ACCA F5 Performance Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 325

Variability in the circumstances of different businesses

With financial performance measurement, there are a limited number of financial

ratios that are used, which can be applied to all types of business.

With NFPIs, the key measures of performance vary between different types of

business, and depend on the nature of the business. For example, the key non-

financial measures of performance for a chemical manufacturer will differ from

those of a passenger transport company such as a bus or train company.

Time scale for achievement

Financial performance targets are often set for a budget period, and actual

performance is compared against budget. Non-financial performance targets need

not be restricted to one year, and in some cases it may be sensible to establish targets

for a longer term (or possibly a shorter term) than one year.

Unfortunately, if some employees are awarded cash bonuses for achieving non-

financial performance targets, there will be a tendency to set annual targets in order

to fit in with the annual budget cycle.

Setting targets for quality

The quality of a product or service may be a key aspect of non-financial

performance. However, it can be very difficult to define what is meant by ‘quality’.

For example, quality could refer to:

Features of a product design or aspects of a service

The number of mistakes that are made in a process

The number of rejected items in quality inspection

Value for money.

There are different aspects of quality, but for the purpose of performance

measurement it is necessary to identify which are the critical or key aspects of

quality, and set quality performance targets accordingly.

3.2 Analysing NFPIs

You need to remember the guidance from the F5 examiner about measuring and

assessing performance. The same guidance applies to non-financial performance as

to financial performance.

It is not sufficient simply to calculate a performance ratio or other performance

measurement.

You need to explain the significance of the ratio – What does it mean? Does it

indicate good or bad performance, and why?

Look at the background information given in the exam question and try to

identify a possible cause or reason for the good or bad performance.

Possibly, think of a suggestion for improving performance. What might be done

by management to make performance better?

Paper F5: Performance management

326 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

3.3 NFPIs in service industries

Management accounting has its origins in manufacturing and construction

industries. Over time, service industries have become a much more significant

aspect of business, especially in countries with developed economies.

Performance measures – both financial and non-financial – are needed for service

industries, but the key measures that are best suited to service industries are often

very different from the key NFPIs in manufacturing.

Even some of the key financial performance measures in service industries may be a

combination of both financial and non-financial performance, such as:

Annual sales revenue per cubic metre of shelf space (ratio used by supermarkets

and other stores)

Cost per tonne-mile carried (road haulage companies)

Cost per passenger-mile carried (transport companies)

Average income per consultant day (management consultancy company).

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 327

The balanced scorecard approach

The concept of the balanced scorecard

The balanced scorecard: four perspectives of performance

Using the balanced scorecard

Conflicting targets for the four perspectives

4 The balanced scorecard approach

4.1 The concept of the balanced scorecard

The balanced scorecard approach was developed by Kaplan and Norton in the

1990s as an approach to measuring performance in relation to long-term objectives.

They argued that for a business entity, the most important objective is a financial

objective. However, in order to achieve financial objectives over the long term, it is

also necessary to achieve goals or targets that are non-financial in nature, as well as

financial.

The concept of the balanced scorecard is that there are several aspects of

performance (‘perspectives on performance’) and targets should be set for each of

them. The different #perspectives’ may sometimes appear to be in conflict with each

other, because achieving an objective for one aspect of performance could mean

having to make a compromise with other aspects of performance. The aim should

be to achieve a satisfactory balance between the targets for each of the different

perspectives on performance. These targets, taken together, provide a balanced

scorecard, and actual performance should be measured against all the targets in the

scorecard.

The reason for having a balanced scorecard is that by setting targets for several key

factors, and making compromises between the conflicting demands of each factor,

managers will take a more balanced and long-term view about what they should be

trying to achieve. A balanced scorecard approach should remove the emphasis on

financial targets and short-term results.

However, although a balanced scorecard approach takes a longer-term view of

performance, it is possible to set shorter-term targets for each item on the scorecard.

In this way it is possible to combine a balanced scorecard approach to measuring

performance with the annual budget cycle, and any annual incentive scheme that

the entity may operate.

4.2 The balanced scorecard: four perspectives of performance

In a balanced scorecard, critical success factors are identified for four aspects of

performance, or four ‘perspectives’:

customer perspective

internal perspective

Paper F5: Performance management

328 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

innovation and learning perspective

financial perspective.

Of these four perspectives, three are non-financial in nature.

For each perspective, Kaplan and Norton argued that an entity should identify key

performance measures and key performance targets. The four perspectives provide

a framework for identifying what those measures should be, although the specific

measures used by each entity will vary according to the nature of the entity’s

business.

For each perspective, the key performance measures should be identified by

answering a key question. The answer to the question indicates what are the most

important issues. Having identified the key issues, performance measures can then

be selected, and targets set for each of them.

Perspective The key question

Customer

perspective

What do customers value?

By recognising what customers value most, the entity can focus

its performance targets on satisfying the customer more

effectively. Targets might be developed for several aspects of

performance such as cost (value for money), quality or place of

delivery.

Internal

perspective

To achieve its financial and customer objectives, what processes

must the organisation perform with excellence?

Management should identify the key aspects of operational

performance and seek to achieve or maintain excellence in this

area. For example, an entity may consider that customers value

the quality of its service, and that a key aspect of providing a

quality service is the effectiveness of its operational controls in

preventing errors from happening.

Innovation

and learning

perspective

How can the organisation continue to improve and create value?

The focus here is on the ability of the organisation to maintain its

competitive position, through the skills and knowledge of its

work force and through developing new products and services, or

making use of new technology as it develops.

Financial

perspective

How does the organisation create value for its owners?

Financial measures of performance in a balanced scorecard

system might include share price growth, profitability and return

on investment.

Several measures of performance may be selected for each perspective, or just one.

Using a large number of different measures for each perspective adds to the

complexity of the performance measurement system.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 329

4.3 Using the balanced scorecard

With the balanced scorecard approach the focus should be on strategic objectives

and the critical success factors necessary for achieving them. The main focus is on

what needs to be done now to ensure continued success in the future.

The main performance report for management each month is a balanced scorecard

report, not budgetary control reports and variance reports.

Examples of measures of performance for each of the four perspectives are as

follows. This list is illustrative only, and entities may use different measurements.:

Perspective Outcome measures

Critical financial

measures

Return on investment

Profitability and profitability growth

Revenue growth

Productivity and cost control

Cash flow and adequate liquidity

Avoiding financial risk: limits to borrowing

Critical customer

measures

Market share and market share growth

Customer profitability: profit targets for each

category of customer

Attracting new customers: number of new customers

or percentage of total annual revenue obtained from

new customers during the year

Retaining existing customers

Customer satisfaction, although measurements of

customer satisfaction may be difficult to obtain

On-time delivery for customer orders

Critical internal measures

Success rate in winning contract orders

Effectiveness of operational controls, measured by

the number of control failures identified during the

period

Production cycle time/throughput time

Amount of re-working of defective units

Critical innovation and

learning measures

Revenue per employee

Employee productivity

Employee satisfaction

Employee retention or turnover rates

Percentage of total revenue earned from sales of new

products

Time to develop new products from design to

completion of development and introduction to the

market

Paper F5: Performance management

330 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example: balanced scorecard

Kaplan and Norton described the example of Mobil in the early 1990s, in their book

The Strategy-focussed Organisation. Mobil, a major supplier of petrol, was competing

with other suppliers on the basis of price and the location of petrol stations. Its

strategic focus was on cost reduction and productivity, but its return on capital was

low.

The company’s management re-assessed their strategy, with the aim of increasing

market share and obtaining stronger brand recognition of the Mobil brand name.

They decided that the company needed to attract high-spending customers who

would buy other goods from the petrol station stores, in addition to petrol.

As its high-level financial objective, the company set a target of increasing return on

capital employed from its current level of about 6% to 12% within three years.

From a financial perspective, it identified such key success factors as

productivity and sales growth. Targets were set for productivity (reducing

operating costs per gallon of petrol sold) and ‘asset intensity’ (ratio of

operational cash flow to assets employed).

From a customer perspective, Mobil carried out market research into who its

customers were and what factors influenced their buying decisions. Targets

were set for providing petrol to customers in a way that would satisfy the

customer and differentiate Mobil’s products from rival petrol suppliers. Key

issues were found to be having petrol stations that were clean and safe, and

offering a good quality branded product and a trusted brand. Targets were set

for cleanliness and safety, speedy service at petrol stations, helpful customer

service and rewarding customer loyalty.

From an internal perspective, Mobil set targets for improving the delivery of its

products and services to customers, and making sure that customers could

always buy the petrol and other products that they wanted, whenever they

visited a Mobil station.

4.4 Conflicting targets for the four perspectives

A criticism that has been made against the balanced scorecard approach is that the

targets for each of the four perspectives might often conflict with each other. When

this happens, there might be disagreement about what the priorities should be.

This problem should not be serious, however, if it is remembered that the financial

is the most important of the four perspectives for a commercial business entity. The

term ‘balanced’ scorecard indicates that some compromises have to be made

between the different perspectives.

A useful sporting analogy was provided in an article in

Financial Management

magazine (Gering and Mntambo, November 2001). They compared the balanced

scorecard to the judgements of a football team manager during a football match. The

objective is to win the match and the key performance measure is the score.

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 331

However, as the match progresses, the manager will look at other important aspects

of performance, such as the number of shots at the goal by each side, the number of

corner kicks, the number of tackles and the percentage of possession of the ball

enjoyed by the team.

Shots on goal corner kicks, tackles and possession of the ball are all necessary factors

in scoring goals, not conceding goals, and winning the match. The manager will

therefore use them as indicators of how well or badly the match is progressing.

However, the score is ultimately the only thing that matters.

In the same way, targets for four perspectives are useful in helping management to

judge progress towards the company’s objectives, but ultimately, success in

achieving those objectives is measured in financial terms. The financial objective is

the most important.

Paper F5: Performance management

332 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

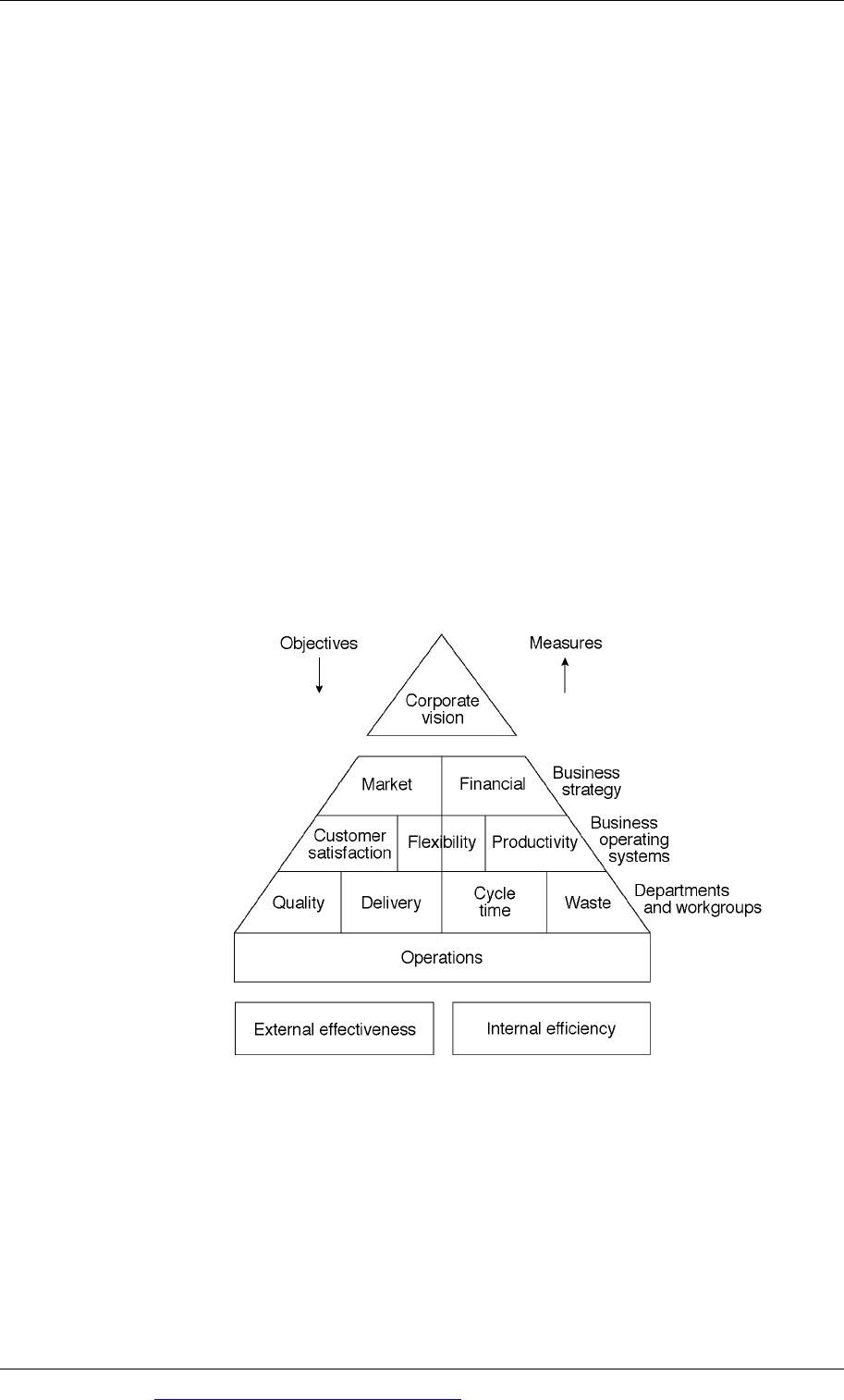

The performance pyramid

The concept of te performance pyramid

The pyramid structure: linking performance targets throughout an

organisation

Interpreting the performance pyramid

5 The performance pyramid

5.1 The concept of the performance pyramid

The performance pyramid is another approach to creating a structure for a

performance measurement system that combines non-financial and financial

performance indicators, and which helps to identify key areas of non-financial

performance.

The concept of a performance pyramid is based on the idea that an entity operates at

different levels and these levels form a hierarchy. The overall objective is at the top

of this hierarchy. Each level has different concerns and different performance

targets are appropriate for each level. However, performance objectives at a lower

level should support the performance objectives at a higher level. Taken together all

the performance objectives taken together support the overall objective of the

business as a whole.

Performance can therefore be seen as a pyramid structure, with a large number of

operational performance targets supporting higher-level targets, leading to targets

for the achievement of overall corporate objectives at the top.

5.2 The pyramid structure: linking performance targets throughout an

organisation

The performance pyramid model was developed by Lynch and Cross (1991. They

argued that traditional performance measurement systems were not as effective as

they should be, because they had a narrow financial focus – concentrating on

measures such as return on capital employed, profitability, cash flow and so on.

They argued that in a dynamic business environment, achieving strategic business

objectives depends on good performance with regard to non-financial aspects of

performance, and in particular:

Customer satisfaction. This is a ‘marketing’ objective: here, the focus is on

external/market effectiveness

Flexibility. The flexibility objective relates to both external effectiveness and

internal efficiency with in the organisation: an entity needs to respond to

developments and changes in circumstances when they occur.

Productivity: resource utilisation. Here, the focus is on internal efficiency, much

of which can be measured by financial performance and financial ratios or

variances)

Chapter 12: The scope of performance measurement

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 333

These key ‘driving forces’ can be monitored at the operational level with

performance measures relating to:

quality

delivery

cycle time (e.g. the length of the production cycle, or the length of the customer

order handling cycle) and

waste.

Lynch and Cross argued that within an organisation, there are different levels of

management and each has its own focus. However, there must be consistency

between performance measurement at each management level, so that performance

measures at the operational level support the corporate strategy.

They presented these ideas in the form of a pyramid of targets and performance that

links operations to corporate strategy.

A performance pyramid can be presented as follows:

Performance pyramid

5.3 Interpreting the performance pyramid

The performance pyramid links strategic objectives with operational targets,

internally-focused objectives with externally-focused objectives, and financial and

non-financial objectives.

Objectives and targets are set from the top level (corporate vision) down to the

operational level. Performance is measured from an operational level upwards.

If performance targets are achieved at the operational level, targets should be

Paper F5: Performance management

334 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

achieved at the operating systems level. Achieving targets for operating systems

should help to ensure the achievement of marketing and financial strategy

objectives, which in turn should enable the organisation to achieve its corporate

objectives.

A key level of performance measurement is at the operating systems level –

achieving targets for customer satisfaction, flexibility and productivity. To

achieve performance targets at this level, operational targets must be achieved -

for quality, delivery, cycle time and waste.

With the exception of flexibility, which has both an internal and an external

aspect, performance measures within the pyramid (and below the corporate

vision level) can be divided between:

- market measures, or measures of external effectiveness, and

- financial measures, or measures of internal efficiency.

The measures of performance are inter-related, both at the same level within the

pyramid and vertically, between different levels in the pyramid. For example:

- New product development is a business operating system. When a new

product is introduced to the market, success depends on meeting customer

needs (customer satisfaction), adapting customer attitudes and production

systems in order to make the changes (flexibility) and delivering the product

to the customer at the lowest cost for the required quality (productivity).

- Achieving improvements in productivity depends on reducing the cycle time

(from order to delivery) or reducing waste.

Lynch and Cross argued that the performance measures that are chosen should link

operations to strategic goals.

All operational departments need to be aware of how they are contributing to

the achievement of strategic goals.

Performance measures should be a combination of financial and non-financial

measures that are of practical value to managers. Reliable information about

performance should be readily available to managers whenever it is needed.