Zhu J. Applications of Fourier Transform to Smile Modeling: Theory and Implementation

Подождите немного. Документ загружается.

68 3 Stochastic Volatility Models

f

1

(

φ

)=E

Q

S(T)

S

0

e

rT

exp(i

φ

lnS(T))

= exp

i

φ

(x

0

+ rT) −

(1+i

φ

)

ρ

σ

(V

0

+

κθ

T)

× E

Q

exp

−

(1+i

φ

)

2

1 −(1 + i

φ

)(1−

ρ

2

) −

2

λρ

σ

T

0

V(t)dt

+

(1+i

φ

)

κρ

σ

T

0

V(t)dt +

(1+i

φ

)

ρ

σ

V(T )

= exp(i

φ

(x

0

+ rT) −s

3

(V

0

+

κθ

T))

× E

Q

exp

−s

1

T

0

V(t)dt −s

2

T

0

V(t)dt + s

3

V(T )

= exp(i

φ

(x

0

+ rT) −s

3

(V

0

+

κθ

T))

× exp

H

6

(T;s

1

,s

2

,s

3

)V

0

+ H

7

(T;s

1

,s

2

,s

3

)

V

0

+ H

8

(T;s

1

,s

2

,s

3

)

= exp(i

φ

(x

0

+ rT)) f

DSR

1

(

φ

) (3.41)

with

f

DSR

1

(

φ

)=exp

−s

3

(V

0

+

κθ

T)+H

6

(T;s

1

,s

2

,s

3

)V

0

+ H

7

(T;s

1

,s

2

,s

3

)

V

0

+ H

8

(T;s

1

,s

2

,s

3

)

, (3.42)

where the parameters s

1

,s

2

and s

3

are defined by

s

1

=

(1+i

φ

)

2

1 −(1 + i

φ

)(1−

ρ

2

) −

2

λρ

σ

,

s

2

= −

(1+i

φ

)

κρ

σ

, s

3

=

(1+i

φ

)

ρ

σ

.

Thus, the whole problem is reduced to computing the expected value in the last

equality, which can be solved by our standard method. The functions H

6

(T), H

7

(T)

and H

8

(T) are given in Appendix B. The explicit form of f

1

(

φ

) has a complex

structure, but is expressed in a closed-form manner with elementary functions.

Similarly, we have

f

2

(

φ

)=E

Q

[exp(i

φ

lnS(T))]

= exp

i

φ

(x

0

+ rT) −

i

φρ

σ

(V

0

+

κθ

T)

× E

Q

exp

−

i

φ

2

1 −i

φ

(1−

ρ

2

) −

2

λρ

σ

T

0

V(t)dt

+

i

φκρ

σ

T

0

V(t)dt +

i

φρ

σ

V(T )

3.4 Double Square Root Model 69

= exp(i

φ

(lnS

0

+ rT) −s

∗

3

(V

0

+

κθ

T))

× E

Q

exp

−s

∗

1

T

0

V(t)dt −s

∗

2

T

0

V(t)dt + s

∗

3

V(T )

= exp(i

φ

(x

0

+ rT) −s

∗

3

(V

0

+

κθ

T))

× exp

H

6

(T;s

∗

1

,s

∗

2

,s

∗

3

)V

0

+ H

7

(T;s

∗

1

,s

∗

2

,s

∗

3

)

V

0

+ H

8

(T;s

∗

1

,s

∗

2

,s

∗

3

)

= exp(i

φ

(x

0

+ rT)) f

DSR

2

(

φ

) (3.43)

with

f

DSR

2

(

φ

)=exp

−s

∗

3

(V

0

+

κθ

T)+H

6

(T;s

∗

1

,s

∗

2

,s

∗

3

)V

0

+ H

7

(T;s

∗

1

,s

∗

2

,s

∗

3

)

V

0

+ H

8

(T;s

∗

1

,s

∗

2

,s

∗

3

)

, (3.44)

where

s

∗

1

=

i

φ

2

1 −i

φ

(1−

ρ

2

) −

2

λρ

σ

,

s

∗

2

= −

i

φκρ

σ

, s

∗

3

=

i

φρ

σ

.

Therefore, the option pricing formula for the model, where stochastic volatilities

follow a double square root process, can be given analogously to the above section,

and share all features and numerical implementation as the Heston model and the

Sch

¨

obel-Zhu model.

3.4.2 Numerical Examples

We discuss this model briefly via some numerical examples. In order to compare

this stochastic volatility model with the Black-Scholes model, we need to calculate

suitable BS benchmark values, as discussed in the previous section. For this purpose

we choose two possible BS prices:

8

The first one called BS

1

is computed according

to the mean level of stochastic volatilities

θ

that is implied by

θ

=

σ

2

/(4

κ

). The

other one denoted by BS

2

is the BS price by choosing the spot volatility as constant

volatility. Each panel below has its own BS

2

as benchmark. Table (3.5)showsthree

data panels based on formulas (3.42) and (3.44) to demonstrate the impact of

ρ

on

option values. We choose

λ

= 1.0 and

κ

= 0.3 which seems to be small compared

with our previous two models.

9

and implies a

θ

being equal to 0.208. All panels in

8

Because the expected average variance with a double square root process can not be given ana-

lytically, we can not calculate a benchmark according to the expected average variance, as with an

Ornstein-Uhlenbeck process in the above subsection. Additionally, due to the restriction

σ

2

= 4

κθ

,

we can not get a good benchmark by letting

σ

→ 0, as done in Stein and Stein (1991).

9

The Longstaff’s (1989) empirical study shows that the values of the parameters

λ

and

κ

in a term

structure model of interest rates indeed are of an order of 10

−2

or 10

−3

respectively.

70 3 Stochastic Volatility Models

Table (3.5) display the similar properties as shown in Table (3.2). Firstly, we find

again that options with different moneyness react to the correlation

ρ

oppositely. For

ITM options, their values decrease with the values of correlation. And OTM options

display a wholly opposite relation with the correlation

ρ

to ITM options. Secondly,

the finding in Subsection 3.3.3 that the bias between the long term mean

θ

and the

spot volatility is important for the prices of options is confirmed. In Panel K we have

θ

= 0.208 and spot volatility as

√

0.04 = 0.2, then option prices in this panel are

overall near these two BS benchmarks regardless of moneyness and correlation. In

contrast to Panel K, the panels L and M are calculated with a spot volatility of 0.1

and 0.3 respectively. Consequently, the option prices in these panels deviate from

BS

1

and BS

2

significantly. Finally, as reported in Subsection 3.3.3, options with

different moneyness present different sensitivity to the correlation

ρ

. While OTM

options are generally sensitive to correlation, ITM options do not change remarkably

with

ρ

. Not surprisingly, we can calibrate the implied volatilities from the data with

the negative correlation in Table (3.5) to capture the empirical volatility smile and

sneer pattern.

Table (3.6) shows the impact of

κ

on option prices. Panel N gives all BS

1

values

since every

κ

corresponds to a

θ

, and each BS

1

is then the benchmark for the option

prices in the corresponding position in the panels O, P and Q. In the case of

κ

= 0.1,

θ

has an extraordinary high value of 0.625 and leads to unsuitable benchmarks. One

obvious finding is that the option price is a decreasing function of

κ

regardless of the

moneyness of options. This phenomenon can be explained as follows: For a fixed

σ

,

the values of the explicit

θ

=

σ

2

/(4

κ

) go up with the falling values of

κ

, and im-

ply a larger mean level of the weighted sum

κ

V(t)+

λ

v(t). Hence, option prices

increase correspondingly. A comparison of panels O, P and Q shows that the true

values of options result from a trade-off between long-term mean and spot volatil-

ity. By its very nature, the BS model can not reflect the dynamic effect of varying

volatilities on the option prices. Based on the above observations most of which are

identical to the models of square root process and Ornstein-Uhlenbeck process, we

conclude that modeling stochastic volatility with a double square root process also

constitutes a promising way in improving the pricing and hedging performance in

practice.

3.5 Other Stochastic Volatility Models

In above sections, we have addressed three stochastic volatility models that admit

analytical CFs under different measures, and therefore also analytical pricing for-

mulas in form of the Fourier inversion. There are some extensions of these three

stochastic volatility models. For example, N

¨

ogel and Mikhailov (2003) considered

the Heston model with time-dependent parameters by iteratively solving the valua-

tion PDEs at discrete time points. Popovici (2003) extended the Sch

¨

obel-Zhu model

by introducing a time-deterministic function for mean level

θ

, and the new process

for stochastic volatility reads

3.5 Other Stochastic Volatility Models 71

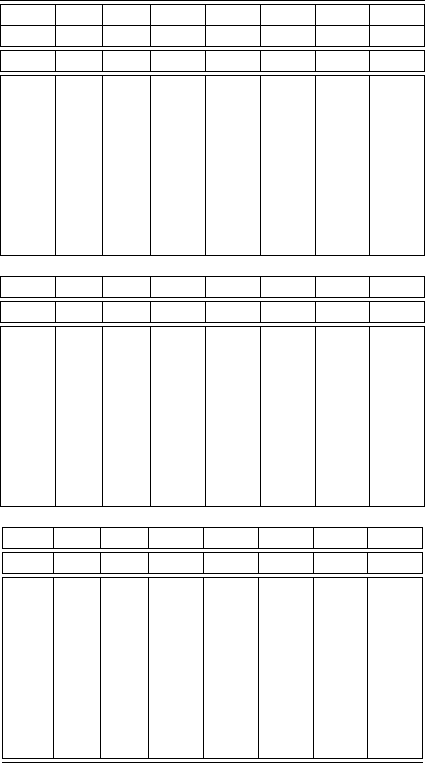

ρ

K

90 95 100 105 110 115 120

BS

1

(

θ

) 15.241 11.518 8.358 5.817 3.885 2.492 1.539

BS

2

(V ) 15.118 11.342 8.142 5.584 3.658 2.293 1.377

-1.00 15.563 11.529 7.811 4.539 1.928 0.359 0.003

-0.75 15.435 11.407 7.753 4.646 2.305 0.891 0.274

-0.50 15.296 11.276 7.688 4.727 2.576 1.265 0.588

-0.25 15.144 11.128 7.605 4.786 2.789 1.569 0.873

0.00 14.977 10.956 7.501 4.826 2.987 1.831 1.132

0.25 14.791 10.753 7.371 4.848 3.150 2.062 1.371

0.50 14.582 10.505 7.206 4.853 3.292 2.271 1.595

0.75 14.353 10.184 6.993 4.839 3.420 2.465 1.806

1.00 14.188 9.681 6.681 4.813 3.546 2.655 2.013

K: V

0

= 0.04,

λ

= 1.0,

κ

= 0.3,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

ρ

K

90 95 100 105 110 115 120

BS

2

(V ) 14.223 9.668 5.684 2.765 1.081 0.3335 0.083

-1.00 14.814 10.524 6.498 3.018 0.612 0.008 0.00

-0.75 14.736 10.417 6.449 3.131 0.972 0.188 0.034

-0.50 14.647 10.314 6.378 3.197 1.228 0.411 0.141

-0.25 14.555 10.200 6.289 3.241 1.431 0.614 0.275

0.00 14.460 10.070 6.179 3.269 1.600 0.797 0.416

0.25 14.364 9.924 6.042 3.280 1.743 0.963 0.557

0.50 14.274 9.757 5.870 3.273 1.866 1.115 0.694

0.75 14.207 9.572 5.643 3.247 1.971 1.255 0.828

1.00 14.188 9.421 5.298 3.190 2.065 1.388 0.959

L: V

0

= 0.01,

λ

= 1.0,

κ

= 0.3,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

ρ

K

90 95 100 105 110 115 120

BS

2

(v) 16.887 13.615 10.784 8.395 6.629 4.848 3.604

-1.00 16.784 13.082 9.701 6.704 4.159 2.147 0.772

-0.75 16.631 12.957 9.646 6.773 4.415 2.624 1.403

-0.50 16.465 12.824 9.591 6.846 4.644 2.997 1.853

-0.25 16.283 12.677 9.528 6.909 4.848 3.316 2.229

0.00 16.078 12.510 9.452 6.962 5.032 3.598 2.561

0.25 15.841 12.315 9.360 7.004 5.201 3.855 2.864

0.50 15.559 12.083 9.249 7.039 5.358 4.094 2.145

0.75 15.202 11.794 9.117 7.068 5.511 4.323 3.413

1.00 14.646 11.410 8.977 7.111 5.671 4.550 3.673

M: V

0

= 0.09,

λ

= 1.0,

κ

= 0.3,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

BS

2

values are calculated according to V

0

= 0.04.

V is the squared volatility.

Table 3.5 The impact of the correlation

ρ

on option prices. The prices of ITM calls (OTM calls)

decrease (increase) with increasing correlations

ρ

.

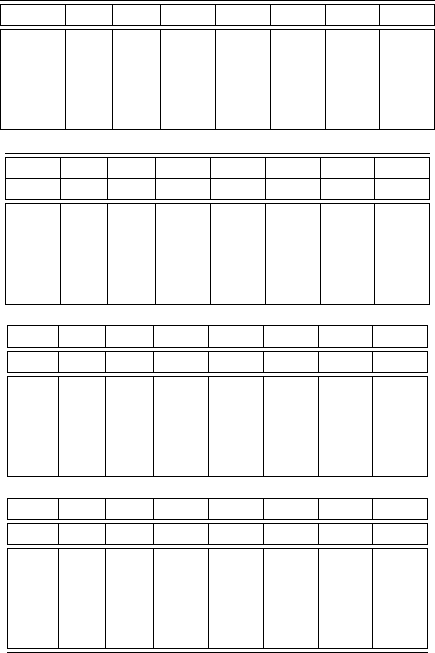

72 3 Stochastic Volatility Models

κ

K

90 95 100 105 110 115 120

θ

=0.125 14.327 9.976 6.258 3.470 1.683 0.711 0.262

θ

=0.156 14.573 10.480 7.017 4.344 2.479 1.304 0.633

θ

=0.208 15.237 11.511 8.350 5.809 3.877 2.485 1.533

θ

=0.313 17.150 13.928 11.131 8.760 6.794 5.197 3.925

θ

=0.625 24.288 21.784 19.506 17.441 15.577 13.898 12.389

N: BS

1

(

θ

) are calculated according to

θ

=

σ

2

/(4

κ

).

κ

K

90 95 100 105 110 115 120

BS

2

(V ) 14.223 9.668 5.684 2.765 1.081 0.335 0.083

0.5 14.508 10.129 6.199 3.150 1.359 0.565 0.245

0.4 14.526 10.155 6.231 3.180 1.381 0.580 0.254

0.3 14.555 10.200 6.289 3.241 1.431 0.614 0.275

0.2 14.595 10.262 6.373 3.333 1.508 0.668 0.309

0.1 14.647 10.341 6.481 3.453 1.612 0.741 0.356

O: V

0

= 0.01,

λ

= 1.0,

ρ

= −0.25,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

κ

K

90 95 100 105 110 115 120

BS

2

(v) 15.118 11.342 8.142 5.584 3.658 2.293 1.377

0.5 14.959 10.868 7.281 4.435 2.475 1.310 0.684

0.4 15.046 10.991 7.434 4.600 2.626 1.430 0.771

0.3 15.144 11.128 7.605 4.786 2.798 1.569 0.873

0.2 15.254 11.280 7.794 4.991 2.991 1.727 0.990

0.1 15.374 11.455 7.999 5.214 3.202 1.902 1.123

P: V

0

= 0.04,

λ

= 1.0,

ρ

= −0.25,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

κ

K

90 95 100 105 110 115 120

BS

2

(v) 16.889 13.615 10.784 8.395 6.629 4.848 3.604

0.5 15.977 12.292 9.080 6.431 4.381 2.893 1.874

0.4 16.125 12.479 9.298 6.664 4.608 3.097 2.043

0.3 16.283 12.677 9.528 6.909 4.848 3.316 2.229

0.2 16.450 12.885 9.768 7.165 5.101 3.547 2.428

0.1 16.625 13.102 10.018 7.432 5.365 3.791 2.639

Q: V

0

= 0.09,

λ

= 1.0,

ρ

= −0.25,

σ

= 0.5,T = 0.5, S = 100, r = 0.0953

BS

2

values are calculated according to spot volatility,

V is the squared volatility.

Table 3.6 The impact of the velocity parameter

κ

on options prices. For the given model

parameters, option prices increase with decreasing velocity parameters

κ

.

dv(t)=

κ

[

θ

1

+(

θ

−

θ

1

)e

−

β

t

]dt +

σ

dW

2

(t).

An analytical CF under the risk-neutral measure for this extended stochastic volatil-

ity model can be derived, as shown by Popovici. In the setting of affine jump-

diffusion state processes, Duffie, Pan and Singleton (1999) set up a stochastic

volatility model where the volatilities are driven by multiple mean-reverting square

root processes, this model is essentially a multi-dimensional Heston model. Gen-

erally, extending a one-dimensional stochastic model to an uncorrelated multi-

dimensional case is a straightforward task by applying the Fourier transform. For

a more detailed discussion on stochastic volatility, please refer to Lewis (2000),

Fouque, Papanicolaou and Sircar (2000), Shephard (2005), and Gatheral (2006).

3.6 Appendices 73

3.6 Appendices

A: Derivation of the CFs with Ornstein-Uhlenbeck Process

The CF f

1

(

φ

) can be calculated as follows:

f

1

(

φ

)=E[exp(−rT −x

0

+(1 + i

φ

)x(T))]

= Eexp(−(rT + x

0

)

+(1 +i

φ

)

x

0

+

T

0

rdt −

1

2

T

0

v

2

(t)dt +

T

0

v(t)dW

1

= exp(i

φ

(rT + x

0

))

× E

exp

(1+i

φ

)

−

1

2

T

0

v

2

(t)dt +

T

0

v(t)dW

1

= exp(i

φ

(rT + x

0

))Eexp((1 + i

φ

)

×

−

1

2

T

0

v

2

(t)dt +

ρ

T

0

v(t)dW

2

+

1 −

ρ

2

T

0

v(t)dW

.

Note that dW s uncorrelated with dW

2

,wehave

f

1

(

φ

)=exp(i

φ

(rT + x

0

))

× E

exp

(1+i

φ

)

−

1

2

T

0

v

2

(t)dt +

ρ

T

0

v(t)dW

2

× exp

1

2

(1+i

φ

)

2

(1−

ρ

2

)

T

0

v

2

(t)dt

= exp(i

φ

(rT + x

0

))

× E

exp

1

2

(1+i

φ

)(i

φ

−

ρ

2

−i

φρ

2

)

T

0

v

2

(t)dt

+(1 +i

φ

)

ρ

T

0

v(t)dW

2

.

Now we replace

T

0

v(t)dW

2

by

v

2

(T)

2

σ

−

v

0

2

σ

−

σ

2

T −

κθ

σ

T

0

v(t)dt +

κ

σ

T

0

v

2

(t)dt

and yield

74 3 Stochastic Volatility Models

f

1

(

φ

)=exp(i

φ

(rT + lnS

0

))

× E

exp

1

2

(1+i

φ

)(i

φ

−

ρ

2

−i

φρ

2

)

T

0

v

2

(t)dt

+(1 + i

φ

)

ρ

v

2

(T)

2

σ

−

v

0

2

σ

−

σ

2

T

−

κθ

σ

T

0

v(t)dt +

κ

σ

T

0

v

2

(t)dt

.

It follows by further calculation,

f

1

(

φ

)=exp(i

φ

(rT + x

0

))

× E

exp

[

1

2

(1+i

φ

)(i

φ

−

ρ

2

−i

φρ

2

+

2

ρκ

σ

]

T

0

v

2

(t)dt

= −

ρκθ

σ

(1+i

φ

)

T

0

v(t)dt +

ρ

2

σ

(1+i

φ

)v

2

(T)

−

ρ

2

σ

(1+i

φ

)v

0

−

ρσ

T

2

(1+i

φ

)

= exp

i

φ

(rT + lnS

0

) −

ρ

2

σ

(1+i

φ

)v

0

−

ρσ

T

2

(1+i

φ

)

× E

exp

−s

1

T

0

v

2

(t)dt −s

2

T

0

v(t)dt + s

3

v

2

(T)

.

The expansion of f

2

(x) follows the same way. What we need to do is to calculate

the expected value

y(v

0

,T)=E

exp

−s

1

T

0

v

2

(t)dt −s

2

T

0

v(t)dt + s

3

v

2

(T)

= E

exp

T

0

(−s

1

v

2

(t) −s

2

v(t))dt

exp(s

3

v

2

(T))

for arbitrary complex numbers s

1

,s

2

and s

3

. and s

1

v

2

(t)+s

2

v(t) is lower bounded.

According to the Feynman-Kac formula, y satisfies the following differential equa-

tion

∂

y

∂τ

= −(s

1

v

2

+ s

2

v)y +

κ

(

θ

−v)

∂

y

∂

v

+

1

2

σ

2

∂

2

y

∂

v

2

with the boundary condition

y(v

0

,0)=exp(s

3

v

2

0

).

It can be shown that the above differential equation always has a solution of the

form

3.6 Appendices 75

y(v

0

,

τ

)=exp

1

2

D(

τ

)v

2

0

+ H

4

(

τ

)v

0

+ H

6

(

τ

)+s

3

v

2

0

= exp

1

2

(

D(

τ

)+2s

3

)v

2

0

+ H

4

(

τ

)v

0

+ H

5

(

τ

)

= exp

1

2

H

3

(

τ

)v

2

0

+ H

4

(

τ

)v

0

+ H

5

(

τ

)

with H

3

(

τ

)=

D(

τ

)+2s

3

. Substituting this into the differential equation, we can

obtain three differential equations that determine H

3

(

τ

), H

4

(

τ

) and H

5

(

τ

) :

1

2

(H

3

)

τ

= −s

1

−

κ

H

3

+

1

2

σ

2

H

2

3

,

(H

4

)

τ

= −s

2

+

κθ

H

3

−

κ

H

4

+

σ

2

H

4

H

3

,

(H

5

)

τ

=

κθ

H

4

+

1

2

σ

2

H

2

4

+

1

2

σ

2

H

3

,

where H

3

(0)=2s

3

,H

4

(0)=0 and H

5

(0)=0. Solving these equations is straight-

forward but tedious.

H

3

(

τ

)=

κ

σ

2

−

γ

1

σ

2

sinh(

γ

1

τ

)+

γ

2

cosh(

γ

1

τ

)

γ

4

,

H

4

(

τ

)=

(

κθγ

1

−

γ

2

γ

3

)(1−cosh(

γ

1

τ

)) −(

κθγ

1

γ

2

−

γ

3

)sinh(

γ

1

τ

)

γ

1

γ

4

σ

2

,

H

5

(

τ

)=−

1

2

ln

γ

4

+

[(

κθγ

1

−

γ

2

γ

3

)

2

−

γ

2

3

(1−

γ

2

2

)]sinh(

γ

1

τ

)

2

γ

3

1

γ

4

σ

2

+

(

κθγ

1

−

γ

2

γ

3

)

γ

3

(

γ

4

−1)

γ

3

1

σ

2

γ

4

+

τ

2

γ

2

1

σ

2

[

κγ

2

1

(

σ

2

−

κθ

2

)+

γ

2

3

]

with

γ

1

=

2

σ

2

s

1

+

κ

2

,

γ

3

=

κ

2

θ

−s

2

σ

2

,

γ

2

=

κ

−2

σ

2

s

3

γ

1

,

γ

4

= cosh(

γ

1

τ

)+

γ

2

sinh(

γ

1

τ

).

B: Derivation of the CFs with Double Square Root Process

Here we do the same thing as in Appendix A. Let y be the related expectation value,

namely

76 3 Stochastic Volatility Models

y(V

0

,T)=E

exp

−s

1

T

0

V(t)dt −s

2

T

0

V(t)dt + s

3

V(T )

,

we have the following PDE by applying the Feynman-Kac formula

∂

y

∂τ

= −(s

1

V + s

2

√

V)y +(

κθ

−

κ

√

V −

λ

V)

∂

y

∂

V

+

1

2

σ

2

V

∂

2

y

∂

V

2

where

τ

denotes time to maturity. The boundary condition is

y(v

0

,0)=exp(s

3

V

0

).

For 4

κθ

=

σ

2

, we think of a solution which takes the form of

y(v

0

,

τ

)=exp(H

6

(

τ

)v

0

+ H

7

(

τ

)

V

0

+ H

8

(

τ

))

with H

6

(0)=s

3

V

0

. Setting the corresponding derivatives into the above PDE, we

obtain a system of ordinary differential equations:

(H

6

)

τ

= −s

1

−

λ

H

6

+

1

2

σ

2

H

2

6

,

(H

7

)

τ

= −s

2

−

κ

H

6

−

1

2

λ

H

7

+

1

2

σ

2

H

6

H

7

,

(H

8

)

τ

=

1

4

σ

2

H

6

−

1

2

κ

H

7

+

1

8

σ

2

H

2

7

.

This leads to the following solutions:

H

6

(

τ

)=

λ

σ

2

−

2

γ

1

σ

2

2

γ

1

sinh(

γ

1

τ

)+

γ

2

cosh(

γ

1

τ

)

2

γ

1

cosh(

γ

1

τ

)+

γ

2

sinh(

γ

1

τ

)

,

H

7

(

τ

)=

2sinh(

1

2

γ

1

τ

)

γ

1

γ

4

σ

2

×

(

κγ

2

−2

γ

3

)cosh(

1

2

γ

1

τ

)+(2

κγ

1

−

γ

2

γ

3

/

γ

1

)sinh(

1

2

γ

1

τ

)

,

H

8

(

τ

)=−

1

2

ln

γ

4

+

1

4

λτ

+

τ

(

γ

2

3

−

κ

2

γ

2

1

)

2

γ

2

1

σ

2

+

(

γ

2

γ

3

−2

κγ

2

1

)

γ

3

2

γ

4

1

σ

2

(

1

γ

4

−1)

+

sinh(

γ

1

τ

)(

κ

2

γ

2

1

−

κγ

2

γ

3

−

γ

2

3

+ 0.5(

γ

2

γ

3

/

γ

1

)

2

)

2

γ

3

1

σ

2

γ

4

,

where

γ

1

=

1

2

λ

2

+ 2

σ

2

s

1

,

γ

2

=

λ

−

σ

2

s

3

,

γ

3

=

1

2

(

λκ

+

σ

2

s

2

),

γ

4

= cosh(

γ

1

τ

)+

γ

2

2

γ

1

sinh(

γ

1

τ

).

Chapter 4

Numerical Issues of Stochastic Volatility Models

In this chapter we address various numerical issues associated with stochastic

volatility models. The sophisticated numerical implementation of stochastic volatil-

ity models is crucial for a sound performance of the pricing engine and the model

calibration, and includes some different aspects: the numerical integration of (in-

verse) Fourier transform, the computation of functions of complex number, espe-

cially the logarithm of complex number, the calculation of Greeks as well as the

simulation of stochastic volatility process. Each of these issues has been already

extensively discussed in financial literature. Here we present a comprehensive and

compact treatment of these numerical issues from the point of view of practitioners.

The discussion on the efficient simulations of stochastic volatility models is left in

the next chapter.

Firstly we give some alternative pricing formulas for European-style options with

CFs, which may be used to improve the efficiency and accuracy of the numeri-

cal integration of inverse Fourier transform in different pricing contexts. In Section

4.2, we discuss risk sensitivities in stochastic volatility models where Vega risk in

the Black-Scholes model is translated into the parameter risks of stochastic volatil-

ity models. Some special risk sensitivities associated with stochastic volatility are

proposed and discussed. In Sections 4.3 and 4.4, we examine two methods for the

numerical integration of inverse Fourier transform in the option pricing formula,

namely direct integration and FFT (Fast Fourier Transform). It will be shown in

Section 4.5 that a sophisticated direct integration method, for instance, with the

Gaussian integration and strike vector computation, may dominate the FFT in terms

not only of efficiency but also of accuracy. Right computing the logarithm of com-

plex number is another numerical problem, and will be discussed in Section 4.6.

The issue with the logarithm of complex number is somehow underestimated in fi-

nancial literature, but is very important for a correct implementation of the option

pricing formula with CFs. We explain the phenomenon of the discontinuousness

of the logarithms of complex number. Three algorithms are given for a sound treat-

ment of this problem in the context of option valuation. The calibration of stochastic

volatility models is of great importance with respect to their practical applications,

and also extensively discussed in a large number of empirical studies. Some simple

J. Zhu, Applications of Fourier Transform to Smile Modeling, Springer Finance,

DOI 10.1007/978-3-642-01808-4

4,

c

Springer-Verlag Berlin Heidelberg 2000, 2010

77