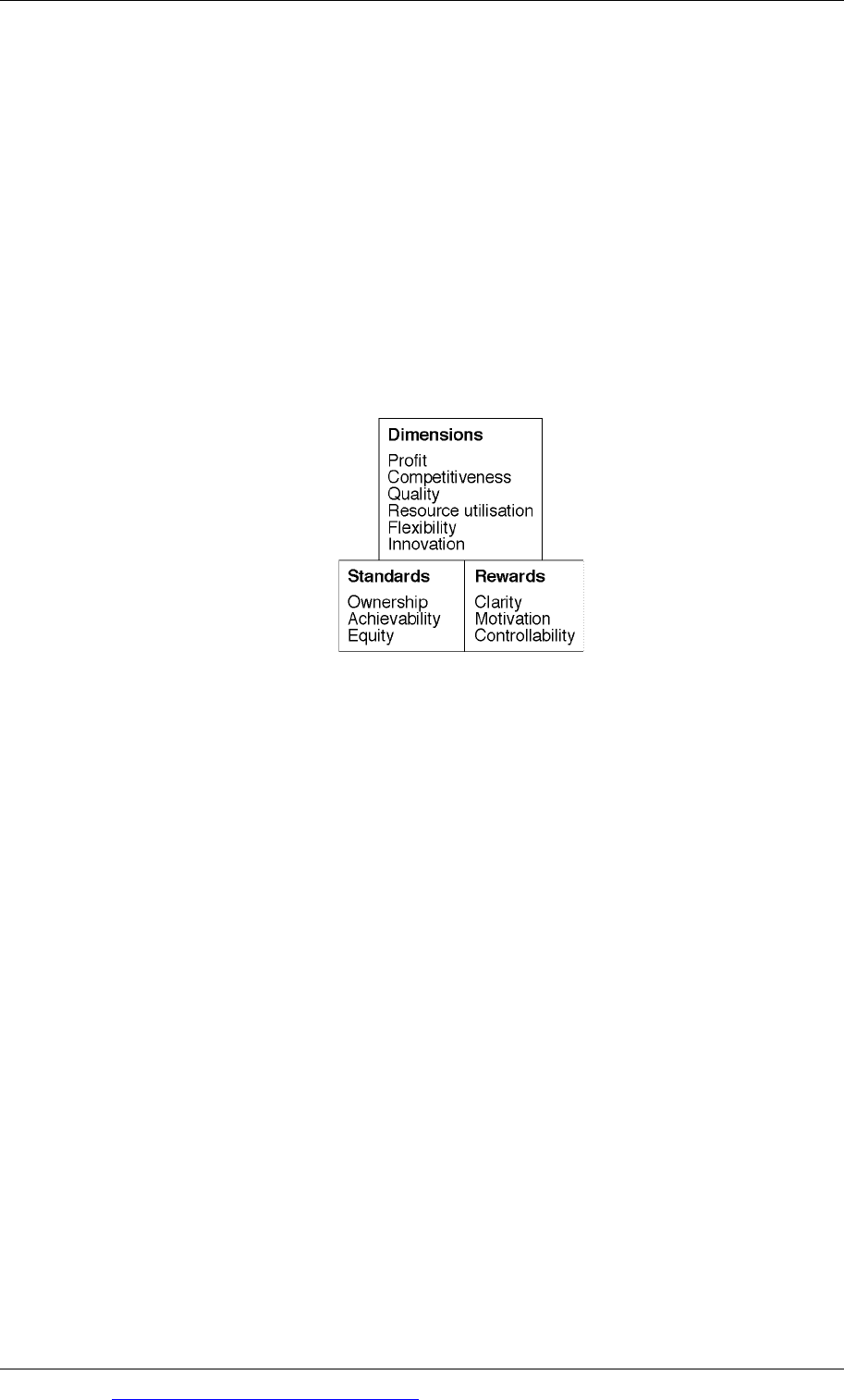

service organisation can be analysed as a combination of three building blocks:

dimensions

standards, and

rewards.

These are shown in the following diagram, which is known as the ‘building block

model’.

Building blocks for performance measurement systems

(Fitzgerald and Moon 1996)

6.3 Dimensions of performance

Dimensions of performance are the aspects of performance that are measured. To

establish a performance measurement system for a service industry, a decision has

to be made about the dimensions of performance that should be used for measuring

performance.

Research by Fitzgerald and others (1993) and by Fitzgerald and Moon (1996)

concluded that there are six aspects to performance measurement that link

performance to corporate strategy. These are:

profit (financial performance)

competitiveness

quality

resource utilisation

flexibility

innovation.

Performance measures should be established for each of these six dimensions. Some

performance measures that might be used for each dimension are set out in the

following table.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 337

Dimension of

performance

Possible measure of performance

Financial

performance

Profitability

Growth in profits

Profit margin

Note: Return on capital employed is possibly not so relevant

in a service industry, where the company employs fairly

small amounts of capital.

Competitiveness

Growth in sales

Retention rate for customers (or percentage of customers

who buy regularly: ‘repeat sales’)

Success rate in converting enquiries into sales

Market share

Service quality

Number of complaints

Whether the rate of complaints is increasing or decreasing

Customer satisfaction, as revealed by customer opinion

surveys

Number of errors discovered

Flexibility

Possibly the mix of different types of work done by

employees, to assess the flexibility of the work force

Possibly the speed in responding to customer requests, to

assess flexibility of response to customers’ needs

Resource

utilisation

Efficiency/productivity measures, such as material wastage

rates, rates of loss in production, labour efficiency

Utilisation rates: percentage of available time utilised in

‘productive’ activities, machine utilsation

Innovation

Number of new services offered

Percentage of total sales income that comes from services

introduced in the last one or two years

Other measures of performance might be appropriate for each dimension,

depending on the nature of the service industry. However, this framework of six

dimensions provides a structure for considering what measures of performance

might be suitable.

The dimensions of performance should also distinguish between:

‘results’ of actions taken in the past, and

‘determinants’ of future performance.

Some dimensions of performance measure the results of decisions that were taken

in the past, that have now had an effect. Fitzgerald and Moon suggested that results

of past actions are measured by:

financial performance and

competitiveness.

Paper F5: Performance management

338 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Other dimensions of performance will not have an immediate effect, and do not

measure the effects of decisions taken in the past. Instead they measure progress

towards achieving strategic objectives in the future. The ‘drivers’ or ‘determinants’

of future performance are:

quality

flexibility

resource utilisation

innovation.

These are dimensions of competitive success now and in the future, and so are

appropriate for measuring the performance of current management. Measuring

performance in these dimensions ‘is an attempt to address the short-termism

criticism frequently levelled at financially-focused reports’ (Fitzgerald). This is

because they recognise that by achieving targets now, future performance will

benefit. Improvements in quality, say, might not affect profitability in the current

financial period, but if these quality improvements are valued by customers, this

will affect profits in the future.

6.4 Standards of performance

The second part of the framework for performance measurement suggested by

Fitzgerald and Moon relates to setting expected standards of performance, once the

dimensions of performance have been selected. This considers behavioural aspects

of performance targets.

There are three aspects to setting standards of performance:

To what extent do individuals feel that they own the standards that will be used

to assess their performance? Do they accept the standards as their own, or do

they feel that the standard shave been imposed on them by senior management?

Do the individuals held responsible for achieving the standards of performance

consider that these standards are

achievable, or not?

Are the standards fair (‘equitable’) for all managers in all business units of the

entity?

It is recognised that individuals should ‘own’ the standards that will be used to

assess their performance, and managers are

more likely to own the standards when

they have been involved in the process of setting the standards

.

It has also been argued that if an individual accepts or ‘owns’ the standards of

performance, better performance will be achieved when the standard is more

demanding and difficult to achieve than when the standard is easy to achieve. This

means that the standards of performance that are likely to motivate individuals the

most are standards that will not be achieved successfully all the time. Budget targets

should therefore be challenging, but not impossible to achieve.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 339

Finding a balance between standards that the company thinks are achievable and

standards that the individual thinks are achievable can be a source of conflict

between senior management and their subordinates.

6.5 Rewards for performance

The third aspect of the performance measurement framework of Fitzgerald and

Moon is rewards. This refers to the structure of the rewards system, and how

individuals will be rewarded for the successful achievement of performance targets.

This aspect of performance also has behavioural implications.

One of the main roles of a performance measurement system should be to ensure

that strategic objectives are achieved successfully, by linking operational

performance with strategic objectives.

According to Fitzgerald, there are three aspects to consider in the reward system.

The system of setting performance targets and rewarding individuals for

achieving those targets must be clear to everyone involved. Provided that

managers accept their performance targets,

motivation to achieve the targets

will be greater when the targets are

clear (and when the managers have

participated in the target-setting process).

Employees may be motivated to work harder to achieve performance targets

when they are

rewarded for successful achievements, for example with the

payment of an annual bonus.

Individuals should only be held responsible for aspects of financial

performance that they can control

. This is a basic principle of responsibility

accounting. A common problem, however, is that some costs are incurred for the

benefit of several divisions or departments of the organisation. The

costs of

these shared services

have to be allocated between the divisions or departments

that use them. The principle that costs should be controllable therefore means

that the allocation of shared costs between divisions must be fair. In practice,

arguments between divisional managers often arise because of disagreements as

to how the shared costs should be shared.

Paper F5: Performance management

340 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 341

Paper F5

Performancemanagement

CHAPTER

13

Divisional performance

Contents

1 Divisional performance evaluation

2 Return on Investment (ROI)

3 Residual income (RI)

4 Divisional performance and depreciation

Paper F5: Performance management

342 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Divisional performance evaluation

Decentralisation of authority

Benefits of decentralisation

Disadvantages of decentralisation

Controllable profit and traceable profit

1 Divisional performance evaluation

1.1 Decentralisation of authority

Decentralisation involves the delegation of authority within an organisation. Within

a large organisation, authority is delegated to the managers of cost centres, revenue

centres, profit centres and investment centres.

A divisionalised structure refers to the organisation of an entity in which each

operating unit has its own management team which reports to a head office.

Divisions are commonly set up to be responsible for specific geographical areas or

product lines within a large organisation.

The term ‘decentralised divisionalised structure’ means an organisation structure in

which authority has been delegated to the managers of each division to decide

selling prices, choose suppliers, make output decisions, and so on.

1.2 Benefits of decentralisation

Decentralisation should provide several benefits for an organisation.

Decision-making should improve, because the divisional managers make the

tactical and operational decisions, and top management is free to concentrate on

strategy and strategic planning.

Decision-making at a tactical and operational level should improve, because the

divisional managers have better ‘local’ knowledge.

Decision-making should improve, because decisions will be made faster.

Divisional managers can make decisions ‘on the spot’ without referring them to

senior management.

Managers may be more motivated to perform well if they are empowered to

make decisions and rewarded for performing well against fair targets

Divisions provide useful experience for managers who will one day become top

managers in the organisation.

Within a large multinational group, there can be tax advantages in creating a

divisional structure, by locating some divisions in countries where tax

advantages or subsidies can be obtained.

Chapter 13: Divisional performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 343

1.3 Disadvantages of decentralisation

Decentralisation can lead to problems.

The divisional managers might put the interests of their division before the

interests of the organisation as a whole. Taking decisions that benefit a division

might have adverse consequences for the organisation as a whole. When this

happens, there is a lack of ‘goal congruence’.

Top management may lose control over the organisation if they allow

decentralisation without accountability. It may be necessary to monitor

divisional performance closely. The cost of such a monitoring system might be

high.

It is difficult to find a satisfactory measure of historical performance for an

investment centre that will motivate divisional managers to take the best

decisions. For example, measuring divisional performance by Return on

Investment (ROI) might encourage managers to make inappropriate long-term

investment decisions. This problem is explained in more detail later.

Economies of scale might be lost. For example, a company might operate with

one finance director. If it divides itself into three investment centres, there might

be a need for four finance directors – one at head office and one in each of the

investment centres. Similarly there might be a duplication of other systems, such

as accounting system and other IT systems.

1.4 Controllable profit and traceable profit

Profit is a key measure of the financial performance of a division. However, in

measuring performance, it is desirable to identify:

costs that are controllable by the manager of the division, and also

costs that are traceable to the division. These are controllable costs plus other

costs directly attributable to the division over which the manager does not have

control.

There may also be an allocation of general overheads, such as a share of head office

costs.

In a divisionalised system, profit centres and investment centres often trade with

each other, buying and selling goods and services. These are internal sales, priced at

an internal selling price (a ‘transfer price’). Reporting systems should identify

external sales of the division and internal sales as two elements of the total revenue

of the division. Transfer prices are the subject of the next chapter.

Paper F5: Performance management

344 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

$

External sales 600,000

Internal sales 150,000

Total sales 750,000

Costs controllable by the divisional manager:

Variable costs 230,000

Contribution 420,000

Controllable fixed costs 140,000

Profit attributable to the manager (controllable profit) 280,000

Costs traceable to the division but outside the manager’s control 160,000

Profit traceable to the division 120,000

Share of general overheads 30,000

Net profit 90,000

Notes

Controllable profit is used to assess the manager and is therefore sometimes

called the managerial evaluation.

Traceable profit is used to assess the performance of the division and is

sometimes called the economic evaluation.

The apportionment of general head office costs should be excluded from the

analysis of the manager’s performance and the division’s performance.

These profit measures can be used with variance analysis, ratio analysis, return on

investment, residual income and non-financial performance measurements to

evaluate performance.