CIMA CO2 Official Learning System - Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

REVISION QUESTIONS C2

580

Question 8

In connection with controls over accounting documents and records that would help to

prevent errors or fraud in the operation of the computerised ledger, complete the missing

words in these sentences:

(i) invoices relate to a properly authorised __________;

(ii) numbered __________ should be raised, for example by storekeeper, to ensure that

goods have been inspected and taken into stores;

(iii) adequate __________ of duties exists;

(iv) purchase ledger records should be checked against __________ statements.

(8 marks)

Question 9

At the year end of TD, an imbalance in the trial balance was revealed that resulted in the

creation of a suspense account with a credit balance of $1,040.

Investigations revealed the following errors:

(i) A sale of goods on credit for $1,000 had been omitted from the sales account.

(ii) Delivery and installation costs of $240 on a new item of plant had been recorded as a

revenue expense.

(iii) Cash discount of $150 on paying a supplier, JW, had been taken, even though the

payment was made outside the time limit.

(iv) Inventories of stationery at the end of the period of $240 had been ignored.

(v) A purchase of raw materials of $350 had been recorded in the purchases account as

$850.

(vi) The purchase returns daybook included a sales credit note for $230 that had been

entered correctly in the account of the receivable concerned, but included with pur-

chase returns in the nominal ledger.

Requirements

(a) Insert the missing items into the table below to show the journal entries required to

correct each of the above errors.

Item Account name Debit Credit

$ $

(i)

(ii)

(iii)

(iv)

(v)

(vi)

(12 marks)

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

581

FUNDAMENTALS OF FINANCIAL ACCOUNTING

(b) Insert the missing items into the suspense account given below to show the correc-

tions to be made.

Suspense account

$ $

(3 marks)

(c) Prior to the discovery of the errors, TD’s gross profi t for the year was calculated at

$35,750 and the net profi t for the year at $18,500.

Insert the missing items below in order to calculate the revised gross and net profi t

fi gures after the correction of the errors.

$

Gross profi t – original 35,750

Add/less *:

Add/less *:

Add/less *:

Revised gross profi t

Net profi t – original 18,500

Add/less *:

Add/less *:

Add/less *:

Add/less *:

Revised net profi t

(5 marks)

(Total marks 20)

Question 10

ARH plc has the following results for the last 2 years of trading:

Income statement of ARH plc

For the year ended 31.12.X4 31.12.9X5

$’000 $’000

Sales 14,400 17,000

Less : cost of sales (11,800) (12,600)

Gross profi t 2,600 4,400

Less : expenses (1,200) (2,000)

Operating profi t 1,400 2,400

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

REVISION QUESTIONS C2

582

Statement of changes in equity of ARH plc

For the year ended 31.12.X4 31.12.X5

Retained earnings start of period 320 1,200

Total comprehensive income for the period 1,400 2,400

Dividends paid (520) (780)

Retained earnings end of period 1,200 2,820

Statement of fi nancial position of ARH plc

At 31 December At 31 December

20X4 20X5

Assets $’000 $’000 $’000 $’000

Non-current assets 2,500 4,000

Current assets

Inventories 1,300 2,000

Receivables 2,000 1,600

Bank balances 2,400 820

5,700 4,420

8,200 8,420

Equity and liabilities

2.4 million ordinary shares of $1 each 2,400 2,400

Revaluation reserves 500 500

Retained earnings 1,200 2,820

4,100 5,720

Non-current liabilities

10% debentures 2,600 –

Current liabilities

Payables 1,500 2,700

8,200 8,420

Requirements

Calculate for 20X4 and 20X5 the:

(i) gross profi t margin,

(ii) operating profi t margin,

(iii) return on capital employed (ROCE), using average capital.

(6 marks)

Question 11

(a) You are given the following details regarding inventory movements during April

20X6:

1 Apr. 100 units on hand, cost $10 each

8 Apr. Inventory sold for $360, with a mark-up of 50%

18 Apr. 38 units purchased for $480 less trade discount of 5%

20 Apr. 50 units sold

23 Apr. 35 units sold

28 Apr. 20 units purchased for $260

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

583

FUNDAMENTALS OF FINANCIAL ACCOUNTING

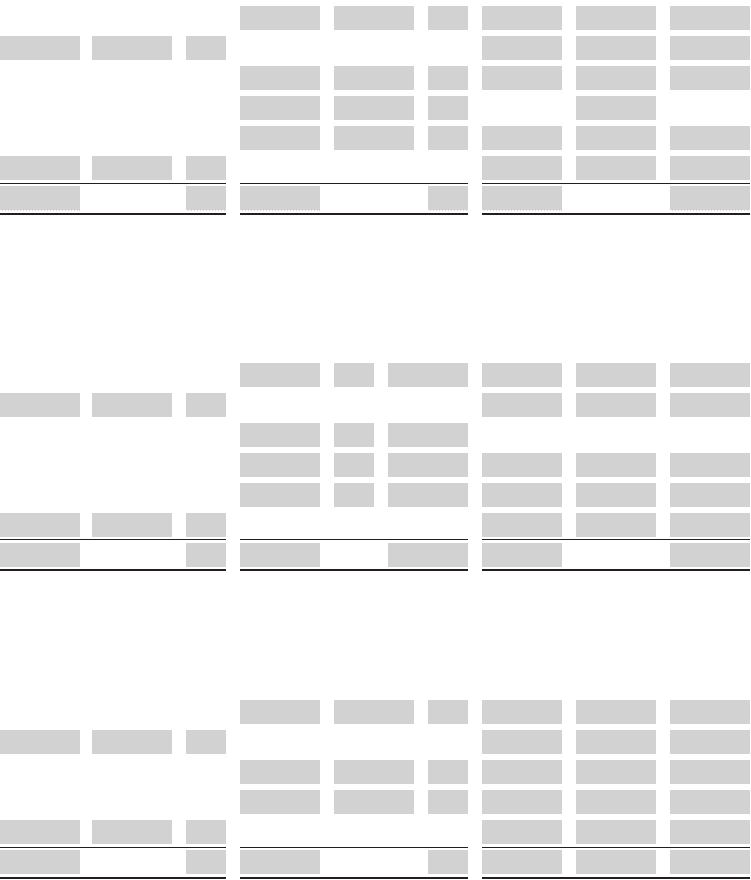

You are required to insert the missing items into the inventory record cards given below,

using the fi rst in, fi rst out (FIFO), last in, fi rst out (LIFO) and average cost (AVCO) cost

formulas, in order to determine the quantity and cost of closing inventory at 30 April 20X6.

Inventory record card – FIFO

Receipts Issues Balance

Date Units $/unit $ Units $/unit $ Units $/unit $

1 Apr. 100 10 1000

8 A p r .

18 Apr.

20 Apr.

2 3 A p r .

28 Apr.

Totals

Inventory record card – LIFO

Receipts Issues Balance

Date Units $/unit $ Units $/

unit

$ Units $/unit $

1 Apr. 100 10 1,000

8 A p r .

18 Apr.

20 Apr.

2 3 A p r .

28 Apr.

Totals

Inventory record card – AVCO

Receipts Issues Balance

Date Units $/unit $ Units $/unit $ Units $/unit $

1 Apr. 100 1,000

8 A p r .

18 Apr.

20 Apr.

2 3 A p r .

28 Apr.

Totals

(10 marks)

(b) If the physical inventory count carried out at 30 April revealed a closing inventory quan-

tity of 50 units, which of the following could be possible reasons for the discrepancy.

(i) Recording of an issue at too high a level

(ii) Recording of a receipt at too high a level

(iii) Recording of a receipt at too low a level

(iv) Recording of an issue at too low a level.

(2 marks)

(Total marks 12)

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

REVISION QUESTIONS C2

584

Question 12

The directors of R Ltd are hoping to negotiate an overdraft to provide working capital for

a proposed expansion of business. The bank manager has called for fi nancial statements for

the last 3 years and the directors have produced the following extracts:

Statements of fi nancial position as at 31 December

20X4 20X5 20X6

$’000 $’000 $’000 $’000 $’000 $’000

Non-current assets 147 163 153

Current assets

Inventories 27 40 46

Receivables 40 45 52

Bank 6 15 8

73 100 106

146 200 212

293 363 365

Current liabilities

(including tax) 33 45 43

20X4 ($’000) 20X5 ($’000) 20X6 ($’000)

Credit sales 360 375 390

Credit purchases 230 250 280

P r o fi t before tax 32 46 14

The bank manager has obtained the following additional information:

(i) The company commenced on 1 January 20X4 with an issued capital of 100,000 $1

ordinary shares issued at a premium of 60¢ each.

(ii) Income tax amounted to $5,000 in 20X5 and $6,000 in 20X6. There was no income

tax for 20X4.

(iii) Dividends paid were of 5¢ per share in 20X4, and 10¢ per share in each of 20X5 and

20X6.

(iv) $18,000 was transferred to general reserves in 20X5.

Requirements

(a) Insert the missing items into the table below to show the income statement for each

of the 3 years.

20X4 20X5 20X6

$’000 $’000 $’000

(3 marks)

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

585

FUNDAMENTALS OF FINANCIAL ACCOUNTING

(b) Insert the missing items into the table below to show the statement of changes in

equity for each of the 3 years.

20X4 20X5 20X6

$’000 $’000 $’000

Gen. res

Retained

earnings Gen. Res

Retained

earnings Gen. Res

Retained

earnings

Balance at start of period

(3 marks)

(c) Insert the missing items into the table below to show the capital section of the state-

ment of fi nancial position for each of the 3 years.

Description 20X4 ($’000) 20X5 ($’000) 20X6 ($’000)

Totals

(4 marks)

(d) (i) The formula for receivables days is:

(ii) The receivables days in each of the 3 years is:

For 20X4: days

For 20X5: days

For 20X6: days

(iii) The formula for payables days is:

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

REVISION QUESTIONS C2

586

(iv) The payables days in each of the 3 years is ( Note : remember to exclude taxation

from payables):

For 20X4: days

For 20X5: days

For 20X6: days

(6 marks)

(e) Deleting text as appropriate, complete the following paragraph, which discusses how

the above changes in receivables and payables days might affect the proposed overdraft.

The company appears to be increasing/decreasing the length of credit given to customers,

which slows down/speeds up the receipt of cash. At the same time it is increasing/decreasing

the length of credit from suppliers, which slows down/speeds up the payment of cash. These

two actions combined will cause the amount of cash available to increase/decrease . If these

payment periods could be brought more into line with each other, the amount of overdraft

required will be higher/lower .

(6 marks)

(Total marks 22)

Question 13

APW Ltd has the following trial balance at 30 April 20X8:

Debit ($’000) Credit ($’000)

Ordinary shares, 50¢ each 1,500

Irredeemable preference shares, 7% 400

Share premium account 200

Retained earnings at 1 May 20X7 580

8% debentures 500

Buildings – at valuation 3,500

Buildings – accumulated depreciation at 1 May 20X7 1,300

Factory plant – cost 1,200

Factory plant – accumulated depreciation at 1 May 20X7 200

O f fi ce equipment – cost 250

O f fi ce equipment – accumulated depreciation at 1 May 20X7 50

Delivery vehicles – cost 600

Delivery vehicles – accumulated depreciation at 1 May 20X7 360

Inventories at 1 May 20X7

Raw materials 234

Work in progress 182

Finished goods 98

Receivables and payables 136 124

Sales tax account 74

Employees ’ income tax and social security tax payable 62

Bank 248

Sales 2,660

Purchases of raw materials 785

Carriage outwards 20

Carriage inwards 40

Returns 104 65

Direct labour 372

Indirect factory labour 118

O f fi ce salaries 130

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

587

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Indirect factory overheads 63

Heat, light and power 120

Rent and insurance 130

Administration expenses 55

Debenture interest 20

Dividends paid – preference 28

Dividends paid – ordinary 140

Bank interest received 12

Bank charges 10

8,335 8,335

You are given the following information at 30 April 20X8:

(i) Inventories are as follows:

Raw materials $256,000

Work in progress $118,000

Finished goods $123,000

You ascertain that fi nished goods consist of three products:

Product Cost included in above valuation ($) Net realisable value ($)

Alpha 71,000 75,000

Beta 31,000 23,000

Delta 21,000 23,000

(ii) Depreciation is to be calculated as follows:

Buildings 5% on valuation (of which 40% is to be apportioned

to the factory)

Factory plant 10% on cost

O f fi ce equipment 20% on the reducing balance

Delivery vehicles 20% on cost

(iii) Wages and salaries costs accrued are:

Direct labour ($) Indirect factory labour ($) Offi ce salaries ($)

Gross wages 34,000 14,000 25,000

Employees ’ income 6,700 2,800 3,900

Tax and social

security deducted

Employer’s social 3,000 1,000 2,000

security tax

(iv) Income tax of $80,000 for the year is to be accrued.

(v) Heat, light and power accrued amounts to $15,000. Forty per cent of heat, light and

power is to be apportioned to the factory.

(vi) Rent and insurance prepaid amounts to $10,000. Thirty per cent of rent and insur-

ance is to be apportioned to the factory.

(vii) The debentures were issued in 20X4, and are due for repayment in 20Y4.

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

REVISION QUESTIONS C2

588

Requirements

(a) Insert the missing items in the income statement for the year ended 30 April 20X8.

Income statement of APW Ltd for the year ended 30 April 20X8

$’000 $’000 $’000 $’000

Sales

Opening inventories of fi nished goods

Opening inventories of raw material

Prime cost

Cost of production transferred to

fi nished goods inventories

Gross profi t

PREPARING FOR THE COMPUTER-BASED ASSESSMENTS (CBAs)

589

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Operating profi t

P r o fi t before tax

(10 marks)

(b) Insert the missing items in the statement of changes in equity for the year ended

30 April 20X8.

Statement of changes in equity of APW Ltd for the year ended 30 April 20X8

Retained Earnings

Balance at start of period

(13 marks)

(c) Which are the two principal accounting conventions that affect the valuation of

inventories.

(i) _____________________________________________________

(ii) _____________________________________________________

(7 marks)

(Total marks 30)