Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

An investor who bought a portfolio of the shares of Class I railroads in 1999 got a

dividend yield of about 2.0 percent. A review of security analysts’ forecasts gave

an average expected growth rate for earnings and dividends of 10.9 percent. The

cost of equity was thus estimated at r

E

2.0 10.9 12.9 percent.

Using the statutory marginal tax rate of 35 percent,

12

the railroad industry

WACC is

Valuing Companies: WACC vs. the Flow-to-Equity Method

WACC is normally used as a hurdle rate or discount rate to value proposed capi-

tal investments. But sometimes it is used as a discount rate for valuing whole com-

panies. For example, the financial manager may need to value a target company to

decide whether to go ahead with a merger.

Valuing companies raises no new conceptual problems. You just treat the com-

pany as if it were one big project. Forecast the company’s cash flows (the hardest

part of the exercise) and discount back to present value. The company’s WACC is

the right discount rate if the company’s debt ratio is expected to remain reasonably

close to constant. But remember:

• If you discount at WACC, cash flows have to be projected just as you would

for a capital investment project. Do not deduct interest. Calculate taxes as if

the company were all-equity-financed. The value of interest tax shields is

picked up in the WACC formula.

• The company’s cash flows will probably not be forecasted to infinity. Financial

managers usually forecast to a medium-term horizon—10 years, say—and add

a terminal value to the cash flows in the horizon year. The terminal value is

the present value at the horizon of post-horizon flows. Estimating the terminal

value requires careful attention because it often accounts for the majority of

the value of the company. See Section 4.5.

• Discounting at WACC values the assets and operations of the company. If the

object is to value the company’s equity, that is, its common stock, don’t forget

to subtract the value of the company’s outstanding debt.

If the task is to value equity, there’s an obvious alternative to discounting com-

pany cash flows at its WACC. Discount the cash flows to equity, after interest and af-

ter taxes, at the cost of equity. This is called the flow-to-equity method. If the com-

pany’s debt ratio is constant over time, the flow-to-equity method should give the

same answer as discounting company cash flows at the WACC and subtracting debt.

The flow-to-equity method seems simple, and it is simple if the proportions of

debt and equity financing stay reasonably close to constant for the life of the com-

pany. But the cost of equity depends on financial leverage; it depends on financial

risk as well as business risk. If financial leverage will change significantly, dis-

counting flows to equity at today’s cost of equity will not give the right answer.

A one-shot change in financing can usually be accommodated. Think again of a

proposed takeover. Suppose the financial manager decides that the target’s 20 per-

cent debt-to-value ratio is stodgy and too conservative. She decides the company

WACC 0.07211.3521.3732 .1291.6272 .098, or about 10%

CHAPTER 19

Financing and Valuation 531

12

The STB actually uses a pretax cost of debt. If the STB’s reported WACC is used as a discount rate, in-

terest tax shields have to be valued separately, as in the adjusted-present-value method described in

Section 19.4.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

could easily support 40 percent debt and asks you to value the target’s shares on

that assumption. Unfortunately you have estimated the cost of equity at the exist-

ing 20 percent ratio. No problem! Adjust the cost of equity (we will revisit the for-

mula in the next section) and proceed as usual. Of course you must forecast and

discount cash flows to equity at the new 40 percent debt ratio. You also have to as-

sume that this debt ratio will be maintained after the takeover.

Mistakes People Make in Using the Weighted-Average Formula

The weighted-average formula is very useful but also dangerous. It tempts people

to make logical errors. For example, manager Q, who is campaigning for a pet proj-

ect, might look at the formula

and think, Aha! My firm has a good credit rating. It could borrow, say, 90 percent of

the project’s cost if it likes. That means and . My firm’s borrowing

rate is 8 percent, and the required return on equity, , is 15 percent. Therefore

or 6.2 percent. When I discount at that rate, my project looks great.

Manager Q is wrong on several counts. First, the weighted-average formula

works only for projects that are carbon copies of the firm. The firm isn’t 90 percent

debt-financed.

Second, the immediate source of funds for a project has no necessary connection

with the hurdle rate for the project. What matters is the project’s overall contribu-

tion to the firm’s borrowing power. A dollar invested in Q’s pet project will not in-

crease the firm’s debt capacity by $.90. If the firm borrows 90 percent of the pro-

ject’s cost, it is really borrowing in part against its existing assets. Any advantage

from financing the new project with more debt than normal should be attributed

to the old projects, not to the new one.

Third, even if the firm were willing and able to lever up to 90 percent debt, its cost

of capital would not decline to 6.2 percent (as Q’s naive calculation predicts). You

cannot increase the debt ratio without creating financial risk for stockholders and

thereby increasing , the expected rate of return they demand from the firm’s com-

mon stock. Going to 90 percent debt would certainly increase the borrowing rate, too.

r

E

WACC .0811 .352 1.92 .151.12 .062

r

E

r

D

E/V .1D/V .9

WACC r

D

11 T

c

2

D

V

r

E

E

V

532 PART V

Dividend Policy and Capital Structure

13

It could change the tax rate too. For example, the firm might have enough pretax income to cover in-

terest payments at 20 percent debt but not at 40 percent. In this case the effective marginal tax rate would

be higher at 20 percent debt.

19.3 ADJUSTING WACC WHEN DEBT RATIOS OR

BUSINESS RISKS CHANGE

The WACC formula assumes that the project to be valued will be financed in the

same proportions of debt and equity as the firm as a whole. What if that is not true?

What if the perpetual crusher project supports debt equal to, say, 20 percent of proj-

ect value, versus 40 percent debt financing for the firm as a whole?

Moving from 40 to 20 percent debt changes all the elements of the WACC for-

mula except the tax rate.

13

Obviously the financing weights change. But the cost

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

of equity is less, because financial risk is reduced. The cost of debt may be

lower too.

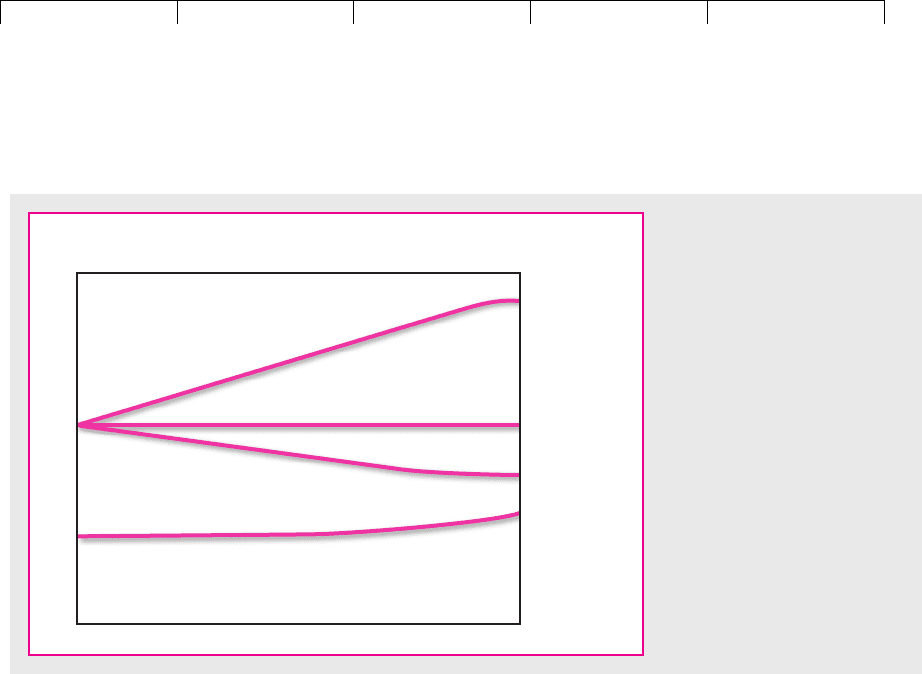

Figure 19.1 plots WACC and the costs of debt and equity as a function of the

debt–equity ratio. The flat line is r, the opportunity cost of capital. Remember, this

is the expected rate of return that investors would want from the project if it were

all-equity-financed. The opportunity cost of capital depends only on business risk

and is the natural reference point.

Suppose Sangria or the perpetual crusher project were all-equity-financed

( ). At that point WACC equals cost of equity, and both equal the opportu-

nity cost of capital. Start from that point in Figure 19.1. As the debt ratio increases,

the cost of equity increases, because of financial risk, but notice that WACC de-

clines. The decline is not caused by use of “cheap” debt in place of “expensive” eq-

uity. It falls because of the tax shields on debt interest payments. If there were no

corporate income taxes, the weighted-average cost of capital would be constant,

and equal to the opportunity cost of capital, at all debt ratios. We showed this in

Chapters 9 and 17.

Figure 19.1 shows the shape of the relationship between financing and WACC,

but we have numbers only for Sangria’s current 40 percent debt ratio. We want to

recalculate WACC at a 20 percent ratio.

Here is the simplest way to do it. There are three steps.

Step 1 Calculate the opportunity cost of capital. In other words, calculate WACC

and the cost of equity at zero debt. This step is called unlevering the WACC. The

simplest unlevering formula is

This formula comes directly from Modigliani and Miller’s proposition I (see Sec-

tion 17.1). If taxes are left out, the weighted-average cost of capital equals the op-

portunity cost of capital and is independent of leverage.

Opportunity cost of capital r r

D

D/V r

E

E/V

D/V 0

r

E

CHAPTER 19 Financing and Valuation 533

r

Debt–equity

ratio (

D/E

)

Cost of equity (

r

E

)

Cost of debt (

r

D

)

Opportunity cost of capital (

r

)

Rates of

return

WACC

FIGURE 19.1

WACC plotted against the debt–

equity ratio. WACC equals the

opportunity cost of capital when

there is no debt. WACC declines

with financial leverage because

of interest tax shields.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

Step 2 Estimate the cost of debt, , at the new debt ratio, and calculate the new

cost of equity.

This formula is Modigliani and Miller’s proposition II (see Section 17.2). It calls for

D/E, the ratio of debt to equity, not debt to value.

Step 3 Recalculate the weighted-average cost of capital at the new financing

weights.

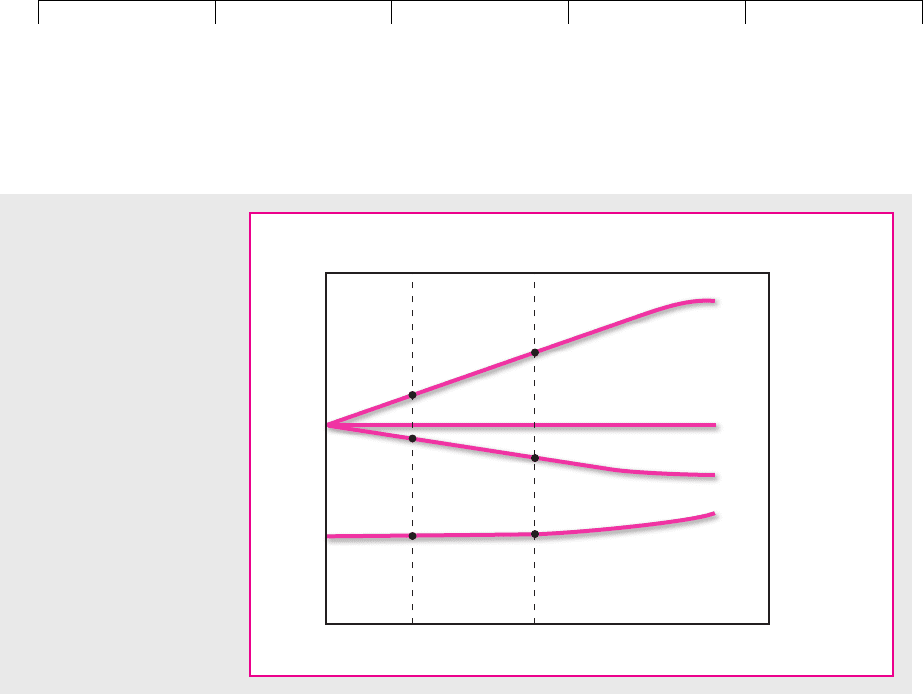

Let’s do the numbers for the perpetual crusher project at or 20 percent.

Step 1. Sangria’s current debt ratio is

Step 2. We will assume that the debt cost stays at 8 percent when the debt ratio

is 20 percent. Then

Note that the debt–equity ratio is .

Step 3. Recalculate WACC.

Figure 19.2 enters these numbers on the plot of WACC versus debt ratio. The 11.4

percent project discount rate at 20 percent debt to value is .56 percentage points

higher than at 40 percent.

Another Example: WACC for U.S. Railroads at 45 percent Debt Let’s return to the

WACC we calculated for large U.S. railroads. We assumed a debt-to-value ratio of

37.3 percent. How would the railroad industry WACC change at 45 percent debt?

WACC .0811 .352

1.22 .131.82 .114 or 11.4%

.2/.8 .25

r

E

.12 1.12 .082 1.252 .13 or 13%

r .08 1.42 .1461.62 .12 or 12%

D/V .4

D/V .20

r

E

r 1r r

D

2D/E

r

D

534 PART V Dividend Policy and Capital Structure

12

8

.25

(

D/V

= .2)

.67

(

D/V

= .4)

10

14

13.0

11.4

8.0

14.6

10.84

8.0

Debt–equity

ratio (

D/E

)

Cost of equity (

r

E

)

Cost of debt (

r

D

)

Opportunity cost of capital (

r

= 12%)

Rates of

return, percent

WACC

FIGURE 19.2

This plot shows WACC for

the Sangria Corporation at

debt-to-equity ratios of 25

and 67 percent. The corre-

sponding debt-to-value

ratios are 20 and 40 percent.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

Step 1. Calculate the unlevered opportunity cost of capital

Step 2. Assume that the cost of debt increases to 8 percent at 45 percent debt. The

cost of equity is

Step 3. Recalculate WACC. If the marginal tax rate stays at 35 percent,

The cost of capital drops by more than one half percentage point. Is this a great

deal? Not as good as it looks. In these simple calculations, the cost of capital drops

as financial leverage increases, but only because of corporate interest tax shields.

In Chapter 18 we reviewed all the reasons why just focusing on corporate interest

tax shields overstates the advantages of debt. For example, costs of financial dis-

tress encountered at high debt levels appear nowhere in the WACC formula or in

the standard formulas relating the cost of equity for leverage.

14

Unlevering and Relevering Betas

Our three-step procedure (1) unlevers and then (2) relevers the cost of equity. Some

financial managers find it convenient to (1) unlever and then (2) relever the equity

beta. Given the beta of equity at the new debt ratio, the cost of equity is determined

from the capital asset pricing model. Then WACC is recalculated.

The formula for unlevering beta was given in Section 9.2.

This equation says that the beta of a firm’s assets is revealed by the beta of a port-

folio of all of the firm’s outstanding debt and equity securities. An investor who

bought such a portfolio would own the assets free and clear and absorb only busi-

ness risks.

The formula for relevering beta closely resembles MM’s proposition II, except

that betas are substituted for rates of return:

The Importance of Rebalancing

The formulas for WACC and for unlevering and relevering expected returns are

simple, but we must be careful to remember underlying assumptions. The most

important point is rebalancing.

Calculating WACC for a company at its existing capital structure requires that the

capital structure not change; in other words, the company must rebalance its capital

structure to maintain the same market-value debt ratio for the relevant future. Take

Sangria Corporation as an example. It starts with a debt-to-value ratio of 40 percent

and a market value of $125 million. Suppose that Sangria’s products do unexpectedly

equity

asset

1

asset

debt

2D/E

asset

debt

1D/V2

equity

1E/V2

WACC .08011 .352.45 .1301.552 .095 or 9.5%

r

E

.108 1.108 .080245/55 .13

r .0721.3732 .1291.6272 .108

CHAPTER 19 Financing and Valuation 535

14

Some financial managers and analysts argue that the costs of debt and equity increase rapidly at high

debt ratios because of costs of financial distress. This in turn would cause the WACC curve in Figure

19.1 to flatten out, and finally increase, as the debt ratio climbs. For practical purposes, this can be a sen-

sible end result. However, formal modeling of the interactions between the cost of financial distress and

the expected rates of return on the company’s securities is not easy.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

well in the marketplace and that market value increases to $150 million. Rebalancing

means that it will then increase debt to ,

15

thus regaining a

40 percent ratio. If market value instead falls, Sangria would have to pay down debt

proportionally.

Of course real companies do not rebalance capital structure in such a mechani-

cal and compulsive way. For practical purposes, it’s sufficient to assume gradual

but steady adjustment toward a long-run target. But if the firm plans significant

changes in capital structure (for example, if it plans to pay off its debt), the WACC

formula won’t work. In such cases, you should turn to the APV method, which we

describe in the next section.

Our three-step procedure for recalculating WACC makes a similar rebalancing as-

sumption.

16

Whatever the starting debt ratio, the firm is assumed to rebalance to main-

tain that ratio in the future. The unlevering and relevering in steps 1 and 2 also ignore

any impact of investors’ personal income taxes on the costs of debt and equity.

17

.4 150 $60 million

536 PART V Dividend Policy and Capital Structure

15

The proceeds of the additional borrowing would be paid out to shareholders or used, along with ad-

ditional equity investment, to finance Sangria’s growth.

16

Similar, but not identical. The basic WACC formula assumes that rebalancing occurs at the end of each

period. The unlevering and relevering formulas used in steps 1 and 2 of our three-step procedure are

exact only if rebalancing is continuous so that the debt ratio stays constant day-to-day and week-to-

week. However, the errors introduced from annual rebalancing are very small and can be ignored for

practical purposes.

17

The response of the cost of equity to changes in financial leverage can be affected by personal taxes.

This is not covered here and is rarely adjusted for in practice.

19.4 ADJUSTED PRESENT VALUE

We now take a different tack. Instead of messing around with the discount rate, we

explicitly adjust cash flows and present values for costs or benefits of financing.

This approach is called adjusted present value, or APV.

The adjusted-present-value rule is easiest to understand in the context of simple

numerical examples. We start by analyzing a project under base-case assumptions

and then consider possible financing side effects of accepting the project.

The Base Case

The APV method begins by valuing the project as if it were a mini-firm financed

solely by equity. Consider a project to produce solar water heaters. It requires a $10

million investment and offers a level after-tax cash flow of $1.8 million per year for

10 years. The opportunity cost of capital is 12 percent, which reflects the project’s

business risk. Investors would demand a 12 percent expected return to invest in the

mini-firm’s shares.

Thus the mini-firm’s base-case NPV is

Considering the project’s size, this figure is not much greater than zero. In a pure

MM world where no financing decision matters, the financial manager would lean

toward taking the project but would not be heartbroken if it were discarded.

NPV 10

a

10

t1

1.8

11.122

t

$.17 million, or $170,000

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

Issue Costs

But suppose that the firm actually has to finance the $10 million investment by is-

suing stock (it will not have to issue stock if it rejects the project) and that issue

costs soak up 5 percent of the gross proceeds of the issue. That means the firm has

to issue $10,526,000 in order to obtain $10,000,000 cash. The $526,000 difference

goes to underwriters, lawyers, and others involved in the issue process.

The project’s APV is calculated by subtracting the issue cost from base-case NPV:

The firm would reject the project because APV is negative.

Additions to the Firm’s Debt Capacity

Consider a different financing scenario. Suppose that the firm has a 50 percent tar-

get debt ratio. Its policy is to limit debt to 50 percent of its assets. Thus, if it invests

more, it borrows more; in this sense investment adds to the firm’s debt capacity.

18

Is debt capacity worth anything? The most widely accepted answer is yes be-

cause of the tax shields generated by interest payments on corporate borrowing.

(Look back to our discussion of debt and taxes in Chapter 18.) For example, MM’s

theory states that the value of the firm is independent of its capital structure except

for the present value of interest tax shields:

This theory tells us to compute the value of the firm in two steps: First compute its

base-case value under all-equity financing, and then add the present value of taxes

saved due to a departure from all-equity financing. This procedure is like an APV

calculation for the firm as a whole.

We can repeat the calculation for a particular project. For example, suppose that

the solar heater project increases the firm’s assets by $10 million and therefore

prompts it to borrow $5 million more. Suppose that this $5 million loan is repaid

in equal installments, so that the amount borrowed declines with the depreciating

book value of the solar heater project. We also assume that the loan carries an in-

terest rate of 8 percent. Table 19.1 shows how the value of the interest tax shields is

calculated. This is the value of the additional debt capacity contributed to the firm

by the project. We obtain APV by adding this amount to the project’s NPV:

With these numbers, the solar heater project looks like a “go.” But notice the dif-

ferences between this APV calculation and an NPV calculated with a WACC used as

the discount rate. The APV calculation assumes debt equal to 50 percent of book

value, paid down on a fixed schedule. NPV using WACC assumes debt is a constant

fraction of market value in each year of the project’s life. Since the project’s value will

inevitably turn out higher or lower than expected, using WACC also assumes that

170,000 576,000 $746,000

APV base-case NPV PV1tax shield2

Firm value value with all-equity financing PV1tax shield2

170,000 526,000 $356,000

APV base-case NPV issue cost

CHAPTER 19

Financing and Valuation 537

18

Debt capacity is potentially misleading because it seems to imply an absolute limit to the amount the

firm is able to borrow. That is not what we mean. The firm limits borrowing to 50 percent of assets as a

rule of thumb for optimal capital structure. It could borrow more if it wanted to run increased risks of

costs of financial distress.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

future debt levels will be increased or reduced as necessary to keep the future debt

ratio constant.

APV can be used when debt supported by a project is tied to the project’s book

value or has to be repaid on a fixed schedule. For example, Kaplan and Ruback used

APV to analyze the prices paid for a sample of leveraged buyouts (LBOs). LBOs are

takeovers, typically of mature companies, financed almost entirely with debt. How-

ever, the new debt is not intended to be permanent. LBO business plans call for gen-

erating extra cash by selling assets, shaving costs, and improving profit margins. The

extra cash is used to pay down the LBO debt. Therefore you can’t use WACC as a dis-

count rate to evaluate an LBO because its debt ratio will not be constant.

APV works fine for LBOs. The company is first evaluated as if it were all-equity-

financed. That means that cash flows are projected after tax, but without any in-

terest tax shields generated by the LBO’s debt. The tax shields are then valued sep-

arately. The debt repayment schedule is set down in the same format as Table 19.1

and the present value of interest tax shields is calculated and added to the all-

equity value. Any other financing side effects are added also. The result is an APV

valuation for the company.

19

Kaplan and Ruback found that APV did a pretty good

job explaining prices paid in these hotly contested takeovers, considering that not

all the information available to bidders had percolated into the public domain.

Kaplan and Ruback were restricted to publicly available data.

538 PART V

Dividend Policy and Capital Structure

Debt Outstanding Interest Present Value

Year at Start of Year Interest Tax Shield of Tax Shield

1 $5,000 $400 $140 $129.6

2 4,500 360 126 108.0

3 4,000 320 112 88.9

4 3,500 280 98 72.0

5 3,000 240 84 57.2

6 2,500 200 70 44.1

7 2,000 160 56 32.6

8 1,500 120 42 22.7

9 1,000 80 28 14.0

10 500 40 14 6.5

Total $576

TABLE 19.1

Calculating the present value of interest tax shields on debt supported by the solar heater project

(dollar figures in thousands).

Assumptions:

1. Marginal tax ; tax shield .

2. Debt principal is repaid at end of year in ten $500,000 installments.

3. Interest rate on debt is 8 percent.

4. Present value is calculated at the 8 percent borrowing rate. The assumption here is that the tax shields are just as

risky as the interest payments generating them.

T

c

interestrate T

c

.35

19

Kaplan and Ruback actually used “compressed” APV, in which all cash flows, including interest tax

shields, are discounted at the opportunity cost of capital. S. N. Kaplan and R. S. Ruback, “The Valua-

tion of Cash Flow Forecasts: An Empirical Analysis,” Journal of Finance 50 (September 1995),

pp. 1059–1093.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

The Value of Interest Tax Shields

In Table 19.1, we boldly assume that the firm can fully capture interest tax shields

of $.35 on every dollar of interest. We also treat the interest tax shields as safe cash

inflows and discount them at a low 8 percent rate.

The true present value of the tax shields is almost surely less than $576,000:

• You can’t use tax shields unless you pay taxes, and you don’t pay taxes unless

you make money. Few firms can be sure that future profitability will be

sufficient to use up the interest tax shields.

• The government takes two bites out of corporate income: the corporate tax

and the tax on bondholders’ and stockholders’ personal income. The corporate

tax favors debt; the personal tax favors equity.

• A project’s debt capacity depends on how well it does. When profits exceed

expectations, the firm can borrow more; if the project fails, it won’t support

any debt. If the future amount of debt is tied to future project value, then the

interest tax shields given in Table 19.1 are estimates, not fixed amounts.

In Chapter 18, we argued that the effective tax shield on interest was probably

not 35 percent ( ) but some lower figure, call it T*. We were unable to pin

down an exact figure for T*.

Suppose, for example, that we believe T* .25. We can easily recalculate the

APV of the solar heater project. Just multiply the present value of the interest tax

shields by 25/35. The bottom line of Table 19.1 drops from $576,000 to

. APV drops to

PV(tax shield) drops still further if the tax shields are treated as forecasts and

discounted at a higher rate. Suppose the firm ties the amount of debt to actual fu-

ture project cash flows. Then the interest tax shields become just as risky as the

project and should be discounted at the 12 percent opportunity cost of capital.

PV(tax shield) drops to $362,000 at T* .25.

Review of the Adjusted-Present-Value Approach

If the decision to invest in a capital project has important side effects on other fi-

nancial decisions made by the firm, those side effects should be taken into account

when the project is evaluated. They include interest tax shields on debt supported

by the project (a plus), any issue costs of raising financing for the project (a minus),

or perhaps other side effects such as the value of a government-subsidized loan

tied to the project.

The idea behind APV is to divide and conquer. The approach does not attempt

to capture all the side effects in a single calculation. A series of present value cal-

culations is made instead. The first establishes a base-case value for the project: its

value as a separate, all-equity-financed mini-firm. Then each side effect is traced

out, and the present value of its cost or benefit to the firm is calculated. Finally, all

the present values are added together to estimate the project’s total contribution to

the value of the firm. Thus, in general,

Project APV base-case NPV

sum of the present values of the side

effects of accepting the project

170,000 411,000 $581,000

APV base-case NPV PV1tax shield2

576,000125/352 $411,000

T

c

.35

CHAPTER 19 Financing and Valuation 539

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

19. Financing and

Valuation

© The McGraw−Hill

Companies, 2003

The wise financial manager will want to see not only the adjusted present value

but also where that value is coming from. For example, suppose that base-case

NPV is positive but the benefits are outweighed by the costs of issuing stock to fi-

nance the project. That should prompt the manager to look around to see if the

project can be rescued by an alternative financing plan.

APV for International Projects

APV is most useful when financing side effects are numerous and important. This

is frequently the case for large international projects, which may have custom-

tailored project financing and special contracts with suppliers, customers, and gov-

ernments.

20

Here are a few examples of financing side effects encountered in the

international arena.

We explain project finance in Chapter 25. It typically means very high debt ra-

tios to start, with most or all of a project’s early cash flows committed to debt ser-

vice. Equity investors have to wait. Since the debt ratio will not be constant, you

have to turn to APV.

Project financing may include debt available at favorable interest rates. Most

governments subsidize exports by making special financing packages available,

and manufacturers of industrial equipment may stand ready to lend money to help

close a sale. Suppose, for example, that your project requires construction of an on-

site electricity generating plant. You solicit bids from suppliers in various coun-

tries. Don’t be surprised if the competing suppliers sweeten their bids with offers

of low interest rate project loans or if they offer to lease the plant on favorable

terms. You should then calculate the NPVs of these loans or leases and include

them in your project analysis.

Sometimes international projects are supported by contracts with suppliers or

customers. Suppose a manufacturer wants to line up a reliable supply of a crucial

raw material—powdered magnoosium, say. The manufacturer could subsidize a

new magnoosium smelter by agreeing to buy 75 percent of production and guar-

anteeing a minimum purchase price. The guarantee is clearly a valuable addition

to project APV: If the world price of powdered magnoosium falls below the mini-

mum, the project doesn’t suffer. You would calculate the value of this guarantee

(by the methods explained in Chapters 20 and 21) and add it to APV.

Sometimes local governments impose costs or restrictions on investment or disin-

vestment. For example, Chile, in an attempt to slow down a flood of short-term cap-

ital inflows in the 1990s, required investors to “park” part of their incoming money in

non-interest-bearing accounts for a period of two years. An investor in Chile during

this period would calculate the cost of this requirement and subtract it from APV.

APV for the Perpetual Crusher Project

Discounting at WACC and calculating APV may seem like totally disconnected ap-

proaches to valuation. But we can show that, with consistent assumptions, they

give nearly identical answers. We demonstrate this for the perpetual crusher proj-

ect introduced in Section 19.1.

In the following calculations, we ignore any issue costs and concentrate on the

value of interest tax shields. To keep things simple, we assume throughout this sec-

540 PART V

Dividend Policy and Capital Structure

20

Use of APV for international projects was first advocated by D. L. Lessard, “Valuing Foreign Cash

Flows: An Adjusted Present Value Approach,” in D. L. Lessard, ed., International Financial Management:

Theory and Application, Warren, Gorham and Lamont, Boston, MA, 1979.