Citibank: basic of corporate finance

Подождите немного. Документ загружается.

5-10 INTRODUCTION TO CAPITAL BUDGETING

v-1.1 v.05/13/94

p.01/14/00

Net Present Value of Cash Flows

The calculation for the present value of a series of cash flows may be

used to find out how much an investor will be willing to pay for an

investment. Because the investor has a specific required rate of return,

it is unlikely that a rational investor will pay more than the present

value for an investment.

Present value

minus initial

investment

The term net present value refers to an investor's position after

making an investment. To calculate the net present value of an

investment, we modify the present value formula by subtracting the

initial investment from the present value calculation.

T

NPV = Σ CF

t

[1/ (1 + R)]

t

– CF

0

t = 1

Where:

NPV = Net present value of the project or investment

T = Number of cash flows generated by the project

CF

t

= Cash flow in period t

CF

0

= Initial cash investment

R = Discount rate (required rate of return)

The original capital investment is often called the cash flow at

time 0 (or present time) and is represented by the symbol CF

0

. The

net present value (NPV) is equal to the sum of all the discounted

cash flows minus the original payment made in order to receive the

cash flows.

Positive /

Negative NPV

A positive NPV means that the investor paid less than the present

value for the stream of cash flows. A negative NPV means that the

investor paid more than the present value for the stream of cash

flows. An NPV equal to zero means that the investor paid the same

amount as the present value for the stream of cash flows.

www.LisAri.com

INTRODUCTION TO CAPITAL BUDGETING 5-11

v.05/13/94 v-1.1

p.01/14/00

Finding NPV

with a financial

calculator

Most financial calculators may be used to calculate NPV. The basic

idea is to input each cash flow in its proper order. Remember to input

the original capital investment (CF

0

) and any other cash outflows as

negative numbers. After inputting the positive and negative cash flows,

input the appropriate discount rate and then push the NPV key to find

the solution. Check the owner's manual for specific details.

Analyzing a

potential

project

Companies often calculate NPV to evaluate potential projects.

Analysts forecast the expected cash flows, discount the cash flows at

the appropriate rate, and subtract the estimated initial capital

investment. A project with a positive NPV creates value for the

shareholders of the company, whereas a project with a negative NPV

destroys value for the shareholders.

Independent

projects

Companies with limited funds to invest, and several potential

independent projects to evaluate, often rank the projects according

to NPV and then invest in those projects with the highest NPV. The

term "independent projects" means that a change in the cash flows in

one project has no effect on the cash flows in any other project —

each project is independent of all others being considered. The

concept of independence is important for making NPV decisions. For

a more thorough discussion on independent events, consult a

probability textbook.

An example will illustrate the use of the net present value formula to

evaluate a project.

www.LisAri.com

5-12 INTRODUCTION TO CAPITAL BUDGETING

v-1.1 v.05/13/94

p.01/14/00

Example

Project A requires a capital investment of $2,000 and promises a

payment of $1,000 at the end of Years One, Two, and Three. If the

investor's required rate of return is 12%, what is the NPV of the

investment? We can use the NPV formula with the values CF

1

, CF

2

,

and CF

3

= $1,000, CF

0

= $2,000, T = 3, and R = 0.12.

T

NPV = Σ CF

t

[1/ (1 + R)]

t

– CF

0

t = 1

NPV = $1,000[1 / (1.12)]

1

+ $1,000[1 / (1.12)]

2

+ $1,000[1 / (1.12)]

3

- $2,000

NPV = $1,000[0.8929] + $1,000[0.7972] + $1,000[0.7118] - $2,000

NPV = $401.83

Using the

financial

calculator

To solve for NPV with your financial calculator, enter each of the cash

flows and capital investments in their proper order. Enter the discount

rate of 12% and push the NPV key to get $401.83. Project A has a

positive net present value.

Analyzing

opportunity cost

for use of funds

Some analysts use net present value to determine if the cash flows are

sufficient to repay the capital investment plus an amount for the

opportunity cost of using the company's funds. A positive NPV means

that the project is able to repay the initial investment, pay the

opportunity cost for the use of the funds, and generate additional funds

that create value for the company; a negative NPV means that the

project cannot generate enough funds to cover the original investment

and the opportunity cost for the use of the funds.

Practice what you have learned about calculating the net present value of an investment by

completing the Practice Exercise that begins on page 5-13; then continue to the section

on "Internal Rate of Return."

www.LisAri.com

INTRODUCTION TO CAPITAL BUDGETING 5-13

v.05/13/94 v-1.1

p.01/14/00

PRACTICE EXERCISE 5.2

Directions: Calculate the answer to each question, then enter the correct answer.

Check your solution with the Answer Key on the next page.

4. A project has an initial investment of $10,000 and a cash flow annuity of $5,000

for three years. If the required rate of return is 10%, what is the NPV of the

project?

$_____________________

Should the project be accepted based on the NPV method of capital budgeting?

_____a) Yes

_____b) No

5. A project has an initial investment of $20,000 and a cash flow annuity of $5,000

for four years. If the required rate of return is 12%, what is the NPV of the project?

$_____________________

Should the project be accepted based on the NPV method of capital budgeting?

_____a) Yes

_____b) No

www.LisAri.com

5-14 INTRODUCTION TO CAPITAL BUDGETING

v-1.1 v.05/13/94

p.01/14/00

ANSWER KEY

4. A project has an initial investment of $10,000 and a cash flow annuity of $5,000

for three years. If the required rate of return is 10%, what is the NPV of the

project?

$2,434.26

Enter -$10,000 as CF

0

and three cash flows of $5,000

Enter 10% as the discount rate

Press the NPV key and you should get $2,434.26

Should the project be accepted based on the NPV method of capital budgeting?

Yes – The project should be accepted because its NPV is positive.

5. A project has an initial investment of $20,000 and a cash flow annuity of $5,000

for four years. If the required rate of return is 12%, what is the NPV of the project?

–$4,813.25

Enter -$20,000 as CF

0

and four cash flows of $5,000

Enter 12% as the discount rate

Press the NPV key and you should get -$4,813.25

Should the project be accepted based on the NPV method of capital budgeting?

No – The project should be rejected because its NPV is negative.

www.LisAri.com

INTRODUCTION TO CAPITAL BUDGETING 5-15

v.05/13/94 v-1.1

p.01/14/00

INTERNAL RATE OF RETURN

Actual rate of

return on

investment

The internal rate of return (IRR) is another calculation for

evaluating the value to shareholders of potential project investments.

The IRR represents the actual rate of return earned on an investment.

The idea of IRR is to find the discount rate that will make the net

present value of the cash flows equal to the initial investment. We

start with the NPV formula.

T

NPV = Σ CF

t

[1 / (1 + R)]

t

– CF

0

t = 1

To calculate the IRR, we set the NPV to 0 and solve for R (the internal

rate of return for the investment). As you can see, this can be very

difficult, especially if T (the number of cash flows) is quite large. The

formula looks like this:

T

O = Σ CF

t

[1 / (1 + R)]

t

– CF

0

t = 1

Finding IRR

with a financial

calculator

Most financial calculators can handle this calculation. The method is

to input the cash flows in the proper order (remember to enter CF

0

as

a negative number) and push the IRR key. Check your owner's manual

for the specifics.

Try the following example using your calculator.

Example

An investment requires an initial investment of $2,000 and will pay

$1,000 at the end of the next three years. Calculate the investment's

internal rate of return (IRR). Enter the cash flows into your

calculator, CF

0

= -$2,000 and CF

1

, CF

2

, and CF

3

= $1,000 each.

Now push the IRR key and you should get IRR = 23.38%.

www.LisAri.com

5-16 INTRODUCTION TO CAPITAL BUDGETING

v-1.1 v.05/13/94

p.01/14/00

Company's

required rate of

return

Many companies and analysts use IRR as an additional tool for making

investment decisions. They refer to a hurdle rate, which is the required

rate of return for a company or investor. A project that generates an

IRR which is greater than the hurdle rate will create value for the

shareholders. A project with an IRR that is less than the hurdle rate

will destroy shareholder value and should not be accepted.

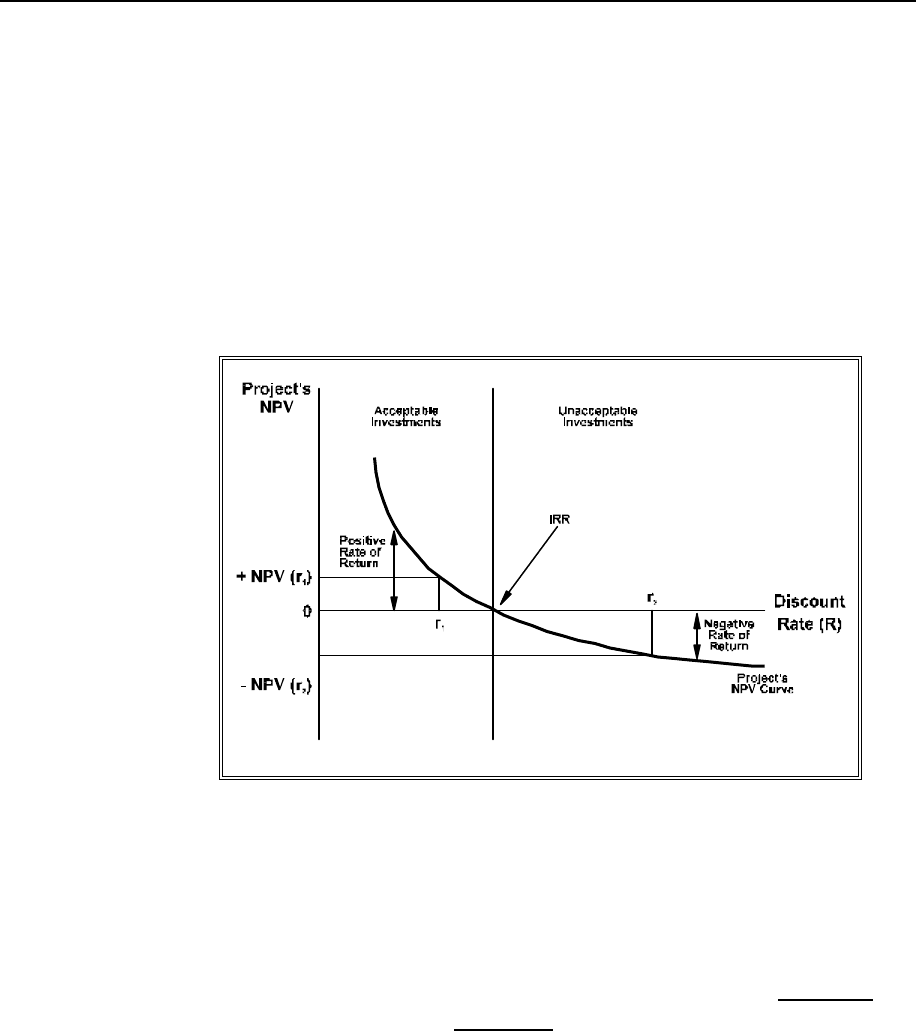

The diagram in Figure 5.1 illustrates the relationship of NPV to IRR.

Figure 5.1: Relationship of NPV to IRR

The vertical axis represents the net present value of the project; the

horizontal axis represents the discount rate (required rate of return)

for the investor. The curved bold line represents the NPV of the

project at different discount rates. As the discount rate increases,

the NPV of the project decreases. The point where the NPV of the

project equals zero (the curved line crosses the horizontal axis) is

the IRR of the project. Acceptable investments have a positive NPV

(above the horizontal axis) and unacceptable investments have a

negative NPV (below the horizontal axis).

www.LisAri.com

INTRODUCTION TO CAPITAL BUDGETING 5-17

v.05/13/94 v-1.1

p.01/14/00

Likewise, an investor with a required rate of return at r

1

will invest

in the project, because the IRR of the project is greater than the

required return. However, an investor with a required rate of return

at r

2

will not invest in the project because the IRR is less than the

hurdle rate.

An investment may have a different NPV curve for each company

doing the analysis, depending on each company's discount rate. This

means that a project may be acceptable for one company, but

unacceptable for another with a higher cost of funds.

Problems with

using IRR for

investment

decisions

Usually, the NPV and the IRR calculations produce the same accept/

reject decisions about investments. However, IRR does have some

problems if the required rate of return (or cost of funds) varies from

year to year. This situation requires a complicated weighted average

IRR. Also, if the cash flows for the project change from positive to

negative (meaning that additional investments are needed later in the

project) or vice-versa, the IRR becomes complicated to use. It is

conceivable that the NPV curve could cross the horizontal axis more

than once producing more than one internal rate of return. For these

reasons, net present value is considered superior to internal rate of

return for making investment decisions.

ADJUSTING NPV AND IRR FOR INFLATION

Cash flows may

change with

inflation

Calculating the net present value and internal rate of return for a

potential investment may require an adjustment for inflation. Actual

cash inflows and outflows may change considerably as inflation

changes. The variation may be large enough to change an invest/ don't

invest decision, especially if the inflation rate is high. Earlier, we

introduced a formula to convert a real, risk-free interest rate to a

nominal interest rate, based on a specific rate of inflation.

R

N

= R

R

+ h + ( h x R

R

)

www.LisAri.com

5-18 INTRODUCTION TO CAPITAL BUDGETING

v-1.1 v.05/13/94

p.01/14/00

Most of the time, analysts estimate future cash flows in nominal

terms and discount them with a nominal rate. The same result is

achieved by estimating future cash flows in real terms and

discounting them with a real discount rate. It is important to be

consistent – discount nominal cash flows with a nominal rate and

real cash flows with a real rate.

Another thing to consider is the effect of inflation on different types

of costs and benefits. One inflation rate may be appropriate for one

type of cost, but inappropriate for another type. Factor-specific

inflation indices may be used to overcome this problem. We only

mention this for your information; these types of considerations are

beyond the scope of this workbook.

OTHER METHODS FOR MAKING INVESTMENT DECISIONS

Payback Period

Time until cash

inflow equals

investment

In addition to the NPV and IRR calculations, there are several other

methods for gaining information that may be used when making capital

budgeting decisions. One popular method is to calculate the payback

period. The payback period is the time it takes for the cumulative cash

flow of a project to equal the initial investment.

Example

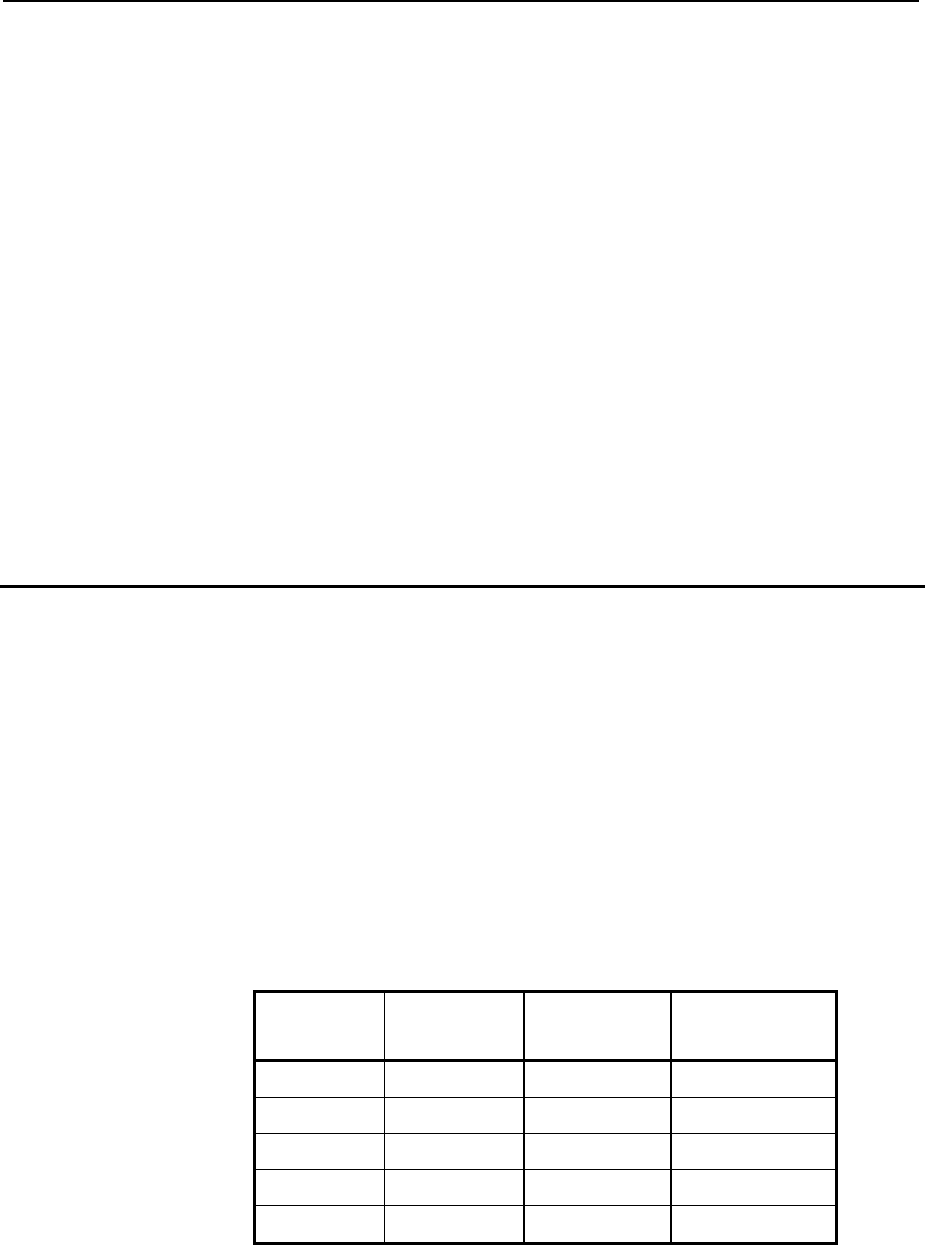

We can illustrate the concept of a payback period with an example. The

cash flows for a potential investment are listed in the table below:

Initial

Investment Cash Flow

Cumulative

Cash Flow

Year 0 $25,000 0 0

Year 1 $ 7,000 $ 7,000

Year 2 $ 9,000 $16,000

Year 3 $10,000 $26,000

Year 4 $13,000 $39,000

www.LisAri.com

INTRODUCTION TO CAPITAL BUDGETING 5-19

v.05/13/94 v-1.1

p.01/14/00

The investor expects to recover the initial investment of $25,000

sometime before the end of Year Three. The cumulative cash flow

at the end of Year Two is $16,000 and at the end of Year Three,

$26,000. Therefore, the payback period is more than two years but

less than three years.

We calculate the payback period by dividing the difference between the

initial investment and the cash flow in Year Two ($9,000) by the cash

flow in Year Three ($10,000) and adding the result to two years.

2 years + ($9,000/$10,000) = 2 + 0.9 = 2.9 years

Hurdle time for

payback period

The 2.9 years may also be expressed as 2 years and 47 weeks, by

multiplying 0.9 years by 52 weeks/year. Those companies that analyze

the payback period may have a hurdle time that must be met to invest in

the project. For example, if the investor in the example has a payback

hurdle of three years, s/he may consider investing in this project.

Problems with

payback period

methodology

The payback period methodology has some weaknesses. First, it does

not take into account the time value of money. Cash flows that will be

received in ten years are weighted the same as cash flows that will be

received in one year. Second, the payback period does not consider any

cash inflows that may occur after the hurdle time. A profitable

investment may be rejected because the cash flows will be received

after the hurdle time. Finally, it is often difficult to set an appropriate

hurdle time, especially if the cash flow pattern is not well-known to the

analyst.

The payback period methodology is a good beginning for analyzing a

potential investment, but it is not recommended as an analyst's key

tool for making investment decisions.

www.LisAri.com