CIMA - C3 Fundamentals Of Business Mathematics

Подождите немного. Документ загружается.

370 Answer bank

(iii) P(None owned) = (1 – P(H)) (1 – P(C)) (1 – P(TV))

= 0.5

× 0.4 × 0.1

= 0.02

(d) (i)

40%

(ii)

66.67%

Workings

Out of every 100 respondents, 50 own their own homes and 50 do not. This gives the bottom row of

the contingency table shown below. Similarly the total column is determined by the 60% of

respondents who own cars. Of the 50 home owners, 40 people (80%

× 50) also own cars. The table

can now be completed as follows.

Home owner

Not home owner

Total

Car

40

20

60

No car

10

30

40

Total

50

50

100

(i) Of the 50 respondents who do not own homes, only 20 own cars = 20/50

× 100% = 40%

(ii) Of the 60 who own cars, only 40 are home owners = 40/60

× 100% = 66.7%

53 B Expected profit = (15,000

× 0.2) + (19,000 × 0.6) + (–1,000 × 0.1)

= 3,000 + 11,400 – 100

= $14,300

If you selected option A, you have totalled all profits.

If you selected option C, you have selected the option with the highest probability.

If you selected option D, you have averaged the profits without using the probabilities.

54 B The diagram is a Venn diagram illustrating two mutually exclusive outcomes.

55 D The rule of addition for two events which are not mutually exclusive = P(A or B)

= P(A) + P(B)

– P(A and B)

If you selected option A, this is the rule of addition for two mutually exclusive events.

Option B is the simple multiplication or AND law.

56 C I, II and III are limitations of expected values.

57 A =

1

B =

6

C =

128

Answer bank 371

Workings

Red

Yellow

Green

Total

Good

25 – 1 = 24

50 – 6 = 44

75 – 15 = 60

128

Faulty

4%

× 25 = 1

12%

× 50 = 6

20% × 75 = 15

22

Total

25

50

75

150

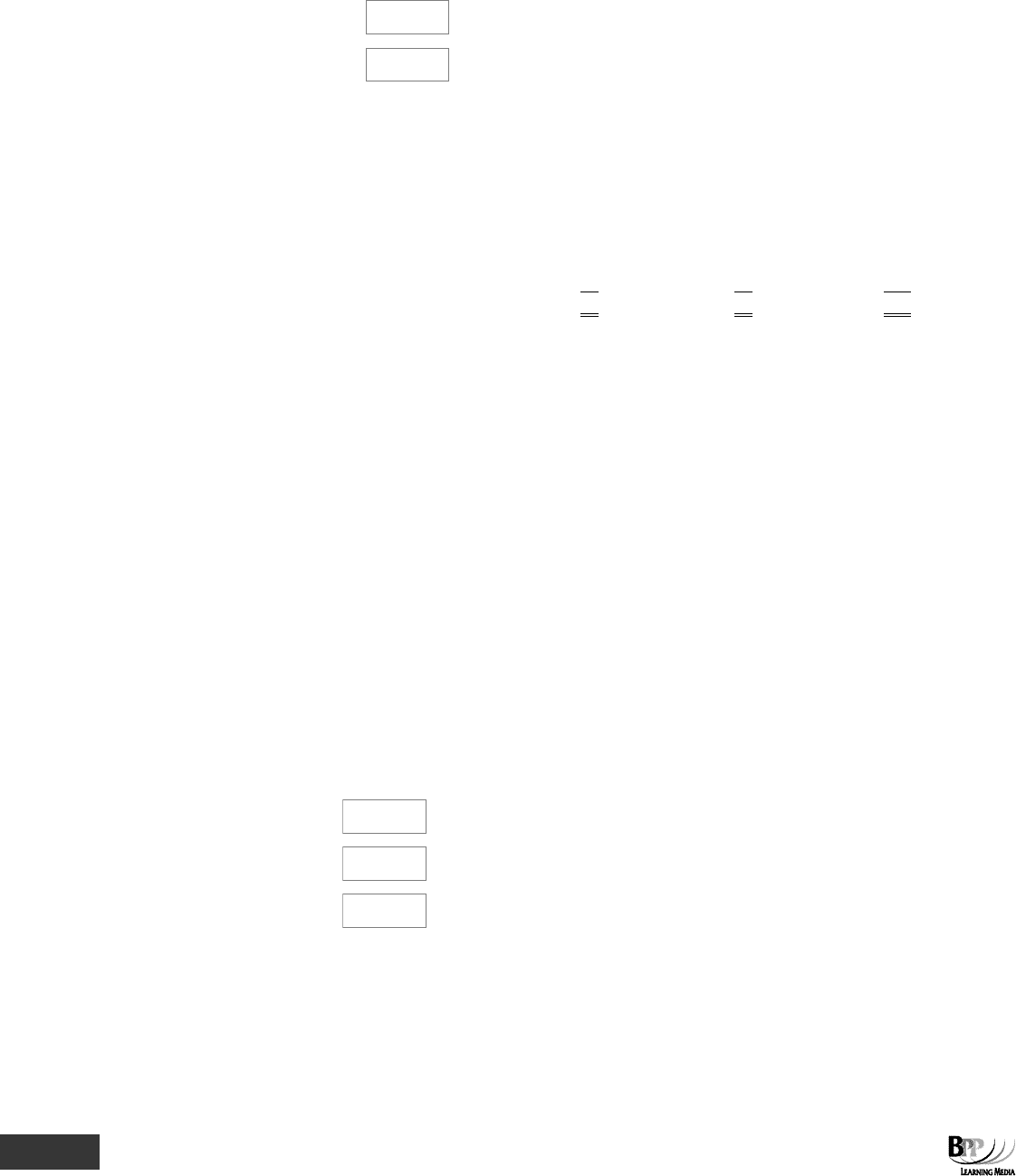

58 D

Pr(elephants weigh between 5,200 kg and 6,000 kg) = 0.5 – 0.0314

= 0.4686

From normal distribution tables, 0.4686 corresponds to a z value of 1.86.

If z =

σ

μx −

1.86 =

σ

200,5000,6 −

σ =

86.1

200,5000,6 −

= 430 kg

The correct answer is therefore D.

Make sure that you draw a sketch of the area that you are interested in when answering an objective

test question such as this. It will help to clarify exactly what you are trying to do.

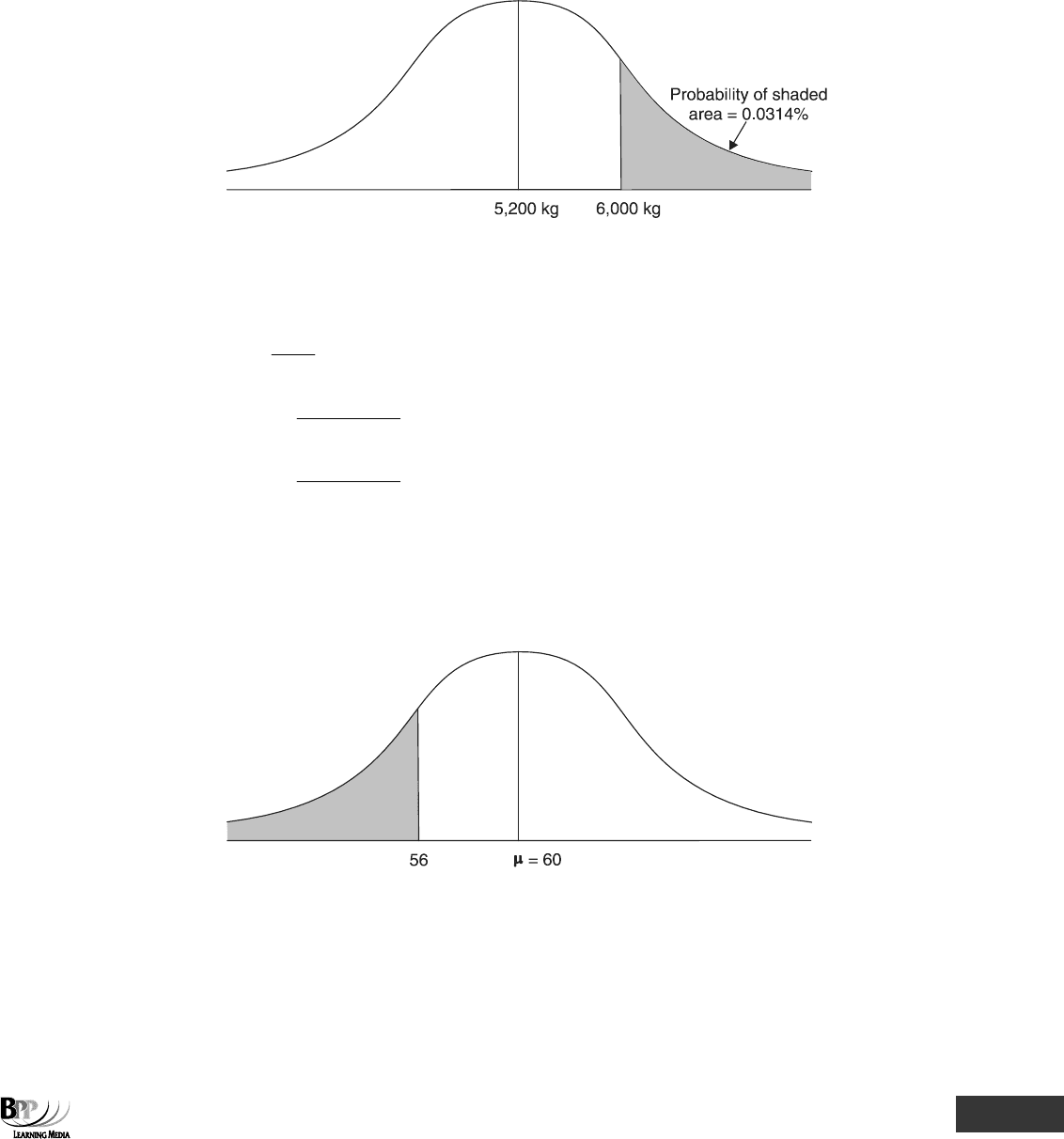

59 D

We are interested in the shaded area of the graph above, which we can calculate using normal

distribution tables.

372 Answer bank

z =

σ

μ−x

=

8.3

6056 −

= 1.05

A z value of 1.05 corresponds to a probability of 0.3531.

The shaded area has a corresponding probability of 0.5 – 0.3531 = 0.1469 or 0.15 or 15%.

Option A is incorrect because it represents the probability of getting a score of 56 or more.

Option B represents the probability of getting a score of 60 or less, ie 50% (the mean represents the

point below which 50% of the population lie and above which 50% of the population lie).

If you selected option C, you forgot to deduct your answer from 0.5.

60 D 28.23% of the population lies between 900 and the mean. Therefore 0.2823 corresponds to a z value

of 0.78 (from normal distribution tables).

If z =

σ

μx −

0.78 =

90

900 μ−

0.78 × 90 = 900 – μ

70.2 = 900 – μ

μ = 900 – 70.2

= 829.8 or 830

Draw a sketch of the area we are concerned with in this question if you had difficulty understanding the

answer.

61 A

We need to find the point z standard deviations above the mean such that 20% of the frequencies

are above it and 30% (50% – 20%) of the frequencies lie between the point z and the mean.

From normal distribution tables, it can be seen that 30% of frequencies lie between the mean and

the point 0.84 standard deviations from the mean.

Answer bank 373

If z =

σ

μx −

0.84 =

600,1

200x −

=

40

200x −

33.6 = x – 200

x = 200 + 33.6

= 233.6 or 234 (to the nearest whole number)

If you selected option B, you incorrectly added one standard deviation to the mean instead of 0.84

standard deviations.

If you selected option C you have added 1.28 standard deviations to the mean instead of 0.84

standard deviations.

If you selected option D, you have found 200 + (1.96 × 40) which accounts for 47.5% of the area

from 200 to point z.

62 (a)

1

(b)

2

+

3

(c)

4

(d)

2

+

3

+

4

=

2

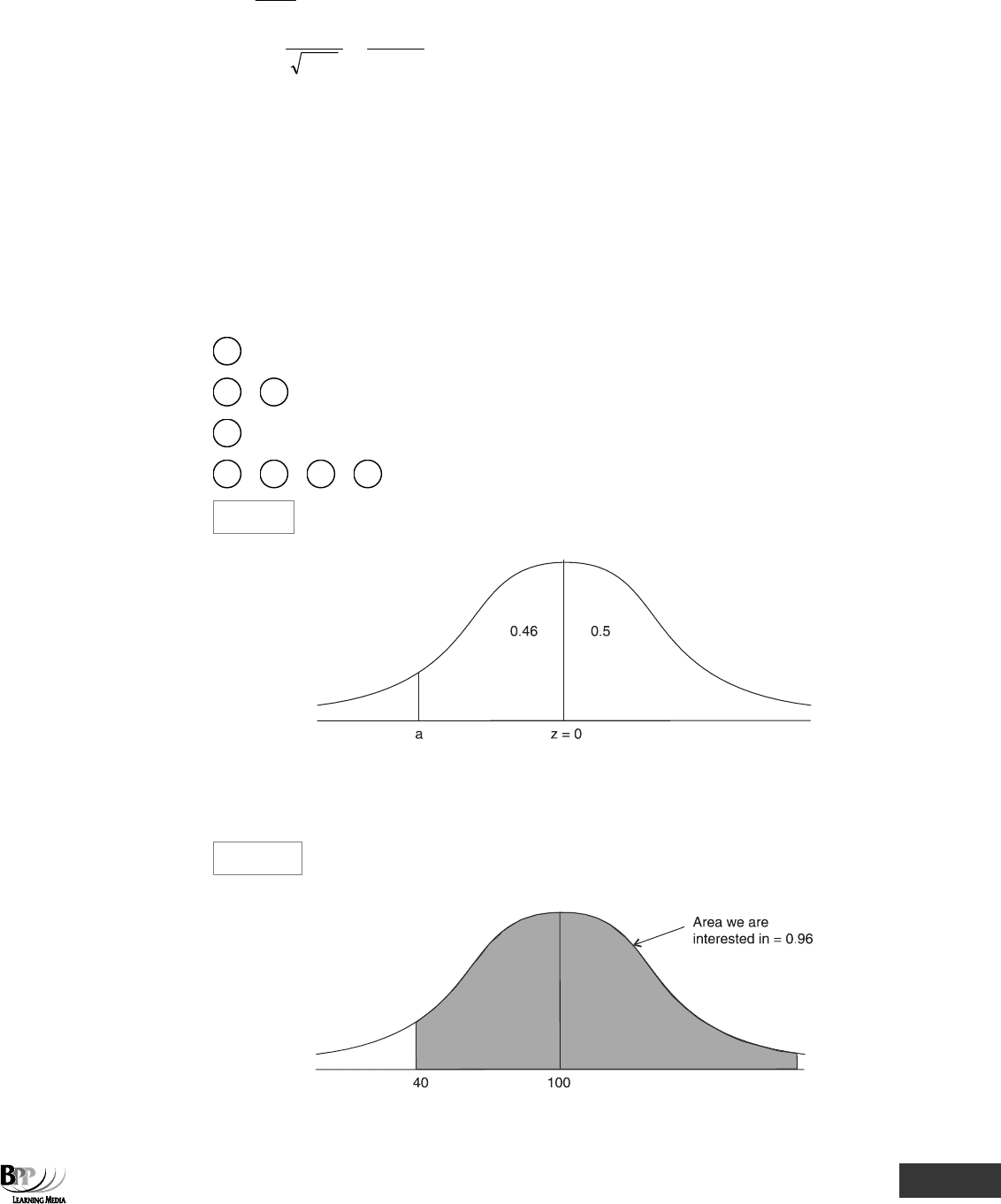

+ 0.5

63 (a)

–1.75

Working

The normal distribution graph above shows the point a above which 96% of the population lies.

Normal distribution tables show that, a z value of 1.75 corresponds to a probability of 0.46. Since a

is less than 0, its value is –1.75.

(b)

34.3 hours

Working

374 Answer bank

Using z =

σ

μx −

where z = 1.75

x = 40

μ = 100

1.75 =

σ

− 10040

σ =

75.1

10040 −

= 34.3 hours (to 1 decimal place)

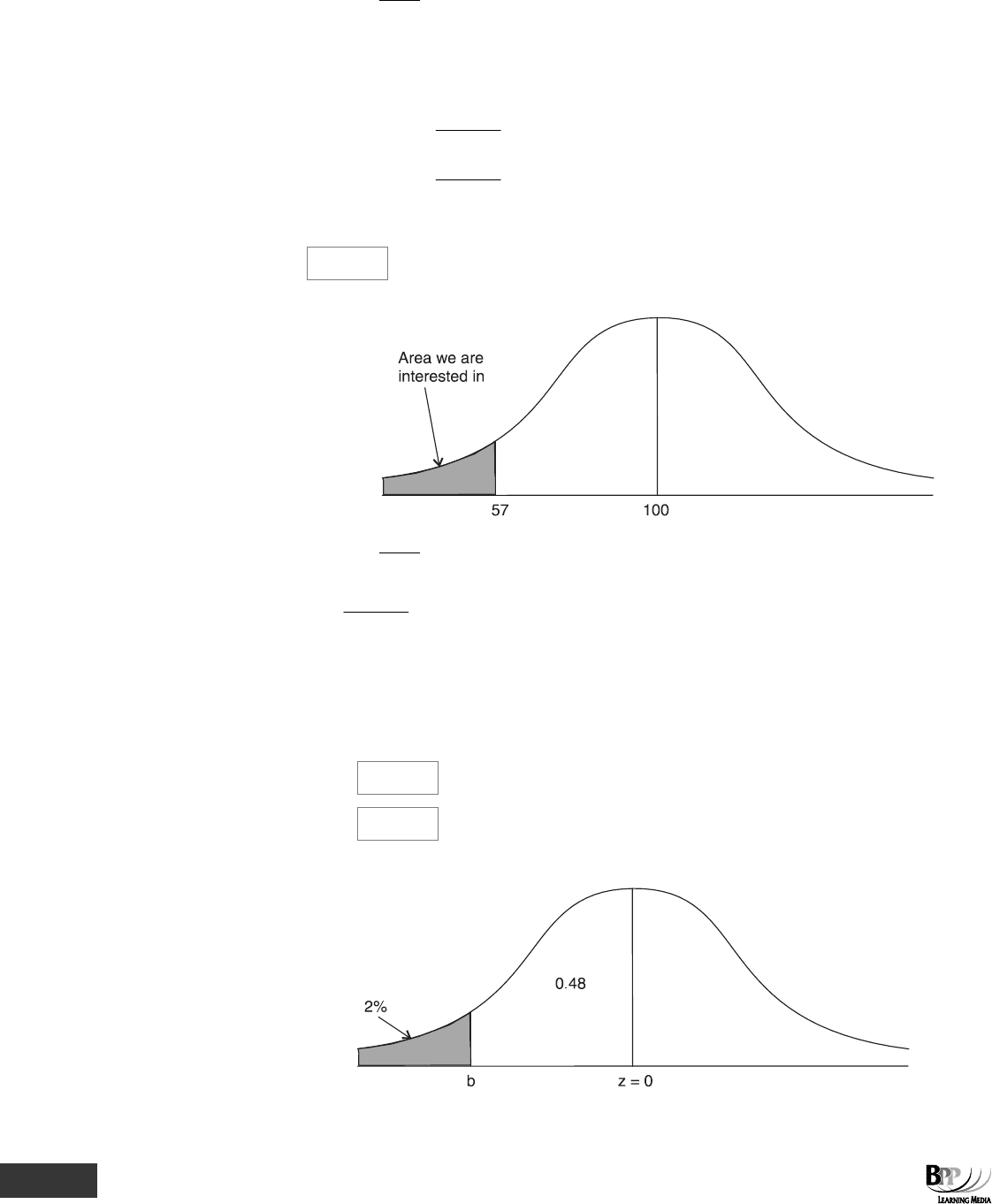

(c)

10.6%

Working

Using z =

σ

μ−x

z =

3.34

10057 −

z = 1.25

When z = 1.25, the proportion of batteries lasting between 57 and 100 hours is 0.3944 (from normal

distribution tables). The area that we are interested in is the area to the left of 57 hours (shaded area

on the graph) = 0.5 – 0.3944 = 0.1056 = 10.6% (to 1 decimal place).

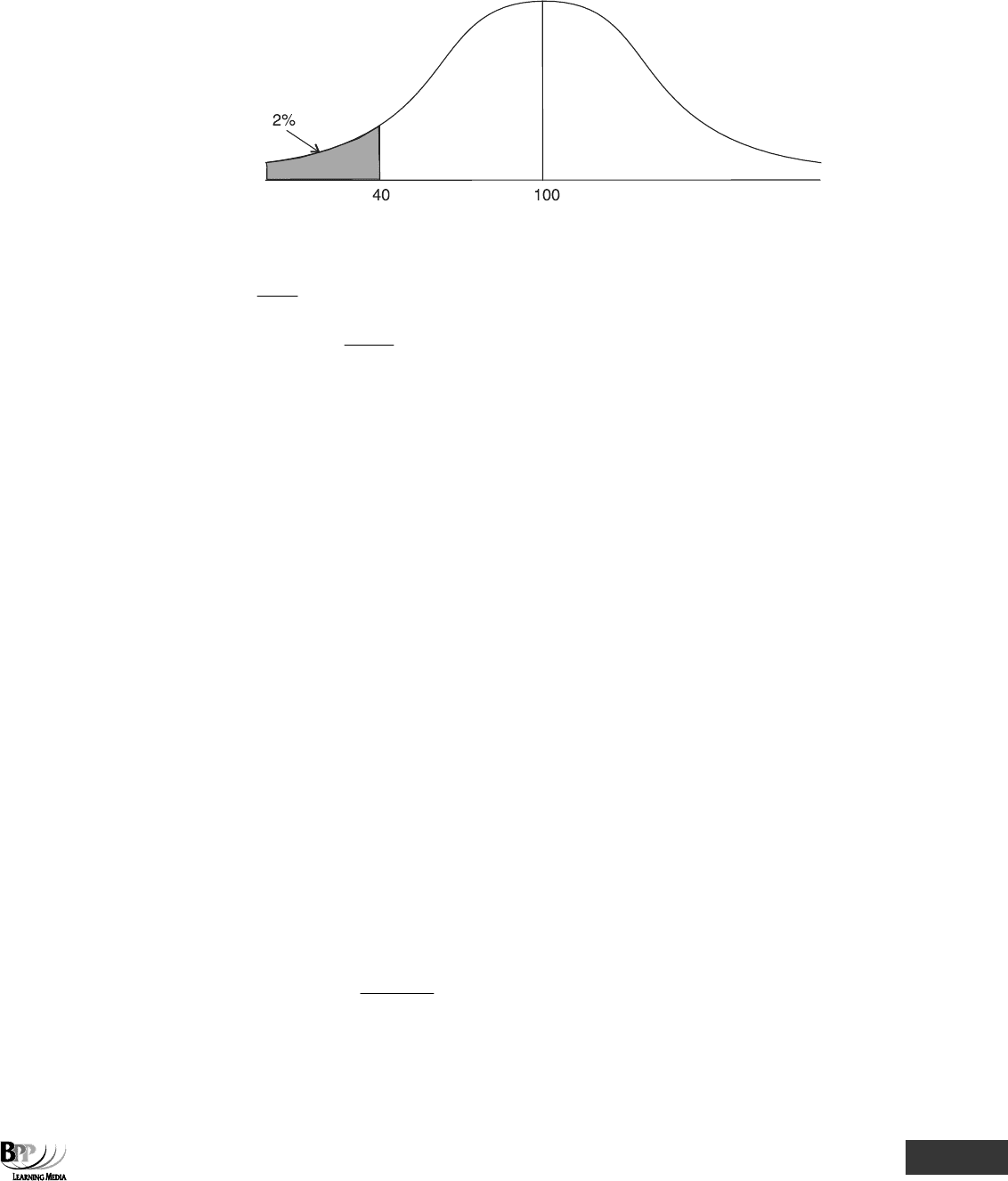

(d) (i)

–2.05

(ii)

111.8

Workings

(1)

Answer bank 375

The area between b and 0 = 48% (0.48), and so from normal distribution tables, the value of

b shown in the graph above is –2.05.

(2)

We want 2% of batteries to last for less than 40 hours. From normal distribution tables, this

corresponds to a z value of –2.05.

If z =

σ

μ−x

–2.05 =

35

40 μ−

(–2.05 × 35) = 40 – μ

–71.75 = 40 – μ

μ = 40 + 71.75

= 111.75

= 111.8 (to 1 decimal place

64 C S = X + nrX

= $2,000 + (8 × 0.12 × $2,000)

= $2,000 + $1,920

= $3,920

If you selected option A, you calculated the interest element only and forgot to add on the original

capital value.

If you selected option B, you used n = 7 instead of n = 8.

If you selected option D, you used the compound interest formula instead of the simple interest

formula.

65 B If S = X + nrX

S – X = nrX (note S – X = interest element)

$1,548 – $900 = nrX

4 years = 4 × 12 = 48 months = n

∴ $648 = 48 r × $900

∴ r =

900£48

648£

×

r = 0.015 or 1.5%

If you selected option C, you misinterpreted 0.015 as 15% instead of 1.5%.

376 Answer bank

If you selected option D, you calculated the annual rate of interest instead of the monthly rate.

66 C $3,000 = 120% of the original investment

∴ Original investment =

120

100

× $3,000

= $2,500

∴ Interest = $3,000 – $2,500

= $500

Make sure that you always tackle this type of question by establishing what the original investment

was first.

If you selected option D, you simply calculated 20% of $3,000 which is incorrect.

67 C If a cost declines by 8% per annum on a compound basis, then at the end of the first year it will be

worth 0.92 the original value.

Now = $12,000

End of year 1 = $12,000 × 0.92

End of year 2 = $12,000 × 0.92

2

End of year 3 = $12,000 × 0.92

3

∴ At the end of year 3, $12,000 will be worth

$12,000 × (0.92)

3

= $9,344

If you selected option A, you calculated the value after four years, not three.

If you selected option B, you have assumed that the cost will decline by 8% × 3 = 24% over 3 years

therefore leaving a value of $12,000 – ($12,000 × 24%) = $12,000 – $2,880 = $9,120.

If you selected option D, you calculated the value after two years, not three.

68 A If house prices rise at 3% per calendar month, this is equivalent to

(1.03)

12

= 1.426 or 42.6% per annum

If you selected option B, you forgot to take the effect of compounding into account, ie 3% × 12 =

36%.

If you selected option C, you incorrectly translated 1.426 into 14.26% instead of 42.6% per annum.

If you selected option D, you forget to raise 1.03 to the power of 12, instead you multiplied it by 12.

69 (a)

15.87

%

Working

15% per annum (nominal rate) is 3.75% per quarter. The effective annual rate of interest is

[1.0375

4

– 1] = 0.1587 = 15.87%

(b)

26.82

%

Working

24% per annum (nominal rate) is 2% per month. The effective annual rate of interest is

[1.02

12

– 1] = 0.2682 = 26.82%

Answer bank 377

70 (a)

$2,941

Working

Value after 3 years = $8,000 × 1.11

3

= $10,941 (to the nearest $)

∴ Interest = $10,941 – $8,000

= $2,941

(b)

$13,881

Working

Value after 5 years = $15,000 × 1.14

5

= $28,881 (to the nearest $)

∴ Interest = $28,881 – $15,000

= $13,881

(c)

$3,601

Working

Value after 4 years = $6,000 × 1.1

2

× 1.15

2

= $9,601 (to the nearest $)

∴ Interest = $9,601 – $6,000

= $3,601

(d)

10.78%

Working

Rate of interest = 5.25% every six months

∴Six monthly ratio = 1.0525

∴Annual ratio = 1.0525

2

= 1.1078

∴Effective annual rate = 10.78% (to 2 decimal places)

(e)

12.68%

Working

Rate of interest = 1% every month

∴ Monthly ratio = 1.01

∴ Annual ratio = 1.01

12

= 1.1268

∴ Effective annual rate = 12.68% (to 2 decimal places)

378 Answer bank

(f)

12.55%

Working

Rate of interest = 3% per quarter

∴ Quarterly ratio = 1.03

∴ Annual ratio = 1.03

4

= 1.1255

∴ Effective annual rate = 12.55% (to 2 decimal places)

71 C Present value of the lease for years 1 – 9 = $12,000 × 5.328

Present value of the lease for years 0 – 9 = $12,000 × (1 + 5.328)

= $12,000 × 6.328

= $75,936

If you selected option A, you calculated the PV of the lease for years 1-9 only. If the first payment is

made now, you must remember to add 1 to the 5.328.

Option B represents the PV of the lease for years 1-10 (the first payment being made in a one year's

time), ie $12,000 × 5.650 = $67,800.

Option D is incorrect because it represents the PV of the lease for years 1-10 plus an additional

payment now (ie $12,000 × (1 + 5.650) = $79,800.

72 D Let A = annual repayments

These repayments, A are an annuity for 15 years at 9%.

Annuity (A) =

factor Annuity

mortgage ofPV

PV of mortgage = $60,000

Annuity factor = 8.061 (9%, 15 years from CDF tables)

∴ Annuity =

061.8

000,60$

= $7,440 (to the nearest $10)

If you selected option A you have confused mortgages with sinking funds and have calculated the PV

of the mortgage as if it occurred at time 15 instead of time 0.

If you selected option B you have forgotten to take account of the interest rates (ie 9% for 15 years).

You have simply divided $60,000 by 15.

If you selected option C, you have not taken into account the fact that the repayments happen at the

year end and that the first repayment is in one year's time and not now.

73 C The IRR can be calculated using the following formula.

IRR = a +

()

%ab

NPVNPV

NPV

b

a

a

⎥

⎦

⎤

⎢

⎣

⎡

−×

−

Answer bank 379

where a = 10%

b = 24%

NPV

a

= $460

NPV

b

= $320

IRR = 10% +

()

%1024

320$460$

460$

⎥

⎦

⎤

⎢

⎣

⎡

−×

−

= 10% + 46%

= 56%

If you selected option A, you have calculated the arithmetic mean of 10% and 24% instead of using

the IRR formula.

If you selected option B you have used an NPV of –$320 instead of +$320 in your calculation.

If you selected option D, you must realise that it is possible to use either two positive or two

negative NPVs as well as a positive and negative NPV. Using the former method, however, the

results will be less accurate.

74 B The payments made on a credit card are an annuity of $x per month.

From cumulative present value tables (3%, 12 periods) the annuity factor is 9.954.

If Annuity =

factor Annuity

annuityof PV

Annuity =

954.9

000,21$

= $2,110

If you selected option A, you have simply divided $21,000 by 12 without any reference to

discounting.

If you selected option C, you have misread the cumulative present value tables (and used the annuity

factor for 12% and 3 periods instead of 12 periods and 3%).

If you selected option D, you have calculated the present value of $21,000 in 12 time periods at a

discount rate of 3% instead of finding the monthly annuity whose present value over 12 months at

3% gives $21,000.

75 A Project A has the highest NPV. When comparing projects it is the NPV of each project which should

be calculated and compared. The correct answer is therefore A.

Mutually exclusive projects should not be selected by comparing the IRRs – Option D is therefore

incorrect, even though it has the highest IRR, it does not have the highest NPV.

Projects B and C do not have the highest NPVs either and so options B and C are incorrect.