Jeanblanc M., Yor M., Chesney M. Mathematical Methods for Financial Markets

Подождите немного. Документ загружается.

450 7 Default Risk: An Enlargement of Filtration Approach

From Girsanov’s theorem (see Section 9.4), the processes

"

W and

"

M,

given by

"

W

t

= W

t

−

t

0

θ

u

du,

"

M

t

= M

t

−

t

0

1

{u<τ}

λ

u

ζ

u

du, (7.9.3)

are G-martingales under Q

1

. To ensure that Y

2,1

is a Q

1

-martingale, we have

to choose

θ

t

=

r

t

− μ

2,t

σ

2,t

.

For the process Y

3,1

to be a Q

1

-martingale, it is necessary and sufficient that

ζ satisfies

λ

t

ζ

t

= μ

3,t

− r

t

+ σ

3,t

r

t

− μ

2,t

σ

2,t

.

To ensure that Q

1

is a probability measure equivalent to P,werequirethat

ζ

t

> −1. The unique martingale measure Q

1

is then given by

L

t

= E

t

·

0

θ

u

dW

u

E

t

·

0

ζ

u

dM

u

.

Proposition 7.9.1.1 Assume that the process θ

t

=

r

t

−μ

2,t

σ

2,t

is bounded, and

ζ

t

=

1

λ

t

μ

3,t

− r

t

+ σ

3,t

r

t

− μ

2,t

σ

2,t

> −1. (7.9.4)

Then the market is arbitrage free and complete. The dynamics of the relative

prices under the unique martingale measure Q

1

are

dY

2,1

t

= Y

2,1

t

σ

2,t

d

"

W

t

,

dY

3,1

t

= Y

3,1

t−

σ

3,t

d

"

W

t

− d

"

M

t

.

This means that any Q

1

-integrable contingent claim Y = G(Y

2

T

,Y

3

T

; D

T

)

is attainable, and its arbitrage price equals

π

t

(Y )=R

−1

t

E(YR

T

|G

t

), ∀t ∈ [0,T] (7.9.5)

where R

t

=exp(−

t

0

r

s

ds).

7.9.2 PDE for Valuation

Since our goal is to develop the PDE approach, it will be essential to postulate

the Markovian property of our model. We assume that the coefficients μ

i

,σ

i

,λ

are regular functions of (t, Y

2

t

,Y

3

t

−

).

Lemma 7.9.2.1 The process (Y

1

,Y

2

,Y

3

,D) is a G-Markov process under

the martingale measure Q

1

. For any attainable claim Y = G(Y

1

T

,Y

2

T

,Y

3

T

; D

T

)

there exists a function C :[0,T] × R

3

×{0, 1}→R such that

π

t

(Y )=C(t, Y

1

t

,Y

2

t

,Y

3

t

; D

t

) .

7.9 PDE Approach for Hedging Defaultable Claims 451

Note that, since Y

1

T

is deterministic, up to a change of notation one

can restrict attention to claims of the form G(Y

2

T

,Y

3

T

; D

T

), the price of

which is C(t, Y

2

t

,Y

3

t

; D

t

). We find it convenient to introduce the pre-default

pricing function C(·;0) = C(t, y

2

,y

3

;0) and the post-default pricing function

C(·;1) = C(t, y

2

,y

3

; 1). In fact, since Y

3

t

=0ifD

t

= 1, it suffices to study

the post-default function C(t, y

2

;1)=C(t, y

2

, 0; 1). Also, we write

b =(r − μ

3

)σ

3

− (μ

3

− r)σ

2

.

Let λ>0 be the default intensity under P,andletζ>−1 be given by formula

(7.9.4) where we do not indicate the dependence on t. (In fact, b, σ, λ and ζ

are Markovian coefficients.) We denote by ∂

i

,i =1, 2 the partial derivative

with respect to y

i

.

Proposition 7.9.2.2 Assume that the functions C(·;0) and C(·;1) belong

to the class C

1,2

([0,T] × R

+

× R

+

, R).ThenC(t, y

2

,y

3

;0) satisfies the PDE

∂

t

C(·;0) + ry

2

∂

2

C(·;0)+(r + ζ)y

3

∂

3

C(·;0)+

1

2

3

i,j=2

σ

i

σ

j

y

i

y

j

∂

ij

C(·;0)

− rC(·;0)+

λ +

b

σ

2

C(t, y

2

;1)− C(t, y

2

,y

3

;0)

=0

subject to the terminal condition C(T,y

2

,y

3

;0) = G(y

2

,y

3

;0),andC(t, y

2

;1)

satisfies the PDE

∂

t

C(·;1)+ry

2

∂

2

C(·;1)+

1

2

σ

2

2

y

2

2

∂

22

C(·;1)− rC(·;1) = 0

subject to the terminal condition C(T,y

2

;1)=G(y

2

, 0; 1).

Proof: For simplicity, we write C

t

= π

t

(Y ). Let us define

ΔC(t, y

2

,y

3

)=C(t, y

2

;1)− C(t, y

2

,y

3

;0).

Then the jump ΔC

t

= C

t

− C

t−

can be represented as follows:

ΔC

t

= 1

{τ=t}

C(t, Y

2

t

;1)− C(t, Y

2

t

,Y

3

t

−

;0)

= 1

{τ=t}

ΔC(t, Y

2

t

,Y

3

t

−

).

We typically omit the variables (t, Y

2

t

−

,Y

3

t

−

,D

t

−

) in expressions ∂

t

C, ∂

i

C, ΔC,

etc. We shall also make use of the fact that for any Borel measurable function

g we have

t

0

g(u, Y

2

u

,Y

3

u

−

) du =

t

0

g(u, Y

2

u

,Y

3

u

) du

since Y

3

u

and Y

3

u

−

differ for at most one value of u (for each ω).

Let ξ

t

= 1

{t<τ}

λ

t

. An application of Itˆo’s formula yields

452 7 Default Risk: An Enlargement of Filtration Approach

dC

t

= ∂

t

Cdt+

3

i=2

∂

i

CdY

i

t

+

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

Cdt

+

ΔC + Y

3

t

−

∂

3

C

dD

t

= ∂

t

Cdt+

3

i=2

∂

i

CdY

i

t

+

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

Cdt

+

ΔC + Y

3

t

−

∂

3

C

dM

t

+ ξ

t

dt

,

and this in turn implies that

dC

t

= ∂

t

Cdt+

3

i=2

Y

i

t

∂

i

C

μ

i

dt + σ

i

dW

t

+

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

Cdt

+ ΔC dM

t

+

ΔC + Y

3

t

−

∂

3

C

ξ

t

dt

=

⎛

⎝

3

i=2

μ

i

Y

i

t

∂

i

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C +

ΔC + Y

3

t

∂

3

C

ξ

t

⎫

⎬

⎭

dt

+ ∂

t

C +

3

i=2

σ

i

Y

i

t

∂

i

C

dW

t

+ ΔC dM

t

.

We now use the integration by parts formula to derive dynamics of the relative

price

C

t

= C

t

(Y

1

t

)

−1

. We find that

Y

1

t

d

C

t

=

3

i=2

σ

i

Y

i

t

∂

i

CdW

t

+ ΔC dM

t

+(∂

t

C − rC

t

) dt

+

⎧

⎨

⎩

3

i=2

μ

i

Y

i

t

∂

i

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C +

ΔC + Y

3

t

∂

3

C

ξ

t

⎫

⎬

⎭

dt .

Hence, using (7.9.3), we obtain

Y

1

t

d

C

t

=

3

i=2

σ

i

Y

i

t

∂

i

Cd

"

W

t

+ ΔC d

"

M

t

− rC

t

dt + ∂

t

C

+

⎧

⎨

⎩

3

i=2

μ

i

Y

i

t

∂

i

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C +

ΔC + Y

3

t

∂

3

C

ξ

t

⎫

⎬

⎭

dt

+

3

i=2

σ

i

Y

i

t

θ∂

i

C + ζξ

t

ΔC − σ

1

3

i=2

σ

i

Y

i

t

∂

i

C

dt.

This means that the process

C admits the following decomposition under Q

1

7.9 PDE Approach for Hedging Defaultable Claims 453

Y

1

t

d

C

t

= −rC

t

dt +

3

i=2

σ

i

Y

i

t

θ∂

i

C + ζξ

t

ΔC + ∂

t

C

dt

+

⎛

⎝

3

i=2

μ

i

Y

i

t

∂

i

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C +

ΔC + Y

3

t

∂

3

C

ξ

t

⎞

⎠

dt

+ d(a Q

1

-martingale) .

From (7.9.5), it follows that the process

C is a martingale under Q

1

. Therefore,

the continuous finite variation part in the above decomposition necessarily

vanishes, and thus we get

0=−rC

t

+ ∂

t

C +

3

i=2

μ

i

Y

i

t

∂

i

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C

+

ΔC + Y

3

t

∂

3

C

ξ

t

+

3

i=2

σ

i

Y

i

t

θ∂

i

C + ζξ

t

ΔC .

Finally, we conclude that

∂

t

C + rY

2

t

∂

2

C +(r + ξ

t

) Y

3

t

∂

3

C +

1

2

3

i,j=2

σ

i

σ

j

Y

i

t

Y

j

t

∂

ij

C

− rC

t

+(1+ζ)ξ

t

ΔC =0.

Recall that ξ

t

= 1

{t<τ}

λ. It is thus clear that the pricing functions C(·, 0) and

C(·; 1) satisfy the PDEs given in the statement of the proposition.

Hedging Strategy

The next result provides a replicating strategy for Y .

Proposition 7.9.2.3 The replicating strategy φ for the claim Y is given by

the formulae

φ

3

t

Y

3

t−

= −ΔC(t, Y

2

t

,Y

3

t−

)=C(t, Y

2

t

,Y

3

t−

;0)− C(t, Y

2

t

;1),

φ

2

t

σ

2

Y

2

t

= σ

3

ΔC +

3

i=2

Y

i

t

σ

i

∂

i

C,

φ

1

t

Y

1

t

= C −φ

2

t

Y

2

t

− φ

3

t

Y

3

t

.

Proof: As a by-product of our previous computations, we obtain

d

C

t

=(Y

1

t

)

−1

3

i=2

σ

i

Y

i

t−

∂

i

Cd

"

W

t

+(Y

1

t

−

)

−1

ΔC d

"

M

t

.

454 7 Default Risk: An Enlargement of Filtration Approach

The self-financing strategy that replicates Y is determined by two components

φ

2

,φ

3

and the following relationship:

d

C

t

= φ

2

t

dY

2,1

t

+ φ

3

t

dY

3,1

t

= φ

2

t

Y

2,1

t

σ

2

d

"

W

t

+ φ

3

t

Y

3,1

t−

σ

3

d

"

W

t

− d

"

M

t

.

By identification, we obtain φ

3

t

Y

3,1

t−

=(Y

1

t

)

−1

ΔC and

φ

2

t

σ

2

Y

2

t

− σ

3

ΔC =

3

i=2

Y

i

t

−

σ

i

∂

i

C.

This yields the claimed formulae.

Corollary 7.9.2.4 In the case of a total default claim, the hedging strategy

satisfies the condition φ

1

t

Y

1

t

+ φ

2

t

Y

2

t

=0.

Proof: A total default corresponds to the assumption that G(y

2

,y

3

, 1) = 0.

We then have C(t, y

2

; 1) = 0, and thus φ

3

t

Y

3

t−

= C(t, Y

1

t

,Y

2

t

,Y

3

t−

; 0) for every

t ∈ [0,T]. Hence, the equality φ

1

t

Y

1

t

+ φ

2

t

Y

2

t

= 0 holds for every t ∈ [0,T]

and ensures that the wealth of a replicating portfolio jumps to zero at default

time.

7.9.3 General Case

Proposition 7.9.3.1 Let σ

2

=0and let Y

1

,Y

2

,Y

3

satisfy

dY

1

t

= rY

1

t

dt,

dY

2

t

= Y

2

t

μ

2

dt + σ

2

dW

t

,

dY

3

t

= Y

3

t

−

μ

3

dt + σ

3

dW

t

+ κ

3

dM

t

.

Assume that κ

3

=0,κ

3

> −1. The market is complete and arbitrage free if

and only if σ

2

(r − μ

3

)=σ

3

(r − μ

2

).

Proof: We leave this to the reader.

Corollary 7.9.3.2 In case of constant coefficients, the risk-neutral intensity

is equal to the historical intensity.

Proof: This follows from the determination of the unique risk-neutral

probability, which transforms the Brownian motion W into

"

W where

d

"

W

t

= W

t

−

μ

2

− r

σ

2

dt = W

t

−

μ

3

− r

σ

3

dt ,

but does not change the martingale M.

7.9 PDE Approach for Hedging Defaultable Claims 455

Proposition 7.9.3.3 The price of a contingent claim Y = G(Y

2

T

,Y

3

T

,D

T

)

can be represented as π

t

(Y )=C(t, Y

2

t

,Y

3

t

,D

t

), where the pricing functions

C(·;0) and C(·;1) satisfy the following PDEs:

∂

t

C(t, y

2

,y

3

;0) + ry

2

∂

2

C(t, y

2

,y

3

;0)+y

3

(r − κ

3

λ) ∂

3

C(t, y

2

,y

3

;0)

+

1

2

3

i,j=2

σ

i

σ

j

y

i

y

j

∂

ij

C(t, y

2

,y

3

;0)

+ λ

C(t, y

2

,y

3

(1 + κ

3

); 1) − C(t, y

2

,y

3

;0)

= rC(t, y

2

,y

3

;0)

and

∂

t

C(t, y

2

,y

3

;1)+ry

2

∂

2

C(t, y

2

,y

3

;1)+ry

3

∂

3

C(t, y

2

,y

3

;1)− rC(t, y

2

,y

3

;1)

+

1

2

3

i,j=2

σ

i

σ

j

y

i

y

j

∂

ij

C(t, y

2

,y

3

;1)=0

subject to the terminal conditions

C(T,y

2

,y

3

;0)=G(y

2

,y

3

;0),C(T,y

2

,y

3

;1)=G(y

2

,y

3

;1).

The replicating strategy φ comprises

φ

2

t

=

1

σ

2

Y

2

t

3

i=2

σ

i

y

i

∂

i

C(t, Y

2

t

,Y

3

t−

,D

t−

)

−

σ

3

σ

2

κ

3

Y

2

t

C(t, Y

2

t

,Y

3

t−

(1 + κ

3

); 1) − C(t, Y

2

t

,Y

3

t−

;0)

,

φ

3

t

=

1

κ

3

Y

3

t−

C(t, Y

2

t

,Y

3

t−

(1 + κ

3

); 1) − C(t, Y

2

t

,Y

3

t−

;0)

,

with φ

1

t

given by φ

1

t

Y

1

t

+ φ

2

t

Y

2

t

+ φ

3

t

Y

3

t

= C

t

.

Proof: This is obtained by lengthy computations, as in Proposition 7.9.2.2.

We leave the details to the reader.

Hedging of a Survival Claim

We shall illustrate Proposition 7.9.3.3 by means of an example. Consider a

survival claim of the form

Y = G(Y

2

T

,Y

3

T

,D

T

)=1

{T<τ}

g(Y

3

T

).

Then the post-default pricing function C

g

(·; 1) vanishes identically, and the

pre-default pricing function C

g

(·; 0) solves the PDE

456 7 Default Risk: An Enlargement of Filtration Approach

∂

t

C

g

(·;0)+ry

2

∂

2

C

g

(·;0)+y

3

(r − κ

3

λ) ∂

3

C

g

(·;0)

+

1

2

3

i,j=2

σ

i

σ

j

y

i

y

j

∂

ij

C

g

(·;0)− (r + λ)C

g

(·;0)=0

with the terminal condition C

g

(T,y

2

,y

3

;0)=g(y

3

). Denote α = r − κ

3

λ and

β = λ(1 + κ

3

).

It is not difficult to check that C

g

(t, y

2

,y

3

;0) = e

β(T −t)

C

α,g,3

(t, y

3

)isa

solution of the above equation, where the function w(t, y)=C

α,g,3

(t, y)isthe

solution of the standard Black and Scholes PDE

∂

t

w + yα∂

y

w +

1

2

σ

2

3

y

2

∂

yy

w − αw =0

with the terminal condition w(T,y)=g(y), that is, the price of the contingent

claim g(Y

T

) in the Black and Scholes framework with interest rate α and

volatility parameter equal to σ

3

.

Let C

t

be the current value of the contingent claim Y ,sothat

C

t

= 1

{t<τ}

e

β(T −t)

C

α,g,3

(t, Y

3

t

).

The hedging strategy of the survival claim is, on the event {t<τ},

φ

3

t

Y

3

t

= −

1

κ

3

e

−β(T −t)

C

α,g,3

(t, Y

3

t

)=−

1

κ

3

C

t

,

φ

2

t

Y

2

t

=

σ

3

σ

2

Y

3

t

e

−β(T −t)

∂

y

C

α,g,3

(t, Y

3

t

) − φ

3

t

Y

3

t

.

Obviously, there is no need for the strategy on the set {τ<t}.

8

Poisson Processes and Ruin Theory

We give in this chapter the main results on Poisson processes, which are

basic examples of jump processes. Despite their elementary properties they

are building blocks of jump process theory. We present various generalizations

such as inhomogeneous Poisson processes and compound Poisson processes.

These processes are not used to model financial prices, due to the simple

character of their jumps and are in practice mixed with Brownian motion, as

we shall present in Chapter 10. However, they represent the main model in

insurance theory. We end this chapter with two sections about point processes

and marked point processes.

The reader can refer to C¸inlar [188], Cocozza-Thivent [190], Karlin and

Taylor [515] and the last chapter in Shreve [795] for the study of standard

Poisson processes, to Br´emaud [124] for general Poisson processes, and to

Jacod and Shiryaev [471], Kallenberg [504], Kingman [523], Last and Brandt

[565], Neveu [669], Prigent [725] and Protter [727] for point processes, and to

Mikosch [651, 652] for applications.

8.1 Counting Processes and Stochastic Integrals

A counting process is a process which increases in unit steps at isolated

times and is constant between these times. It can be constructed as follows. Let

(T

n

,n≥ 0) be a sequence of random variables defined on the same probability

space (Ω,F, P) such that

T

0

=0,T

n

<T

n+1

for T

n

< ∞.

This sequence models the times when jumps occur. We define the family of

random variables, for t ≥ 0,

N

t

=

n if t ∈ [T

n

,T

n+1

[

+∞ otherwise,

M. Jeanblanc, M. Yor, M. Chesney, Mathematical Methods for Financial

Markets, Springer Finance, DOI 10.1007/978-1-84628-737-4

8,

c

Springer-Verlag London Limited 2009

457

458 8 Poisson Processes and Ruin Theory

or, equivalently,

N

t

=

n≥1

1

{T

n

≤t}

=

n≥0

n1

{T

n

≤t<T

n+1

}

,N

0

=0.

This counting process (N

t

,t≥ 0), associated with the sequence (T

n

,n≥ 0), is

increasing and right-continuous. We denote by N

t

−

the left-limit of N

s

when

s → t,s<tand by ΔN

s

= N

s

−N

s−

the jump process of N.Theexplosion

time is the r.v. T =sup

n

T

n

. In what follows, we reduce our attention to the

case T = ∞.

Let F be a given filtration. A counting process is F-adapted if and only if

the random variables (T

n

,n ≥ 1) are F-stopping times. In that case, for any

n,theset{N

t

≤ n} = {T

n+1

>t} belongs to F

t

.

The natural filtration of N denoted by F

N

where F

N

t

= σ(N

s

,s ≤ t)is

the smallest filtration F

N

which satisfies the usual hypotheses and such that

N is F

N

-adapted.

The stochastic integral

t

0

C

s

dN

s

is defined pathwise as a Stieltjes

integral for every bounded measurable process (not necessarily F

N

-adapted)

(C

t

,t≥ 0) by

(CN)

t

:=

t

0

C

s

dN

s

=

]0,t]

C

s

dN

s

:=

∞

n=1

C

T

n

1

{T

n

≤t}

.

We emphasize that the integral

t

0

C

s

dN

s

is here an integral over the time

interval ]0,t], where the upper limit t is included and the lower limit 0

excluded. This integral is finite since there is a finite number of jumps during

thetimeinterval]0,t]. We shall also write

t

0

C

s

dN

s

=

s≤t

C

s

ΔN

s

where the right-hand side contains only a finite number of non-zero terms. The

integral

∞

0

C

s

dN

s

is defined as

∞

0

C

s

dN

s

=

∞

n=1

C

T

n

, when the right-hand

side converges.

We shall also use the differential notation d(CN)

t

:=C

t

dN

t

.

We can associate a random measure to any counting process as follows.

For any Borel set Λ ⊂ R

+

, for any ω,set

μ(ω, Λ)=#{n ≥ 1:T

n

(ω) ∈ Λ}.

For any ω,themapΛ → μ(ω, Λ) defines a positive measure on R

+

. One can

note that μ(ω, dt)=

n

δ

T

n

(ω)

(dt).

8.2 Standard Poisson Process 459

The random variable N

t

canbewrittenas

N

t

(ω)=μ(ω,]0,t]) =

]0,t]

μ(ω, ds)

and the Stieltjes (or stochastic) integral as

t

0

C

s

dN

s

=

t

0

C

s

μ(ds).

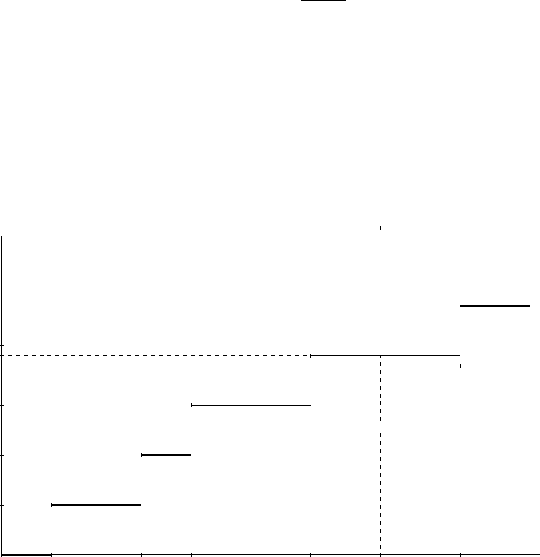

8.2 Standard Poisson Process

8.2.1 Definition and First Properties

The standard Poisson process is a counting process such that the random

variables (T

n+1

−T

n

,n≥ 0) are independent and identically distributed with

exponential law of parameter λ with λ>0. Hence, the explosion time is

infinite and

P(N

t

= n)=e

−λt

(λt)

n

n!

.

The standard Poisson process can be redefined as follows (see e.g., C¸ inlar

[188]): it is a counting process without explosion (i.e., T = ∞) such that

• for every s, t ≥ 0ther.v. N

t+s

− N

t

is independent of F

N

t

,

• for every s, t,ther.v.N

t+s

− N

t

has the same law as N

s

.

or, in an equivalent way, a counting process without explosion whose

increments are independent and stationary.

-

6

0

T

1

T

2

T

3

tT

4

T

5

1

2

3

N

t

=4

5

•

•

•

•

•

Fig. 8.1 Poisson process