Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

The 2010 version of the form has not been issued as we go to press.

Section 5.6

Miscellaneous Deductions 5-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

5-22 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 5.7

PHASE-OUT OF ITEMIZED DEDUCTIONS

& EXEMPTIONS FOR HIGH-INCOME TAXPAYERS

Please note: The following section does not apply to the 2010 tax year. The discus-

sion is included in the text because the phase-outs have been part of the tax calcu-

lation for prior years and are expected to return as part of the law for 2011 and

future tax years.

The following sec tion covers the complex calculation of the itemized deduction

and exemption phase-outs for high-inco me individuals as it applied to 2009 tax

returns. Almost all commercial tax software preparation programs calculate the

phase-outs automatically, so few tax preparers actually calculate these by hand.

However, this section will be useful for students wishing to understand how the

phase-outs work and for anyone preparing high-income tax returns by hand.

Limitation on Total Itemized Deductions

In 2009, an individual taxpayer whose adjusted gross income exceeds a threshold amount

must reduce the amount of his or her total itemi zed deductions by 1 percent of the excess

of adjusted gross income over the threshold amount. The threshold amount for 2009 is

$166,800 ($83,400 for married, filing separately). The reduction in the itemized ded u c -

tions is limited to 26

2

/

3

percent of itemized deductions other than the deductions for med-

ical expenses, investment interest expense, casualty and theft losses, and wagering losses

to the extent of wagering gains. Thus, medical expenses, investment interest expense,

casualty and theft losses, and wagering losses are not subject to the o verall limitation.

EXAMPLE Francis and Marcia are married taxpayers who file a joint income tax

return for 2009. In 2009, they have adjusted gross income of $186,850

and itemized deductions of $20,000. The itemized deductions are

from charitable contributi ons and state income taxes. Only $19,799

($20,000 $201) of the itemized deductions are allowed in calculat-

ing taxable income. The reduction in the amount of itemized deduc-

tions claimed by Francis and Marcia is calculated as follows:

Lesser of:

$201 ¼ 1% ($186,850 $166,800), or

$5,333 ¼ 26

2

=

3

% $20,000 N

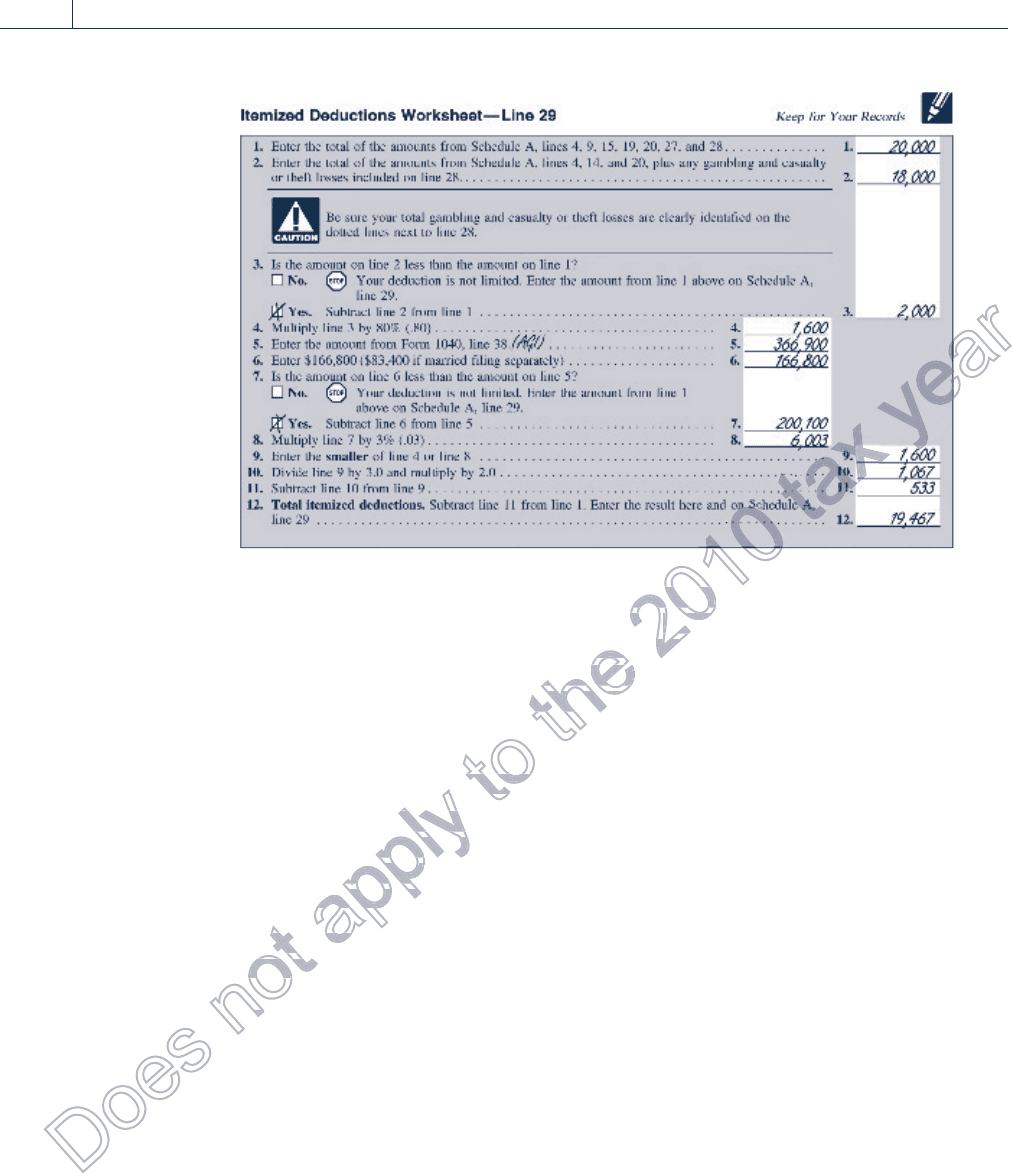

EXAMPLE Use the same facts as in the preceding example, but assume that

gross income is $366,900, and the itemized deductions consist of

$18,000 in casualty losses (after the $500 floor and after applying the

10 percent of adjusted gross income limitation) and $2,000 in state

income taxes. In 2009, Francis and Marcia may deduct only $19,467

($20,000 $533) of itemized deductions. The reduction in the other-

wise allowable itemized deduction amount is equal to the lesser of

$2,001 (1% [$366,900 $166,800]) or $533 (26

2

/

3

% $2,000). The

reduction in the amount of itemized deductions may also be calcu-

lated using the Itemized Deductions Worksheet provided in the

Form 1040 Instructions, as shown on the next page. N

Personal and Dependency Exemptions

Taxpayers are allowed two types of exemptions: personal and dependency as covered

in Chapter 1. For 2009, each exemption reduces adjusted gross income by $3,650.

Section 5.7

Phase-out of Itemized Deductions & Exemptions for High-Income Taxpayers 5-23

D

o

e

1

e

s

$

s

grogro

$18$18

s

$1

s

8

s

gro

gro

$18

n

e the se the s

ii

n

the

n

e the s

in

o

o

$5,$5,

o

$5

o

3

o

5

$5,3

$5

t

5,33

t

$20$20

333333

t

01

3

t

$2

t

20

$20

333

a

a

1%1%

a

1%

a

%

a

¼

1%

1%

p

FrancFranc

p

is

p

ranc

p

Franci

ranc

p

The reThe re

is anis an

p

ed

and

p

he r

h

p

e

The re

is an

he r

sa

l

iteite

eded

e ite

edu

y

emi

uc

y

nsns

emizemiz

ctct

y

sa

zed

tio

y

ons

mi

ons

temize

ct

t

0,

nd

t

0,00,0

dsds

t

00

t

20

t

ha

h

20,0

dst

o

o

ve adve ad

00. T00. T

o

ea

00

o

Th

o

av

0

o

ve ad

000. T

ead

00 T

t

yer

ust

t

yers wyers w

t

ers

t

t

yers w

t

h

subjecsubjec

ww

h

j

wh

h

subje

subjec

w

e

nvesnves

ct toct to

e

to

e

t

e

ec

e

t

nve

inves

ct to

nve

tt

2

thethe

ses, anses, an

enen

2

the

sses,

m

2

d

an

2

h

the

ses, and

men

0

nd

0

the itthe it

deducdeduc

dd

0

he

dedu

0

ct

0

nt

d

0

he

the it

deduc

d

the i

deduc

1

u

temi

1

ounoun

temiztemiz

1

mo

oun

temiz

0

d

0

of theof the

tfor2tfor2

0

of th

for

0

20

0

t

0

old

of the

tfor2

of th

for

t

m

xce

t

momo

t

mou

t

m

t

amou

xce

a

a

untunt

a

ou

a

nt

a

a

ount

nt

x

y

e

a

r

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The exemption deducti on may be reduced, but not to less than two-thirds of the $3,650

exemption amount, or $2,433, for high-income taxpayers. If a taxpayer’s adjusted gross

income (AGI) exceeds a certain threshold amount, the exemption deduction is reduced

by one-third of 2 percent for each $2,500 ($1,250 for married taxpayers filing separately)

or fraction thereof by which the taxpayer’s AGI exceeds the threshold amount. The thresh-

old amounts for 2009 are:

Filing Status Threshold Amount

Single $166,800

Married, filing jointly 250,200

Married, filing separately 125,100

Head of household 208,500

The maximum reduction in the exemption deduction is $1,217 per exemption (or one-

third of $3,650).

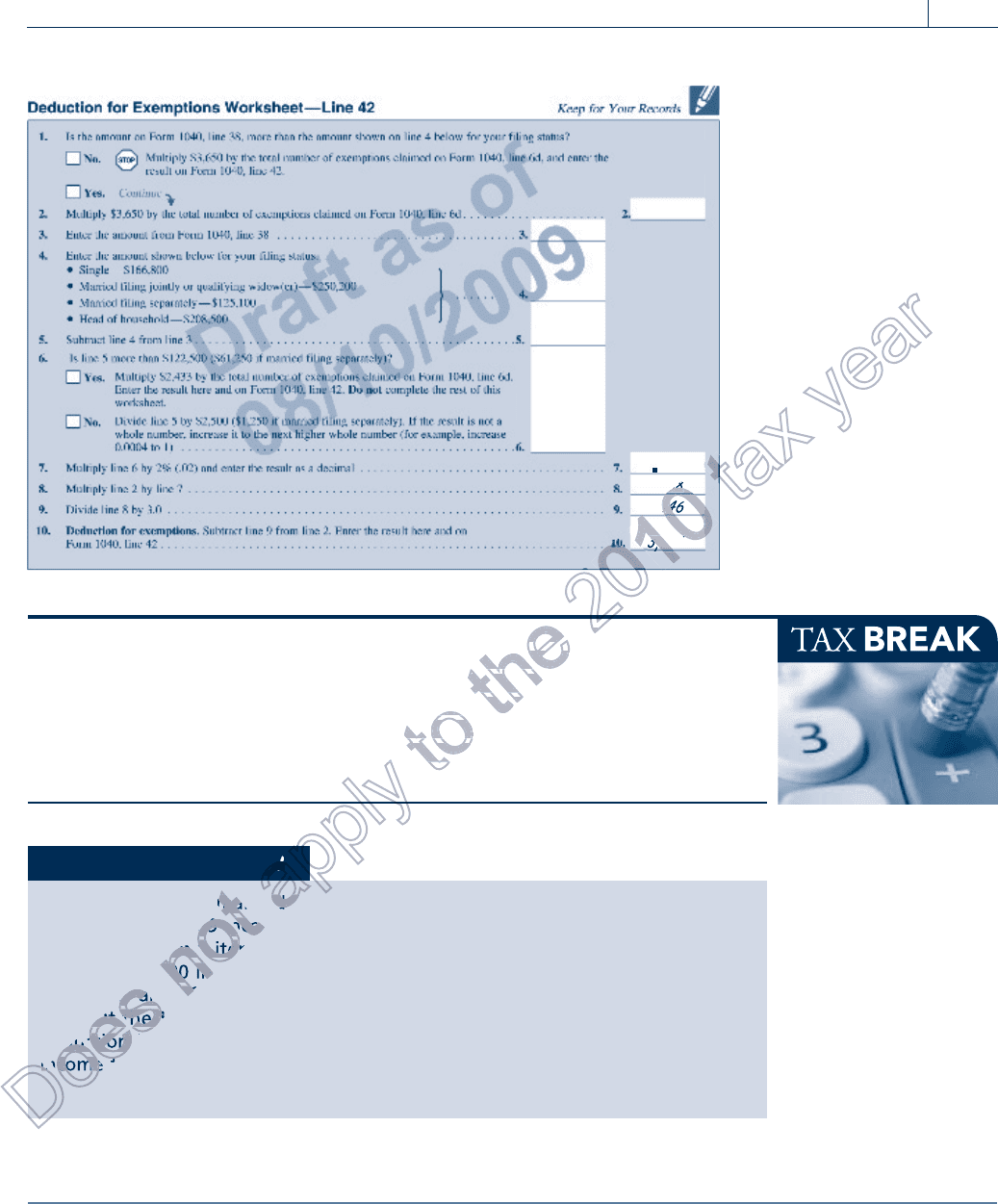

EXAMPLE In 2009, Heather is a single taxpayer with adjusted gross income of

$180,100. She is entitled to one exemption worth $3,650. Heather’s

exemption must be reduced by $146 (12% $3,650

1

/

3

). The

12 percent is calculated as follows:

1. ($180,100 $166,800) / $2,500 ¼ 5.32, which is rounded up to 6.

2. 2% 6 ¼ 12%, the exemption reduction percentage.

3. The exemption reduction percentage is reduced to one-third of

that amount.

Heather’s allowed exemption amount is $3,504 ($3,650 $146).

The allowed exemption amount may also be calculated using the

Deduction for Exemptions Worksheet provided in the Form 1040

Instructions, as shown on the next page. If Heather had an exemption

for a dependent, this exemption would also be reduced to $3,504. N

5-24 Chapter 5

Itemized Deductions and Other Incentives

D

o

e

s

n

XX

n

EX

n

XA

o

hird ohird o

o

hird

o

o

o

th

o

hird o

hird

t

of

t

TheThe

of $of $

t

he m

f

t

T

t

Th

The

of $

xi

a

HeadHead

aximaxim

a

He

a

i

a

a

a

ead

Head

axim

i

p

rried,rried,

dofhdofh

p

fho

p

ied

of

r

p

ed

rried,

ad of h

ied,

dof

p

d, filind, filin

filinfilin

ouou

p

n

ling

p

fili

filin

,

p

fili

d, filin

, filin

ou

filin

filin

l

ngng

ng j

y

joi

y

oinoin

y

ntl

y

oin

t

t

t

t

t

o

o

o

t

xpxpa

t

p

t

axp

xpa

h

$,$,

payer’s Apayer’s A

h

yer’s

h

$2,50

$2,50

payer’s A

AG

e

damdam

0 ($10 ($1

AGAG

e

($1,2

1

e

00

e

($

da

dam

0 ($1,

AG

0($

2

ut nut n

mm

taxptaxp

untunt

2

ome

ou

2

tax

tn

ut n

m

taxp

unt,

xpa

0

ot toot to

0

ot to

0

le

0

no

0

not to l

xpay

ot to

1

ess

1

1

0

0

0

e

e

e

a

a

a

a

r

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

When total itemized deductions are about the same as the standard deduction

each year, an individual can time the payment of deductions in order to itemize

deductions every other year. A taxpayer usually has discretion over the timing of

property tax payments, charitable contributions, year-end mortgage interest pay-

ments, and certain medical expenses. Shifting the payment of these deductions

to one tax year will result in a larger benefit over a 2-year period than would

otherwise be available.

SECTION 5.8

EDUCATIONAL INCENTIVES

Qualified Tuition Programs (QTP)

A Qualified Tuition Program (sometimes called a Section 529 tuition plan) allows tax-

payers (1) to buy in-kind tuition credits or certificates for qualified higher education

expenses or (2) to contribute to an account established to meet qualified higher education

Self-Study Problem 5.7

Elvis and Greta are married taxpayers who file a joint income tax return for

2009. On their 2009 income tax return, they have adjusted gross income of

$181,000 and total itemized deductions of $12,000. The itemized deductions

consist of $5,000 in state income taxes and a $7,000 casualty loss (after the

$500 floor and after applying the 10 percent of adjusted gross income limita-

tion). Of the $12,000 of itemized deductions, what amount is allowed as a

deduction in calculating taxable income on Elvis and Greta’s 2009 federal

income tax return?

$ ____________

3,650

180,100

166,800

13,300

.12

438

146

3,504

6

X

X

Section 5.8

Educational Incentives 5-25

D

D

i

D

D

D

D

in

o

duc

come

o

o

o

duc

come

com

e

e

Of t

ction

e

e

e

e

Of t

ction

t

Of

tio

s

s

or an

the $

s

s

or an

the $

n

tota

000 in

af

n

n

tota

000 in

af

o

o

09 in

al ite

o

o

o

o

09 in

al item

09 in

l ite

t

t

ma

nco

t

t

t

ma

ncom

a

a

a

a

a

5.7

ed t

a

a

a

a

a

a

a

a

a

a

5.7

ed t

dt

p

p

p

p

p

p

p

p

p

p

p

p

p

p

l

l

y

y

y

y

y

y

y

t

fit

t

tintin

efit oefit o

t

g

to

t

ft

tin

tin

efit ov

ove

o

,,

gthegthe

oveove

o

the

o

e

o

ng

ns,

ns,

gthe

over

the

ove

t

ear

t

hashas

ear-ear-

t

sd

ar

t

h

t

d

a

has

ear-

h

deducdeduc

discrdiscr

h

du

discr

h

a

dedu

deduct

s discre

e

e

e

thethe

ctionction

e

e

ion

e

s

e

s

e

the

e

the s

ctions

the

t

2

2

2

2

2

2

2

an

0

0

0

0

1

3,50

3,50

38

14

438

1

4

14

t

t

t

t

a

x

y

e

a

r

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

expenses. Such Qualified Tuition Programs may be sponsored by a state government or a

private institution of higher learning. Distributions are generally not taxable if the funds

are used to pay qualified higher education expenses. Qualified higher education expenses

include tuition, fees, books, supplies, and equipment required for the enrollment or atten-

dance at an eligible educational institution. In addition, taxpayers are allowed reasonable

room and board costs, subject to certain limitations. The earnings portion of distributions

that are not used for qualified tuition expenses are includable in the distributee’s gross

income under the annuity income rules and are subject to a 10 percent early withdrawal

penalty.

EXAMPLE In 2010, Karen uses in-kind credits of $5,000 that were purchased

through a state qualified tuition program for her son’s college tuition.

The tuition is a qualified higher education expense of the son. There-

fore, the $5,000 distribution will be excluded from Karen’s or her

son’s income. N

EXAMPLE In 2010, Ken uses a distribution from a state QTP of $9,000 (of which

$2,000 is earnings) to pay for his son’s qualified highe r education

expenses. None of the $9,000 is taxable to Ken or his son. N

For 2009 and 2010, qualifying expenses for Section 529 plans include computer

technology such as computers, peripheral equipment, software, Internet access,

and related services. The computer t echnology must be used primarily for

education.

Unlik e Educati onal Savings Accounts, discussed on the next page, there is no income

limit on the amount of contributions to a Qualified Tuition Program. Like an Educational

Savings Account, however, the contributions are not deductible. Any contributions are

gifts, however, and thus subject to the gift tax rules. In addition, most programs impose

some form of overall maximum contribution for each beneficiary based on estimated future

higher education expenses.

EXAMPLE Bill has AGI of $275,000 and has two children. He chooses to contrib-

ute $9,000 (he is allowed to contribute any amount up to the limit

imposed by his state’s law) to a QTP for each of his children in 2010,

even with his high AGI. The $18,000 is not deductible to Bill, but any

earnings on the contribution accumulate tax free and are not taxable

if used for future qualified higher education expenses. N

A taxpayer may claim an American Opportunity credit or lifetime learning credit (dis-

cussed in detail in Chapter 6) for a tax year and exclude from gross income amounts distrib-

uted (both the principal and the earnings portions) from a qualified tuition program on behalf

of the same student. This is true as long as the distribution is not used for the same expenses

for which a credit was claimed. However, the amount of qualified higher education expenses

for a tax year for purposes of calculating the exclusion from income must be reduced by

scholarships, veterans’ benefits, military reserve benefits, employer-provided educational

assistance amounts, and American Opportunity and lifetime learning credits amounts.

5-26 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE In 2010, Sammy receives $15,000 from a qualified tuition program.

He uses the funds to pay for his college tuition and other qualified

higher education expenses. Sammy also claims an American Opportu-

nity credit of $1,500 for the year, based on the same expenses. For

purposes of the QTP exclusion calculation, the $15,000 must be

reduced to $13,500 ($15,000 $1,500). N

The tax law provides that if the total distributions from a qualified tuition program and

from an educational savings account exceed the total amount of qualified higher education

expenses, the taxpayer will have to allocate the expenses among the distributions for pur-

poses of determining how much of each distribution is excludable.

There are billions of dollars invested in the increasingly popular Section 529 Qual-

ified Tuition Programs across the country. The plans offered by different states

vary significantly and it is possible for a taxpayer to invest in the plan of a state

other than the state that he lives in. The following two Web sites offer informa-

tion comparing state plans and answers to questions regarding plan operation:

www.collegesavings.org and www.savingforcollege.com.

Educational Savings Accounts

Taxpayers are allowed to set up educational savings accounts, also known as Coverdell Edu-

cation Savings Accounts, to pay for qualified higher education expenses. The maximum

amount a taxpayer can contribute annually to an educational savings account for a beneficiary

is $2,000. Contributions are not deductible and are subject to income limits. Contributions

cannot be made to an educational savings account after the date on which the designated ben-

eficiary becomes 18 years old. In addition, contributions cannot be made to a beneficiary’s

educational savings account during any year in which contributions are made to a qualified

state tuition program on behalf of the same beneficiary. The educational savings account exclu-

sion for distributions of income is available in any tax year in which the beneficiary claims the

American Opportunity credit or the lifetime learning credit (see Chapter 6), provided the dis-

tribution is not used for the same expenses for which the credit was claimed.

Contributions to educational savings accounts are phased out between AGIs of $95,000

and $110,000 for single taxpayers and $190,000 and $220,000 for married couples who file

a joint return. Like regular and Roth IRAs, contributions must be made by April 15 of the

following year.

EXAMPLE Joe, who is single, would like to contribute $2,000 to an educational

savings account for his 12-year-old son. However, his AGI is $105,000,

so his contribution is limited to $667, calculated as follows:

($110,000 upper limit $105,000 AGI)

$15,000

$ 2,000 ¼ $667 contribution

$15,000 is the spread between the upper and lower phase-out limits. N

For parents with income above the allowable limit, a gift may be made to a child

and the contribution may be made to an educational savings account by the

child. There is no requirement that the contributor have earned income as there

is for IRAs.

Section 5.8

Educational Incentives 5-27

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Amounts received from an educational savings account are tax free if they are used for

qualified education expenses. Qualified education expenses include tuition, fees, books, sup-

plies, and related equipment for private, elementary, and secondary school expenses as well

as for college. Room and board also qualify if the student’s course load is at least 50 percent

of the full-time course load. If the distributions during a tax year exceed qualified education

expenses, part of the excess is treated as a return of capital (the contributions), and part is

treated as a distribution of earnings. The distribution is presumed to be pro rata from

each category. The exclusion for the distribution of earnings is calculated as follows:

Qualified education expenses

Total distribution

Earnings ¼ Exclusion

EXAMPLE Amy receives a $2,000 distribution from her educational savings

account. She uses $1,800 to pay for qualified education expenses. On

the date of the distribution, Amy’s account balance is $5,000, $3,000

of which are her contributions. Because 60 percent ($3,000/$5,000) of

her account balance represents her contributions, $1,200 ($2,000

60%) of the distribution is a tax-free return of capital and $800

($2,000 40%) is a distribution of earnings. The excludable amount

of the earnings is calculated as follows:

$1,800

$2,000

$800 ¼ $720 (thus, the amount taxable is $80,

or $800 $720).

Amy’s adjusted basis for her savings account is reduced to $1,800

($3,000 $1,200). N

Higher Education Expenses Deduction

Please note: The deduction for higher education expenses is expected to be extended to 2010

by Congress in the final weeks of 2010. Please see the Whittenburg companion Web site

for updated information.

Taxpayers are allowed an ‘‘above-the-line’’ deduction for qualified tuition and related

expenses incurred during the tax year. The deduction will be allowed for qualified tuition

and related expenses for enrollment at an institution of higher education during the tax

year. In addition, the deduction will be allowed for qualified expenses paid during a tax

year if those expenses are in connection with an academic term beginning during the tax

year or during the first 3 months of the next tax year.

EXAMPLE Jerry pays $2,000 for his son’s college tuition in November 2010 for

the spring 2011 term. The spring term starts in January 2011. The

$2,000 is deductible in 2010, even though it is for education provided

in a later tax year. N

The total amount of qualified tuition and related expenses for the higher education

expense deduction must be reduced by certain items. The reduction applies to: (1) exclud-

able interest from higher education savings bonds, (2) excludable distributions from qual-

ified state tuition plans, and (3) excludable distributions from educational savings accounts.

EXAMPLE Matty pays $20,000 in tuition for her children to attend college in 2010.

Included in that amount is $5,000 she received from a qualified state

tuition plan and $3,000 excluded interest from educational saving

bonds. Matty’s qualified tuition expense for purposes of the higher

education expense deduction is $12,000 ($20,000 $5,000 $3,000). N

5-28 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The deduction may not exceed a specified annual amount. The deduction is $4,000 for

single and head of household taxpayers with modified AGI below $65,000 and for married

filing jointly taxpayers with modified AGI below $130,000. The amount is $2,000 for sin-

gle taxpayers with modified AGI between $65,000 and $80,000 and for married joint filers

with modified AGI between $130,000 and $160,000. Taxpayers with AGI exceeding the

limits are not allowed a deduction.

EXAMPLE In 2010, Juan is single and has qualified higher education expenses of

$7,000. His modified AGI is $62,000. He gets a $4,000 above-the-line

deduction. If his modified AGI were $66,000, he would get a $2,000

deduction. N

Self-Study Problem 5.8

a. Abby has a distribution of $10,000 from a qualified tuition program, of

which $3,000 represents taxable earnings. The funds are used to pay for her

daughter’s qualified higher education expenses. How much of the $10,000

distribution is taxable to the daughter?

$ ____________

b.During 2010, Henry (a single taxpayer) has a salary of $85,000 and interest

income of $4,000. Calculate the maximum contribution Henry is allowed for

an educational savings account.

$ ____________

KEY POINTS

Learning Objectives Key Points

LO 5.1:

Understand the nature and treat-

ment of medical expenses.

Taxpayers are allowed a deduction for medical expenses paid for themselves, their spouse,

and their dependents.

Qualified medical expenses are deductible only to the extent they exceed 7.5 percent of a

taxpayer’s adjusted gross income.

Qualified medical expenses include such items as prescription medicines and drugs, insulin,

fees for doctors, dentists, nurses, and other medical professionals, hospital fees, hearing

aids, dentures, eyeglasses, contact lenses, medical transportation and lodging, crutches,

wheelchairs, guide dogs, birth control prescriptions, acupuncture, psychiatric care, medical

insurance premiums, and various other listed medical expenses.

LO 5.2:

Calculate the itemized deduction

for taxes.

The following taxes are deductible: income taxes (state, local, and foreign), sales taxes (by

election in lieu of state and local income tax), real property taxes (state, local, and foreign),

and personal property taxes (state and local).

Nondeductible taxes include the following: federal income taxes; employee portion of Social

Security taxes; estate, inheritance, and gift taxes (except in unusual situations not discussed

here); gasoline taxes; excise taxes; and foreign taxes if the taxpayer elects a foreign tax credit.

If real estate is sold during the year, the taxes must be divided between the buyer and

seller based on the number of days in the year that each taxpayer held the property.

To be deductible, personal property taxes must be levied based on the value of the prop-

erty. Personal property taxes of a fixed amount, or those calculated on a basis other than

value, are not deductible.

Section 5.8

Educational Incentives 5-29

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

LO 5.3:

Apply the rules for an individual

taxpayer’s interest deduction.

Deductible personal interest includes qualified residence interest (mortgage interest), prepay-

ment penalties, investment interest, and certain interest associated with a passive activity.

Nondeductible consumer interest includes interest on any loan, the proceeds of which are

used for personal purposes, such as credit card interest, finance charges, and automobile

loan interest, with the exception of the interest on ‘‘qualified home equity debt’’ used for

these purposes.

Qualified residence interest is the sum of the interest paid on ‘‘qualified residence acquisi-

tion debt’’ plus ‘‘qualified home equity debt.’’

Deductible investment interest is limited to the taxpayer’s net investment income, which is

investment income such as dividends and interest, less investment expenses other than

interest.

LO 5.4:

Determine the charitable contribu-

tions deduction.

To be deductible, the donation must be made in cash or property.

Donations must be made to a qualified recipient.

The following contributions are not deductible: gifts to social clubs, labor unions, interna-

tional organizations, and political parties; contributions of time, service, the use of property,

or blood; contributions where benefit is received from the contribution, for example, tuition

at a parochial school; and wagering costs, such as church bingo and raffle tickets.

For donated property other than cash, the general rule is that the deduction is equal to the

fair market value of the property at the time of the donation.

LO 5.5:

Compute the deduction for casu-

alty and theft losses.

A casualty is a complete or partial destruction of property resulting from an identifiable

event of a sudden, unexpected, or unusual nature. Examples include property damage from

storms, floods, shipwrecks, fires, automobile accidents, and vandalism.

For the partial destruction of business or investment property and the partial or complete

destruction of personal property, the deduction is the decrease in fair market value of the

property, not to exceed the adjusted basis of the property.

For the complete destruction of business and investment property, the deduction is the

adjusted basis of the property.

The amount of each personal casualty loss is reduced by $100 and only the excess over 10

percent of the taxpayer’s adjusted gross income is deductible.

LO 5.6:

Identify miscellaneous itemized

deductions.

Miscellaneous deductions fall into two categories, those limited to the extent the total

exceeds 2 percent of adjusted gross income and those with no limitation.

Examples of items which are not subject to the 2 percent of adjusted gross income limita-

tion are handicapped impairment-related work expenses, certain estate taxes, amortizable

bond premiums, terminated annuity payments, and gambling losses to the extent of gam-

bling winnings.

Common miscellaneous deductions that are subject to the 2 percent limitation include unre-

imbursed employee business expenses and employee business expenses reimbursed under a

nonaccountable plan, investment expenses, tax return preparation fees, union dues, job-

hunting expenses, and professional subscriptions.

LO 5.7:

Understand the basic theory

behind the itemized deduction and

exemption phase-outs for high-

income taxpayers for years prior to

and subsequ ent to 201 0.

In 2009, an individual taxpaye r whose adjusted gross income exceeds a threshold amount

must reduce the amount of his or her total itemized deductions by 1 percent of the excess

of adjusted gross income over the threshold amount.

The 2009 exemption deduction is phased out to a minimum of two-thirds of the $3,650

exemption amount, or $2,433, if a taxpayer has adjusted gross income (AGI) exceeding a

certain threshold amount.

LO 5.8:

Understand the tax implications

of using educational savings

vehicles.

A Qualified Tuition Program (a Section 529 plan) allows taxpayers (1) to buy in-kind tuition

credits or certificates for qualified higher education expenses or (2) to contribute to an

account established to meet qualified higher education expenses. Earnings on the account

are not taxable if the account is used for qualified higher education expenses.

5-30 Chapter 5

Itemized Deductions and Other Incentives

e

ertaertai

D

i

D

rta

D

m

xem

ertai

erta

o

o

pp

ntnt

o

th

o

nt

o

p

o

o

p

nt

nt

e

h

e

onon

hre

hre

e

h

e

on

on a

hre

n

h

s

s

amam

sho

sho

s

sh

am

am

sho

n

un

n

untunt

dd

t

unt

da

o

,

o

,or

,o

o

t

o

t, o

,o

t

r

t

dd

rr

t

d

de

or $

2

a

ducduc

2424

a

ct

4

a

duc

2

d

duct

2,43

24

p

3,

p

tiontion

33,33,

p

o

3

ion

tion

33,

io

33

p

if a

p

nisnis

ifif

is

p

i

nis

if

is

f

l

p

y

ph

t

y

ha

tax

y

phph

tt

y

ph

pha

ta

t

se

t

ss

eded

t

ed

t

es

esh

ed

d

o

do

do

o

do

o

hol

hol

do

do

t

t

t

aa

t

a

a

tt

h

mo

h

momo

h

mo

amo

t

e

untunt

e

e

ount

unt

2

dedded

2

de

2

ded

ded

0

uctuct

0

duc

duct

uc

1

io

1

tio

io

tio

0

sbsb

0

0

s

0

0

c

b

ns b

sb

t

y

t

ee

11

t

e

t

ed

e

y1

a

pepe

a

a

e

a

p

a

1

s

1pe

rc

x

aa

tt

ercerc

x

a

e

x

th

ce

x

t

a

th

erce

y

re

nt

y

h

o

y

resres

tt

y

es

resh

nt

e

f

e

holdhold

ff

e

e

hold

e

ld

hold

ft

hol

a

h

a

dd

aa

a

a

a

a

a

d

a

d

d

am

a

r

mo

r

mm

r

m

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.