ACCA F1 Accountant in Business - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 5: History and role of accounting in business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 175

This legal requirement applies to companies only. However, tax law requires the

owners of sole trader businesses and business partners to maintain sufficient

accounting records so that their tax liability on the profits of their business can be

calculated.

2.2 Company law: duty to prepare financial statements

Companies are also required by law to prepare financial statements, usually for

each financial year of the company. The financial statements must be approved by

the directors of the company, who must be satisfied that they give a true and fair

view of assets, liabilities, financial position and profit or loss of the company for the

year.

With some exceptions, every company must prepare its own financial

statements. These are called individual company accounts.

Companies that own one or more subsidiary companies are called ‘parent

companies’ of a group of companies. Parent companies are required to prepare

consolidated accounts for the group as a whole, also called group accounts as if

the group of companies were a single operating company.

Financial statements consist of:

A statement of financial position (sometimes called a balance sheet), showing

the assets, liabilities and owners’ capital (‘equity capital’ or ‘share capital and

reserves’) of the company

an income statement, showing the profit or loss for the financial period

(financial year)

a statement of cash flows, showing the cash received and paid out by the

company during the year

a statement of changes in equity, showing how the component elements of the

owners’ capital has changed during the year

some additional information, in notes to the financial statements. For example,

UK company law requires companies to provide information about employee

numbers and costs.

In the UK, there is also a legal requirement for companies to prepare a directors’

report in addition to the financial statements and a report by the external auditors.

A company’s directors are required to provide a copy of the annual report and

accounts to each shareholder (and any other person entitled to receive a copy).

In most countries, public companies must present the annual report and accounts

to the shareholders in an annual general meeting of the company.

2.3 Company law: duty to file the annual report and accounts

Although the regulations vary for different types of company, there is a general

requirement for companies to submit a copy of their annual report and accounts

Paper F1: Accountant in business

176 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

with a government body. In the UK, companies are required to ‘file’ their annual

report and accounts with the Registrar of Companies.

Members of the public may (on payment of a suitable fee) obtain access to these

filed accounts, for the purpose of inspecting them.

2.4 Company law: the requirement for audited accounts

With some exceptions, a company’s annual accounts must be audited by

independent (‘external’) auditors, and the accounts must contain a statement by the

auditors (the auditors’ report) about whether in their view the accounts give a true

and fair view.

External auditing is explained in more detail in a later chapter.

2.5 Laws, regulations and the format and content of company accounts

National laws vary in the amount of detail that they specify concerning the format

and content of company accounts (the financial statements and notes to the

statements).

The law might specify how a statement of financial position or income statement

should be presented, and the minimum items that it should contain. However,

guidance on the format of the statement of financial position and income statement

is also provided on one of the international accounting standards.

Financial statements are prepared in accordance with some long-established

principles of accounting, such as the going concern concept and accruals concept.

These principles of accounting are not contained in company, but all businesses are

expected to comply with them when preparing financial statements.

Some regulatory bodies responsible for preparing accounting standards have

produced a statement of principles and guidelines. The most important of these is

the Framework for the Preparation and Presentation of Financial Statements,

which has been produced and published by the International Accounting Standards

Board.

Accounting standards also specify much of the content of financial statements, but

they do not provide a comprehensive set of rules.

2.6 The purpose of accounting standards

As stated earlier, national accounting standards are issued in some countries by a

national standard-setting body. International accounting standards (now called

International Financial Reporting Standards or IFRSs) are issued by the

International Accounting Standards Board (IASB).

The stated objectives of the IASB include the aim of developing a single set of global

accounting standards that:

are of a high quality, understandable and enforceable, and

Chapter 5: History and role of accounting in business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 177

will require high quality, transparent and comparable information in financial

statements.

In other words, the IASB aims to achieve consistency and comparability in financial

reporting, throughout the world, through the adoption of its IFRSs by every

country.

IFRSs can be made enforceable by national law. As mentioned earlier, the

requirement for stock market companies to use IFRSs to produce financial

statements is already included in company law throughout the European Union.

IFRSs deal with a range of different matters:

Some IFRSs require the inclusion of an additional financial statement in the

report and accounts. For example, one IFRS requires business entities to include

a cash flow statement in their annual accounts.

Some IFRSs deal with the accounting treatment of specific issues, such as

accounting for leases, asset impairment and reporting earnings per share.

Many IFRSs specify additional information that should be provided in notes to

the financial statements.

Enforcement of IFRSs

The International Accounting Standards Board does not have any powers to enforce

its accounting standards.

Enforcement comes through the adoption by national governments of IFRSs for

company reporting, and the enforcement of national regulations by the national

authorities.

2.7 Stock market regulations

Companies whose shares are traded on a stock market must comply with certain

regulations. These regulations might be issued by the governing body responsible

for supervision of the financial markets in that particular country. In the UK for

example, stock market regulations are issued by the Financial Services Authority

which is the government body responsible for supervision of the financial markets

in the UK.

Most stock market regulations do not concern accounting and financial reporting.

However, some regulations might include a requirement for stock market

companies to include specific items of information in their published financial

accounts. Regulations might also specify the maximum period of time within which

a company must prepare its annual report and accounts after the end of its financial

year.

Paper F1: Accountant in business

178 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The main financial systems in business

Business systems and financial systems

Accounting for purchases

Sales invoicing system

Payroll system

Credit control system

Cash and working capital management

Controls for business and IT systems

3 The main financial systems in business

3.1 Business systems and financial systems

Every business organisation has operational systems for achieving its purposes and

applying its policies. The main operational systems make up the value chain, and

include purchasing, manufacturing or service provision, and marketing and sales.

These business activities are supported by administrative systems, such as human

relations management systems (‘personnel management’) and accounting systems.

This section provides a brief description of the main financial/accounting systems.

3.2 Accounting for purchases

In large business organisations, there is a specialist buying department with

responsibility for purchasing supplies (raw materials, components, office supplies

and other items) from external suppliers.

A typical purchase transaction (in a large organisation) goes through the following

stages.

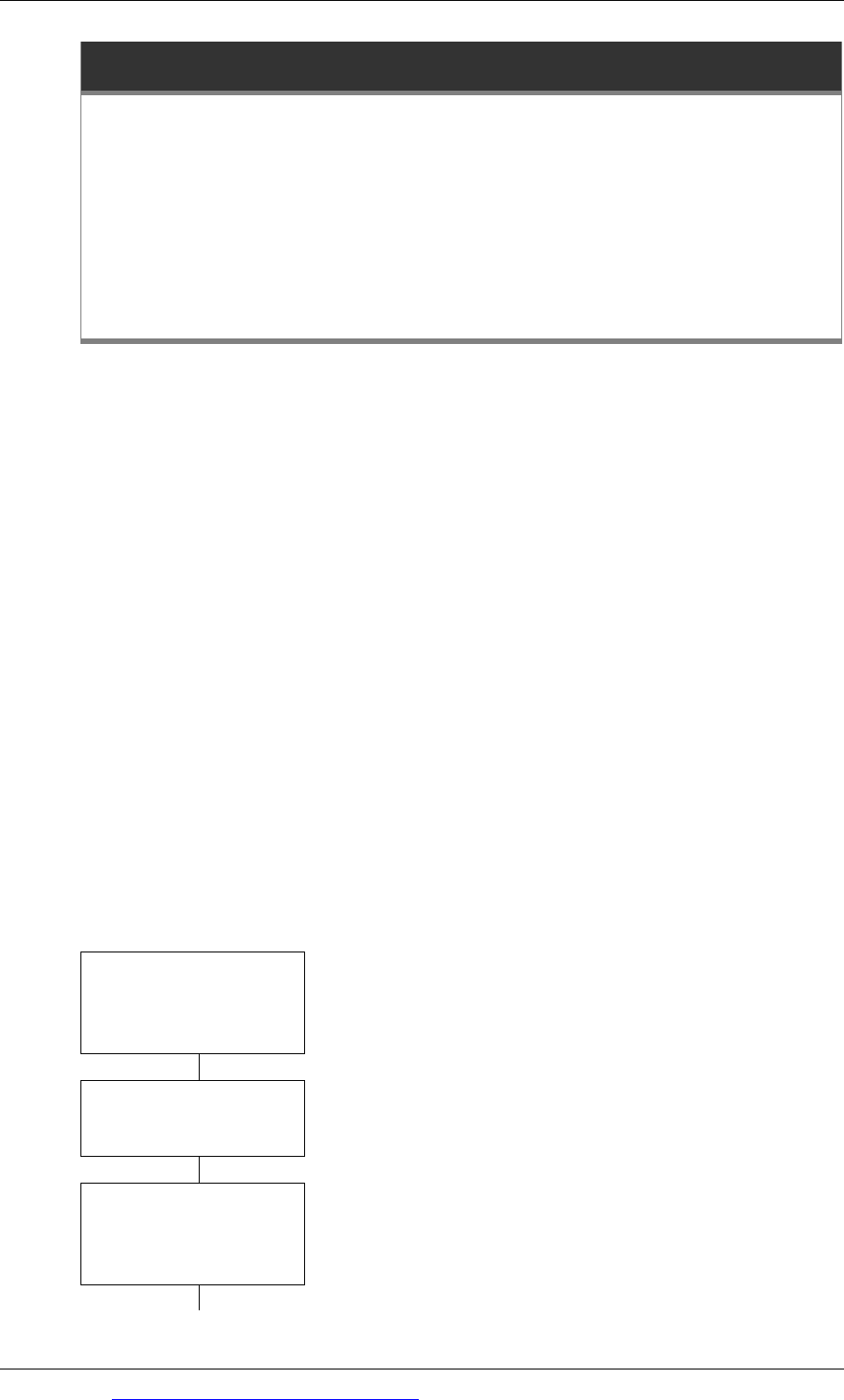

Purchase requisition

A request (properly authorised) is sent to the

buying department, asking it to purchase a

quantity of a particular item. The requisition might

come from the manager of the stores department.

Purchase order

The buyer places an order with a supplier,

probably after checking prices and delivery terms

with a number of different suppliers.

Delivery note

The supplier delivers the goods. The person

making the delivery provides a delivery note, as

evidence that the goods have been delivered. This

is signed by the person receiving the goods.

Chapter 5: History and role of accounting in business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 179

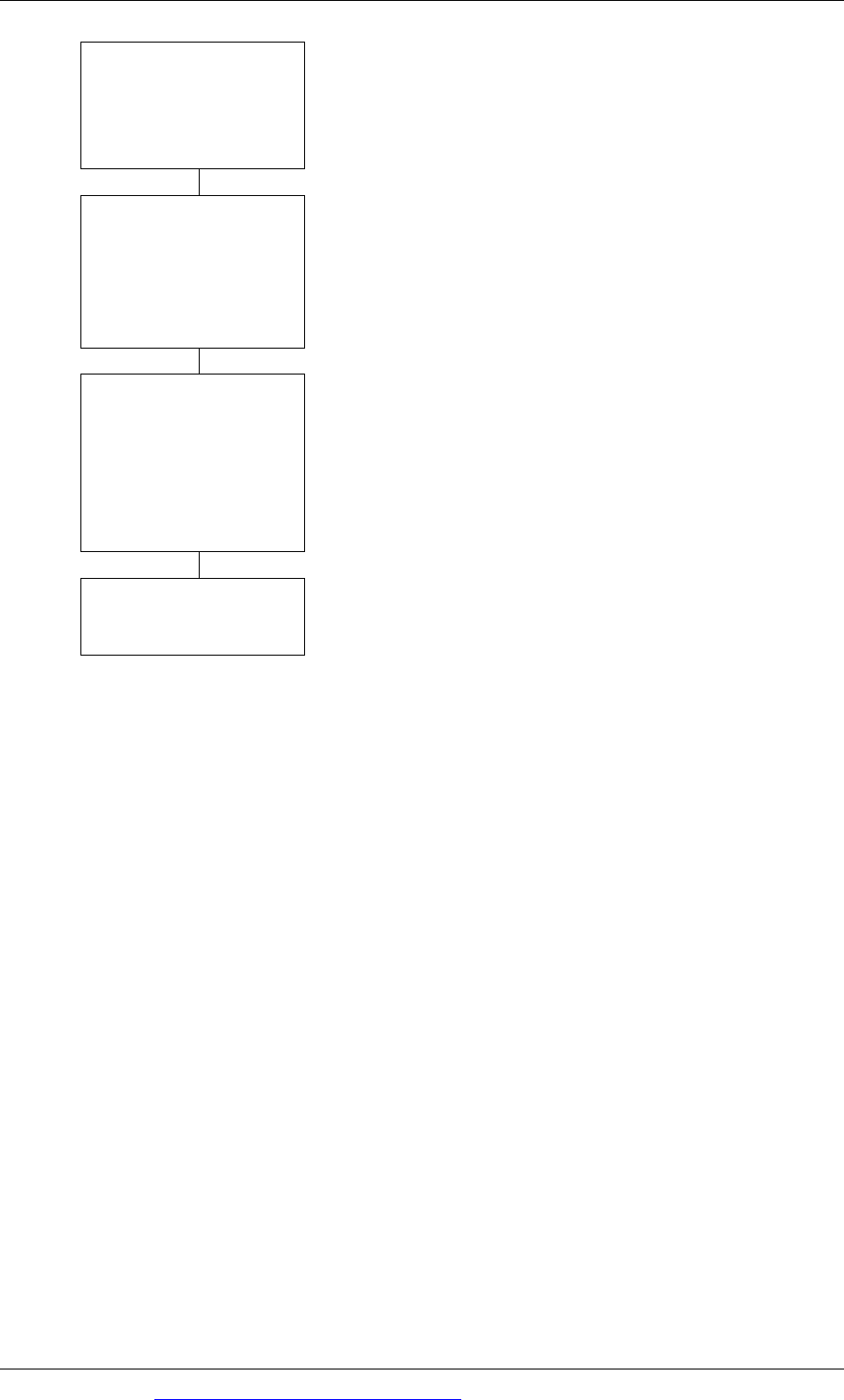

Goods received note

The delivery note is used to prepare an internal

document, called a goods received note (GRN).

This includes details of the goods received,

including the inventory code for the item. A copy

of the GRN is sent to the accounts department.

Purchase invoice

An invoice is received from the supplier. Suppliers

normally give customers a specified length of time

for making the payment (the ‘credit period’). The

supplier’s invoice, called the purchase invoice,

specifies the goods supplied, their cost and the date

by which payment is required.

Accounting record for

the purchase invoice

The first accounting entry is made for the purchase

transaction. The accountant or book-keeper

matches the purchase invoice with the GRN and a

copy of the purchase order, to make sure that the

details agree. If they do agree, a record is made in

the accounting system for the invoice received (the

amount payable).

Accounting record for

the payment

The invoice is eventually paid (by the accounts

department). A record of the payment must be

entered in the accounting system.

The accounting system also records goods returned to suppliers, for example

because they are faulty. The supplier gives a reduction in price for returned goods,

and acknowledges this in a document called a credit note. Details of credit notes are

also entered in the accounting system.

At any time the accounting system for purchases can provide information about:

the total cost of purchases in a given period of time, such as for the year to date

the amount currently owed to suppliers, both individually and in total.

Inventory records

The purchasing system for accounting might also be linked to a system for

recording inventory (an inventory control system). The inventory control system

records quantities of inventory received and used, and the cost of the inventory. It

also provides a record of the quantity and value of inventory currently held.

The purchases system might be linked to the inventory control system, because

details of goods received can be transferred from the purchases system into the

inventory control system.

3.3 Sales invoicing system

A sales invoicing system is a system for producing invoices and recording sales,

where goods or services are sold to a customer on credit. When goods or services

Paper F1: Accountant in business

180 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

are sold on credit, the customer is allowed a period of time before they have to be

paid for. A sales invoice is sent to the customer, giving details of the items sold, the

amount payable and the date by which payment is due.

A sales invoicing system is used to:

produce sales invoices for sending to customers

recording the amount owed

recording payments received from (credit) customers.

A typical credit sale transaction for the sale of goods goes through the following

stages.

Sales order

A sales order is received from the customer. The

order goes through a credit check. (Credit control

is explained later.) The sales order is processed.

Delivery note

The goods are delivered to the customer, who signs

the delivery note. A copy of the delivery note is

sent to the accounts department.

Sales invoice

A sales invoice is produced from the sales order

and delivery note, and the invoice is sent to the

customer.

Accounting record for

the sales invoice

The first accounting entry is made for the credit

sales transaction. The accountant or book-keeper

records the details of the sales invoice in the

accounting system.

Accounting record for

payment received

When the customer eventually pays, the payment

is sent or notified to the accounts department, and

a record of the payment is made in the accounting

system.

The accounting system also records goods returned by customers, for example

because they are faulty. The amount of the reduction in the amount payable is

recorded in a credit note, which is sent to the customer. A copy of the credit note is

used to record the sales return in the accounting system.

At any time the accounting system for sales invoices can provide information about:

the total value of sales on credit in a given period of time, such as for the year to

date

the amount currently receivable from credit customers, both individually and in

total.

Chapter 5: History and role of accounting in business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 181

3.4 Payroll system

The payroll system is the system for:

Recording the total amount payable in wages and salaries to employees

Calculating the amount deductible from the pay of each employee, for tax and

other items (such as pension contributions)

Providing employees with details of their total wage or salary for the period, the

deductions and the net pay in cash

Issuing instructions for the payment to employees of the money they are owed.

Payment might be in the form of a cheque or even cash; however, it is now

common for wages and salaries to be paid directly into the employee’s bank

account.

Recording details of the wages and salary costs in the accounting system, the

amounts of deductions (for tax and other items) and the amounts paid in cash to

employees.

When some employees are paid weekly wages, the payroll system is operated each

week. There is also a monthly payroll for salaried employees.

The accounting system must record each of the following items, for each employee

individually and for the work force in total:

Gross pay (= total pay) A

Deductions for tax and other items.

Each deduction should be itemised separately

(B)

Net pay (= money paid to the employee) A – B

In order to prepare the payroll, the payroll staff must have the following

information:

a list of every employee, and the department in which he or she works

the annual salary of the employee or hourly rate of pay (for wage earners) and

overtime rate

for hourly-paid workers, the number of hours worked in the week, including

hours worked overtime

details of other payments, such as bonuses

details for making the deductions from gross pay, for tax and other items

details for making the payment of the net wage or salary (for example, bank

account details for each employee).

3.5 Credit control system

A credit control system operates whenever goods or services are sold on credit. The

purpose of a credit control system is to:

make decisions about allowing credit to customers

monitoring the payment record of credit customers

reviewing the amount of credit allowed to existing credit customers

collecting amounts overdue from credit customers.

Paper F1: Accountant in business

182 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Giving credit

When a new customer applies for credit terms, a decision has to be made about

whether to allow the customer credit terms, and if so how much credit should be

allowed. (If you have a credit card, you should be familiar with this process from

the decision of the credit card company about how much credit to allow you when

you were first given the card.)

For example, a company might have standard credit terms of allowing customers 30

days to pay from the date of the sales invoice. It might then agree to allow a new

customer credit on those terms up to, say, €10,000. This is the customer’s authorised

‘credit limit’.

Before deciding whether to allow credit to a new customer, the credit control

department should carry out a credit check on the customer. Typical methods of

obtaining credit information are:

a credit reference from one or two other suppliers to the customer

a credit reference from the customer’s bank

possibly, by paying for a credit status report on the customer from a specialist

credit reference agency

in the case of a corporate customer, by asking for and analysing the company’s

financial statements.

Monitoring payment records and reviewing credit limits

When a customer is given credit, the customer’s payment record should be

monitored regularly, to check whether the customer has paid invoices on time and

has not been allowed to exceed his agreed credit limit.

When a customer has a good credit record, a decision might be taken to raise the

credit limit (or agree to raise the credit limit if the customer makes a request).

Collecting overdue payments

The credit control section might also be responsible for trying to collect overdue

payments from credit customers. These are customers who have not paid an invoice

within the period allowed by the credit terms.

This process involves preparing a list of overdue payments, and contacting the

customer to ask for payment.

If customers continue to refuse to pay, or ignore requests for payment, further

action might be considered, such as legal action to obtain payment or the sale of the

amount receivable to a debt collection agency.

Chapter 5: History and role of accounting in business

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 183

3.6 Cash and working capital management

Cash management

Businesses need cash to operate. If an entity does not have enough cash to make a

payment when the payment is due, it might be forced out of business. (The entity

might be ‘insolvent’ because it is unable to pay the money it owes, and it might be

forced into liquidation by a creditor, through legal process. When a business goes

into liquidation, its existence is brought to an end.)

It is therefore essential to manage cash, to make sure that there is always enough

available for making essential payments. Or if the cash is not available, there should

be an arrangement with a bank to borrow extra money immediately, for example in

the form of a bank overdraft facility.

Some business entities are ‘cash rich’, which means that they have more cash than

they need. A cash surplus might be permanent, in which case management should

decide how the surplus should be used. If a cash surplus is only expected to be

temporary, a decision might be taken to invest it in a short-term investment, such as

a bank deposit account, to earn some interest.

Cash management involves the following activities:

managing the bank account or bank accounts of the business

making cash payments

banking cash receipts

arranging bank overdrafts

investing temporary cash surpluses

making continual forecasts of cash receipts and payments (‘cash budgets’) to

make sure that there should be sufficient cash (or unused bank overdraft facility)

to make essential payments when these are due

monitoring actual cash flows.

Working capital management

There are several definitions of working capital. One definition is that working

capital is the amount of funding that a business entity has to support its day-to-day

operational activities.

A business needs funding for its day-to-day operations for the following reasons.

It needs to buy raw materials and components, and inventories of materials and

components represent goods that have been bought but not yet used.

If it is a manufacturing business, it has work-in-progress. This is inventory of

items that are in the process of production, but have not yet been completed.

Work-in-progress represents materials purchased and other costs incurred, for

goods that have not yet been produced and sold.

If it is a manufacturing business, it also has inventory of finished goods. Finished

goods are items that have been manufactured but have not yet been sold.

Paper F1: Accountant in business

184 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Finished goods represents materials purchased and other costs incurred, for

items that have not yet been sold.

Business entities that sell goods or services on credit have receivables. These are

amount owed by credit customers. Amounts receivable represent items that

have been produced and sold, but for which no money has yet been received.

A business therefore needs funding for all its inventories and receivables. It has

incurred costs in acquiring these assets, but has not yet received payment.

To some extent, inventories and receivables are financed by amounts payable to

suppliers. In other words, credit taken from suppliers helps to fund working capital.

This is why a common definition of working capital is as follows:

Inventories A

Trade receivables (money owed by customers) B

Trade payables (money owed to suppliers (C)

Working capital A + B - C

Working capital ties up cash. Money has to be spent acquiring inventories and on

goods that are sold to credit customers.

The management of working capital mainly involves:

avoiding excessive inventories, for example by speeding up inventory turnover

(using it more quickly)

avoiding excessive trade receivables, for example by making sure that credit

customers pay what they owe on time

making sure that suitable credit terms are negotiated with suppliers.

By managing working capital efficiently, a business will avoid having to invest too

much in inventories and receivables, and this will improve cash flow. There is a

close link between cash management and working capital management for this

reason.

3.7 Controls for business and IT systems

Risks

In any business system – including purchasing, production, service provision, sales,

credit management and cash management systems – there are risks that something

will go wrong.

A risk is the possibility that something that is expected to happen does not actually

happen. In business system, the risks are often on the ‘downside’, which means that

when something unexpected happens, it is usually unwelcome and ‘bad news’.

There are many different types of risk in business operations.