Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE, Chapter 7: Accounting principles page 31

• The business will last another 6 years, until 31 December 2010. At this date it will

quietly expire.

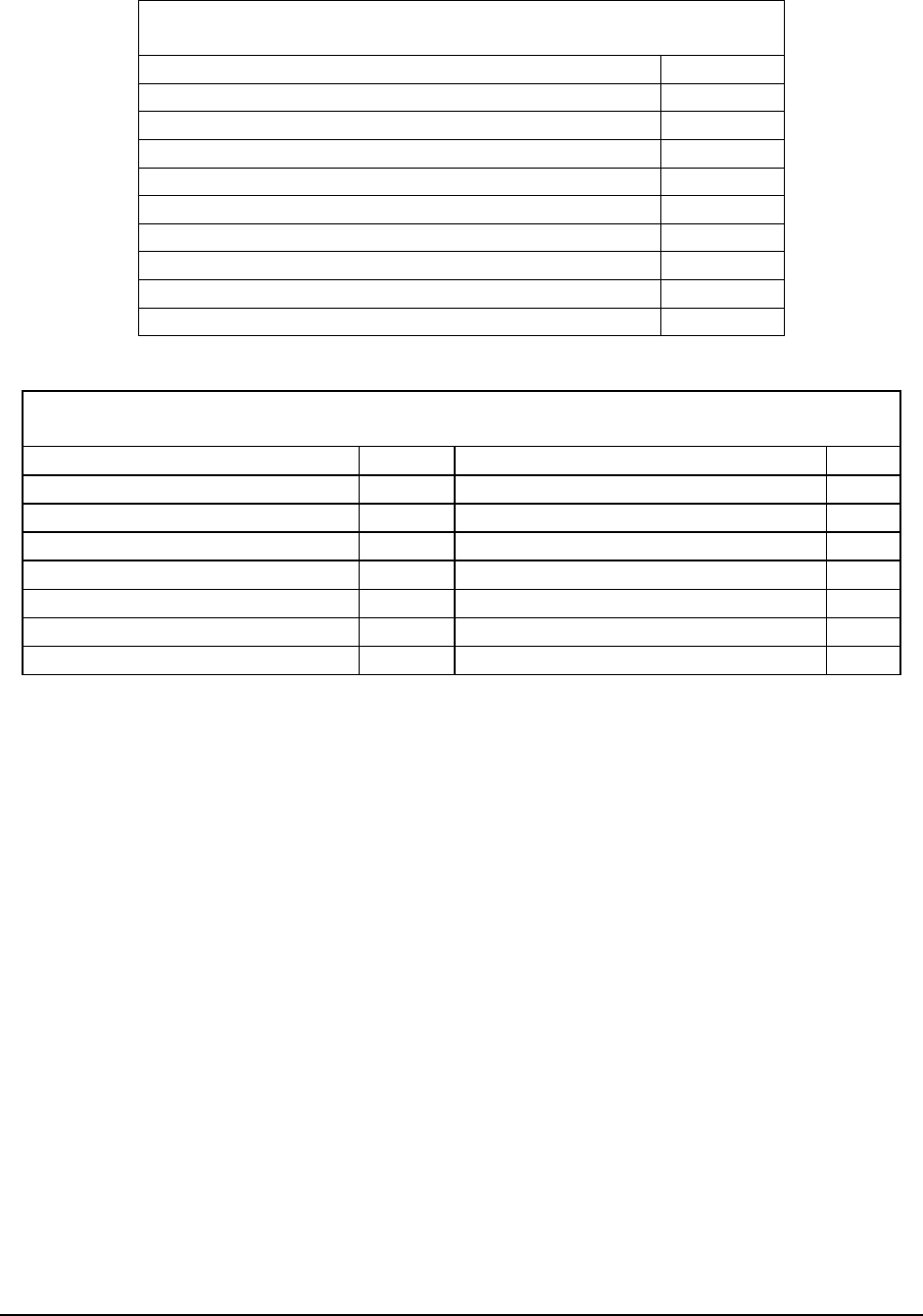

5

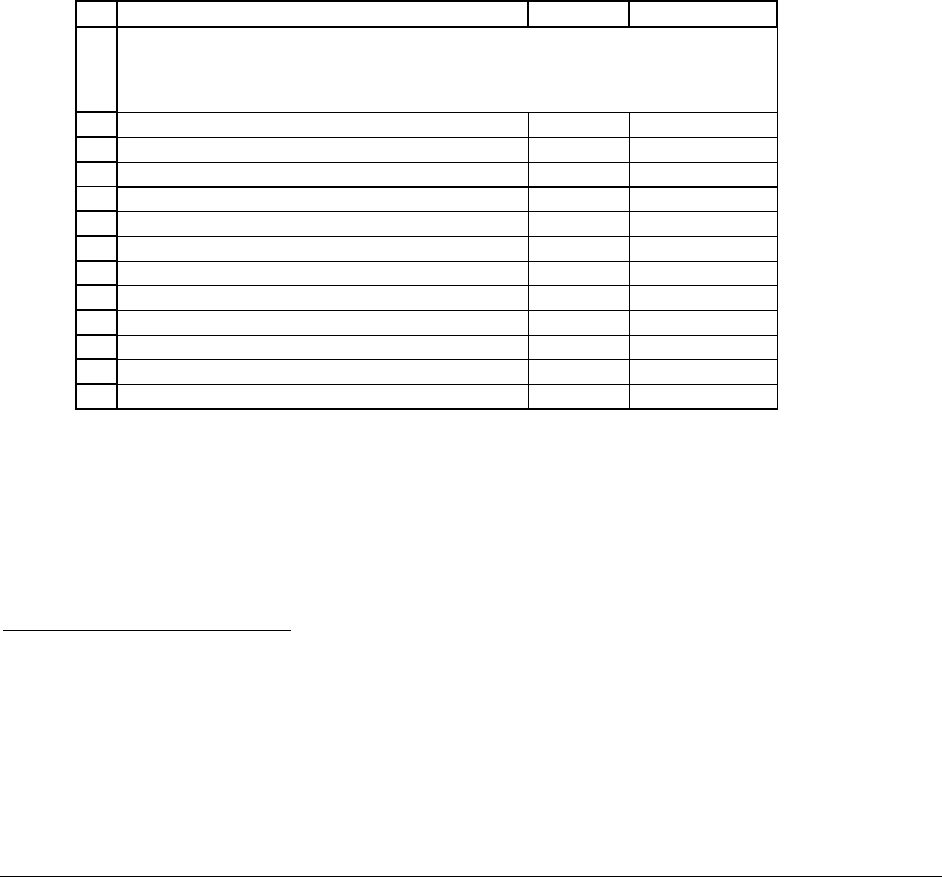

Brother-Sister assume that at the end of 2010 they’ll be able to sell the

building for $150,000. At that point the building will have been on ATS’s books for 6 ½

years. Since its monthly depreciation is $666.67, its accumulated depreciation will be

$52,000 (= 78 months *$666.67). Because the building was purchased for $80,000, its

book value at the end of 2010 will be $28,000 (book value = initial cost minus

accumulated depreciation). The net, after-tax cash flow from selling the building is given

below:

1

2

3

4

5

6

7

8

9

10

11

12

13

ABC

Book value of building

Initial cost 80,000

Accumulated depreciation, end 2010 52,000 <-- =78*666.67

Book value 28,000 <-- =B3-B4

Market value 150,000

Taxable gain 122,000 <-- =B7-B5

State tax on marketable gain (5%) 6,100 <-- =5%*B8

Gain for Federal tax purposes 115,900 <-- =B8-B9

Federal tax (36%) 41,724 <-- =36%*B10

Total taxes 47,824 <-- =B11+B9

Net after-tax cash flow from sale of building 102,176 <-- =B7-B12

ANYTOWN TRAVEL SERVICES (ATS), INC.

Building residual value at end-2010

5

A lot of the value of the business derives from the fact that Anytown didn’t have a taxi service. Brother-sister

figure that in another few years, more taxi operators will enter the business and make the business less profitable.

They’ve already started lobbying the Anytown city council to introduce strict taxi licensing regulations (with

existing operators grandfathered in ... ).

PFE, Chapter 7: Accounting principles page 32

Valuing the business

To value the business, ATS need to compute the cash flows and discount them by an

appropriate cost of capital. They assume that the appropriate discount rate is 30%. Here’s their

calculation:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

ABCDE

Date FCF

A

dditional capex Residual value Total

31-Dec-04 206,658 206,658

31-Dec-05 206,658 -40,000 166,658

31-Dec-06 206,658 206,658

31-Dec-07 206,658 206,658

31-Dec-08 206,658 -40,000 166,658

31-Dec-09 206,658 206,658

31-Dec-10 206,658 102,176 308,834

Discount rate 30%

Enterprise value =

PV of future free cash flows

560,922 <-- =NPV(B11,E3:E9)

Add back cash balances

on 31 December 2003

179,436

Asset value of firm,

31 December 2003

740,358

Debt on 31 December 2003 57,000 <-- Outstanding mortgage

Value of equity 683,358 <-- =B15-B16

ANYTOWN TRAVEL SERVICES (ATS), INC.

Quick and dirty valuation

Here are the details of the valuation:

•

Assuming a discount rate of 30% for the cash flows, the enterprise value on 31 December

2003 at $560,922. We use the term

enterprise value to denote the present value of the

firm’s future free cash flows and terminal value.

6

•

In addition to this enterprise value, the firm has $179,436 cash on hand on 31 December

2003. Adding this cash to the enterprise value gives the asset value of the firm on this

date as $740,358.

6

We have an extended discussion of the enterprise value in the next chapter.

PFE, Chapter 7: Accounting principles page 33

• Since there is a mortgage outstanding on this date of $57,000, brother-sister’s equity

stake in the business is worth $683,358 = $740,358 - $57,000.

Not bad for a year’s work!

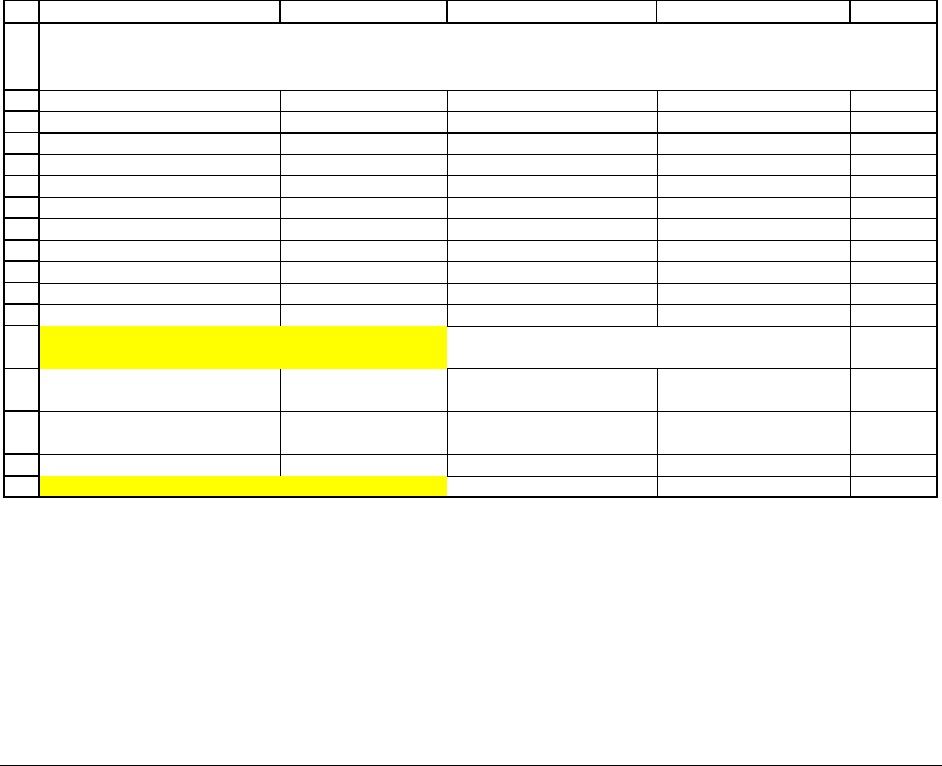

Technical comment: mid-year discounting

In Chapter 4, section000, we discussed the concept of mid-year discounting to account

for the fact that cash flows occur throughout the year and not at year’s end. Mid-year

discounting assumes that the annual cash flows occur in mid-year, and not at year’s end.

Had Brother and Sister valued their firm by using mid-year discounting, they would have

concluded that the equity value of the Anytown Travel Services was $761,985:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

ABCDE

Date FCF

A

dditional capex Residual value Total

31-Dec-04 206,658 206,658

31-Dec-05 206,658 -40,000 166,658

31-Dec-06 206,658 206,658

31-Dec-07 206,658 206,658

31-Dec-08 206,658 -40,000 166,658

31-Dec-09 206,658 206,658

31-Dec-10 206,658 102,176 308,834

Discount rate 30%

Enterprise value =

PV of future free cash flows

639,549 <-- =NPV(B11,E3:E9)*(1+B11)^0.5

Add back cash balances

on 31 December 2003

179,436

Asset value of firm,

31 December 2003

818,985

Debt on 31 December 2003 57,000 <-- Outstanding mortgage

Value of equity 761,985 <-- =B15-B16

ANYTOWN TRAVEL SERVICES (ATS), INC.

Valuation assuming mid-year discounting

PFE, Chapter 7: Accounting principles page 34

Conclusion

In this chapter we’ve reviewed the basic methodology of financial accounting. We’ve

reviewed the construction of the balance sheet, the profit and loss statement, and the statement of

cash flows of a business. In addition we showed how to construct a free cash flow statement and

how to use this statement to value a business.

PFE, Chapter 8: Financial planning models page 1

CHAPTER 8: FINANCIAL PLANNING MODELS

*

this version: 24 July 2003

Chapter contents

Overview......................................................................................................................................... 1

8.1. Initial accounting statements for a financial planning model................................................. 3

8.2. Building a financial planning model.......................................................................................8

8.3. Extending the model to years 2 and beyond......................................................................... 18

8.4. Free cash flow (FCF): measuring the cash produced by the firm’s operations................... 21

8.5. Reconciling the cash balances—the consolidated statement of cash flows.......................... 25

Conclusion .................................................................................................................................... 28

Exercises....................................................................................................................................... 29

Overview

This chapter explains how to build spreadsheet models that allow you to predict the

future performance of a firm. These models are called financial planning models or pro forma

models. In accounting jargon a “pro forma” statement is something that looks like an accounting

statement but that is forward looking. Financial planning models look like accounting

statements; however, whereas accounting statements report what happened to the firm in the

*

Notice: This is a preliminary draft of a chapter of Principles of Finance by Simon Benninga

(benninga@wharton.upenn.edu

). Check with the author before distributing this draft (though

you will probably get permission). Make sure the material is updated before distributing it. All

the material is copyright and the rights belong to the author and MIT Press.

PFE, Chapter 8: Financial planning models page 2

past, a financial planning model predicts what the firm’s accounting statements will look like in

the future.

Financial planning models have a variety of uses:

• Projecting future financing needs of the firm: Building a financial planning model helps

you predict whether the firm will need financing in the future. It also helps you tie the

firm’s financing needs to its future performance. For example—does an increase in the

growth rate of sales create cash or use cash? The answer is not always clear: More sales

produce more profits (and hence produce more cash). However, an increase in the

growth rate of sales may also require more capital investment (machines, land, etc.) and

may require greater net working capital. A financial planning model can help us sort out

these two opposing trends.

• Business plans: When you make a business plan (which you then take to investors to get

financing or to a bank to explain why you need a loan and can pay it back), you’ll often

need to build a pro forma model of your firm. The model you build illustrates your

assumptions about the financial and business environment in which your firm will

operate in the future. Valuation: They can be used to predict the future free cash flows,

dividends, and profits of a firm. Chapter 9 shows how to use the pro forma prediction of

future cash flows to value a firm.

In this chapter we develop a simple model that illustrates the methodology of financial

planning models. In the next chapter we will use a financial planning model to value the firm.

PFE, Chapter 8: Financial planning models page 3

Finance and accounting concepts used in this chapter

• This chapter assumes familiarity with the accounting concepts reviewed in Chapter 7.

• Net present value, present value

• Cash flows and free cash flows (FCF)

Excel concepts and functions used in this chapter

• Excel formulas and model building

• Relative versus absolute copying

• Circular references

• Data tables

8.1. Initial accounting statements for a financial planning model

Financial planning models are predictions of what a firm’s future financial statements

will look like. To build such a model we start with the present—the firm’s current financial

statements. To illustrate the process by which financial planning models are constructed, in the

next section we will project five years of financial statements for Whimsical Toenails, a

company which runs a chain of toenail-painting parlors. Whimsical’s management and bankers

want to project the firm’s future performance, and we will help them by constructing a financial

planning model.

Our starting point is Whimsical Toenail’s current income statement and balance sheet:

PFE, Chapter 8: Financial planning models page 4

WHIMSICAL TOENAILS

INITIAL INCOME STATEMENT

Sales 1,000

Cost of goods sold -500

Depreciation -100

Interest payments on debt -32

Interest earned on cash 6

Profit before tax 375

Taxes -150

Profit after tax 225

Dividends -90

Retained earnings 135

WHIMSICAL TOENAILS

INITIAL BALANCE SHEET

Assets Liabilities and equity

Cash 80 Current liabilities 80

Current assets 150 Debt 320

Fixed assets

Fixed assets at cost 1,070 Equity

Accumulated depreciation -300 Stock (paid-in capital) 450

Net fixed assets 770 Accumulated retained earnings 150

Total assets 1,000 Total liabilities and equity 1,000

Accounting terminology versus financial planning model terminology

Before proceeding further, some comments on our use of terminology. While most of the

terminology in this chapter follows the standard accounting nomenclature, some changes are

necessary to accommodate the structure of financial planning models. For example, while

accountants use “current assets” to denote both operating and financial short-term assets,

financial planning models use “current assets” to mean only operating short-term assets (to

emphasize this point, the terminology “operating current assets” is sometimes used). Similarly,

in the accounting framework “current liabilities” includes both operational items (like accounts

payable—bills which are as yet unpaid by the firm) and financial items (like short-term debt and

current portion of long term debt). Financial planning models use “current liabilities” to denote

PFE, Chapter 8: Financial planning models page 5

operational items. To emphasize this point, we sometimes use the terminology “operating

current liabilities.”

Current assets—what’s included in the financial planning model and what’s not?

In financial planning models the “current assets” category contains only items that are

related to the operations of the firm. Here are several typical items that would be included in the

financial planning model definition of current assets.

• Accounts receivable: These are payments due from customers and are generated by

the operations of the firm. Since accounts receivable are generated by the firm’s

sales, they are included in the operating current assets of the financial planning

model.

• Inventories: Inventories include both raw materials to be used for production and

unsold finished products. Inventories are part of the operating current assets of the

financial planning model.

• Prepaid expenses: Prepaid expenses are costs which the firm pays before it actually

receives the associated services. An example might be rent paid by the firm for future

periods: If the firm pays this rent in advance (for example, not month-by-month, but

6 months in advance), then this prepayment of the rent is recorded by the accountant

as a prepaid expense and is recorded as a current asset. For our financial planning

model, we usually assume that these are part of operating current assets.

Which accounting current assets are not included in the financial planning model

definition of current assets? There are two important examples:

PFE, Chapter 8: Financial planning models page 6

• Cash: The “cash” item on the balance sheet refers to money kept in the firm’s bank

accounts. Sometimes the accounting line item is called “cash and equivalents,” with the

second term denoting assets like certificates of deposit and money market accounts which

can be easily converted into cash. “Cash” is an operating current asset to the extent that it

is needed by the firm for its daily operations. In most cases, however, the cash accounts

on the balance sheets simply refer to non-operating assets which are kept in liquid form

by the firm.

• Marketable securities: This item on the balance sheet refers to other financial assets—

such as stocks and bonds—bought by the firm. Marketable securities are not needed for

the firm’s operations, and are thus not an operating current asset.

The distinction between cash as an operating asset and cash as a store of value is usually

obvious once you understand the business of the firm. A taxi driver needs to keep some cash on

hand in order to make change for his customers, and a supermarket needs to keep some cash in

the till for the same reason; in these cases at least some of the cash is an operating current asset

(although even for a taxi or supermarket, most of the cash is likely to be a financial, non-

operating current asset). On the other hand, in March 2003, Microsoft reported having $4.3

billion in cash and another $41.9 billion in marketable securities. It is unlikely that almost any of

this $46.2 billion is needed for daily operations. It is not an operating current asset, but rather a

financial current asset.