CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

100

4: Marginal costing and pricing decisions ⏐ Part A Cost determination and behaviour

Answer

C

Indirect costs are 20% of direct costs. Let D = direct costs and I = indirect costs.

So D + I = Full cost

Therefore D + 20% D = Full cost

Therefore 1.15 (D+ 0.2D) = Selling price

Therefore 1.15 × 1.2D = Selling price

Therefore 1.38D = Selling price

So the mark-up on direct costs is 38%

Or, assume that direct costs are $100

$

$

Direct costs

100

100

Indirect costs

20

120

Mark-up (15%)

18

Mark-up (balancing figure)

38

Selling price

138

Selling price

138

If you struggle with percentage calculations you need to spend some time getting them clear in your head. Percentage

calculations are vital for margin and mark-up questions.

Chapter Roundup

• Whereas fully absorbed product costs include fixed overhead, the marginal cost of a product usually consists of variable

costs only.

• Contribution is an important measure in marginal costing, and it is calculated as the difference between sales value and

marginal or variable cost.

•

Marginal costing is an alternative method of costing to absorption costing. In marginal costing, only variable costs are

charged as a cost of sale and a contribution is calculated. Closing inventories of work in progress or finished goods are

valued at marginal (variable) production cost. Fixed costs are treated as a period cost, and are charged in full against

profit in the accounting period in which they are incurred.

•

A price determined using full cost plus pricing is based on full cost plus a percentage mark-up for profit.

•

Marginal cost plus prices are based on the marginal cost of production or the marginal cost of sales, plus a profit

margin.

Assessment

focus point

121433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 4: Marginal costing and pricing decisions

101

Quick Quiz

1 Sales value – marginal cost of sales = …………………………………………………………..

2 Identify which of the following relate to either

A = Absorption costing

M = Marginal costing

A or M

(a) Closing inventories valued at marginal production cost

(b) Closing inventories valued at full production cost

(c) Cost of sales include some fixed overhead incurred in previous period in

opening inventory values

(d) Fixed costs are charged in full against profit for the period

3 Which of the following are arguments in favour of marginal costing?

(a) It is simple to operate.

(b) There is no under or over absorption of overheads.

(c) Fixed costs are the same regardless of activity levels.

(d) The information from this costing method may be used for decision making.

4 ABC Co plans to sell 1,200 units of product B. A 12% return is required on the $1,000,000 annual investment in product

B. A selling price of $500 per unit has been set.

The full cost of product B is $

.

5 XYZ Co produces a component W. The standard cost card for component W is as follows:

$

Production costs

Fixed

255.70

Variable

483.50

Selling costs

Fixed

124.80

Variable

75.60

Profit

60.40

Selling price

1,000.00

(a) Under an absorption costing system, what would be the value of inventory?

• $255.70 • $739.20 • $483.20 • $227.80

(b) Under a variable costing system, what would be the value of inventory?

• $483.50 • $75.60 • $136.00 • $124.80

6 When comparing the profits reported under absorption costing and marginal costing during a period when the level of

inventory increased:

A Absorption costing profits will be higher and closing inventory valuations lower than those under marginal

costing

B Absorption costing profits will be higher and closing inventory valuations higher than those under marginal

costing

122433 www.ebooks2000.blogspot.com

102

4: Marginal costing and pricing decisions ⏐ Part A Cost determination and behaviour

C Marginal costing profits will be higher and closing inventory valuations lower than those under absorption costing

D Marginal costing profits will be higher and closing inventory valuations higher than those under absorption

costing

Answers to quick quiz

1 Contribution

2

(a) Closing inventory valued at marginal production cost M

(b) Closing inventory valued at full production cost A

(c) Cost of sales include some fixed overhead incurred in previous period in

opening inventory values A

(d) Fixed costs are charged in full against profit for the period M

3 All are arguments in favour of marginal costing.

4 Required return = 12% × $1,000,000 = $120,000

Expected revenue = 1,200 × $500 = $600,000

Expected cost = expected revenue – required return

∴ Expected cost = $(600,000 – 120,000) = $480,000

∴ Full cost per unit = $480,000/1,200 = $400

5 (a) $255.70 + $483.50 = $739.20

Selling costs are never included in inventory valuations. The valuation under absorption costing is the full

production cost so it is the sum of the fixed production cost and the variable production cost.

(b) $483.50

Selling costs are never included in inventory valuations. The valuation under a variable costing system is the

variable production cost.

6 B Closing inventory valuation under absorption costing will always be higher than under marginal costing because

of the absorption of fixed overheads into closing inventory values.

The profit under absorption costing will be greater because the fixed overhead being carried forward in closing

inventory is greater than the fixed overhead being written off in opening inventory.

Now try the questions below from the Question Bank

Question numbers Page

16–20 354

A or M

123433 www.ebooks2000.blogspot.com

103

Topic list Learning outcomes Syllabus references Ability required

1 Inventory valuation A(vi) A(3) Application

2 FIFO (first in, first out) A(vi), (vii) A(3) Application, Comprehension

3 LIFO (last in, first out) A(vi), (vii) A(3) Application, Comprehension

4 AVCO (cumulative weighted average pricing) A(vi) A(3) Application

5 Inventory valuation and profitability A(vi) A(3) Application

6 Documentation A(vi) A(3) Comprehension

Inventory valuation

Introduction

The investment in inventory is a very important one for most businesses, both in terms of

monetary value and relationships with customers (no inventory, no sale, loss of customer

goodwill). It is therefore vital that management are aware of the major costing problem

relating to materials, that of pricing materials issues and valuing inventory at the end of each

period.

In this chapter we will therefore consider the methods for pricing materials issues/valuing

inventory. We will look at the various methods, their advantages and disadvantages and their

impact on profitability.

124433 www.ebooks2000.blogspot.com

104

5: Inventory valuation ⏐ Part A Cost determination and behaviour

1 Inventory valuation

The correct pricing of issues and valuation of inventory are of the utmost importance because they have a direct effect

on the calculation of profit. Several different methods can be used in practice.

1.1 Valuing inventory in financial accounts

You may be aware from your studies for the Fundamentals of Financial Accounting paper that, for financial accounting

purposes, inventories are valued at the lower of cost and net realisable value. In practice, inventories will probably be

valued at cost in the stores records throughout the course of an accounting period. Only when the period ends will the

value of the inventory in hand be reconsidered so that items with a net realisable value below their original cost will be

revalued downwards, and the inventory records altered accordingly.

1.2 Charging units of inventory to cost of production or cost of sales

It is important to be able to distinguish between the way in which the physical items in inventory are actually issued. In

practice a storekeeper may issue goods in the following way.

• The oldest goods first

• The latest goods received first

• Randomly

• Those which are easiest to reach

By comparison the cost of the goods issued must be determined on a consistently applied basis, and must ignore the

likelihood that the materials issued will be costed at a price different to the amount paid for them.

This may seem a little confusing at first, and it may be helpful to explain the point further by looking at an example.

1.3 Example: inventory valuation

Suppose that there are three units of a particular material in inventory.

Units Date received Purchase cost

A June 20X1 $100

B July 20X1 $106

C August 20X1 $109

In September, one unit is issued to production. As it happened, the physical unit actually issued was B. The accounting

department must put a value or cost on the material issued, but the value would not be the cost of B, $106. The

principles used to value the materials issued are not concerned with the actual unit issued, A, B, or C. Nevertheless, the

accountant may choose to make one of the following assumptions.

(a) The unit issued is valued as though it were the earliest unit in inventory, ie at the purchase cost of A, $100.

This valuation principle is called FIFO, or first in, first out.

(b) The unit issued is valued as though it were the most recent unit received into inventory, ie at the purchase

cost of C, $109. This method of valuation is LIFO, or last in, first out.

(c) The unit issued is valued at an average price of A, B and C, ie $105.

(It may be that each item of inventory is marked with the purchase cost, as it is received. This method is known as the

specific price method. In the majority of cases this method is not practical.)

FA

S

T F

O

RWAR

D

125433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 5: Inventory valuation

105

1.4 A chapter example

In the following sections we will consider each of the pricing methods detailed above (and a few more), using the

following transactions to illustrate the principles in each case.

TRANSACTIONS DURING MAY 20X6

Market value

per unit on date

Quantity

Unit cost

Total cost

of transaction

Units

$

$

$

Opening balance, 1 May

100

2.00

200

Receipts, 3 May

400

2.10

840

2.11

Issues, 4 May

200

2.11

Receipts, 9 May

300

2.12

636

2.15

Issues, 11 May

400

2.20

Receipts, 18 May

100

2.40

240

2.35

Issues, 20 May

100

2.35

Closing balance, 31 May

200

2.38

1,916

2 FIFO (first in, first out)

FIFO assumes that materials are issued out of inventory in the order in which they were delivered into inventory: issues

are priced at the cost of the earliest delivery remaining in inventory.

FIFO (first in, first out) is 'used to price issues of goods or materials based on the cost of the oldest units held,

irrespective of the sequence in which the actual issue of units held takes place. Closing stock is, therefore, valued at the

cost of the oldest purchases.' CIMA Official Terminology

2.1 Example: FIFO

Using FIFO, the cost of issues and the closing inventory value in the transactions in section 1.4 would be as follows.

Date of issue

Quantity issued

Value

Units

$

$

4 May

200

100 o/s at $2

200

100 at $2.10

210

410

11 May

400

300 at $2.10

630

100 at $2.12

212

842

20 May

100

100 at $2.12

212

Cost of issues

1,464

Closing inventory value

200

100 at $2.12

212

100 at $2.40

240

452

1,916

FA

S

T F

O

RWAR

D

Key term

126433 www.ebooks2000.blogspot.com

106

5: Inventory valuation ⏐ Part A Cost determination and behaviour

Notes

(a) The cost of materials issued plus the value of closing inventory equals the cost of purchases plus the value of

opening inventory ($1,916).

(b) The market price of purchased materials is rising dramatically. In a period of inflation, there is a tendency with

FIFO for materials to be issued at a cost lower than the current market value, although closing inventories tend to

be valued at a cost approximating to current market value. FIFO is therefore essentially a historical cost method,

materials included in cost of production being valued at historical cost.

2.2 Advantages and disadvantages of the FIFO method

Advantages

Disadvantages

It is a logical pricing method which probably represents

what is physically happening: in practice the oldest

inventory is likely to be used first.

FIFO can be cumbersome to operate because of the

need to identify each batch of material separately.

It is easy to understand and explain to managers.

Managers may find it difficult to compare costs and

make decisions when they are charged with varying

prices for the same materials.

The inventory valuation can be near to a valuation based

on replacement cost.

In a period of high inflation, inventory issue prices will

lag behind current market value.

Question

FIFO

Complete the table below in as much detail as possible using the information in Sections 1.4 and 2.1.

Receipts Issues Inventory

Date

Quantity

Unit price

$

Amount

$

Quantity

Unit price

$

Amount

$

Quantity

Unit price

$

Amount $

127433

www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 5: Inventory valuation

107

Answer

Receipts Issues Inventory

Date

Quantity

Unit price

$

Amount

$

Quantity

Unit price

$

Amount

$

Quantity

Unit price

$

Amount $

1.5.X3

100

2.00

200.00

3.5.X3

400

2.10

840.00

100

2.00

200.00

400

2.10

840.00

500

1,040.00

4.5.X3

100

2.00

200.00

100

2.10

210.00

300

2.10

630.00

9.5.X3

300

2.12

636.00

300

2.10

630.00

300

2.12

636.00

600

1,266.00

11.5.X3

300

2.10

630.00

100

2.12

212.00

200

2.12

424.00

18.5.

X3

100

2.40

240.00

200

2.12

424.00

100

2.40

240.00

300

664.00

20.5.X3

100

2.12

212.00

100

2.12

212.00

100

2.40

240.00

31.5.X3

200

452.00

Note that this type of record is called a perpetual inventory system as it shows each receipt and issue of inventory as it

occurs.

128433 www.ebooks2000.blogspot.com

108

5: Inventory valuation ⏐ Part A Cost determination and behaviour

3 LIFO (last in, first out)

LIFO assumes that materials are issued out of inventory in the reverse order to which they were delivered: the most

recent deliveries are issued before earlier ones, and issues are priced accordingly.

LIFO (last in, first out) is 'used to price issues of goods or materials based on the cost of the most recently received

units. Cost of sales in the income statement is, therefore, valued at the cost of the most recent purchases.'

CIMA Official Terminology

3.1 Example: LIFO

Using LIFO, the cost of issues and the closing inventory value in the example above would be as follows.

Date of issue

Quantity issued

Valuation

Units

$

$

4 May

200

200 at $2.10

420

11 May

400

300 at $2.12

636

100 at $2.10

210

846

20 May

100

100 at $2.40

240

Cost of issues

1,506

Closing inventory value

200

100 at $2.10

210

100 at $2.00

200

410

1,916

Notes

(a) The cost of materials issued plus the value of closing inventory equals the cost of purchases plus the value of

opening inventory ($1,916).

(b) In a period of inflation there is a tendency with LIFO for the following to occur.

(i) Materials are issued at a price which approximates to current market value (or economic cost).

(ii) Closing inventories become undervalued when compared to market value.

3.2 Advantages and disadvantages of the LIFO method

Advantages Disadvantages

Inventories are issued at a price which is close to current

market value.

The method can be cumbersome to operate because it

sometimes results in several batches being only part-used

in the inventory records before another batch is received.

Managers are continually aware of recent costs when

making decisions, because the costs being charged to

their department or products will be current costs.

LIFO is often the opposite to what is physically happening

and can therefore be difficult to explain to managers.

As with FIFO, decision making can be difficult because of

the variations in prices.

FA

S

T F

O

RWAR

D

Key term

129433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 5: Inventory valuation

109

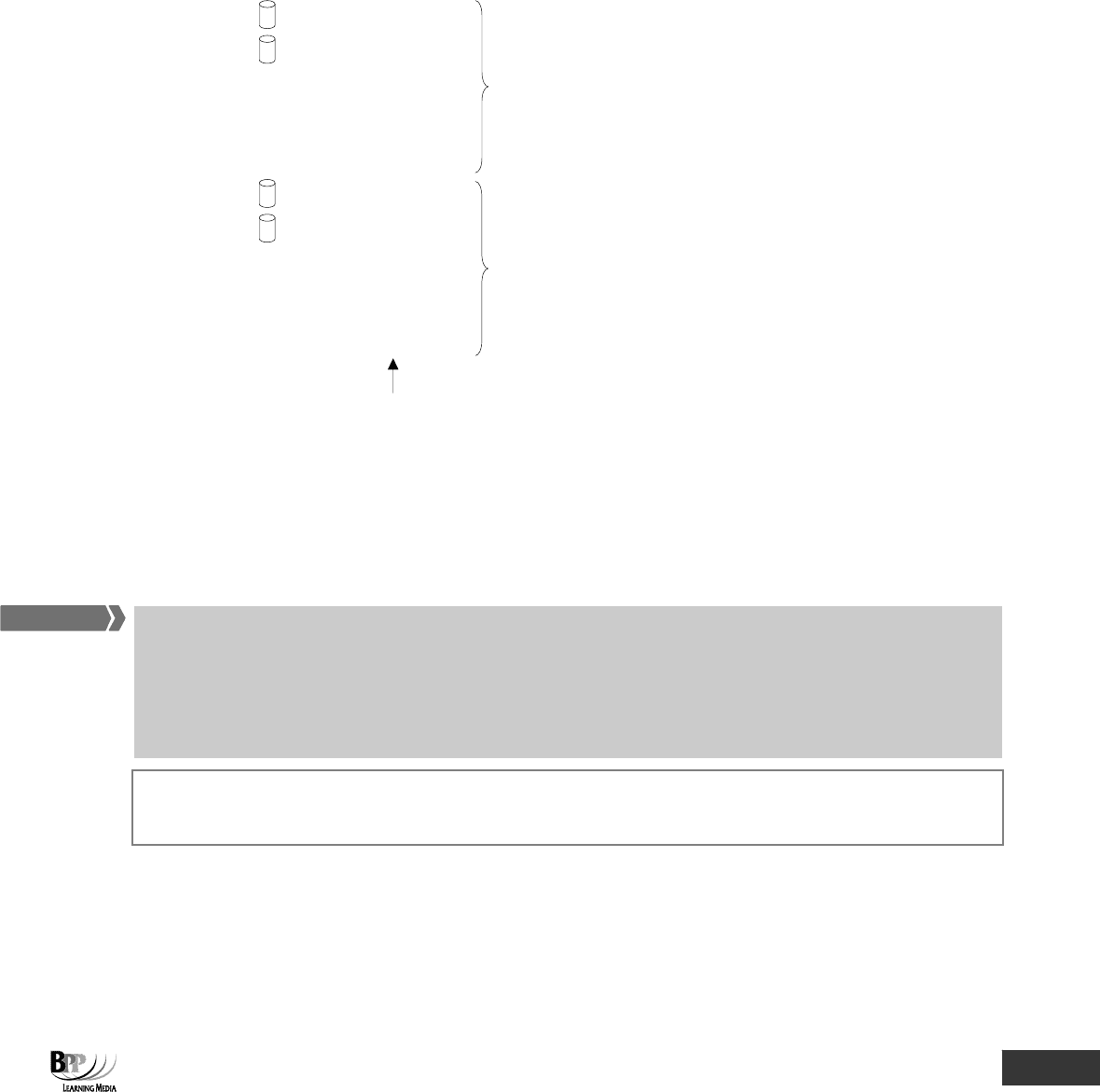

3.3 Changing from LIFO to FIFO or from FIFO to LIFO

You may get an assessment question which asks you what would happen to closing inventory values or gross profits if a

business changed its method from LIFO to FIFO or vice versa. You may find it easier to think about this using diagrams.

Let's consider a very simple example where four barrels of inventory are purchased during a month of rising prices, and

two are used. There is no opening inventory.

Cost

Jan 1

st

$100 per barrel

Jan 19

th

$150 per barrel

LIFO – these

barrels would be

left as closing

inventory $250

FIFO – these

barrels would be

issued to

production first

(and charged to

cost of sales)

$250)

Jan 20

th

$200 per barrel

Jan 31

st

$250 per barrel

LIFO – these

barrels would be

issued to

production first

(and charged to

cost of sales)

$450

FIFO – these

barrels would be

left as closing

inventory $450

Notice the rising prices

As you can see, during a period of rising prices, the closing inventory value using LIFO would be $250 and using FIFO

would be higher at $450. The charge to cost of sales will be lower using FIFO and therefore the gross profit will be

higher.

4 AVCO (cumulative weighted average pricing)

The cumulative weighted average pricing method (or AVCO) calculates a weighted average price for all units in

inventory. Issues are priced at this average cost, and the balance of inventory remaining would have the same unit

valuation. The average price is determined by dividing the total cost by the total number of units.

A new weighted average price is calculated whenever a new delivery of materials is received into store. This is the key

feature of cumulative weighted average pricing.

Average cost is 'used to price issues of goods or materials at the weighted average cost of all units held'.

CIMA Official Terminology

FA

S

T F

O

RWAR

D

Key terms

130433 www.ebooks2000.blogspot.com