Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Chapter 5

Itemized Deductions

and Other Incentives

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 5.1 Understand the nature and treatment of medical expenses.

LO 5.2 Calculate the itemized deduction for taxes.

LO 5.3 Apply the rules for an individual taxpayer’s interest deduction.

LO 5.4 Determine the charitable contributions deduction.

LO 5.5 Compute the deduction for casualty and theft losses.

LO 5.6 Identify miscellaneous itemized deductions.

LO 5.7 Understand the basic theory behind the itemized deduction

and exemption phase-outs for high-income taxpayers for

years prior to and subsequent to 2010.

LO 5.8 Understand the tax implications of using educational

savings vehicles.

Overview

The tax law allows individual taxpayers to deduct certain items from gross income when cal-

culating taxable income. One kind of deduction is the deduction for (above-the-line) AGI such

as alimony paid, deductible IRAs, and the expenses of self-employed persons (on Schedule C)

or landlords (on Schedule E). These deductions are discussed in Chapters 1–4.

The other type of deduction in the individual tax formula is the deduction from AGI. The

standard deduction in Chapter 1 is an example of a deduction from AGI. This chapter will

introduce the Schedule A itemized deductions and temporary special additions to the stan-

dard deduction. Itemized deductions fall into six categories: medical, state and local taxes,

interest, charitable contributions, casualty and theft losses, and miscellaneous deductions.

Unreimbursed employee expenses are deductible as a miscellaneous itemized deduction.

Most itemized deductions are personal expenses which Congress has deemed to be deductible

for various social or economic policy purposes. For example, in order to encourage home own-

ership, the tax law allows a deduction (within certain limits) for personal home mortgage interest.

When calculating taxable income, individuals determine their standard deduction and their

allowable itemized deductions, and use the larger of the two. For example, if a taxpayer’s stan-

dard deduction is $8,400 and her itemized deductions are $14,200, she would use her itemized

deductions in calculating taxable income. On the other hand, if her itemized deductions were

$6,500, she would use the larger $8,400 standard deduction in computing taxable income.

5-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 5.1

MEDICAL EXPENSES

Medical expenses are the first itemized deduction on Schedule A. Taxpayers are allowed a deduc-

tion for the medical expenses paid for themselves, their spouse, and dependents. Congress

decided, however, that a certain portion of medical expenses is personal in nature and should

not be deductible; therefore, limitations have been established on the amount that may be

deducted. Medical expenses can only be deducted to the extent that they exceed 7.5 percent

of the taxpayer’s AGI. The formula for calculating a taxpayer’s medical expense deduction is

as follows:

Prescription medicines and drugs, insulin, doctors,

dentists, hospitals, medical insurance premiums

$ xxx

Other medical and dental expenses, such as lodging,

transportation, eyeglasses, contact lenses, etc.

xxx

Less: insurance reimbursements (

xxx)

Subtotal xxx

Less: 7.5 percent of adjusted gross income (

xxx)

Excess expenses qualifying for the m edical deduction

$ xxx

What Qualifies as a Medical Expense?

Expenses that are deductible as medical expenses include the cost of items for the diagno-

sis, cure, mitigation, treatment, and prevention of disease. Also included are expenditures

incurred that affect any structure or function of the body. Therefore, amounts for all of the

following categories of expenditures qualify as medical expenses:

Prescription medicines and drugs and insulin

Fees for doctors, dentists, nurses, and other medical professionals

Hospital fees

Hearing aids, dentures, eyeglasses, and contact lenses

Medical transportation and lodging

Medical aids, such as crutches, wheelchairs, and guide dogs

Birth control prescriptions

Acupuncture

Psychiatric care

Medical insurance premiums

Certain capital expenditures

Nursing home care for the chronically ill (e.g., Alzheimer’s disease care)

The IRS has allowed the follow ing unusual medical expenses:

Long-distance phone calls made to a psychological counselor

New siding replacing old siding on a home because the taxpayer was

allergic to mold growing on the old siding

A wig prescribed by a psychiatrist for a taxpayer upset by hair loss

A cell phone for a taxpayer who may need instantaneous medical help

Treatments provided by an Indian medicine man

Certain medical expenses are not deductible. For example, the cost of travel for the gen-

eral improvement of the taxpayer’s health is not deducti ble. The expense of a swimming

5-2 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

pool is not deductible unless the pool is designed specially for the hydrotherapeutic treat-

ment of the taxpayer’s illness. No deduction is allowed for the cost of weight-loss programs

(unless prescribed by a doctor; diet foods do not qualify) or marriage counseling. Medical

expenses for unnecessary cosmetic surgery or similar procedures are not deductible.

Cosmetic surgery is considered unnecessary unless it corrects (1) a congenital abnormality,

(2) a personal injury resulting from an accident or trauma, or (3) a disfiguring disease. In

general, unnecessary cosmetic surgery is any procedure which is directed at improving the

patient’s appe arance and does not meaningfully promote the proper function of the body

or prevent or treat illness or disease.

Although laws in California, Arizona, and some other states legalize marijuana

for medical use in some instances, the IRS has ruled that taxpayers ca nnot

deduct the cost of marijuana as a medical expense.

Medical Insurance

Medical insuranc e includes standard health policies, whether the benefits are paid to the

taxpayer or to the provider of the services directly. In addition, the premiums paid for

membership in health maintenance plans are deductible as medical insurance, as are sup-

plemental payments for optional Medicare coverage. Insurance policies that pay a specific

amount each day or week the taxpayer is hospitalized are not considered medical insurance

and the premiums are not deductible. Premiums paid for qualified long-term care insur-

ance policies are also deductible medical expenses up to specified limits which change

each year and are based on the age of the taxpayer.

Self-employed taxpayers are allowed, subject to certain limitations, a deduction in arriv-

ing at adjusted gross income equal to 100 percent of the medical insurance premiums paid

for themselves and their families. Long-term car e insurance prem iums, up to a specified

amount based on the taxpayer’s age, are considered health insurance for this pur pose. If

a deduction is taken for these items in arriving at AGI, then these same expenses are

excluded from the medical expense deduction on Schedule A.

Medicines and Drugs

Prescription medicines and drugs and insulin are the only drugs deductible as medical

expenses. No deduction is allowed for drugs purchased illegally from abroad, including

Canada and Mexico. Nonprescription medicines such as over-the-counter antacids, allergy

medications, and pain relievers, even if recommended by a physician, are not deductible as

a medical expense.

Capital Expenditures

Payments for special equipment purchased and installed in the taxpayer’s home for medical rea-

sons may also be deductible. Unlike other capital expenditures, allowable amounts are deducted

fully in the year the item is purchased. If the expenditure is for an improvement that increases

the value of the taxpayer’s property, the deduction is limited to the amount by which the expen-

diture exceeds the increase in the value of the property. If the value of the property does not

increase as a result of the expenditure, the entire cost is deductible. The cost of upkeep and

operation of an item, the cost of which qualified as a medical expense, is also deductible, pro-

vided the medical reason for the improvement or special equipment still exists.

Section 5.1

Medical Expenses 5-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE A taxpayer ha s a heart condition and installs an elevator in his home

at a cost of $6,000. The value of the home is increased by $4,000 as

a result of the improvement. The taxpayer is allowed a deduction of

$2,000 ($6,000 $4,000), the excess of the cost of the equipment

over the increase in the value of the taxpayer’s home. N

Transportation

Transportation expenses primarily for and necessary to medical care are deductible, includ-

ing amounts paid for taxis , trains, buses, airplanes, and ambulances. Taxpayers may also

claim a deduction for the use of their personal automobile for medical transportation.

However, only out-of-pocket expenses such as the cost of gas and oil are deductible. Main-

tenance, insurance, general repair, and depreciation expenses are not deductible. If the tax-

payer does not wish to deduct actual costs of transportation by personal automobile, a

standard mileage rate of 16.5 cents per mile may be used to calculate the deduction. In

addition to the deduction for actual automobile costs or the standard mileage amount,

parking and toll fees for medical transportation are deductible medical expenses. If the

transportation expenses are for the medical care of a dependent child, the amounts are

deductible by the parent.

Lodging for Medical Care

Taxpayers may deduct the cost of lodging up to $50 per night, per person, on a trip pri-

marily for and essential to medical care provided by a physician or a licensed hospital. The

deductio n is allowed for the patient and an individual accompanying the patient, such as

the parent of a child. However, no deduction is allowed if the trip involves a significant

element of recreation or vacation. No deduction is allowed for meal costs.

A Las Vegas dentist admitted he provided free dental work to an IRS revenue

officer in exchange for reductions of his $100,000 tax debt. Both men were

indicted on conspiracy and bribery charges.

Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) combine tax-deductible contributions to medical spend-

ing accounts with qualifying high-deductible medical insurance. Regular health insurance

plans with low deductibles and co-payments will not qualify for use with an HSA. Personal

contributions to an HSA are limited to certain dollar amounts depending on age and

whether the insurance is for an individual or a family. Contributions to HSAs are a deduc-

tion for AGI just l ike the deduction for IRAs. Earnings accumulated in an HSA are not

taxed, and distributions to cover medical expenses are not taxed or penalized. Any amounts

left in the HSA which are not used to pay medical expenses will compound tax free like an

IRA investment.

HSAs are meant to take the place of Medical Savings Accou nts (MSAs), allowed since

1997 but rarely used despite extensive publ icity. The newer HSAs are expected to have

wider appeal since they are available to a variety of taxpayers. Individuals with MSAs

5-4 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

can roll them over into the new HSAs. For more info rmation on HSAs, con sult the IRS

Web site or a tax research service.

SECTION 5.2

TAXES

The next itemized deduction that taxpayers are allowed is the deduction for certain state,

local, and foreign taxes paid during the year. The purpose of the deduction for taxes is to

relieve the burden of multiple taxation of the same income . However, the tax law distin-

guishes betwee n a ‘‘tax’’ an d a ‘‘fee. ’’ A tax is imposed by a government to raise revenue

for general public purposes, and a fee is a charge with a direct benefit to the person paying

the fee. Taxes are gener ally deductible; fees are not deductible. For example, postage, fish-

ing licenses, and dog tags are not deductible as taxes.

If a taxpayer itemizes his or her deductions on Schedule A, the following taxes are

deductible for 2010:

Income taxes (state, local, and foreign)

Sales taxes (by election in lieu of state and local income tax)

Real estate property taxes (state, local, and foreign)

Personal property taxes (state and local)

The following taxes are not deductible:

Federal income taxes

Employee portion of Social Security taxes

Estate, inheritance, and gift taxes (except in unusual situations not discussed here)

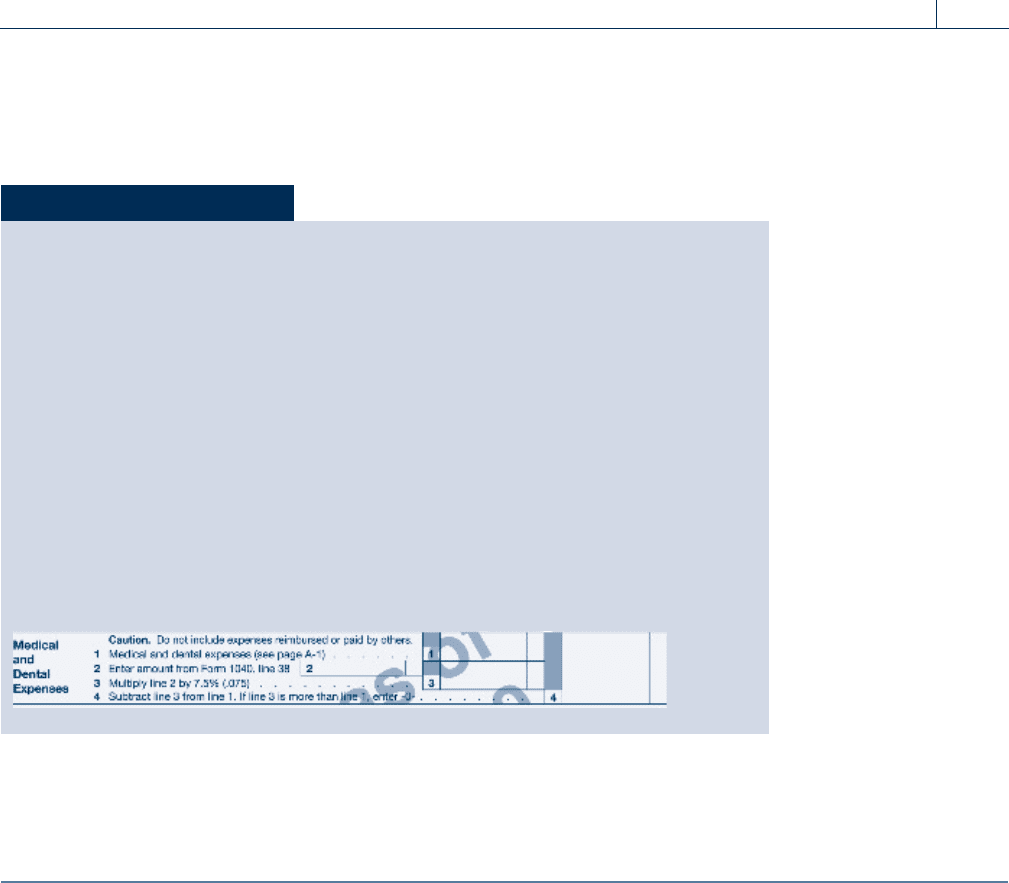

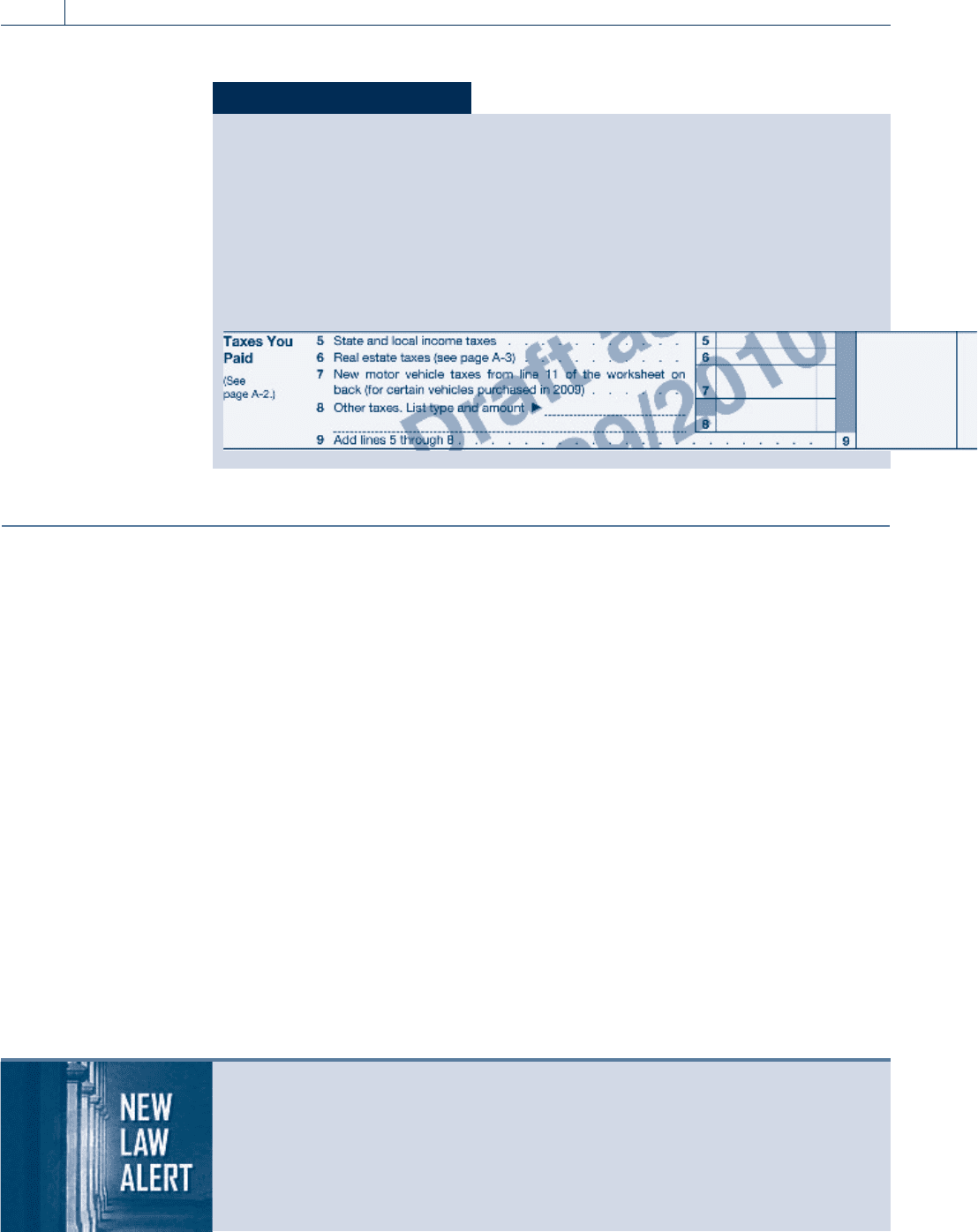

Self-Study Problem 5.1

During the 2010 tax year, Frank and Betty paid the following medical expenses:

Hospitalization insurance $ 425

Prescription medicines and drugs 364

Hospital bills 2,424

Doctor bills 725

Eyeglasses for Frank’s dependent mother 75

Doctor bills for Betty’s sister, who is claimed

as a dependent by Frank and Betty

220

In addition, in 2010, they drove 848 miles for medical transportation in

their personal automobile. Their insurance company reimbursed Frank and

Betty $1,420 during the year for the medical expenses. If their adjusted gross

income for the year is $25,400, calculate their medical expense deduction.

Use the segment of Schedule A of Form 1040 reproduced below.

Section 5.2

Taxes 5-5

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Foreign taxes if the taxpayer elects a foreign tax credit

Gasoline taxes

Excise taxes

Taxes paid in connection with a trade or business or any activity for the production of

income, such as payroll taxes, personal property taxes, etc., are deductible for adjusted

gross income by the taxpayer on Schedule C, E, or F, instead of Schedule A.

Income Taxes and Sales Taxes

Please note: As we go to press, the deduction for sales tax is expected to be extended to 2010

by Congress in the final weeks of 2010. Please see the Whittenburg companion Web site

for updated information.

Taxpayers may elect to take either state and local sales and use taxes or state and local

income taxes as it emized deductions. The election to take a deduction for state sales tax

instead of state income t ax primarily benefits taxpayers in states with no income taxes or

low income tax rates.

For taxpayers electing to deduct state and local income taxes paid during 2010, the

amount of the deduction is the t otal amount of state and local taxes withheld from

wages plus any amounts actually paid during the year, even if the tax pay ments are for a

prior year’s tax liability. If the taxpayer receives a refund of taxes deducted in a previous

year, the refund must generally be include d in gross income in the year the refund is

received. Taxes which did not provide any tax benefit (reduction in taxes) in the year

paid are not required to be included in income in the year received as a refund. For exam-

ple, a taxpayer claiming the standard deduction in the year taxes are paid does not receive a

tax benefit for the payment and is not required to include a tax refund received the follow-

ing year in income.

EXAMPLE For 2010, Mary elects to take state income taxes rather than state

sales taxes as an itemized deduction. Mary has $1,800 of state income

taxes withheld from her wages during 2010. In April of 2010, she

paid an additional $250 on her 2007 state income tax return. Mary’s

deduction for state income taxes is $2,050 ($1,800 + $250). Her state

income tax liability for the 2009 year was $1,650, resulting in a $150

refund ($1,800 $1,650) that was received in 2010. The $150 refund is

reported as income in the 2010 return, assuming Mary received a ben-

efit from the state tax deduction for 2009. N

For taxpayers electing to deduct sales taxes in 2010, the deduction may be calculated by

using either (a) actual sales taxes paid or (b) sales taxes from IRS tables plus the actual

amount of sales tax for motor vehicles, boats, airplanes, and building materials (not appli-

ances or furnishings) for building or improving a residence. Taxpayers choosing to deduct

actual sales taxes paid will be required to keep extensive records to support the amount of

the deduction claimed including receipts for every item purchased during the year subject

to sales tax.

Property Taxes

Taxes that are levied on state, local, or foreign real property for the general public welfare

are deductible. However, special assessmen ts charged to prov ide local benefit to property

owners are not deductible; these amounts increase the basis of the taxpayer’s property.

Also, service fees, such as garbage fees and homeowner association fees, are not deductible

as property taxes.

5-6 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

If real estate is sold during the year, the taxes must be divided betwe en the buyer and the

seller, and the division must be made according to the number of days in the year that each

taxpayer held the property.

EXAMPLE Sally sells her home to Patty on March 2, 2010. The taxes for 2010

are paid by Patty and they total $1,825, or $5.00 per day ($1,825/

365 days). The purchaser is treated as the owner on the day of sale.

Sally is entitled to deduct 60 days of real property taxes or $300

(60 days $5.00 per day). Patty deducts $1,525 (305 days $5.00

per day). N

Generally, the escrow company or closing agent handling the sale of the property will

make the allocation of taxes for the buyer and the seller and the result will be reflected in

the settlement charges on the transfer of the title. These amounts are itemized on closing

statements for the sale, which are provided to the buyer and the seller.

EXAMPLE William purchased a new residence from John in 2010. William’s clos-

ing statement shows that he receives a credit for $299.80 in taxes

that he will pay later in the year for the seller. Assuming that William

pays $525.00 in total taxes on the property later in 2010, his property

tax deduction for 2010 would be $225.20 ($525.00 $299.80). John,

the seller, would be allowed a deduction for $299.80 plus any other

taxes he paid prior to selling the property. N

Taxpayers who do not itemize deductions on Schedule A are allowed to take

an extra deduction in addition to the standard deduction for a portion of the

property tax paid in 2008 and 2009. As we go to press, this deduction is

expected to be extended to 2010. The amount of the deduction allowed is

$500 for single taxpayers and $1,000 for married taxpayers. If the property

tax paid is less than $500, or $1,000 if ma rried, the deduction is limited to

the amount paid. Taxpayers must fill in Schedule L, ‘‘Standard Deduction

for Certain Filers,’’ to claim this deduction.

Personal Property Taxes

To be deductible as an itemized deduction, property taxes must be levied based on the

value of the property. Taxes of a fixed amount, or those calculated on a basis other than

value, are not deductible. For example, automobile fees that are calculated on the basis

of the automobile’s weight are not deductible.

EXAMPLE Rich lives in a state that charges $20 per year plus 2 percent of the

value of the automobile for vehicle registration. If Rich pays $160

[$20 þ (2% $7,000)] for his automobile registration, he may

deduct only $140, the amount that is based on the value of the

automobile. N

Section 5.2

Taxes 5-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 5.3

INTEREST

Taxpayers are allowed a deduction for certain interest paid or accrued during the tax year.

Interest is defined as an amount paid for the use of borrowed funds. The type and amount

of the deduction depend on the purpose for which the money is borrowed. Interest on

loans for business, rent, and royalty activities is deducted for adjusted gross income. Cer-

tain interest on loans for personal purposes is deductible as an itemized deduction. The fol-

lowing types of personal interest are deductible:

Qualified residence interest (mortgage interest)

Mortgage interest prepayment penalties

Investment interest

Certain interest associated with a passive activity

Interest on other loans for personal purposes which do not fall into one of the above

categories is generally referred to as consumer interest and is not deductibl e. Consumer

interest includes interest on any loan, the proceeds of which are used for personal purposes,

such as bank charge card interest, finance charges, and automobile loan interest. Interest on

loans used to aquire assets generating tax-exempt income is also not deductible.

The following items are not considered ‘‘interest’’ and, therefore, are also not deductible:

Service charges

Credit investigation fees

Loan fees other than ‘‘points’’ discussed later under Prepaid Interest

Interest paid to carry single premium life insurance

Premium on convertible bonds

Many lenders require that certain home mortgage borrowers pay for private

mortgage insuranc e (PMI) or other agency mortgage insurance to protect the

lender. Mortgage insurance issued related to debt used to acquire a principal

residence is fully deductible in years 2007 through 2010 for taxpayers with

adjusted gross income of $100,000 or less ($50,000 or less if married and filing

separately). The deduction is phased out for AGI over $100,000, and is fully

phased out for AGI over $109,000.

Self-Study Problem 5.2

Sharon is single, lives in Idaho, and has adjusted gross income of $21,150 for

2010. Sharon elects to deduct state income tax rather than state sales tax. The

tax withheld from her salary for state income taxes is $1,050, and in May of

the same year she received a $225 refund on her state income tax return for

the prior year. Sharon paid real estate taxes on her house of $825 for the year

and an automobile registration fee of $110, of which $25 is based on the

weight of the automobile and the balance on t he value of t he property. Use

the taxes section of Schedule A below to report Sharon’s deduction for state

and local taxes.

5-8 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Taxpayer’s Obligation

To deduct interest on a debt, the taxpayer must be legally liable for the debt. No deduction

is allowed for payments made for another’s obligation, where the taxpayer is not liable for

payment. Also, both the lender and the borrower must intend for the loan to be repaid.

EXAMPLE Bill makes a payment on his son’ s home mortgage since his son is

unable to make the current payment. The interest included in the

mortgage payment is not deductible by Bill since the mortgage is not

his obligation. Bill’s son cannot deduct the interest since he did not

make the payment. N

Note: A recent court case has decided that a relative, who essentially has an own-

ership interest in the residence, may deduct mortgage interest paid even if not

named on the loan.

EXAMPLE Mary loans her daughter $50,000 to start a business. The daughter is

19 years old and unsophisticated in business. No note is signed and

no repayment date is mentioned. Mary would be surprised if the

daughter’s business venture is a success. Since, in all likelihood, a true

debtor-creditor relationship is not created, any interest paid by the

daughter is not deductible. N

Prepaid Interest

Cash basis taxpayers are r equired to use the accrual basis for deducting prepaid interest.

Prepaid interest must be capitalized and the deduction spread over the life of the loan.

This requirement does not apply to points paid on a mortgage loan for purchasing or

improving a taxpayer’s principal residence, pr ovided points are customari ly charged and

they do not e xceed the normal rate. Such points paid on a mortgage for the purchase of

a personal residence may be deducted in the year they are pa id. Points paid to refinance

a home mortgage are not deductible when paid, but must be capitalized and the deduction

spread over the life of the loan. Points charged for specific loan services, such as the lend-

er’s appraisal fee and other settlement fees, are not deductible.

EXAMPLE On November 1, 2010, Allen, a cash basis taxpayer, obtains a 6-month

loan of $500,000 on a new apartment building. On November 1, Allen

prepays $36,000 interest on the loan. He must capitalize the prepaid

interest and deduct it over the 6-month loan period. Therefore, his

interest deduction for 2010 is $12,000 ($36,000/6 months 2 months). N

Qualified Residence, Home Equity, and Consumer Interest

Since 1991, no deduction has been available for consumer (personal) interest, such as inter-

est on credit cards and loans for personal automobiles. Qualified residence interest, how-

ever, is a type of personal interest specifically allowed as a deduction. The term ‘‘qualified

residence interest’’ is the sum of the interest paid on ‘‘qualified residence acquisition debt’’

plus ‘‘qualified home equity debt.’’ The aggregate amount of qualified acquisition debt may

not exceed $1,000,000 ($500,000 for married filing separately), and the aggregate amount

of qualified home equity debt may not exceed $100,000 ($50,000 for married filing sepa-

rately). Thus, the total amount of acquisition and home equity debt on the taxpayer’s res-

idence may not exceed $1,100,000 ($550,000 for married filing separately).

Section 5.3

Interest 5-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The term ‘‘acquisition debt’’ is defined as debt secured by the taxpayer’s principal or

second residence incurred in acquiring, constructing, or substantially improving that resi-

dence. Refinanced debt is treated as acquisition debt only to the extent it does not exceed

the principal amount of acquisition debt immediately before the refinancing. The term

‘‘home equity debt’’ is defined as debt secured by the taxpayer’s principal or second resi-

dence, and which is not acquisition debt. Interest on qualifying home equity debt is deduct-

ible even if the proceeds are used for personal purposes.

EXAMPLE Vicky’s residence has a fair market value of $300,000. The first mort-

gage, used to buy the house 10 years ago, is $125,000. This year, she

borrows $115,000 on a second mortgage secured by the house, to

send her children to college. The interest paid on the first mortgage

is fully deductible, but interest on only $100,000 of the second mort-

gage is deductible.

Assume $8,000 of interest is paid by Vicky on the first mortgage

and $7,000 is paid on the second mortgage. Vicky’s mortgage interest

deduction is calculated as follows:

Interest on acquisition debt $ 8,000

Interest on home equity debt

$7,000 $100,000/$115,000

6,087

Mortgage interest deduction allowed

$14,087

The remaining interest on the home equity debt ($7,000 $6,087 ¼

$913) is considered nondeductible personal interest. N

An additional limit on the $100,000 qualified home equity debt allowed is the fair mar-

ket value of the residence. For example, assume a taxpayer has the maximum $1,000,000 of

acquisition debt and $100,000 of home equity debt. If the fair market value of the residence

goes down to $1,050,000, only $50,000 of the home equity debt will qualify for an interest

deduction. The reduction in home values during the recent recession has made this limi-

tation more relevant than in past years.

Deduction for consumer inter est, including any excess mortgage interest, automobile

loan interest, and interest on credit cards, is not allowed.

If the sum of mortgage interest and other itemized deductions is less than the

standard deduction, no tax benefit is received from the mortgage interest pay-

ments. In this case, a taxpayer may wish to pay the mortgage off as quickly as

possible since few investments earn a guaranteed tax-free return equal to the

interest rate on a home mortgage.

Education Loan Interest

Taxpayers are allowed a deducti on for adjusted gross income for certain interest paid on

qualified education loans. The deduction is limited to $2,500 for 2010, and is phased

out for single taxpayers with modified AGI of $60,000 to $75,000 and for married tax-

payers with modified AGI of $120,000 to $150,000. Qualified higher education expenses

include tuition, room and board, and related expenses.

5-10 Chapter 5

Itemized Deductions and Other Incentives

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.