ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 8: Marginal costing and absorption costing

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 185

3.2 The difference in profit between marginal costing and absorption costing

The profit for an accounting period calculated with marginal costing is different

from the profit calculated with absorption costing. The difference in profit is due

entirely to the differences in inventory valuation.

When there is no opening or closing inventory, exactly the same profit will be

reported using marginal costing and absorption costing.

The main difference between absorption costing and marginal costing is that:

in absorption costing, inventory cost includes a share of fixed production

overhead costs

in marginal costing, inventory cost contains no fixed production overhead costs.

The following rules may be applied to calculate the difference in the profit for a

period calculated with marginal costing and with absorption costing.

3.3 Calculating the difference in profit: increase in inventory during a

period

Look at the difference between the quantity of opening inventory and closing

inventory. Establish whether:

closing inventory is larger than opening inventory, or

closing inventory is less than opening inventory.

Closing inventory is higher than opening inventory when the quantity produced in

the period is more than the quantity sold. If the cost per unit is a constant amount,

using marginal costing or absorption costing, when the production quantity exceeds

the sales quantity:

There is an increase in inventory during a period

Closing inventory is therefore higher in value than opening inventory

The increase in inventory will be greater with absorption costing, by the amount

of the increase in fixed production costs in the inventory value

The production cost of sales is therefore lower with absorption costing than with

marginal costing, and the difference is this increase in fixed costs in the

inventory value

Therefore the profit is higher with absorption costing than with marginal

costing, by the amount of the increase in fixed costs in the inventory value.

Paper F2: Management Accounting

186 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

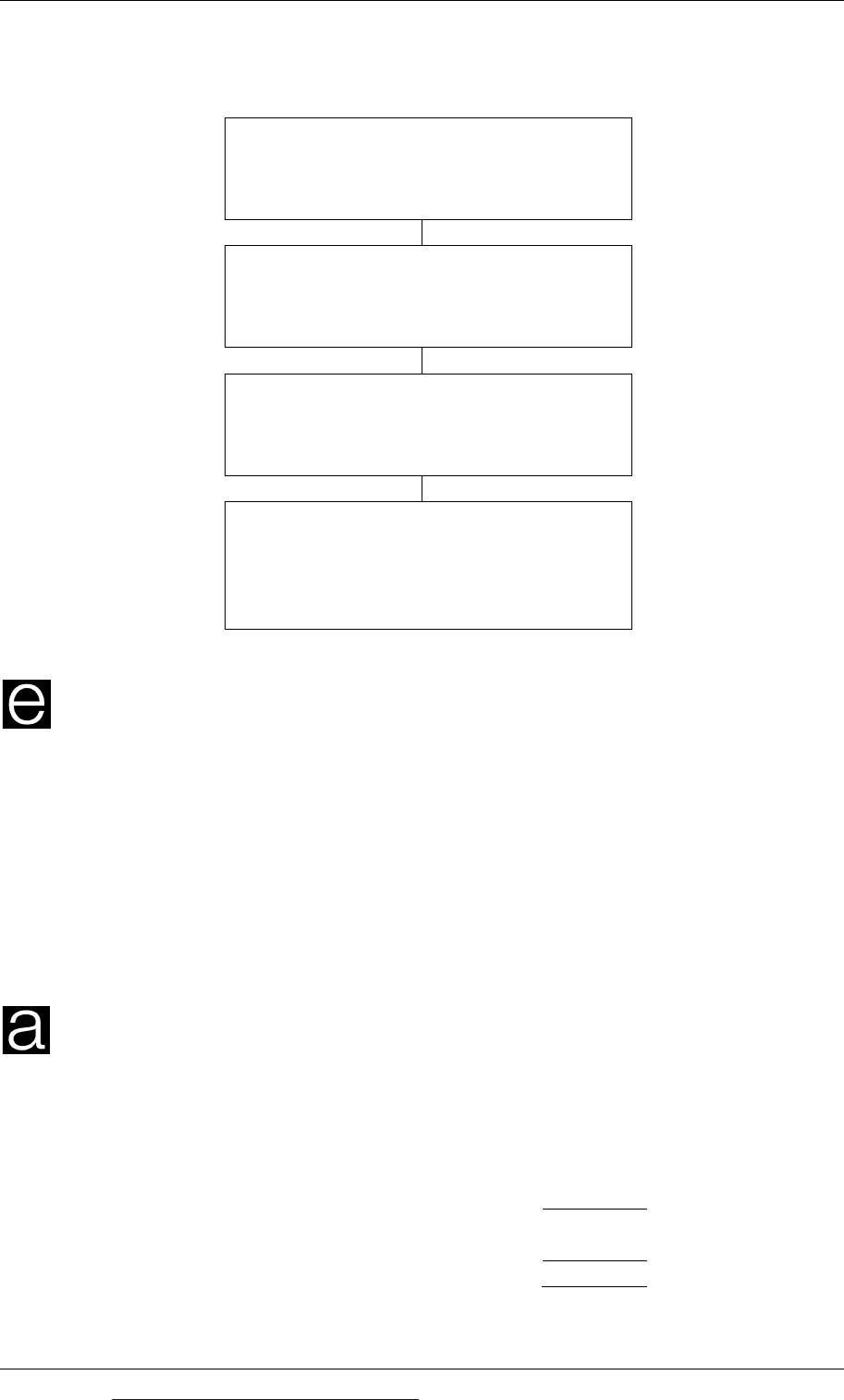

Basic rule: comparing marginal costing

and absorption costing profit

Production volume bigger than sales

volume

Increase in inventory

(closing – opening inventory)

Absorption costing profit higher than

marginal costing profit

Difference in profit = amount of fixed

production overhead in the increase in

inventory

Example

A company uses marginal costing. In the financial period that has just ended,

opening inventory was $8,000 and closing inventory was $15,000. The reported

profit for the year was $96,000.

If the company had used absorption costing, opening inventory would have been

$16,000 and closing inventory would have been $34,000.

Required

What would have been the profit for the year if absorption costing had been used?

Answer

There was an increase in inventory. It was $7,000 using marginal costing (= $15,000 –

$8,000). It would have been $19,000 using absorption costing.

$

Increase in inventory, marginal costing 7,000

Increase in inventory, absorption costing 19,000

Difference (profit higher with absorption costing) 12,000

Profit with marginal costing 96,000

Profit with absorption costing 108,000

Chapter 8: Marginal costing and absorption costing

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 187

The profit is higher with absorption costing because there has been an increase in

inventory (production volume has been more than sales volume.)

3.4 Calculating the difference in profit: reduction in inventory during a

period

When there is a reduction in inventory during a period, and closing inventory is

lower in value than opening inventory, the reverse situation applies.

Closing inventory is lower than opening inventory when the quantity sold exceeds

the quantity produced in the period. If the cost per unit is a constant amount, using

marginal costing or absorption costing, when the sales quantity exceeds the

production quantity:

There is a reduction in inventory during a period.

Closing inventory is therefore lower in value than opening inventory

The reduction in inventory will be greater with absorption costing, by the fixed

production costs in the amount by which inventory has been reduced.

The production cost of sales is therefore higher with absorption costing than

with marginal costing, and the difference is the amount of fixed production costs

in the reduction in inventory value.

Therefore the profit is lower with absorption costing than with marginal costing,

by the amount of the fixed costs in the fall in inventory value.

Basic rule: comparing marginal costing

and absorption costing profit

Sales volume bigger than production

volume

Reduction in inventory

(closing – opening inventory)

Absorption costing profit lower than

marginal costing profit

Difference in profit = amount of fixed

production overhead in the reduction in

inventory

Paper F2: Management Accounting

188 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company uses absorption costing. In the financial period that has just ended,

opening inventory was $76,000 and closing inventory was $49,000. The reported

profit for the year was $183,000.

If the company had used marginal costing, opening inventory would have been

$40,000 and closing inventory would have been $28,000.

Required

What would have been the profit for the year if marginal costing had been used?

Answer

There was a reduction in inventory. It was $27,000 using absorption costing (=

$76,000 – $49,000). It would have been $12,000 using marginal costing.

$

Reduction in inventory, absorption costing 27,000

Reduction in inventory, marginal costing 12,000

Difference (profit higher with marginal costing) 15,000

Profit with absorption costing 183,000

Profit with marginal costing 198,000

Profit is higher with marginal costing because there has been a reduction in

inventory during the period.

3.5 Summary: comparing marginal and absorption costing profit

An examination might test your ability to calculate the difference between the

reported profit using marginal costing and the reported profit using absorption

costing. To calculate the difference, you might need to make the following simple

calculations.

Calculate the increase or decrease in inventory during the period, in units.

Calculate the fixed production overhead cost per unit.

The difference in profit is the increase or decrease in inventory quantity

multiplied by the fixed production overhead cost per unit.

If there has been an increase in inventory, the absorption costing profit is higher.

If there has been a reduction in inventory, the absorption costing profit is lower.

You should ignore fixed selling overhead or fixed administration overhead.

These are written off in full as a period cost in both absorption costing and

marginal costing, and only fixed production overheads are included in

inventory values.

Chapter 8: Marginal costing and absorption costing

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 189

Example

The following information relates to a manufacturing company for the next costing

period.

Production 16,000 units Fixed production costs $80,000

Sales 14,000 units Fixed selling costs $28,000

Using absorption costing, the profit for this period would be $60,000

Required

What would have been the profit for the year if marginal costing had been used?

Answer

Ignore the fixed selling overheads. These are irrelevant since they do not affect the

difference in profit between marginal and absorption costing.

There is an increase in inventory by 2,000 units, since production volume (16,000

units) is higher than sales volume (14,000 units).

If absorption costing is used, the fixed production overhead cost per unit is $5 (=

$80,000/16,000 units).

The difference between the absorption costing profit and marginal costing profit

is therefore $10,000 (= 2,000 units × $5).

Absorption costing profit is higher, because there has been an increase in

inventory.

Marginal costing profit would therefore be $60,000 – $10,000 = $50,000.

Exercise 2

A company budgets to make 37,000 units of a product and fixed production costs are

expected to be $111,000.

The budgeted direct costs of production are $5 per unit, and there are no variable

overhead costs. Budgeted sales are 40,000 units and the sales price is $11 per unit.

Budgeted administration overheads and selling and distribution overheads are

$80,000 (all fixed costs).

Required

(a) Calculate the expected profit for the period using marginal costing.

(b) Having calculated the marginal costing profit, calculate what the absorption

costing profit would be for the period. (Assume that the cost per unit of

opening inventory is the same as the cost per unit of closing inventory.)

Paper F2: Management Accounting

190 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Advantages and disadvantages of absorption and marginal costing

Advantages and disadvantages of absorption costing

Advantages and disadvantages of marginal costing

4 Advantages and disadvantages of absorption and

marginal costing

The previous sections of this chapter have explained the differences between

marginal costing and absorption costing as methods of measuring profit in a period.

Some conclusions can be made from these differences.

The amount of profit reported in the cost accounts for a financial period will

depend on the method of costing used.

Since the reported profit differs according to the method of costing used, there

are presumably reasons why one method of costing might be used in preference

to the other. In other words, there must be some advantages (and disadvantages)

of using either method.

4.1 Advantages and disadvantages of absorption costing

Absorption costing has a number of advantages and disadvantages.

Advantages of absorption costing

Inventory values include an element of fixed production overheads. This is

consistent with the requirement in financial accounting that (for the purpose of

financial reporting) inventory should include production overhead costs.

Calculating under/over absorption of overheads may be useful in controlling

fixed overhead expenditure.

By calculating the full cost of sale for a product and comparing it will the selling

price, it should be possible to identify which products are profitable and which

are being sold at a loss.

Disadvantages of absorption costing

Absorption costing is a more complex costing system than marginal costing.

Absorption costing does not provide information that is useful for decision

making (like marginal costing does).

4.2 Advantages and disadvantages of marginal costing

Marginal costing has a number of advantages and disadvantages.

Chapter 8: Marginal costing and absorption costing

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 191

Advantages of marginal costing

It is easy to account for fixed overheads using marginal costing. Instead of being

apportioned they are treated as period costs and written off in full as an expense

the income statement for the period when they occur.

There is no under/over-absorption of overheads with marginal costing, and

therefore no adjustment necessary in the income statement at the end of an

accounting period.

Marginal costing provides useful information for decision making.

Contribution per unit is constant, unlike profit per unit which varies as the

volume of activity varies.

Disadvantages of marginal costing

Marginal costing does not value inventory in accordance with the requirements

of financial reporting. (However, for the purpose of cost accounting and

providing management information, there is no reason why inventory values

should include fixed production overhead, other than consistency with the

financial accounts.)

Marginal costing can be used to measure the contribution per unit of product, or

the total contribution earned by a product, but this is not sufficient to decide

whether the product is profitable enough. Total contribution has to be big

enough to cover fixed costs and make a profit.

Practice multiple choice questions

1 The costs and sales revenue in a period are as follows.

$000

Direct materials 24

Direct labour 36

Direct expenses 5

Variable production overheads 6

Fixed production overheads 70

Administration overheads 30

Variable selling overheads 8

Fixed selling overheads 35

Sales 250

What is the total contribution for the period?

A $171,000

B $176,000

C $179,000

D $184,000

(2 marks)

Paper F2: Management Accounting

192 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

2 The following information relates to a manufacturing company for the next costing

period.

Production 24,000 units Fixed production costs $96,000

Sales 25,000 units Fixed selling costs $75,000

Using marginal costing, the profit for this period would be $65,000

Required

What would have been the profit for the year if absorption costing had been used?

A $58,000

B $61,000

C $69,000

D $72,000

(2 marks)

3 The following information relates to a manufacturing company for the next costing

period.

Production 32,000 units Fixed production costs $160,000

Sales 30,000 units Fixed selling costs $30,000

Using absorption costing, the profit for this period would be $101,000

Required

What would have been the profit for the year if marginal costing had been used?

A $89,000

B $91,000

C $111,000

D $113,000

(2 marks)

4 The following information relates to a manufacturing company for the next costing

period.

Fixed production costs $125,000

Fixed selling costs $25,000

Production 25,000 units

The profit for the period using absorption costing would be $15,000 less than if

marginal costing were used.

Required

What is the expected sales volume in the period?

A 22,000 units

B 23,000 units

C 27,000 units

D 28,000 units

(2 marks)

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 193

Paper F2

Management Accounting

CHAPTER

9

Job costing, batch costing

and service costing

Contents

1 Jobcosting

2 Batchcosting

3 Servicecosting

Paper F2: Management Accounting

194 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Job costing

The nature of job costing

The cost of a job

Cost records and accounts for job costing

1 Job costing

Costing systems are used to record total costs. They are also used to record the costs

of individual cost units. The method used to measure the cost of cost units depends

on the production system and how the products are made.

1.1 The nature of job costing

Job costing is used when a business entity carries out tasks or jobs to meet specific

customer orders. Although each job might involve similar work, they are all

different and are carried out to the customer’s specific instructions or requirements.

Examples of ‘jobs’ include work done for customers by builders or electricians,

audit work done for clients by a firm of auditors, and repair work on motor vehicles

by a repair firm.

Job costing is similar to contract costing, in the sense that each job is usually

different and carried out to the customer’s specification or particular requirements.

However, jobs are short-term and the work is usually carried out in a fairly short

period of time. Contracts are usually long-term and might take several months or

even years to complete.

1.2 The cost of a job

A cost is calculated for each individual job, and this cost can be used to establish the

profit or loss from doing the job.

Job costing differs from most other types of costing system because each cost unit is

a job, and no two jobs are exactly the same. Each job is costed separately.

The expected cost of a job has to be estimated so that a price for the job can be

quoted to a customer.

A costing system should also calculate the actual cost of each job that has been

carried out.

A job costing system is usually based on absorption costing principles, and in

addition a cost is included for non-production overheads, as follows.