ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 3: Cost behaviour and cost estimation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 45

For example, it might be assumed that the total selling and distribution costs for a

company each month are mixed costs. If this assumption is used, the total mixed

costs can be divided into two separate parts, fixed costs and variable costs.

If costs can be analysed as a fixed amount of cost per period plus a variable cost per

unit, estimating what future costs should be, or what actual costs should have been,

becomes fairly simple.

Example

The management accountant of a manufacturing company has estimated that

production costs in a factory that manufactures Product Y are fixed costs of $250,000

per month plus variable costs of $3 per unit of Product Y output.

The expected output next month is 120,000 units of Product Y. Expected total costs

are therefore:

$

Variable costs (120,000 × $3) 360,000

Fixed costs 250,000

Total costs 610,000

Paper F2: Management Accounting

46 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

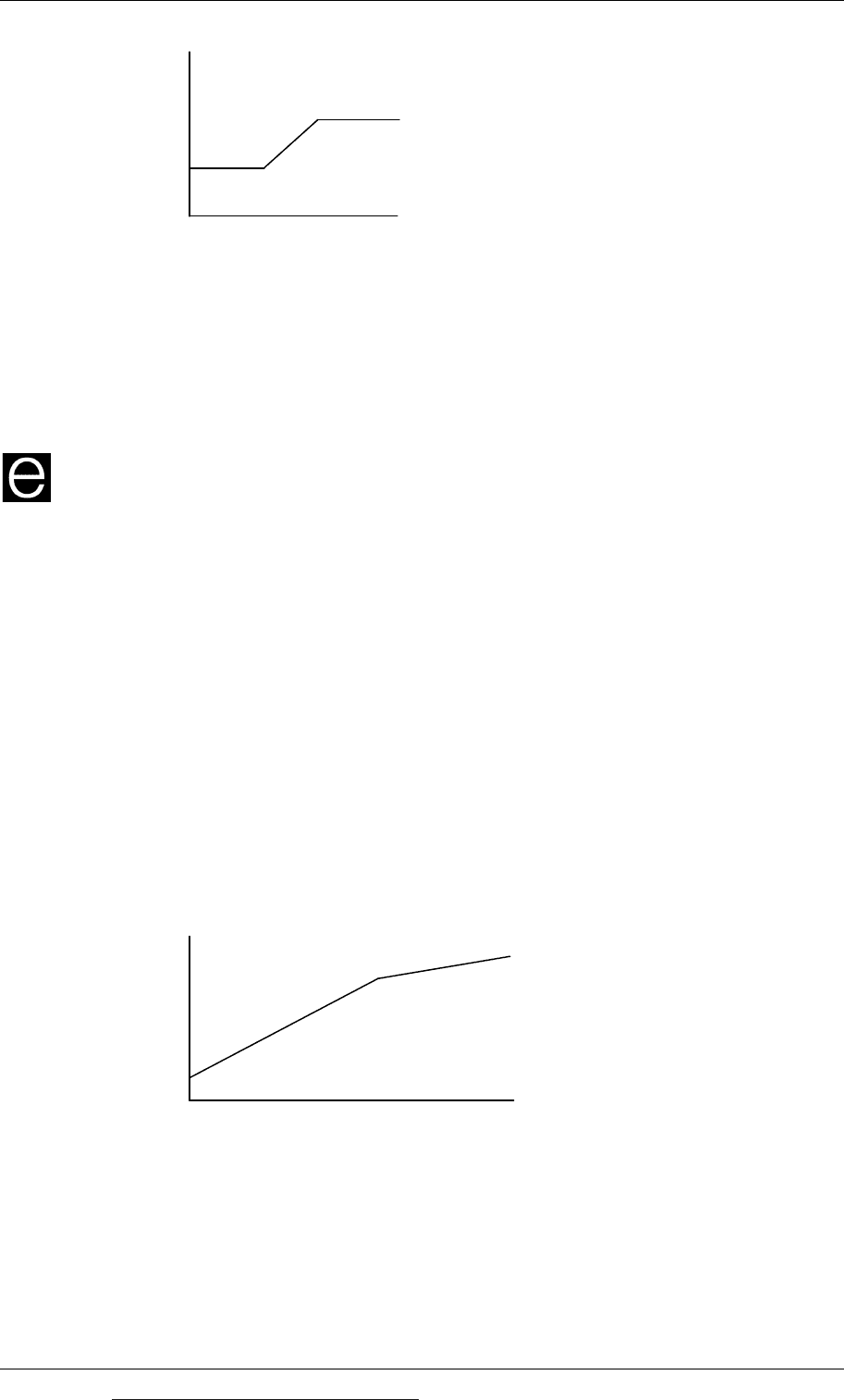

Other cost behaviour patterns

Stepped fixed cost

More unusual cost behaviour patterns

2 Other cost behaviour patterns

Some cost items are variable costs, fixed costs or mixed costs. Costs in total might

have a cost behaviour pattern that is very close to being a mixed cost. However

there are many cost items that have a more unusual cost behaviour pattern. Unusual

cost behaviour patterns can be shown on a cost behaviour graph.

2.1 Stepped fixed cost

A stepped fixed cost is a cost which:

has a fixed cost behaviour pattern within a limited range of activity, and

goes up or down in steps when the volume of activity rises above or falls below

certain levels.

On a cost behaviour graph, step fixed costs look like steps rising from left to right.

Total

cost

$

Activity level

Example

A company might pay its supervisors a salary of $4,000 each month. When

production is less than 3,500 hours each month, only one supervisor is needed: when

production is between 3,501 and 7,000 hours each month, two supervisors are

needed. When output is over 7,000 hours each month, three supervisors are needed.

These supervision costs are therefore fixed costs within a certain range of output,

b

ut go up or down in steps as the output level rises above or falls below certain

levels.

Chapter 3: Cost behaviour and cost estimation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 47

A cost behaviour graph for the supervision costs can be drawn as follows.

$

2.2 More unusual cost behaviour patterns

You may be examined on your understanding of more unusual cost behaviour

patterns. Several are shown below.

Changes in total variable costs

T

otal variable

costs

(a) (b)

Total variable

costs

Volume of activity

Volume of activity

In (a), the variable cost per unit is a particular amount up to a certain level of

activity or output, and is a lower amount for all units above that level of activity.

For example, the cost might be $2 per unit up to 10,000 units and $1.50 per unit for

each unit over 10,000 units.

In (b), the variable cost per unit is a particular amount up to a certain level of

activity or output, and above that level of activity the variable cost per unit is a

lower amount for all units (not just for the units above that level of activity). For

example, a supplier might offer a price of $5 per unit for all units of a raw material,

up to 10,000 units per order. If the size of an order is more than 10,000 units, the cost

per unit will be $4.75.

Minimum and maximum charges

The cost behaviour pattern in the graph below illustrates a cost during a period

when there is a charge per unit, subject to a minimum charge and a maximum

charge per period.

Paper F2: Management Accounting

48 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Total cost

Volume of activity

Other patterns

In your examination, you might be given another unusual cost behaviour pattern,

and asked to identify the type of cost to which the cost behaviour pattern relates.

You will need to study the pattern to identify its fixed and/or variable

characteristics, and try to identify what type of cost fits the pattern shown. Here is

just one example.

Example

Study the following cost behaviour graph and identify which of the following cost

items is shown in the graph.

Total electricity charges for a factory, where the electricity supplier charges:

A a fixed annual charge plus a constant amount for each unit of electricity

consumed, subject to a maximum annual charge

B a constant amount for each unit of electricity consumed up to a certain

amount, and a lower charge per unit for consumption above that amount

C a constant amount for each unit of electricity consumed but if consumption

exceeds a certain amount the charge is reduced to a lower amount for the

total amount consumed

D a fixed charge for the year, then a constant amount for each unit of electricity

consumed up to a certain amount, and a lower charge per unit for

consumption above that amount

£

Total

cost

0

Volume of activity

The cost behaviour graph shows that there is some charge even when consumption

is zero. This means that there must be a fixed cost element in the annual charge.

Total costs then rise in a straight-line fashion up to a certain level of consumption

(so variable costs are a constant amount per unit) and above that level total costs

continue to rise but the rate of increase is less steep (so variable costs are a new but

lower constant amount per unit).

The cost item shown in the graph must therefore be D.

Chapter 3: Cost behaviour and cost estimation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 49

Cost estimation: high/low method

Cost estimation

A linear cost function for total costs

High/low analysis

High/low analysis when there is a step change in fixed costs

High/low analysis when there is a change in the variable cost per unit

3 Cost estimation: high/low method

3.1 Cost estimation

For the purposes of planning and decision-making, it is often necessary to prepare

an estimate of costs. For example, it is often necessary to estimate the total annual

costs of an activity or a responsibility centre, or the total annual costs of production

overheads or marketing overheads.

Unless there are reasons for a different approach, it is usual to make a cost estimate

on the assumption that total costs (for a large number of different cost items

together) are a mixture of fixed costs and variable costs. In order to estimate costs, it

is therefore necessary to make an estimate of:

fixed costs for the period, and

the variable cost per unit of output or sales, or the variable cost per unit of

activity (for example, the variable cost per hour worked).

In the same way, individual items of mixed cost can be divided into fixed and

variable cost elements. Two cost estimation techniques are:

high/low analysis

linear regression analysis.

This chapter explains the high/low method. The linear regression method will be

explained in a later chapter.

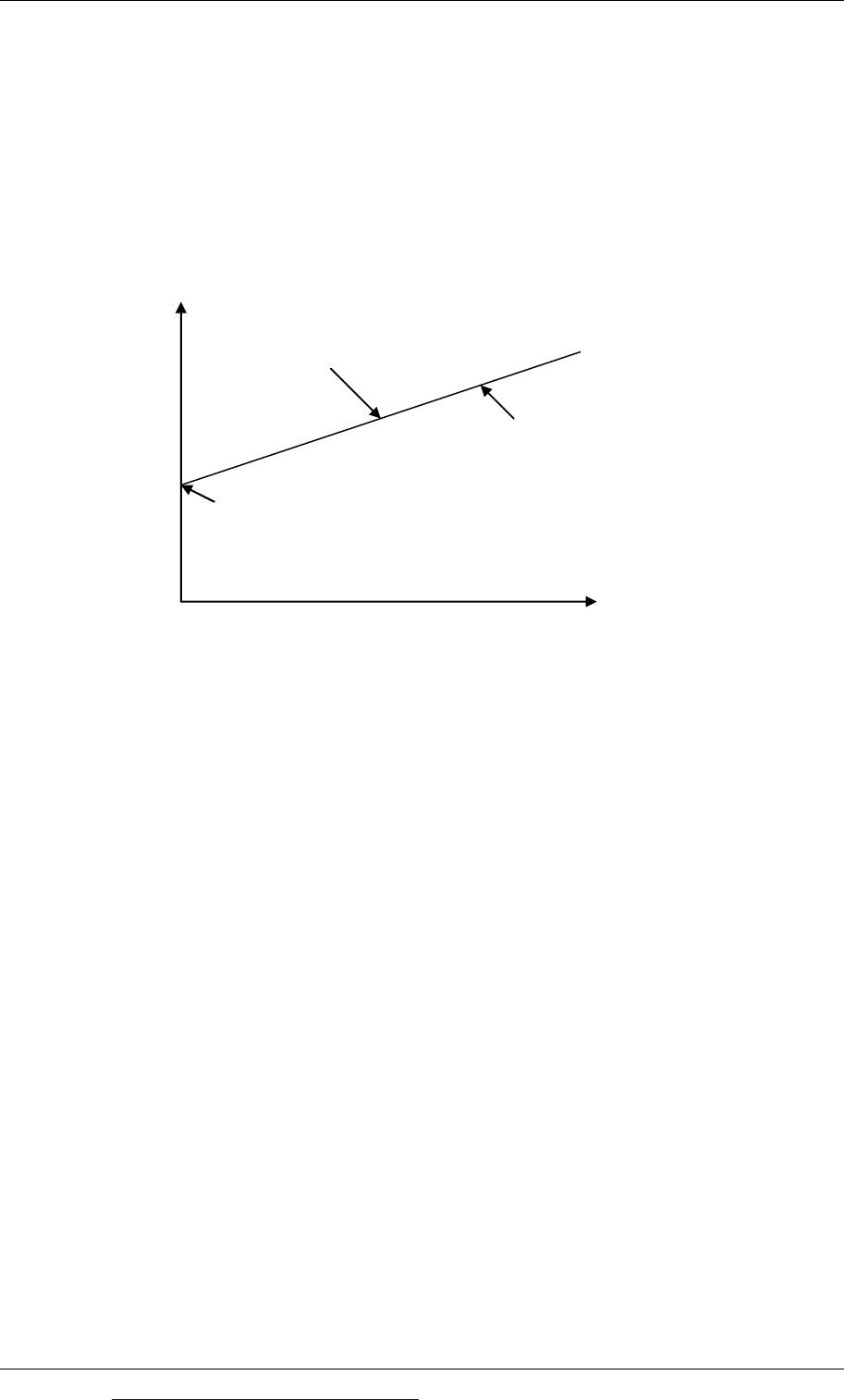

3.2 A linear function for total costs

If total costs can be divided into fixed costs or variable costs per unit of output or

unit of activity, a formula for total costs is:

y = a + bx

where

y = total costs in a period

x the number of units of output or the volume of activity in the period

a = the fixed costs in the period

Paper F2: Management Accounting

50 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

b = the variable cost per unit of output or unit of activity.

Graph of linear cost function

On a cost behaviour graph, total costs would be shown as a straight line, rising with

the total volume of activity. (It is a cost behaviour graph for a mixed cost.) This

rather simple formula is therefore a ‘linear function’ for total costs.

The linear cost function equation y = a + bx can be drawn as follows.

Total

cost

y

gradient of cost function = b

(variable cost per unit)

cost function

y = a + bx

(total cost line)

a = fixed cost

Volume of activit

y

x

3.3 High/low analysis

High/low analysis can be used to estimate fixed costs and variable costs per unit

whenever:

there are figures available for total costs at two different levels of output or

activity

it can be assumed that fixed costs are the same in total at each level of activity,

and

the variable cost per unit is constant at both levels of activity.

High/low analysis therefore uses two historical figures for cost:

the highest recorded output level, and its associated total cost

the lowest recorded output level, and its associated total cost.

It is assumed that these ‘high’ and ‘low’ records of output and historical cost are

representative of costs at all levels of output or activity.

The difference between the total cost at the high level of output and the total cost at

the low level of output is entirely variable cost. This is because fixed costs are the

same in total at both levels of output.

Chapter 3: Cost behaviour and cost estimation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 51

The method

There are just a few simple steps involved in high/low analysis.

Step 1

Take the activity level and cost for:

the highest activity level

the lowest activity level.

Step 2

The difference between the total cost of the highest activity level and the total cost of

the lowest activity level consists entirely of variable costs. This is because the fixed

costs are the same at all levels of activity.

Activity

level

$

High: Total cost of A

= TCa

Low: Total cost of B

= TCb

Difference: Variable cost of (A – B) units (A – B)

= TCa - TCb

From this difference, we can therefore calculate the variable cost per unit of activity.

Variable cost per unit = $(TCa – TCb)/ (A – B) units

Having calculated a variable cost per unit of activity, we can now calculate fixed

costs.

Step 3

Having calculated the variable cost per unit, apply this value to the cost of either the

highest or the lowest activity level. (It does not matter whether you use the high

level or the low level of activity. Your calculation of fixed costs will be the same.)

Calculate the total variable costs at this activity level.

Step 4

The difference between the total cost at this activity level and the total variable cost

at this activity level is the fixed cost.

Substitute in the ‘low’ equation Cost

$

Total cost of (low volume of activity) TCb

Variable cost of (low volume of activity) V

Therefore fixed costs per period of time TCb - V

You now have an estimate of the variable cost per unit and the total fixed costs.

The high/low method is a simple but important technique that you need to

understand. Study the following example carefully.

Paper F2: Management Accounting

52 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company has recorded the following costs in the past four months:

Month Activity

Total cost

Direct labour hours

$

January 5,800

40,300

February 7,700

47,100

March 8,200

48,700

April 6,100

40,650

Required

Using high/low analysis, prepare an estimate of total costs in May if output is

expected to be 7,000 direct labour hours.

Answer

(1) Steps 1 and 2: Calculate the variable cost per hour

Take the highest level of activity and the lowest level of activity, and the total costs

of each. Ignore the other data for levels of activity in between the highest and the

lowest.

Hours

$

High: Total cost of 8,200 hours

= 48,700

Low: Total cost of 5,800 hours

= 40,300

Difference: Variable cost of 2,400 hours

= 8,400

Therefore variable cost per direct labour hour = $8,400/2,400 hours = $3.50.

(2) Steps 3 and 4: Calculate fixed costs

Substitute in the ‘high’ equation Cost

$

Total cost of 8,200 hours 48,700

Variable cost of 8,200 hours (× $3.50 per hour) 28,700

Therefore fixed costs per month 20,000

(3) Using the cost analysis: Prepare a cost estimate

Cost estimate for May Cost

$

Fixed costs 20,000

Variable cost (7,000 hours × $3.50 per hour) 24,500

Estimated total costs 44,500

The technique can be used any time that you are given two figures for total costs, at

different levels of activity or volumes of output, and you need to estimate fixed

costs and a variable cost per unit.

Chapter 3: Cost behaviour and cost estimation

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 53

3.4 High/low analysis when there is a step change in fixed costs

High/low analysis can be used even when there is a step increase in fixed costs

between the ‘low’ and the ‘high’ activity levels, provided that the amount of the step

increase in fixed costs is known.

The method of analysis to use depends on whether the step increase in the fixed cost

is stated as a money amount of cost, or whether it is stated as a percentage increase.

The step increase in fixed costs is given as a money amount

If the step increase in fixed costs is given as a money amount, the total cost of the

‘high’ or the ‘low’ activity level should be adjusted by the amount of the increase, so

that total costs for the ‘high’ and ‘low’ amounts are the same.

The high/low method can then be used in the normal way to obtain a fixed cost and

a variable cost per unit. The fixed cost will be either the fixed cost at the ‘high’ level

or at the ‘low’ level, depending on how you made the adjustment to fixed costs

before making the high/low analysis. You can then calculate the fixed costs at the

other level of activity by adding or subtracting the step change in fixed costs, as

appropriate.

Example

A company has the following costs at two activity levels.

Activity Total cost

units $

17,000 165,000

22,000 195,000

The variable cost per unit is constant over this range of activity, but there is a step

fixed cost and total fixed costs increase by $15,000 when activity level equals or

exceeds 19,000 units.

Required

Using high/low analysis, calculate the total cost of 20,000 units.

Answer

There is an increase in fixed costs above 19,000 units of activity, and to use the

high/low method, we need to make an adjustment for the step fixed costs. Since we

are required to calculate the total cost for a volume of activity above 19,000 units, the

simplest approach is to add $15,000 to the total cost of 17,000 units, so that the fixed

costs of 17,000 units and 22,000 units are the same and are also the amount of fixed

costs for 20,000 units.

Paper F2: Management Accounting

54 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(1) Steps 1 and 2: Calculate the variable cost per unit

Units

$

High: Total cost 22,000 units

= 195,000

Low: Adjusted total cost: $(165,000 + 15,000) 17,000 units

= 180,000

Difference: Variable cost of 5,000 units

= 15,000

Therefore variable cost per unit = $15,000/5,000 units = $3 per unit.

(2) Steps 3 and 4: Calculate fixed costs (above 19,000 units)

Substitute in the ‘high’ equation Cost

$

Total cost of 22,000 units 195,000

Variable cost of 22,000 units (× $3 per unit) 66,000

Therefore fixed costs (above 19,000 units) 129,000

(3) Using the cost analysis: Prepare a cost estimate

Cost estimate Cost

$

Fixed costs (above 19,000 units) 129,000

Variable cost (20,000 units × $3) 60,000

Estimated total costs 189,000

The step increase in fixed costs is given as a percentage amount

When the step change in fixed costs between two activity levels is given as a

percentage amount, the problem is a bit more complex, and to use high/low

analysis we need a third figure for total cost, at another level of activity somewhere

in between the ‘high’ and the ‘low’ amounts.

Total fixed costs will be the same for:

the ‘in between’ activity level and

either the ‘high’ or the ‘low’ activity level.

High/low analysis should be applied to the two costs and activity levels for which

total fixed costs are the same, to obtain an estimate for the variable cost per unit and

the total fixed costs at these activity levels. Total fixed costs at the third activity level

(above or below the step change in fixed costs) can then be calculated making a

suitable adjustment for the percentage change.